Key Insights

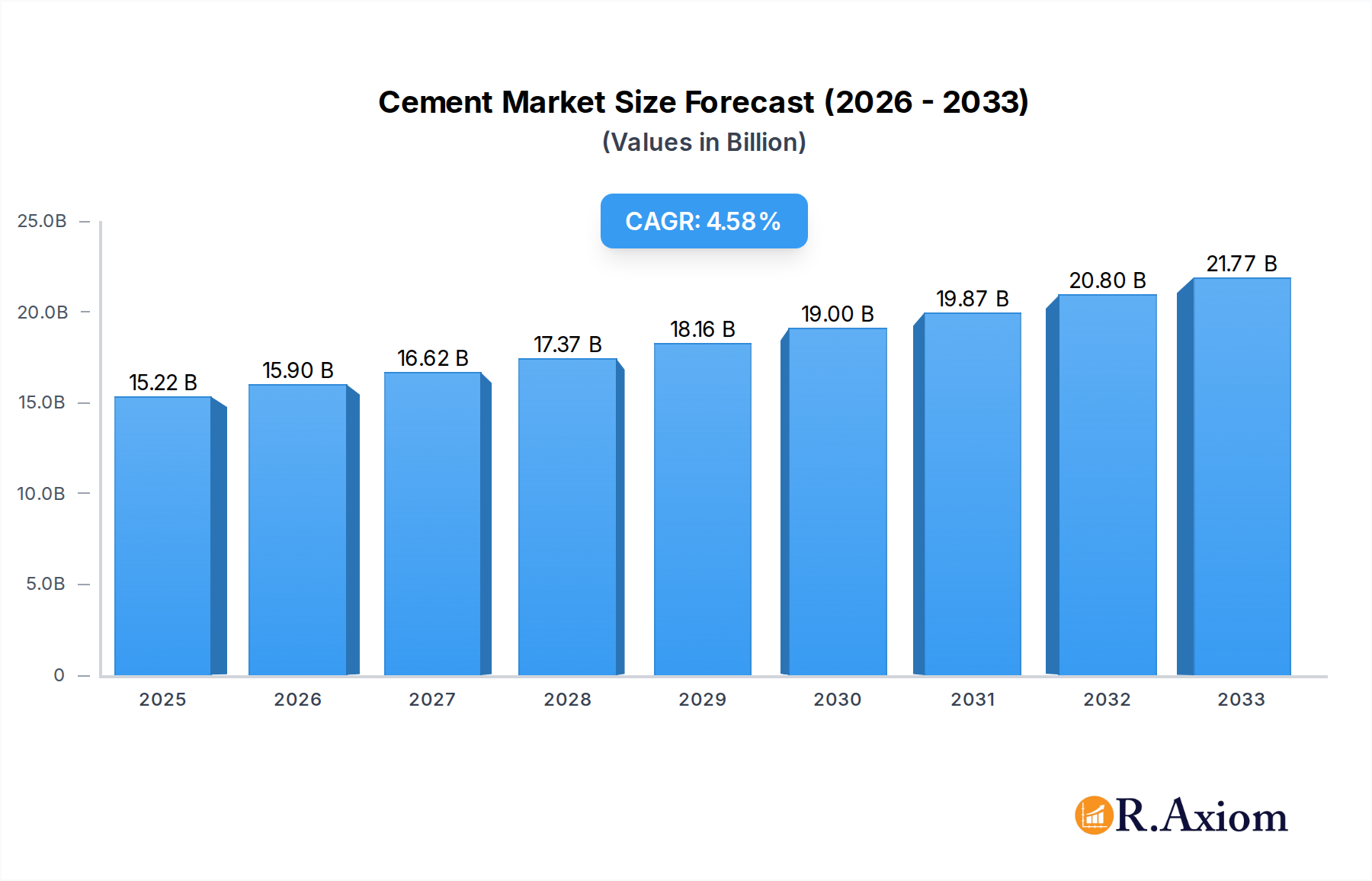

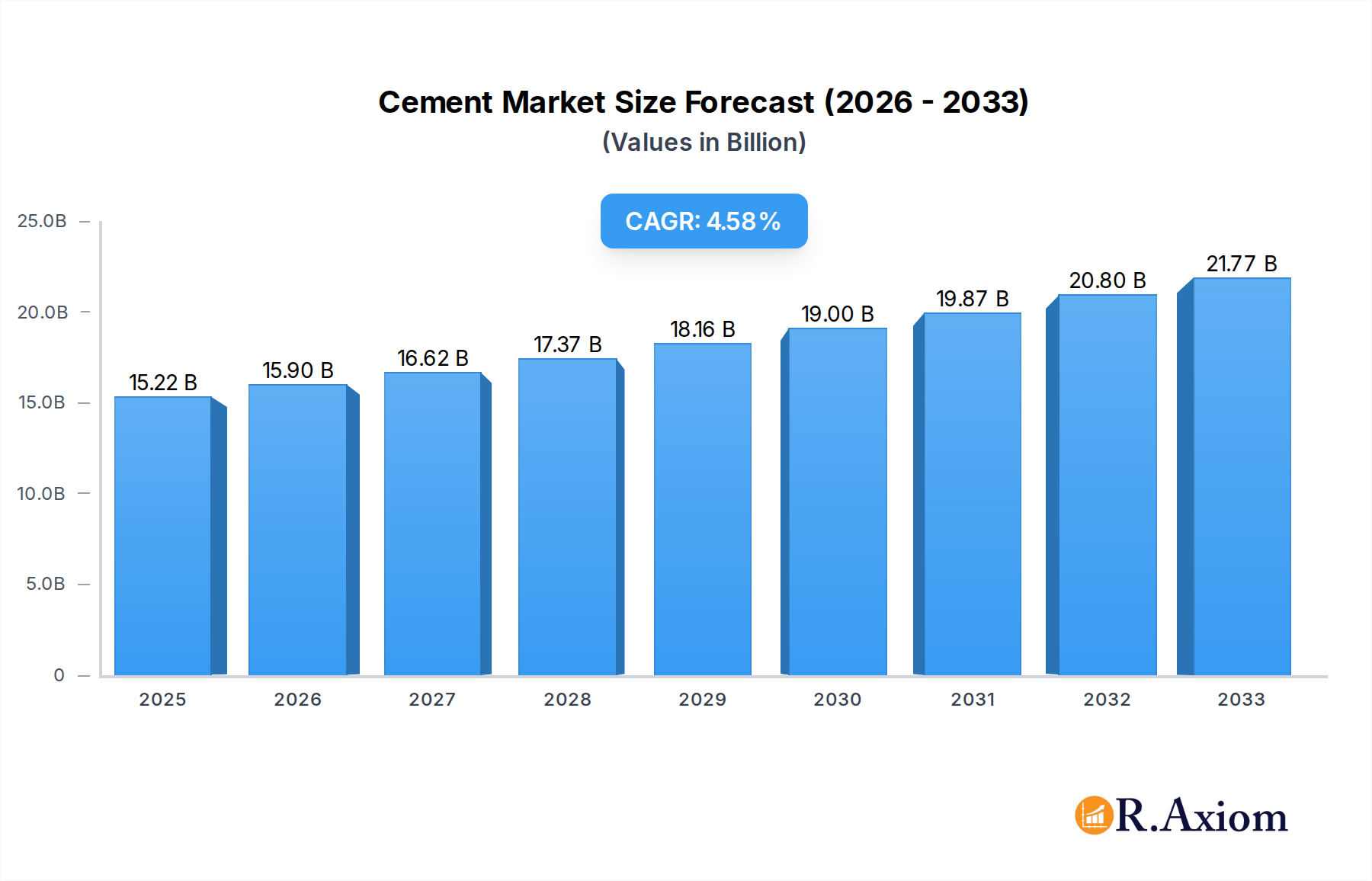

The global cement market is poised for substantial growth, projecting a market size of $15.22 billion in 2025 and an impressive CAGR of 4.5% through 2033. This robust expansion is primarily driven by significant investments in infrastructure development across both developed and emerging economies. The increasing demand for sustainable construction practices and the adoption of eco-friendly cement alternatives are also key growth catalysts. Furthermore, urbanization trends, particularly in the Asia Pacific region, are fueling the demand for residential and commercial construction, thereby boosting cement consumption. The market's diverse applications, ranging from residential buildings to large-scale commercial projects, ensure a broad and consistent demand base. Innovations in cement production, focusing on reducing carbon emissions and enhancing durability, are also contributing to market dynamism and attracting significant investments from leading industry players like CNBM, Anhui Conch Cement, and China Resources Cement Holdings.

Cement Market Size (In Billion)

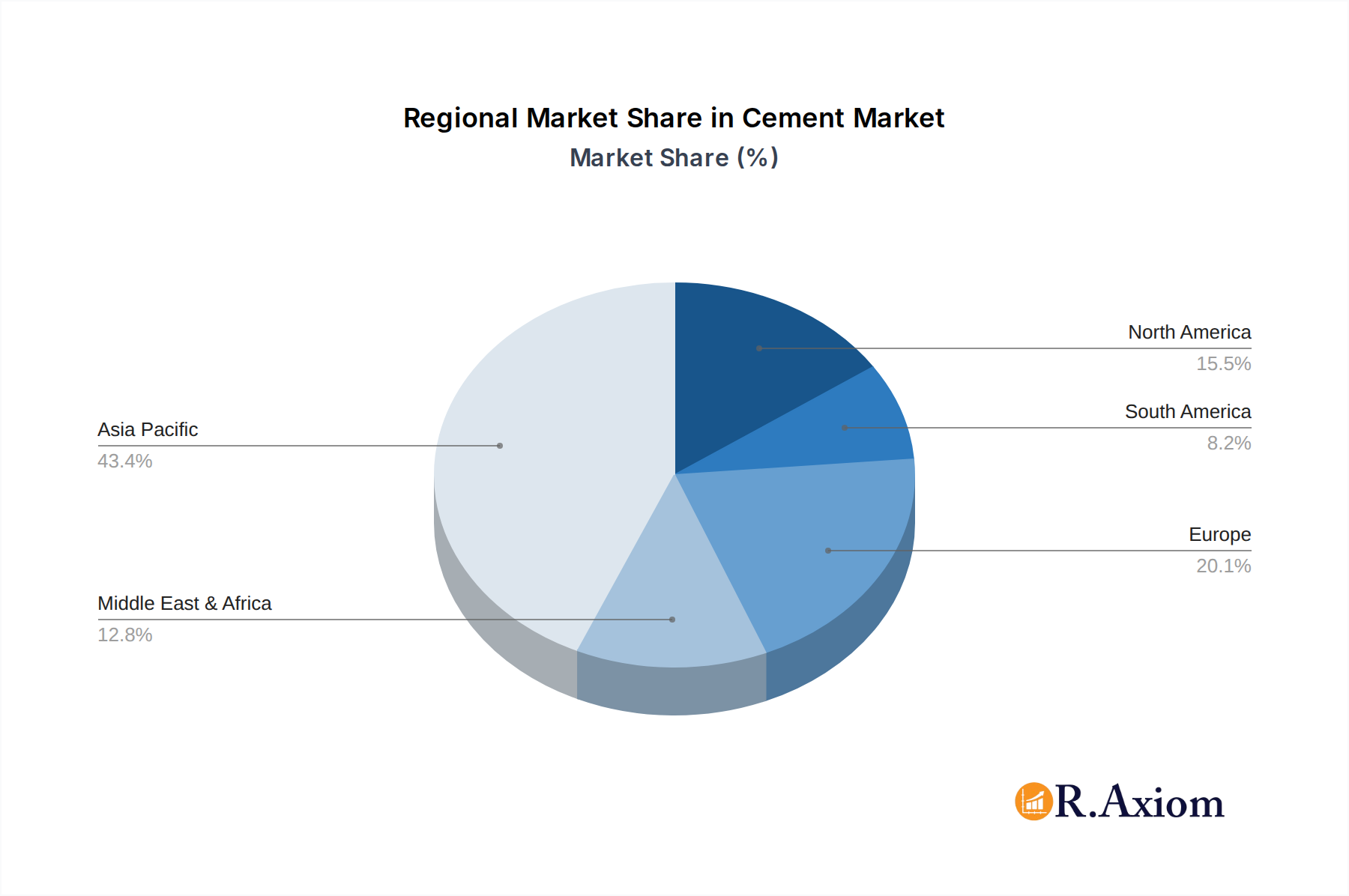

The cement market is characterized by a variety of segments catering to specific construction needs, including Portland cement, white cement, hydraulic cement, and alumina cement. The residential and commercial sectors represent the largest application segments, driven by population growth and economic development. While the market is experiencing a healthy upward trajectory, certain restraints, such as fluctuating raw material prices and stringent environmental regulations, necessitate strategic adaptation from manufacturers. However, the ongoing technological advancements, coupled with favorable government policies promoting construction activities, are expected to outweigh these challenges. The Asia Pacific region, with China and India leading the charge, is anticipated to remain the dominant market, owing to massive infrastructure projects and a burgeoning construction industry. Europe and North America also present significant opportunities, driven by renovation projects and the demand for high-performance and sustainable building materials.

Cement Company Market Share

Cement Market Concentration & Innovation

The global cement market exhibits a dynamic concentration landscape, with major players like CNBM, Anhui Conch Cement, and Tangshan Jidong Cement dominating significant market shares, estimated to be in the tens of billions. While the market is mature in many developed regions, emerging economies continue to drive demand, leading to localized competition and evolving market penetration. Innovation is a critical differentiator, fueled by increasing environmental regulations and the pursuit of sustainable construction materials. Key innovation drivers include the development of low-carbon cements, such as blended cements and alternative binders, alongside advancements in production efficiency and digitalization. Regulatory frameworks, particularly those focused on carbon emissions and energy consumption, are profoundly shaping market dynamics. Product substitutes, though limited in their ability to fully replace cement in core applications, are seeing growth in niche areas, prompting cement manufacturers to enhance their value proposition. End-user trends are increasingly leaning towards durable, sustainable, and aesthetically pleasing construction, influencing product development and marketing strategies. Mergers and acquisitions (M&A) remain a strategic tool for market consolidation and capacity expansion, with deal values often reaching into the billions. For instance, significant M&A activities have been observed among the top tier companies, contributing to the concentration of market power. The drive for innovation and sustainability is reshaping the competitive landscape, pushing companies to invest heavily in research and development to maintain their market position and capture future growth opportunities, particularly in the infrastructure and residential construction sectors.

Cement Industry Trends & Insights

The global cement industry is undergoing a significant transformation, characterized by robust growth driven by urbanization, infrastructure development, and evolving construction practices. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% over the forecast period of 2025-2033, with an estimated market size of over a trillion dollars by 2033. This growth is underpinned by massive investments in infrastructure projects worldwide, including roads, bridges, airports, and public housing, particularly in developing nations. Technological disruptions are playing a pivotal role, with a growing emphasis on sustainable cement production. This includes the adoption of energy-efficient kilns, waste heat recovery systems, and the development of innovative, low-carbon cementitious materials that reduce the industry's environmental footprint. The push towards green building certifications and stringent emission standards is compelling manufacturers to invest in cleaner technologies, impacting operational costs and capital expenditure. Consumer preferences are also shifting, with a greater demand for durable, aesthetically appealing, and environmentally friendly building materials. This has led to increased interest in specialized cements and customized concrete solutions. The competitive dynamics within the industry are intensifying, with both established giants and agile new entrants vying for market share. Companies are increasingly focusing on strategic partnerships, mergers, and acquisitions to gain economies of scale, expand their geographical reach, and acquire new technologies. The digital transformation of the supply chain, from raw material sourcing to logistics and customer delivery, is also a key trend, enhancing efficiency and reducing operational costs. Furthermore, the rise of modular construction and prefabrication techniques is influencing the demand for specific types of cement and admixtures that facilitate faster construction times and higher quality finishes. The industry's ability to adapt to these trends, particularly in embracing sustainable practices and innovative product development, will be crucial for long-term success and market penetration in a rapidly evolving global construction landscape.

Dominant Markets & Segments in Cement

The global cement market's dominance is significantly influenced by a confluence of factors, including economic policies, infrastructure spending, and urbanization rates across various regions. Asia Pacific, particularly China, continues to be the leading market due to its massive infrastructure projects and high construction activity. Within this region, the Residential application segment consistently drives substantial demand, fueled by rapid population growth and increasing disposable incomes, contributing billions to market revenue. The Commercial segment also holds significant importance, driven by the expansion of retail spaces, offices, and hospitality industries, with market penetration reaching high levels.

The Portland Cement type dominates the overall market, accounting for a substantial majority of sales due to its versatility, strength, and widespread application in various construction projects, with market volumes in the billions. Hydraulic Cement is also a crucial segment, essential for underwater construction and structures requiring high resistance to water and sulfates, securing billions in revenue. While White Cement and Alumina Cement represent smaller niche markets, they are critical for specialized applications such as decorative finishes, high-temperature refractory materials, and chemical-resistant structures, each contributing hundreds of millions to the overall market value.

Key drivers for the dominance of these markets and segments include:

- Economic Policies: Government stimulus packages, infrastructure investment plans, and favorable housing policies directly impact cement consumption. For example, China's extensive infrastructure development initiatives have historically propelled cement demand.

- Infrastructure Development: The construction of new roads, bridges, dams, and public transportation systems are primary demand generators for bulk cement. Billions are invested annually in such projects globally.

- Urbanization: The rapid influx of populations into urban centers necessitates extensive construction of residential buildings, commercial complexes, and supporting infrastructure, creating a sustained demand for cement.

- Technological Advancements: Innovations in cement production that enhance strength, durability, and sustainability, such as blended cements and low-carbon alternatives, are gaining traction and influencing market share.

- Regulatory Frameworks: Stricter building codes and environmental regulations, while posing challenges, also drive the demand for higher-quality and specialized cement types.

The interplay of these factors ensures that regions and segments aligned with robust economic growth and significant infrastructure investments will continue to lead the global cement market, with billions in ongoing transactions.

Cement Product Developments

Cement product development is primarily focused on enhancing sustainability and performance. Innovations include the widespread adoption of blended cements, incorporating supplementary cementitious materials like fly ash and slag, to reduce clinker content and lower carbon emissions, contributing to lower costs and environmental benefits worth billions. The development of high-performance concretes (HPCs) and ultra-high-performance concretes (UHPC) offers superior strength, durability, and longevity, catering to demanding infrastructure projects and architectural designs. Furthermore, advancements in self-healing cements and geopolymer cements are addressing long-term structural integrity and environmental concerns, respectively. These product developments are crucial for gaining competitive advantages in a market increasingly driven by green building initiatives and specialized construction needs, with market adoption of these advanced products growing into the hundreds of millions.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the global cement market, encompassing key segments critical to understanding its dynamics. The Application segmentation includes Residential construction, a fundamental driver of demand owing to global population growth and urbanization, with its market size projected to exceed hundreds of billions by 2033. The Commercial segment, encompassing retail, office, and hospitality construction, represents another significant revenue stream, expected to grow into the tens of billions with increased business expansion. In terms of Types, Portland Cement remains the dominant category, forming the backbone of most construction projects, with its market value anticipated to reach trillions. Hydraulic Cement is crucial for infrastructure projects requiring water resistance, holding a market value in the billions. White Cement serves niche markets in decorative and architectural applications, projected to grow into the hundreds of millions, while Alumina Cement is vital for high-temperature and chemically resistant applications, with its market size expected to reach hundreds of millions. Each segment's growth projections and competitive dynamics are thoroughly examined.

Key Drivers of Cement Growth

The cement sector's growth is propelled by a trifecta of technological, economic, and regulatory factors. Economically, burgeoning urbanization worldwide and significant government investments in infrastructure development, such as the construction of high-speed rail networks and smart city projects, are major catalysts, injecting billions into the sector. Technological advancements are driving the demand for advanced cementitious materials with enhanced performance characteristics and reduced environmental impact, leading to innovations in low-carbon cements and durable concrete solutions. Regulatory frameworks, particularly those promoting sustainable construction practices and setting emission reduction targets, are indirectly boosting the market by encouraging the adoption of cleaner production technologies and innovative, eco-friendly cement products. The focus on circular economy principles is also fostering new opportunities in waste utilization for cement production.

Challenges in the Cement Sector

Despite robust growth drivers, the cement sector faces significant challenges. Stringent environmental regulations and increasing pressure to reduce carbon emissions necessitate substantial investments in cleaner technologies, impacting profitability and potentially increasing operational costs by billions for non-compliant facilities. Fluctuations in raw material prices and energy costs create volatility in production expenses, affecting profit margins. Intense competition, especially in mature markets, leads to price wars and reduced profitability. Moreover, logistical complexities in transporting cement, a high-volume, low-value commodity, can escalate costs and impact supply chain efficiency. The long lifespan of cement infrastructure also means that replacement demand is often slow, requiring a consistent pipeline of new construction projects to sustain growth.

Emerging Opportunities in Cement

Emerging opportunities in the cement sector lie in the burgeoning demand for sustainable and innovative building materials. The global push for net-zero construction is creating a market for low-carbon cements, alternative binders, and recycled materials, representing billions in future revenue potential. The growth of prefabricated and modular construction techniques offers opportunities for specialized cement products that facilitate faster assembly and higher quality. Furthermore, advancements in digital technologies, such as AI-powered predictive maintenance and blockchain for supply chain transparency, can enhance operational efficiency and create new service-based revenue streams. The increasing focus on infrastructure resilience in the face of climate change is also driving demand for durable and climate-resilient cementitious materials.

Leading Players in the Cement Market

- CNBM

- Anhui Conch Cement

- Tangshan Jidong Cement

- BBMG

- China Resources Cement Holdings

- Shanshui Cement

- Hongshi Group

- Taiwan Cement

- Tianrui Group Cement

- Asia Cement (China)

- Huaxin Cement

Key Developments in Cement Industry

- 2023 (Q4): Launch of new generation of low-carbon Portland Limestone Cement (PLC) by multiple leading manufacturers, aiming to reduce CO2 emissions by up to 20%.

- 2024 (Q1): Major merger and acquisition activity within the Asian market, consolidating market share for key players and expanding production capacities by billions.

- 2024 (Q2): Increased investment in waste heat recovery systems across European cement plants, enhancing energy efficiency and reducing operational costs.

- 2024 (Q3): Rollout of digital tracking and supply chain management platforms by several multinational cement companies to improve logistics and customer service.

- 2025 (Ongoing): Pilot projects for carbon capture, utilization, and storage (CCUS) technologies in large-scale cement production facilities, with potential to abate millions of tons of CO2 annually.

Strategic Outlook for Cement Market

The strategic outlook for the cement market is overwhelmingly positive, driven by persistent global urbanization and massive infrastructure investments, projected to add trillions to market value. The increasing demand for sustainable building materials presents a significant opportunity for companies that can innovate and adapt to greener production methods and product offerings. Strategic focus on research and development for low-carbon cements, coupled with investments in digitalization for enhanced operational efficiency, will be paramount for sustained growth and competitive advantage. Mergers and acquisitions will continue to play a crucial role in market consolidation and accessing new technologies and markets, shaping the competitive landscape for years to come.

Cement Segmentation

-

1. Application

- 1.1. Residential

- 1.2. Commercial

-

2. Types

- 2.1. Portland Cement

- 2.2. White Cement

- 2.3. Hydraulic Cement

- 2.4. Alumina Cement

Cement Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cement Regional Market Share

Geographic Coverage of Cement

Cement REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Portland Cement

- 5.2.2. White Cement

- 5.2.3. Hydraulic Cement

- 5.2.4. Alumina Cement

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Cement Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Portland Cement

- 6.2.2. White Cement

- 6.2.3. Hydraulic Cement

- 6.2.4. Alumina Cement

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Cement Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Residential

- 7.1.2. Commercial

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Portland Cement

- 7.2.2. White Cement

- 7.2.3. Hydraulic Cement

- 7.2.4. Alumina Cement

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Cement Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Residential

- 8.1.2. Commercial

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Portland Cement

- 8.2.2. White Cement

- 8.2.3. Hydraulic Cement

- 8.2.4. Alumina Cement

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Cement Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Residential

- 9.1.2. Commercial

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Portland Cement

- 9.2.2. White Cement

- 9.2.3. Hydraulic Cement

- 9.2.4. Alumina Cement

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Cement Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Residential

- 10.1.2. Commercial

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Portland Cement

- 10.2.2. White Cement

- 10.2.3. Hydraulic Cement

- 10.2.4. Alumina Cement

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Cement Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Residential

- 11.1.2. Commercial

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Portland Cement

- 11.2.2. White Cement

- 11.2.3. Hydraulic Cement

- 11.2.4. Alumina Cement

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CNBM

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Anhui Conch Cement

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tangshan Jidong Cement

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BBMG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 China Resources Cement Holdings

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Shanshui Cement

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hongshi Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Taiwan Cement

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Tianrui Group Cement

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Asia Cement (China)

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Huaxin Cement

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 CNBM

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cement Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Cement Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Cement Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cement Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Cement Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cement Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Cement Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cement Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Cement Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cement Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Cement Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cement Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Cement Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cement Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Cement Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cement Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Cement Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cement Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Cement Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cement Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cement Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cement Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cement Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cement Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cement Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cement Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Cement Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cement Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Cement Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cement Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Cement Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cement Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Cement Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Cement Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Cement Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Cement Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Cement Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Cement Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Cement Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Cement Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Cement Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Cement Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Cement Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Cement Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Cement Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Cement Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Cement Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Cement Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Cement Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cement Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cement Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cement?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Cement?

Key companies in the market include CNBM, Anhui Conch Cement, Tangshan Jidong Cement, BBMG, China Resources Cement Holdings, Shanshui Cement, Hongshi Group, Taiwan Cement, Tianrui Group Cement, Asia Cement (China), Huaxin Cement.

3. What are the main segments of the Cement?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cement," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cement report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cement?

To stay informed about further developments, trends, and reports in the Cement, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence