Key Insights

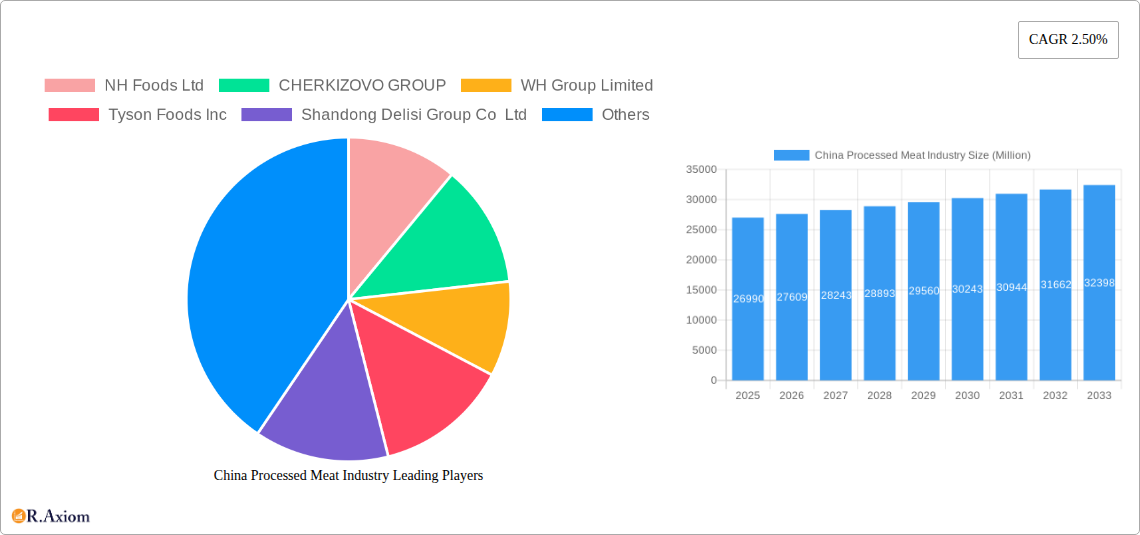

The China processed meat industry, valued at $26.99 billion in 2025, is projected to experience steady growth, driven by several key factors. Rising disposable incomes and urbanization are fueling increased demand for convenient and readily available protein sources, boosting consumption of processed meat products. Changing lifestyles and time constraints are also contributing to the industry's expansion, as consumers opt for processed meats for their ease of preparation and longer shelf life. The market is segmented by distribution channel (supermarkets/hypermarkets, convenience stores, online retailing, others), meat type (poultry, beef, pork, mutton, others), and product type (chilled, frozen, canned/preserved). Poultry and pork are expected to dominate the meat type segment, while supermarkets and hypermarkets remain the largest distribution channel. However, the growing popularity of online grocery shopping is driving significant growth in the e-commerce segment. While the industry faces challenges like fluctuating raw material prices and increasing consumer awareness of health concerns related to processed meat consumption, strategic partnerships, product diversification, and focus on healthier options are likely to mitigate these challenges.

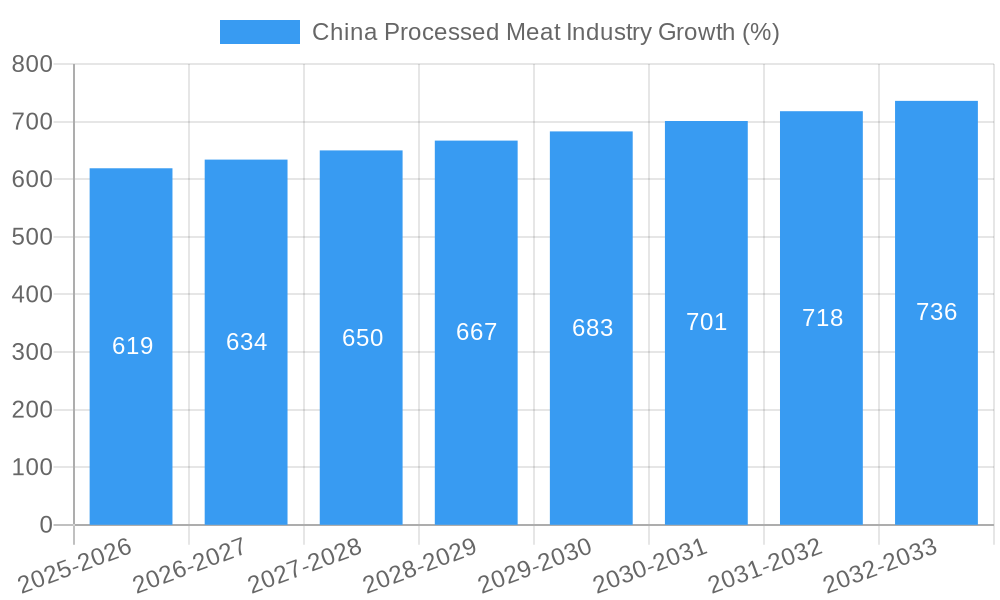

Growth in the sector is expected to continue, albeit at a moderate pace, reflecting the overall maturation of the Chinese market. The 2.50% CAGR suggests a consistent, albeit not explosive, expansion. This sustainable growth is likely supported by continued economic development and a stable population. Competition among major players like NH Foods Ltd, CHERKIZOVO GROUP, and WH Group Limited, along with domestic players like Shandong Delisi Group Co Ltd and China Yurun Food Group Ltd, is intense. These companies are focused on innovation, expanding product lines, and improving distribution networks to maintain market share. The government’s focus on food safety and regulations will also influence the industry's trajectory, pushing companies to adopt higher standards and enhance transparency. Future growth will depend on factors like consumer preferences for healthier options, the effectiveness of marketing campaigns, and sustained economic growth in China.

This comprehensive report provides an in-depth analysis of the China processed meat industry, offering valuable insights for industry stakeholders, investors, and strategic decision-makers. The study period covers 2019-2033, with 2025 as the base and estimated year, and a forecast period of 2025-2033. The historical period analyzed is 2019-2024. The report incorporates data on market size, growth projections, segment-wise analysis, and competitive landscape, utilizing rigorous research methodologies and reliable data sources. The report analyzes key players such as NH Foods Ltd, CHERKIZOVO GROUP, WH Group Limited, Tyson Foods Inc, Shandong Delisi Group Co Ltd, Foster Farms, Hormel Foods Corporation, Zhucheng Waimao Co Ltd, China Xiangtai Food Co Ltd, and China Yurun Food Group Ltd.

China Processed Meat Industry Market Concentration & Innovation

This section analyzes the market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and mergers & acquisitions (M&A) activities within the China processed meat industry. The market is characterized by a combination of large multinational corporations and domestic players, leading to a moderately concentrated market structure. Market share data for key players will be presented, revealing the dominance of specific companies in various segments. The xx Million market value is primarily driven by increasing consumer demand, especially in urban areas, and the growing preference for convenient and ready-to-eat food products.

- Market Concentration: The Herfindahl-Hirschman Index (HHI) will be calculated to quantify market concentration, with detailed analysis of market share held by top players. We anticipate a moderately high concentration level.

- Innovation Drivers: Key innovation drivers include advancements in processing technologies (e.g., automation, improved preservation methods), product diversification (e.g., ready-to-eat meals, value-added products), and sustainable packaging solutions.

- Regulatory Frameworks: Analysis of existing and upcoming food safety regulations, labeling requirements, and environmental standards impacting the industry. The influence of government policies on market growth and investment will be explored.

- Product Substitutes: Examination of competitive pressures from alternative protein sources, such as plant-based meats and insect-based products.

- End-User Trends: Analysis of evolving consumer preferences, including health consciousness, demand for organic and natural products, and increasing reliance on online retail channels.

- M&A Activities: Review of significant M&A deals in the industry, including deal values and their impact on market dynamics. For example, the xx Million acquisition of Mecom Group by Smithfield Foods in 2021 significantly expanded production capacity.

China Processed Meat Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the China processed meat industry. The market is experiencing substantial growth, driven by factors such as rising disposable incomes, urbanization, changing lifestyles, and increasing demand for convenient food options. However, challenges such as fluctuating raw material prices, stringent regulatory requirements, and competition from alternative protein sources also exist. The forecasted Compound Annual Growth Rate (CAGR) for the period 2025-2033 is expected to be xx%, reflecting a strong growth trajectory.

The penetration of processed meat products in various consumer segments will be analyzed, including regional variations in consumption patterns. Technological advancements such as automation and improved packaging technologies are enhancing efficiency and extending product shelf life. Consumer preferences are shifting toward healthier and more convenient options, driving innovation in product development and marketing strategies. Competitive dynamics are intensifying, with both domestic and international players vying for market share. The market penetration of online retail channels is expected to further increase, offering new opportunities for growth and distribution.

Dominant Markets & Segments in China Processed Meat Industry

This section identifies the dominant regions, countries, and segments within the China processed meat industry, based on factors such as market size, growth rate, and consumption patterns. Analysis will include a deep dive into the leading distribution channels (Supermarkets/Hypermarkets, Convenience Stores, Online Retailing, Other Distribution Channels), meat types (Poultry, Beef, Pork, Mutton, Other Meat Types), and product types (Chilled, Frozen, Canned/Preserved).

- Dominant Distribution Channels: Supermarkets/hypermarkets are likely to remain the dominant distribution channel, but online retailing is experiencing rapid growth.

- Dominant Meat Types: Pork is expected to remain the most dominant meat type, followed by poultry. Beef consumption is growing, while mutton holds a smaller but steady market share.

- Dominant Product Types: Frozen and chilled products hold the largest market share due to their convenience and ease of storage. Canned/preserved products cater to a specific segment.

Key Drivers for Dominance:

- Economic policies: Government support for agricultural development and infrastructure investment contributes to the growth of specific segments.

- Infrastructure: Well-developed cold chain logistics infrastructure facilitates the distribution of chilled and frozen products.

- Consumer preferences: Shifting consumer preferences towards convenient, ready-to-eat, and healthier options influence segment growth.

China Processed Meat Industry Product Developments

The China processed meat industry is witnessing significant product innovations, driven by technological advancements and evolving consumer preferences. Companies are focusing on developing healthier options, such as reduced-sodium and low-fat products. Ready-to-eat and convenience-focused products are gaining popularity. Technological innovations in packaging extend shelf life and improve product preservation, enhancing supply chain efficiency. The focus on product differentiation through unique flavors and healthier options is gaining traction, catering to diverse consumer preferences and enhancing market competitiveness.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the China processed meat industry, segmenting the market by distribution channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retailing, Other Distribution Channels), meat type (Poultry, Beef, Pork, Mutton, Other Meat Types), and product type (Chilled, Frozen, Canned/Preserved). Each segment's market size, growth projections, and competitive dynamics are assessed. The analysis includes detailed market forecasts for each segment for the period 2025-2033. Market sizes are predicted in Millions.

Key Drivers of China Processed Meat Industry Growth

The growth of the China processed meat industry is driven by several factors:

- Rising disposable incomes: Increased purchasing power enables consumers to spend more on processed meat products.

- Urbanization: A growing urban population creates higher demand for convenient, ready-to-eat meals.

- Technological advancements: Automation and improved processing technologies enhance efficiency and reduce costs.

- Government support: Policies promoting agricultural development and infrastructure investment support the industry's growth.

Challenges in the China Processed Meat Industry Sector

The China processed meat industry faces several challenges:

- Stringent food safety regulations: Compliance with strict regulations requires significant investment.

- Fluctuating raw material prices: Variations in raw material costs impact profitability.

- Competition from alternative protein sources: Plant-based meats and other alternatives are emerging as competitors.

- Supply chain disruptions: Maintaining efficient and reliable supply chains can be challenging.

Emerging Opportunities in China Processed Meat Industry

The China processed meat industry presents several emerging opportunities:

- Growth of e-commerce: Expanding online retail channels create new opportunities for distribution and sales.

- Demand for healthy and organic products: Consumers are increasingly seeking healthier options, creating demand for products with reduced sodium, fat, and additives.

- Innovation in product development: Development of novel and value-added products can increase market share and profitability.

Leading Players in the China Processed Meat Industry Market

- NH Foods Ltd

- CHERKIZOVO GROUP

- WH Group Limited

- Tyson Foods Inc

- Shandong Delisi Group Co Ltd

- Foster Farms

- Hormel Foods Corporation

- Zhucheng Waimao Co Ltd

- China Xiangtai Food Co Ltd

- China Yurun Food Group Ltd

Key Developments in China Processed Meat Industry Industry

- 2021: Smithfield Foods Inc. acquired Mecom Group, expanding its production of ham, salami, sausages, bacon, and other meat products by 4,000 tonnes per month.

- 2021: Hormel Foods acquired Kraft Heinz snack Planters, diversifying its product portfolio.

Strategic Outlook for China Processed Meat Industry Market

The China processed meat industry is poised for continued growth, driven by rising disposable incomes, urbanization, and evolving consumer preferences. Opportunities exist in the development of healthier and more convenient products, expansion into online retail channels, and strategic alliances and acquisitions. Companies that adapt to changing consumer demands, invest in technological advancements, and maintain efficient supply chains are best positioned for success in this dynamic market. The market is expected to reach xx Million by 2033.

China Processed Meat Industry Segmentation

-

1. Meat Type

- 1.1. Poultry

- 1.2. Beef

- 1.3. Pork

- 1.4. Mutton

- 1.5. Other Meat Types

-

2. Product Type

- 2.1. Chilled

- 2.2. Frozen

- 2.3. Canned/Preserved

-

3. Distribution Channel

- 3.1. Supermarkets/Hypermarkets

- 3.2. Convenience Stores

- 3.3. Online Retailing

- 3.4. Other Distribution Channels

China Processed Meat Industry Segmentation By Geography

- 1. China

China Processed Meat Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing demand for convenient and ready-to-eat food products boosts the processed meat market

- 3.3. Market Restrains

- 3.3.1. Rising health awareness and concerns about the consumption of processed meats

- 3.4. Market Trends

- 3.4.1. Growing trend towards healthier and lower-fat options

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Processed Meat Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Meat Type

- 5.1.1. Poultry

- 5.1.2. Beef

- 5.1.3. Pork

- 5.1.4. Mutton

- 5.1.5. Other Meat Types

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Chilled

- 5.2.2. Frozen

- 5.2.3. Canned/Preserved

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Supermarkets/Hypermarkets

- 5.3.2. Convenience Stores

- 5.3.3. Online Retailing

- 5.3.4. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Meat Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 NH Foods Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 CHERKIZOVO GROUP

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 WH Group Limited

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Tyson Foods Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Shandong Delisi Group Co Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Foster Farms

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Hormel Foods Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Zhucheng Waimao Co Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 China Xiangtai Food Co Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 China Yurun Food Group Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 NH Foods Ltd

List of Figures

- Figure 1: China Processed Meat Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Processed Meat Industry Share (%) by Company 2024

List of Tables

- Table 1: China Processed Meat Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Processed Meat Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 3: China Processed Meat Industry Revenue Million Forecast, by Meat Type 2019 & 2032

- Table 4: China Processed Meat Industry Volume K Tons Forecast, by Meat Type 2019 & 2032

- Table 5: China Processed Meat Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 6: China Processed Meat Industry Volume K Tons Forecast, by Product Type 2019 & 2032

- Table 7: China Processed Meat Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 8: China Processed Meat Industry Volume K Tons Forecast, by Distribution Channel 2019 & 2032

- Table 9: China Processed Meat Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: China Processed Meat Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 11: China Processed Meat Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: China Processed Meat Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 13: China Processed Meat Industry Revenue Million Forecast, by Meat Type 2019 & 2032

- Table 14: China Processed Meat Industry Volume K Tons Forecast, by Meat Type 2019 & 2032

- Table 15: China Processed Meat Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 16: China Processed Meat Industry Volume K Tons Forecast, by Product Type 2019 & 2032

- Table 17: China Processed Meat Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 18: China Processed Meat Industry Volume K Tons Forecast, by Distribution Channel 2019 & 2032

- Table 19: China Processed Meat Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: China Processed Meat Industry Volume K Tons Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Processed Meat Industry?

The projected CAGR is approximately 2.50%.

2. Which companies are prominent players in the China Processed Meat Industry?

Key companies in the market include NH Foods Ltd, CHERKIZOVO GROUP, WH Group Limited, Tyson Foods Inc, Shandong Delisi Group Co Ltd, Foster Farms, Hormel Foods Corporation, Zhucheng Waimao Co Ltd, China Xiangtai Food Co Ltd, China Yurun Food Group Ltd.

3. What are the main segments of the China Processed Meat Industry?

The market segments include Meat Type, Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.99 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing demand for convenient and ready-to-eat food products boosts the processed meat market.

6. What are the notable trends driving market growth?

Growing trend towards healthier and lower-fat options.

7. Are there any restraints impacting market growth?

Rising health awareness and concerns about the consumption of processed meats.

8. Can you provide examples of recent developments in the market?

In 2021, Smithfield Foods Inc. acquired Mecom Group, which is a meat processing company for rising its production in terms of ham, soft salami, dry salami and sausages, bacon, smoked items, and meat products as Mecom Group has two large plants which produce 4,000 tonnes of production per month.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Processed Meat Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Processed Meat Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Processed Meat Industry?

To stay informed about further developments, trends, and reports in the China Processed Meat Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence