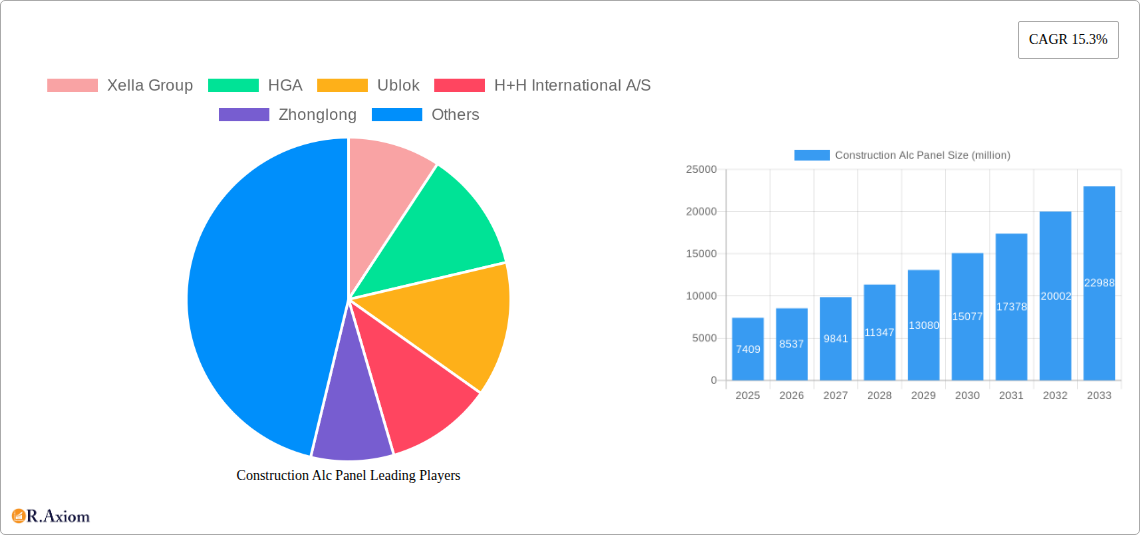

Key Insights

The global market for Autoclaved Aerated Concrete (AAC) panels is experiencing robust growth, projected to reach a significant size with an impressive Compound Annual Growth Rate (CAGR) of 15.3%. This expansion is primarily driven by the increasing demand for lightweight, energy-efficient, and sustainable building materials across various construction sectors. The inherent properties of AAC panels, such as excellent thermal insulation, fire resistance, and acoustic performance, make them an attractive alternative to traditional construction materials. The construction of industrial and commercial buildings, characterized by large-scale projects and a focus on operational efficiency, represents a substantial segment for AAC panels. Simultaneously, the residential building sector is witnessing a growing adoption due to heightened consumer awareness regarding energy savings and environmental impact. The market's value, currently measured in millions, is set to see a substantial increase throughout the forecast period.

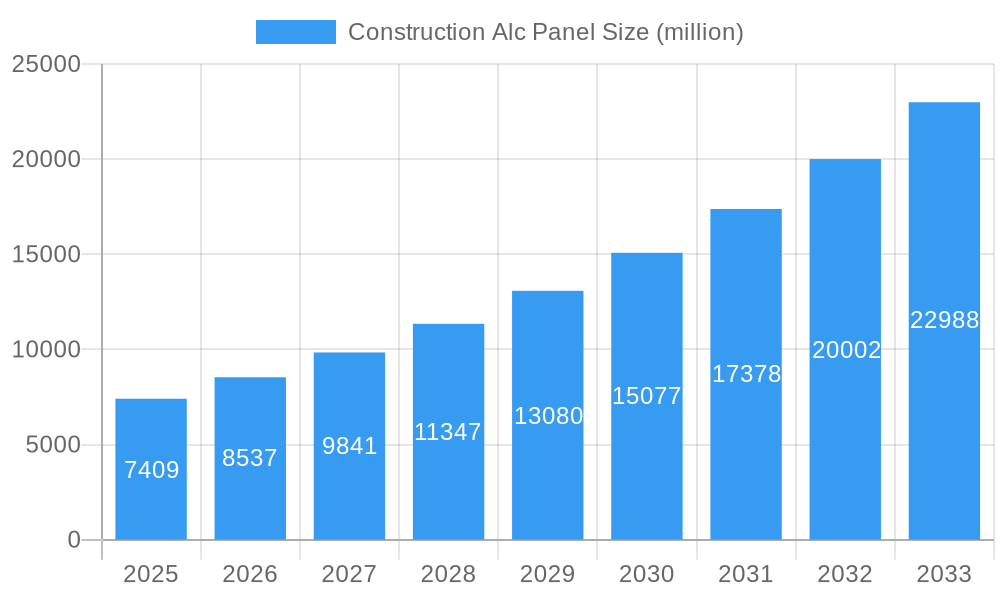

Construction Alc Panel Market Size (In Billion)

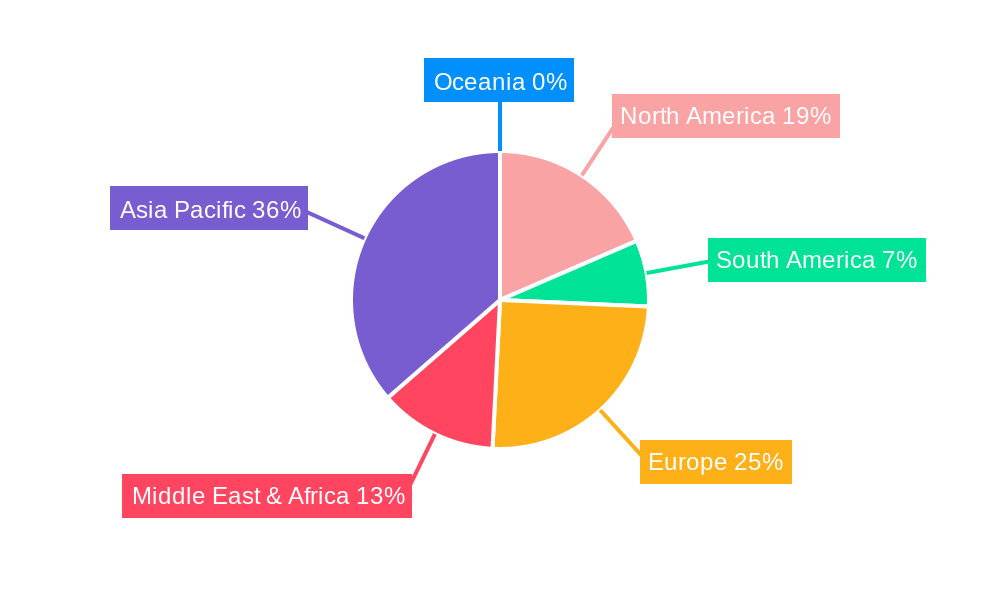

The market is further propelled by advancements in manufacturing technologies and a growing emphasis on green building certifications. Fly ash, a waste product from coal combustion, is increasingly being utilized as a key raw material in AAC panel production, enhancing its sustainability profile and cost-effectiveness. This trend aligns with global initiatives promoting circular economy principles in the construction industry. Key players are actively investing in research and development to improve product performance and expand their geographical reach, contributing to market dynamism. However, challenges such as higher initial costs compared to some conventional materials and the need for specialized handling and installation techniques can pose moderate restraints. Geographically, the Asia Pacific region, particularly China and India, is emerging as a dominant force due to rapid urbanization, infrastructure development, and supportive government policies for sustainable construction. North America and Europe also present significant opportunities driven by stringent building codes and a growing preference for eco-friendly solutions.

Construction Alc Panel Company Market Share

This in-depth report provides a granular analysis of the global Construction AAC (Autoclaved Aerated Concrete) Panel market, offering critical insights for stakeholders seeking to understand market dynamics, growth drivers, and competitive landscapes. Spanning a study period from 2019 to 2033, with a base year of 2025 and a forecast period extending from 2025 to 2033, this report delves into historical trends and future projections. The estimated market size for 2025 is valued at over $10,000 million, with projections indicating significant expansion in the coming years. This comprehensive report utilizes high-traffic keywords relevant to construction materials, building solutions, and sustainable construction to ensure maximum search visibility for industry professionals, investors, and decision-makers.

Construction Alc Panel Market Concentration & Innovation

The global Construction AAC Panel market is characterized by a moderate level of concentration, with a few dominant players holding significant market share, estimated to be over 45% collectively in the base year of 2025. However, the presence of a growing number of regional manufacturers and specialized providers indicates increasing fragmentation and competitive intensity. Innovation within the sector is primarily driven by the demand for energy-efficient and sustainable building materials. Key innovation drivers include advancements in manufacturing processes leading to improved panel strength and insulation properties, the development of composite AAC panels for enhanced performance, and research into more sustainable raw material sourcing. Regulatory frameworks, such as stringent building codes and environmental standards, are playing a crucial role in shaping product development and market adoption. For instance, building performance regulations in North America and Europe are encouraging the use of materials like AAC panels for their superior thermal insulation capabilities, reducing energy consumption in buildings. Product substitutes, including traditional concrete blocks, precast concrete, and insulated metal panels, continue to pose a competitive challenge, though AAC panels are gaining traction due to their unique advantages. End-user trends are increasingly favoring lightweight, durable, and fire-resistant construction materials. The growing emphasis on green building certifications and reduced carbon footprints in construction projects further bolsters the demand for AAC panels. Mergers and acquisitions (M&A) activities, with an estimated total deal value exceeding $500 million in the historical period (2019-2024), are shaping the market structure. These strategic consolidations are aimed at expanding geographical reach, acquiring new technologies, and strengthening product portfolios.

Construction Alc Panel Industry Trends & Insights

The Construction AAC Panel industry is poised for robust growth, driven by several interconnected trends and insights. The global market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 7.2% during the forecast period (2025–2033), indicating a substantial upward trajectory. This growth is underpinned by a confluence of factors, including escalating urbanization, a burgeoning global population, and a continuous need for efficient and sustainable construction solutions. The increasing adoption of AAC panels in various construction segments is a significant market penetration indicator. The industrial sector, for instance, is witnessing a higher demand for AAC panels due to their fast construction capabilities, fire resistance, and load-bearing properties, making them ideal for factory buildings and warehouses where rapid project completion is crucial. Similarly, the commercial building segment benefits from the energy efficiency and design flexibility offered by AAC panels, catering to the evolving needs of office spaces, retail outlets, and hospitality venues seeking to reduce operational costs and enhance occupant comfort. The residential construction sector is also a key contributor, as homeowners and developers increasingly recognize the long-term cost savings associated with the thermal insulation provided by AAC panels, leading to lower heating and cooling expenses.

Technological disruptions are playing a pivotal role in enhancing the competitiveness of AAC panels. Innovations in manufacturing processes, such as the optimization of autoclaving techniques and the refinement of raw material formulations, have led to panels with improved strength-to-weight ratios, enhanced water resistance, and greater dimensional stability. The development of specialized AAC panel systems, including those designed for specific structural applications or offering integrated insulation features, further diversifies the product offering and caters to niche market demands. Furthermore, advancements in digital design and construction technologies, such as Building Information Modeling (BIM), are facilitating the integration of AAC panels into complex architectural designs, streamlining the construction process and reducing material wastage.

Consumer preferences are shifting towards materials that offer a combination of sustainability, performance, and cost-effectiveness. AAC panels align well with these preferences, providing excellent thermal and acoustic insulation, superior fire safety, and a lighter environmental footprint compared to traditional building materials. The growing awareness among end-users about the benefits of energy-efficient buildings and the long-term economic advantages of investing in high-performance materials is a key driver for AAC panel adoption.

The competitive dynamics within the AAC panel market are intensifying. Manufacturers are focusing on product differentiation through innovation, quality improvement, and the development of value-added services. Strategic partnerships and collaborations are becoming more common as companies seek to expand their market reach, access new technologies, and enhance their supply chain efficiencies. The global market penetration of AAC panels, while still nascent in some regions, is steadily increasing, driven by supportive government policies, growing construction activity, and heightened environmental consciousness. The estimated market penetration is projected to reach over 25% in key developed markets by 2033.

Dominant Markets & Segments in Construction Alc Panel

The global Construction AAC Panel market exhibits distinct regional and segmental dominance, driven by economic policies, infrastructure development, and evolving construction practices.

Regional Dominance:

- Asia-Pacific: This region is the largest and fastest-growing market for Construction AAC Panels. Key drivers include:

- Rapid Urbanization and Infrastructure Development: Countries like China and India are experiencing unprecedented urban growth, leading to massive investments in residential, commercial, and industrial infrastructure. This surge in construction activity directly translates to a higher demand for building materials like AAC panels.

- Government Initiatives and Supportive Policies: Many governments in the Asia-Pacific region are actively promoting the use of green building materials and energy-efficient construction techniques through incentives, subsidies, and favorable building codes. For example, initiatives promoting affordable housing and sustainable development in China and Southeast Asian nations are significant growth catalysts.

- Growing Awareness of Sustainable Building: An increasing focus on environmental sustainability and reducing carbon footprints in construction is leading to a greater preference for AAC panels, known for their eco-friendly attributes.

- Economic Growth and Rising Disposable Incomes: The expanding middle class in many Asian countries translates to increased spending on housing and commercial spaces, driving overall construction demand.

- Favorable Manufacturing Landscape: The region boasts a robust manufacturing base for construction materials, enabling cost-effective production and widespread availability of AAC panels. The estimated market share of the Asia-Pacific region is projected to exceed 55% by 2033.

Segmental Dominance:

Application: Residential Building: This segment holds the largest market share within the Construction AAC Panel industry.

- Increasing Demand for Affordable and Energy-Efficient Housing: AAC panels offer excellent thermal insulation, reducing energy bills for homeowners. Their lightweight nature also allows for faster construction, contributing to cost savings.

- Growing Middle Class and Homeownership: Rising disposable incomes and a desire for modern living spaces drive demand for new residential constructions.

- Government Support for Housing Projects: Various government schemes aimed at promoting housing development, especially affordable housing, further fuel the demand for AAC panels. The residential segment is estimated to account for over 40% of the total market application share.

Type: Silica Sand: AAC panels manufactured using silica sand as a primary raw material dominate the market.

- Availability and Cost-Effectiveness: Silica sand is a widely available and relatively inexpensive raw material, making it a preferred choice for large-scale production of AAC panels.

- Proven Performance and Durability: Silica sand-based AAC panels have a long history of successful application, demonstrating excellent strength, fire resistance, and durability.

- Established Manufacturing Processes: The manufacturing processes for silica sand-based AAC are well-established and optimized, contributing to consistent product quality and supply. This type of AAC panel is estimated to hold over 70% of the market by raw material type.

The dominance of these segments and regions underscores the market's trajectory towards sustainable, energy-efficient, and cost-effective construction solutions, driven by economic growth and supportive policies.

Construction Alc Panel Product Developments

Product innovation in Construction AAC Panels is primarily focused on enhancing performance characteristics and expanding application versatility. Recent developments include the introduction of high-strength AAC panels capable of bearing heavier loads, making them suitable for a wider range of structural applications beyond traditional infill. Advances in surface treatments and coatings have also improved water resistance and weatherability, extending the lifespan of AAC panel constructions. Furthermore, manufacturers are developing customized AAC panel solutions tailored for specific needs, such as acoustic insulation panels designed for quieter environments or fire-rated panels that meet stringent safety regulations. These product developments aim to offer competitive advantages by providing superior thermal efficiency, reduced construction time, and improved building aesthetics, meeting the evolving demands of the modern construction industry.

Report Scope & Segmentation Analysis

This report encompasses a comprehensive analysis of the global Construction AAC Panel market, meticulously segmented to provide granular insights. The segmentation covers key applications and raw material types, offering a detailed understanding of market dynamics.

Application: Industrial Building: This segment focuses on the use of AAC panels in manufacturing plants, warehouses, and other industrial facilities. Growth projections for this segment indicate a CAGR of over 6.5% as industries increasingly prioritize rapid construction and energy-efficient operational spaces. Market sizes are estimated to exceed $3,000 million by 2033, with competitive dynamics driven by the demand for fire-resistant and structurally sound solutions.

Application: Commercial Building: This segment analyzes the application of AAC panels in office buildings, retail spaces, and hospitality structures. With an estimated CAGR of over 7.0%, this segment is driven by the demand for sustainable and aesthetically pleasing commercial spaces. Market sizes are projected to surpass $4,000 million by 2033, characterized by competitive efforts to offer customized designs and enhanced thermal comfort.

Application: Residential Building: This segment explores the use of AAC panels in houses, apartments, and multi-family dwellings. Projected to witness a CAGR of over 7.5%, this segment is propelled by the demand for energy-efficient, affordable, and comfortable housing solutions. Market sizes are expected to reach over $5,000 million by 2033, with competitive advantages stemming from cost savings and improved living conditions.

Type: Silica Sand: This segment details the AAC panels predominantly manufactured using silica sand. With an estimated CAGR of around 7.0%, this segment benefits from the material's widespread availability and established performance. Market sizes are projected to be over $8,000 million by 2033, with competitive dynamics revolving around cost-efficiency and consistent product quality.

Type: Fly Ash: This segment examines AAC panels that incorporate fly ash, a byproduct of coal combustion, as a primary or supplementary raw material. This segment is anticipated to grow at a CAGR of over 6.0% as environmental regulations and sustainability initiatives gain momentum. Market sizes are projected to exceed $2,000 million by 2033, with competitive factors including the increasing focus on waste utilization and eco-friendly building materials.

Key Drivers of Construction Alc Panel Growth

The growth of the Construction AAC Panel market is propelled by a multifaceted array of drivers, encompassing technological advancements, economic impetus, and regulatory support. Technologically, the continuous innovation in manufacturing processes leads to improved panel properties such as enhanced insulation, fire resistance, and structural integrity, making them more attractive for modern construction. Economically, rapid urbanization, particularly in developing nations, and the subsequent increase in construction activities for residential, commercial, and industrial sectors, create a substantial demand for efficient building materials. Furthermore, a growing global emphasis on sustainable development and green building initiatives is a significant catalyst. Government policies and building codes that promote energy efficiency and the use of eco-friendly materials directly favor the adoption of AAC panels. The rising awareness among consumers and developers regarding the long-term cost savings associated with energy-efficient structures further bolsters market expansion.

Challenges in the Construction Alc Panel Sector

Despite the robust growth prospects, the Construction AAC Panel sector faces several challenges that could temper its expansion. Regulatory hurdles, such as the need for standardization and acceptance in diverse building codes across different regions, can slow down market penetration. Supply chain complexities, particularly in ensuring the consistent availability of raw materials like silica sand and the efficient distribution of finished products, can lead to price volatility and production delays. Competitive pressures from established building materials like traditional concrete and bricks, which may have lower initial costs, also present a challenge. Additionally, the perceived higher initial investment cost for AAC panels compared to some conventional alternatives can be a barrier for price-sensitive buyers, despite the long-term operational savings. The adoption rate can also be influenced by a lack of awareness or understanding among some segments of the construction industry regarding the benefits and proper installation techniques of AAC panels.

Emerging Opportunities in Construction Alc Panel

The Construction AAC Panel market is ripe with emerging opportunities driven by evolving market demands and technological advancements. The growing global focus on sustainability and net-zero emissions is creating a significant opportunity for AAC panels, which offer superior thermal insulation and a lower carbon footprint compared to conventional materials. The increasing demand for prefabricated and modular construction solutions also presents a growth avenue, as AAC panels are lightweight and easy to handle, making them ideal for off-site manufacturing. Furthermore, the expansion of construction activities in emerging economies, coupled with government support for green building practices, opens up new geographical markets for AAC panel manufacturers. The development of specialized AAC panel systems for specific applications, such as those with enhanced acoustic properties or integrated facade systems, also represents a lucrative opportunity for product diversification and market penetration.

Leading Players in the Construction Alc Panel Market

- Xella Group

- HGA

- Ublok

- H+H International A/S

- Zhonglong

- Changtong

- Lian Hai Yuan Yang

- Nanjing Asahi New Building Materials

- Bauroc

- BBMG

- AKG Gazbeton

- Xinfan Building Materials

- Siporex

- Ecotrend New Building Materials

- Shandong Hailiang

- Shandong Hengrui New Building Materials

Key Developments in Construction Alc Panel Industry

- 2023 May: Xella Group announced a strategic partnership to expand its AAC production capacity in Eastern Europe, aiming to meet growing regional demand.

- 2022 December: H+H International A/S launched a new range of high-performance AAC panels with improved insulation properties, targeting the residential construction market in Northern Europe.

- 2021 August: Bauroc acquired a smaller regional AAC manufacturer in the Baltics, strengthening its market presence and expanding its product portfolio.

- 2020 July: Shandong Hailiang invested in advanced manufacturing technology to enhance the efficiency and sustainability of its AAC panel production.

- 2019 November: Nanjing Asahi New Building Materials introduced an innovative AAC panel system designed for faster installation in commercial buildings.

Strategic Outlook for Construction Alc Panel Market

The strategic outlook for the Construction AAC Panel market is highly optimistic, driven by a convergence of strong market fundamentals and evolving industry trends. The global push towards sustainable construction and energy efficiency will continue to be a primary growth catalyst, favoring AAC panels due to their inherent environmental benefits and superior thermal performance. Increased investments in infrastructure development across emerging economies, coupled with supportive government policies promoting green building, will further fuel market expansion. Manufacturers who focus on product innovation, such as developing panels with enhanced functionalities and exploring new raw material compositions, will be well-positioned to capture market share. Strategic collaborations, mergers, and acquisitions will likely continue as companies seek to consolidate their market positions, gain access to new technologies, and expand their geographical reach. The market is expected to witness a sustained upward trajectory, presenting significant opportunities for stakeholders across the value chain.

Construction Alc Panel Segmentation

-

1. Application

- 1.1. Industrial Building

- 1.2. Commercial Building

- 1.3. Residential Building

-

2. Type

- 2.1. Silica Sand

- 2.2. Fly Ash

Construction Alc Panel Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Construction Alc Panel Regional Market Share

Geographic Coverage of Construction Alc Panel

Construction Alc Panel REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Industrial Building

- 5.1.2. Commercial Building

- 5.1.3. Residential Building

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Silica Sand

- 5.2.2. Fly Ash

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Construction Alc Panel Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Industrial Building

- 6.1.2. Commercial Building

- 6.1.3. Residential Building

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Silica Sand

- 6.2.2. Fly Ash

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Construction Alc Panel Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Industrial Building

- 7.1.2. Commercial Building

- 7.1.3. Residential Building

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Silica Sand

- 7.2.2. Fly Ash

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Construction Alc Panel Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Industrial Building

- 8.1.2. Commercial Building

- 8.1.3. Residential Building

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Silica Sand

- 8.2.2. Fly Ash

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Construction Alc Panel Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Industrial Building

- 9.1.2. Commercial Building

- 9.1.3. Residential Building

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Silica Sand

- 9.2.2. Fly Ash

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Construction Alc Panel Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Industrial Building

- 10.1.2. Commercial Building

- 10.1.3. Residential Building

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Silica Sand

- 10.2.2. Fly Ash

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Construction Alc Panel Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Industrial Building

- 11.1.2. Commercial Building

- 11.1.3. Residential Building

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Silica Sand

- 11.2.2. Fly Ash

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Xella Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 HGA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ublok

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 H+H International A/S

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Zhonglong

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Changtong

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lian Hai Yuan Yang

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Nanjing Asahi New Building Materials

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bauroc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 BBMG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AKG Gazbeton

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Xinfan Building Materials

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Siporex

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ecotrend New Building Materials

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Shandong Hailiang

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Shandong Hengrui New Building Materials

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Xella Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Construction Alc Panel Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Construction Alc Panel Revenue (million), by Application 2025 & 2033

- Figure 3: North America Construction Alc Panel Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Construction Alc Panel Revenue (million), by Type 2025 & 2033

- Figure 5: North America Construction Alc Panel Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Construction Alc Panel Revenue (million), by Country 2025 & 2033

- Figure 7: North America Construction Alc Panel Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Construction Alc Panel Revenue (million), by Application 2025 & 2033

- Figure 9: South America Construction Alc Panel Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Construction Alc Panel Revenue (million), by Type 2025 & 2033

- Figure 11: South America Construction Alc Panel Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Construction Alc Panel Revenue (million), by Country 2025 & 2033

- Figure 13: South America Construction Alc Panel Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Construction Alc Panel Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Construction Alc Panel Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Construction Alc Panel Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Construction Alc Panel Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Construction Alc Panel Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Construction Alc Panel Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Construction Alc Panel Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Construction Alc Panel Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Construction Alc Panel Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Construction Alc Panel Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Construction Alc Panel Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Construction Alc Panel Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Construction Alc Panel Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Construction Alc Panel Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Construction Alc Panel Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Construction Alc Panel Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Construction Alc Panel Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Construction Alc Panel Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Construction Alc Panel Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Construction Alc Panel Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Construction Alc Panel Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Construction Alc Panel Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Construction Alc Panel Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Construction Alc Panel Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Construction Alc Panel Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Construction Alc Panel Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Construction Alc Panel Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Construction Alc Panel Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Construction Alc Panel Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Construction Alc Panel Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Construction Alc Panel Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Construction Alc Panel Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Construction Alc Panel Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Construction Alc Panel Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Construction Alc Panel Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Construction Alc Panel Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Construction Alc Panel Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Construction Alc Panel?

The projected CAGR is approximately 15.3%.

2. Which companies are prominent players in the Construction Alc Panel?

Key companies in the market include Xella Group, HGA, Ublok, H+H International A/S, Zhonglong, Changtong, Lian Hai Yuan Yang, Nanjing Asahi New Building Materials, Bauroc, BBMG, AKG Gazbeton, Xinfan Building Materials, Siporex, Ecotrend New Building Materials, Shandong Hailiang, Shandong Hengrui New Building Materials.

3. What are the main segments of the Construction Alc Panel?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 7409 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Construction Alc Panel," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Construction Alc Panel report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Construction Alc Panel?

To stay informed about further developments, trends, and reports in the Construction Alc Panel, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence