Key Insights

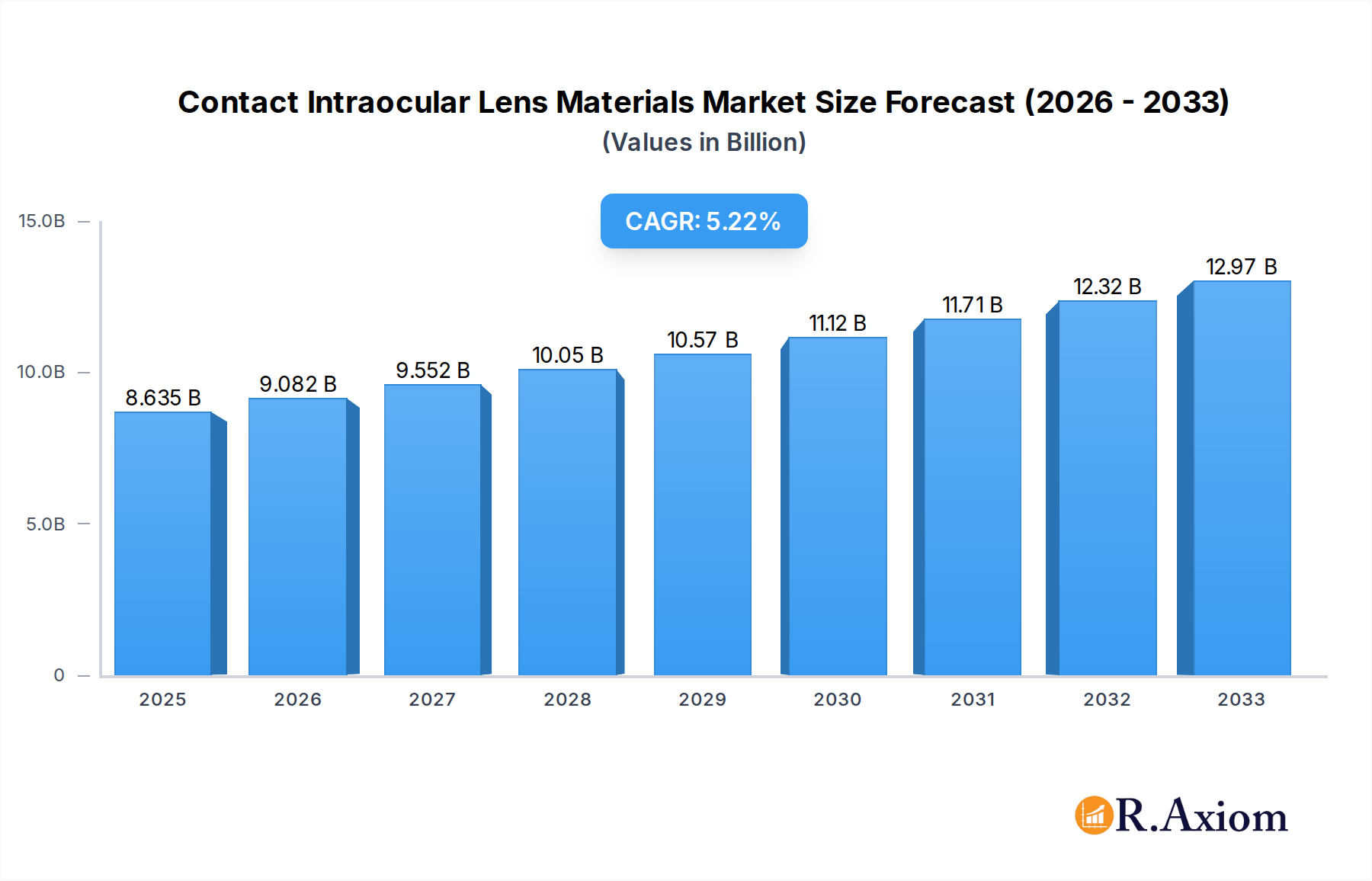

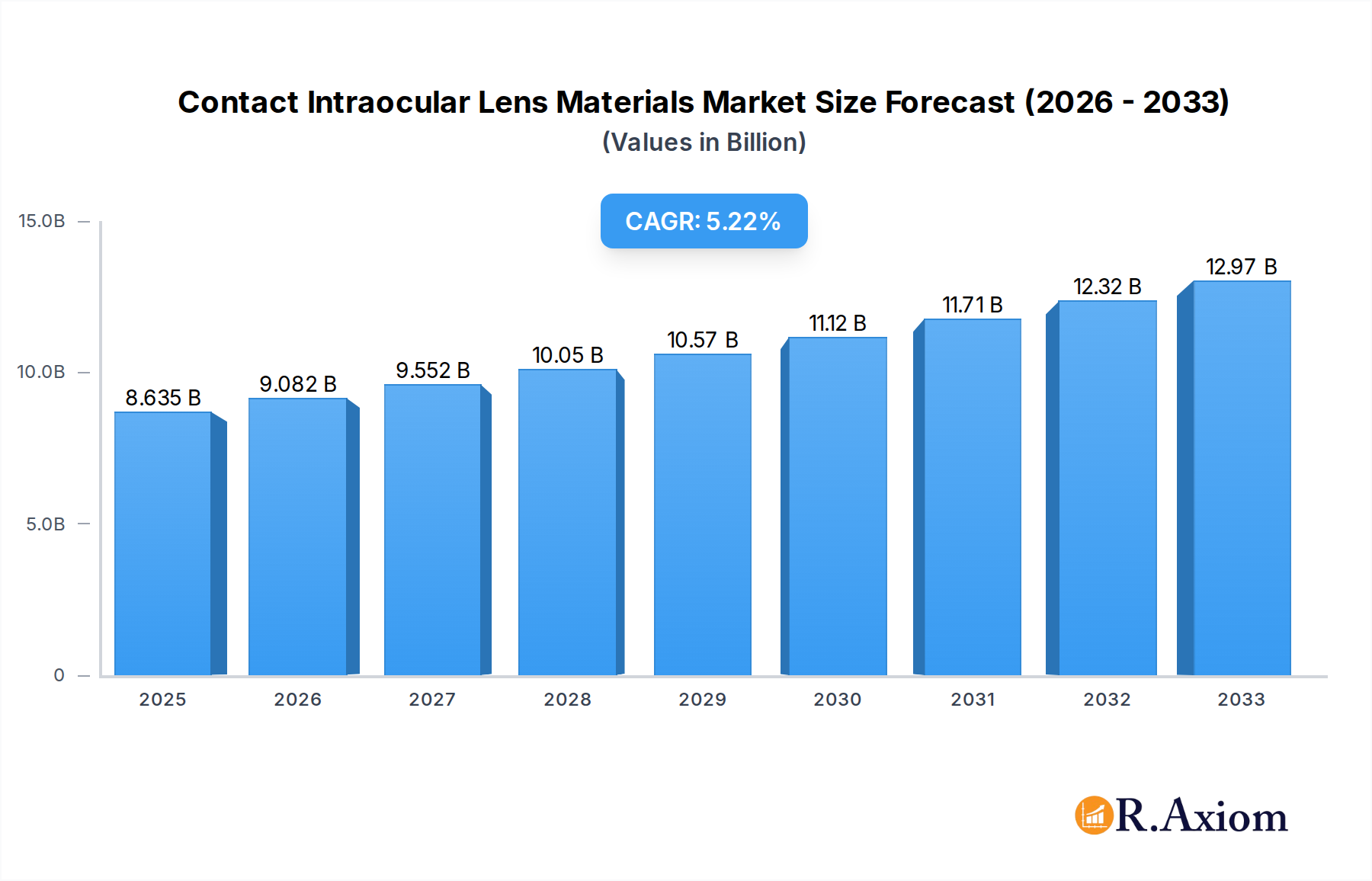

The global Contact and Intraocular Lens Materials market is poised for significant expansion, projected to reach $8635 million by 2025. Driven by an escalating prevalence of eye conditions such as cataracts, refractive errors, and dry eye syndrome, alongside an aging global population, the demand for advanced vision correction solutions is on a steady rise. The market is experiencing a robust Compound Annual Growth Rate (CAGR) of 5.4%, indicating sustained and healthy growth throughout the forecast period. Key market drivers include advancements in material science leading to more biocompatible and comfortable lens materials, increasing disposable incomes enabling greater access to elective vision correction procedures, and a growing awareness among consumers about the benefits of specialized contact lenses and intraocular lens implants for improved quality of life. The continuous innovation in lens technology, particularly in areas like multifocal and toric intraocular lenses and specialized silicone hydrogel contact lenses, is further fueling market penetration.

Contact Intraocular Lens Materials Market Size (In Billion)

The market segmentation reveals diverse opportunities across various applications and material types. Contact lenses, intraocular lenses, and orthokeratology lenses represent significant application segments, each with unique material requirements. Silicone hydrogel and hydrogel materials dominate the contact lens segment due to their superior oxygen permeability and comfort. In the intraocular lens segment, materials like hydrophilic acrylate and fluorosilicone acrylate are gaining traction due to their enhanced optical properties and biocompatibility. Restraints, such as stringent regulatory approvals for new materials and the high cost of advanced lens technologies, are present but are being progressively addressed by market participants through research and development and strategic partnerships. Major players like Contamac, Menicon, and Bausch & Lomb are actively investing in R&D to develop next-generation materials that offer enhanced functionalities, contributing to the overall market dynamism and future growth trajectory.

Contact Intraocular Lens Materials Company Market Share

Contact Intraocular Lens Materials Market Concentration & Innovation

The Contact Intraocular Lens Materials market exhibits moderate to high concentration, driven by significant R&D investments and stringent regulatory approvals. Innovation is primarily fueled by the pursuit of enhanced visual outcomes, biocompatibility, and patient comfort. Key innovation drivers include advancements in polymer science for superior oxygen permeability and reduced protein deposition, as well as the development of novel biomaterials for improved intraocular lens (IOL) performance and extended wear contact lenses. Regulatory frameworks, particularly in North America and Europe, play a crucial role in market access and product differentiation, influencing material certifications and manufacturing standards. Product substitutes, such as refractive surgery, present a constant competitive pressure, necessitating continuous innovation in contact and intraocular lens materials to maintain market share. End-user trends are shifting towards premium, high-performance materials that offer improved wettability, flexibility, and UV protection. Mergers and acquisitions (M&A) activity, while not at an explosive rate, indicates strategic consolidation and expansion by key players seeking to leverage complementary technologies or expand their product portfolios. M&A deal values are projected to reach several hundred million dollars annually as companies look to acquire innovative material technologies or gain market access.

- Market Concentration: Moderate to High

- Key Innovation Drivers:

- Enhanced Oxygen Permeability

- Improved Biocompatibility

- Increased Patient Comfort & Extended Wear

- Reduced Protein Deposition

- Advanced UV Protection

- Regulatory Impact: Strict approvals influencing market entry and product differentiation.

- Competitive Landscape: Driven by continuous innovation against refractive surgery alternatives.

- End-User Preferences: Demand for premium, high-performance materials.

- M&A Activity: Strategic consolidation for technology acquisition and market expansion, with estimated annual deal values in the hundreds of millions of dollars.

Contact Intraocular Lens Materials Industry Trends & Insights

The Contact Intraocular Lens Materials market is poised for robust growth, projected to witness a compound annual growth rate (CAGR) of approximately 6.5% from 2025 to 2033. This expansion is primarily fueled by a confluence of factors including the rapidly aging global population, leading to an increased incidence of cataracts and thus a higher demand for intraocular lenses. Furthermore, the growing prevalence of myopia and hyperopia, coupled with an increasing awareness and adoption of contact lenses for vision correction and cosmetic purposes, significantly contributes to market penetration. Technological advancements are revolutionizing material science, leading to the development of next-generation silicone hydrogel and fluorosilicone acrylate materials that offer superior oxygen transmission rates, enhanced wettability, and improved comfort for extended wear. These material innovations are critical for the success of both daily disposable contact lenses and advanced multifocal or toric intraocular lenses.

The competitive dynamics within the industry are intensifying, with established players investing heavily in research and development to maintain their market edge and newer entrants vying for market share with specialized material solutions. Consumer preferences are increasingly aligning with personalized vision correction solutions, driving demand for materials that can be tailored for specific refractive errors and eye conditions. The orthokeratology segment, in particular, is experiencing significant traction due to its non-surgical approach to myopia management, creating opportunities for specialized lens materials that offer breathability and precise corneal reshaping capabilities. The market penetration of advanced contact lens materials, such as those offering blue light filtering or anti-fog properties, is also on the rise as consumers become more health-conscious and seek lenses that provide additional benefits beyond basic vision correction. The increasing disposable income in emerging economies and the expanding healthcare infrastructure are further supporting market growth by improving access to advanced ophthalmic solutions.

Dominant Markets & Segments in Contact Intraocular Lens Materials

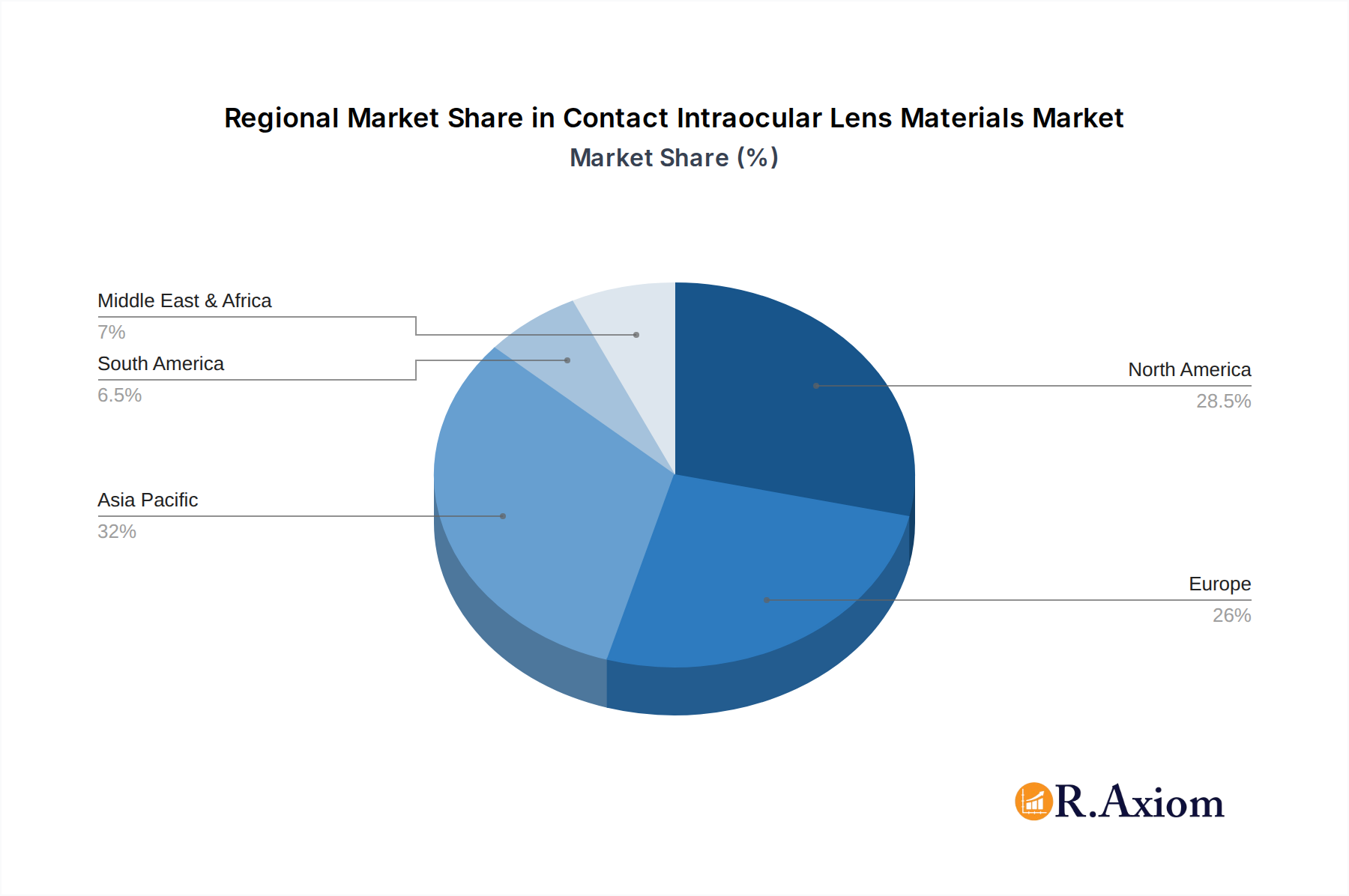

The global Contact Intraocular Lens Materials market is currently dominated by North America, with the United States spearheading regional growth. This dominance is attributable to several key drivers, including a highly developed healthcare infrastructure, strong purchasing power, significant investments in R&D by leading companies, and a high prevalence of age-related eye conditions like cataracts. Government initiatives promoting eye health and the early adoption of advanced ophthalmic technologies further bolster the market's strength in this region.

Application Segmentation Dominance:

- Intraocular Lenses: This segment holds the largest market share, driven by the escalating global incidence of cataracts, particularly among the aging population. The increasing preference for premium multifocal and toric IOLs, which require sophisticated material properties, contributes significantly to this dominance. Economic policies supporting the healthcare sector and advancements in surgical techniques further fuel demand. Market size for IOL materials is estimated at over five thousand million dollars in the base year 2025.

- Contact Lenses: The contact lens segment is experiencing substantial growth, propelled by rising myopia and hyperopia prevalence worldwide, coupled with a growing trend towards daily disposable lenses and cosmetic contact lenses. Advancements in silicone hydrogel and hydrogel materials have enhanced comfort and oxygen permeability, increasing market penetration. The expanding middle class in emerging economies is a key demographic driving growth. Market size for contact lens materials is projected to exceed four thousand million dollars by 2025.

- Orthokeratology Lenses: While a smaller segment, orthokeratology lenses are exhibiting the fastest growth rate. This surge is attributed to the non-surgical nature of myopia management, especially among pediatric populations, and increasing awareness of its benefits. The development of specialized, highly permeable materials is crucial for the success and adoption of these lenses.

Type Segmentation Dominance:

- Silicone Hydrogel: This material type dominates the contact lens market due to its superior oxygen permeability, which allows for extended wear and improved eye health. Its biocompatibility and comfort make it a preferred choice for both daily and reusable lenses. The widespread adoption of silicone hydrogel technology is a testament to its market penetration. Market share for silicone hydrogel materials is estimated at over six thousand million dollars in 2025.

- Hydrogel: Hydrogel materials continue to hold a significant share, particularly in lower-cost contact lenses and as a base for some IOLs, due to their excellent water retention properties and comfort. However, their lower oxygen permeability compared to silicone hydrogels limits their application in extended wear.

- Hydrophobic Acrylate: This segment is crucial for intraocular lenses, offering excellent refractive stability, durability, and a low risk of posterior capsular opacification. The development of hydrophobic acrylic materials with improved optical clarity and handling characteristics is a key focus. Market size for hydrophobic acrylate materials is estimated at over three thousand million dollars in 2025.

- PMMA (Polymethyl Methacrylate): While largely superseded by newer materials in contact lenses, PMMA still holds a niche in some intraocular lens applications, particularly in developing markets due to its cost-effectiveness.

- Hydrophilic Acrylate: These materials offer a balance of water content and flexibility, finding applications in both contact lenses and certain types of IOLs where a softer material is desired.

- Fluorosilicone Acrylate: This advanced material type is gaining traction for its exceptional oxygen permeability, UV blocking capabilities, and resistance to protein and lipid deposits. It is increasingly being incorporated into premium contact lenses and specialized IOLs. Market size for fluorosilicone acrylate materials is estimated at over one thousand million dollars in 2025.

Contact Intraocular Lens Materials Product Developments

Recent product developments in Contact Intraocular Lens Materials are focused on enhancing biocompatibility, improving visual performance, and extending wearability. Innovations include advanced hydrophobic acrylic materials for IOLs that offer superior refractive stability and reduced posterior capsular opacification, as well as the development of next-generation silicone hydrogel and fluorosilicone acrylate materials for contact lenses. These materials boast higher oxygen permeability, improved wettability for enhanced comfort, and built-in UV protection. The introduction of drug-eluting capabilities within IOL materials and contact lens substrates to manage post-operative inflammation or ocular conditions also represents a significant trend, providing a competitive advantage by offering integrated therapeutic benefits.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global Contact Intraocular Lens Materials market, encompassing a detailed segmentation by Application and Type. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033.

Application Segmentation:

- Contact Lenses: This segment includes materials for soft contact lenses (hydrogel, silicone hydrogel) and rigid gas permeable lenses. Growth is driven by increasing myopia and hyperopia prevalence, as well as the demand for daily disposable lenses. Market size for this segment is estimated at four thousand million dollars in 2025.

- Intraocular Lenses: This segment covers materials used in IOLs for cataract surgery, including monofocal, multifocal, and toric lenses. Driven by the aging population and demand for improved visual outcomes. Market size for this segment is projected to reach five thousand million dollars in 2025.

- Orthokeratology Lenses: This niche segment focuses on materials for overnight vision correction lenses. Growth is fueled by the rising trend in myopia management. Market size for this segment is projected to reach five hundred million dollars in 2025.

Type Segmentation:

- Silicone Hydrogel: Dominant in contact lenses due to high oxygen permeability. Market size estimated at six thousand million dollars in 2025.

- Hydrogel: Widely used in soft contact lenses for comfort and water retention. Market size estimated at two thousand million dollars in 2025.

- PMMA: Primarily used in basic IOLs, especially in cost-sensitive markets. Market size estimated at three hundred million dollars in 2025.

- Hydrophilic Acrylate: Offers a balance of properties for contact lenses and some IOLs. Market size estimated at one thousand million dollars in 2025.

- Hydrophobic Acrylate: Crucial for IOLs, providing refractive stability. Market size estimated at three thousand million dollars in 2025.

- Fluorosilicone Acrylate: Advanced material for premium contact lenses and specialized IOLs. Market size estimated at one thousand million dollars in 2025.

- Others: Encompasses novel and emerging materials with specialized properties. Market size estimated at two hundred million dollars in 2025.

Key Drivers of Contact Intraocular Lens Materials Growth

The growth of the Contact Intraocular Lens Materials market is propelled by a confluence of technological, economic, and demographic factors. The rapidly aging global population is a primary driver, leading to an increased incidence of age-related eye conditions such as cataracts, thereby escalating the demand for intraocular lenses. Concurrently, the escalating prevalence of myopia and hyperopia worldwide, coupled with a growing consumer preference for non-surgical vision correction, fuels the demand for advanced contact lenses. Technological advancements in polymer science are enabling the development of novel materials with superior oxygen permeability, enhanced biocompatibility, and improved comfort, facilitating extended wear and better patient outcomes. Furthermore, increasing healthcare expenditure and access to advanced ophthalmic solutions in emerging economies are expanding the market reach and accessibility of these essential materials.

Challenges in the Contact Intraocular Lens Materials Sector

Despite robust growth, the Contact Intraocular Lens Materials sector faces several significant challenges. Stringent regulatory approval processes in major markets, such as those mandated by the FDA and EMA, can lead to lengthy development cycles and substantial R&D costs, acting as a barrier to entry for smaller companies. Fluctuations in raw material prices, particularly for specialized polymers, can impact manufacturing costs and profitability. Moreover, intense competition from established players and the constant threat of substitute technologies, such as advancements in refractive surgery, necessitate continuous innovation and price optimization. Supply chain disruptions, as evidenced by recent global events, can also pose a risk to the consistent availability of critical raw materials and finished products, impacting market stability.

Emerging Opportunities in Contact Intraocular Lens Materials

The Contact Intraocular Lens Materials market is ripe with emerging opportunities, particularly in the realm of personalized vision correction and the integration of advanced functionalities. The growing demand for smart contact lenses capable of continuous intraocular pressure monitoring or drug delivery presents a significant opportunity for material innovation. The expanding market for orthokeratology lenses, driven by increased awareness of myopia management strategies, offers scope for developing specialized, highly breathable materials. Furthermore, the development of bio-integrated materials that promote better cellular integration and reduce immune response in IOLs holds considerable potential. The growing disposable income and improving healthcare infrastructure in emerging economies also represent a vast, untapped market for both conventional and advanced ophthalmic materials.

Leading Players in the Contact Intraocular Lens Materials Market

- Contamac

- Menicon

- Paragon

- Bausch & Lomb

- STAAR Surgical

- Acuity Polymers

- BenQ Materials

- Aishenghua (Suzhou) Optics

- Pharnorcia

Key Developments in Contact Intraocular Lens Materials Industry

- 2024: Launch of next-generation silicone hydrogel materials offering enhanced comfort and oxygen permeability for daily disposable contact lenses.

- 2023: Introduction of advanced hydrophobic acrylic IOL materials with improved optical stability and reduced glare for multifocal lenses.

- 2023: Strategic partnership announced between major material suppliers to develop sustainable and eco-friendly lens materials.

- 2022: Significant investment in R&D for fluorosilicone acrylate materials, focusing on improved UV protection and protein resistance.

- 2021: Acquisition of a specialized polymer manufacturer by a leading IOL company to secure proprietary material technology.

- 2020: Advancements in hydrophilic acrylate formulations for enhanced wettability and reduced dry eye symptoms in contact lens wearers.

- 2019: Introduction of novel PMMA-based IOLs for cost-effective cataract surgery in emerging markets.

Strategic Outlook for Contact Intraocular Lens Materials Market

The strategic outlook for the Contact Intraocular Lens Materials market is overwhelmingly positive, driven by sustained innovation and growing global demand for improved vision correction. Future growth will be characterized by the increasing adoption of advanced materials like fluorosilicone acrylates and specialized hydrogels that offer enhanced performance and patient comfort. The market will also witness a greater integration of digital technologies, leading to the development of "smart" lenses with sensing or therapeutic capabilities. Strategic collaborations between material manufacturers and lens fabricators, along with targeted acquisitions of innovative technologies, will continue to shape the competitive landscape. The expanding healthcare access in emerging economies presents a significant opportunity for market expansion, particularly for cost-effective yet high-performance material solutions. The focus on biocompatibility and sustainability in material development will also be a key differentiator for market leaders.

Contact Intraocular Lens Materials Segmentation

-

1. Application

- 1.1. Contact Lenses

- 1.2. Intraocular Lenses

- 1.3. Orthokeratology Lenses

-

2. Type

- 2.1. Silicone Hydrogel

- 2.2. Hydrogel

- 2.3. PMMA

- 2.4. Hydrophilic Acrylate

- 2.5. Hydrophobic Acrylate

- 2.6. Fluorosilicone Acrylate

- 2.7. Others

Contact Intraocular Lens Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Contact Intraocular Lens Materials Regional Market Share

Geographic Coverage of Contact Intraocular Lens Materials

Contact Intraocular Lens Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Contact Lenses

- 5.1.2. Intraocular Lenses

- 5.1.3. Orthokeratology Lenses

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Silicone Hydrogel

- 5.2.2. Hydrogel

- 5.2.3. PMMA

- 5.2.4. Hydrophilic Acrylate

- 5.2.5. Hydrophobic Acrylate

- 5.2.6. Fluorosilicone Acrylate

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Contact Intraocular Lens Materials Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Contact Lenses

- 6.1.2. Intraocular Lenses

- 6.1.3. Orthokeratology Lenses

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Silicone Hydrogel

- 6.2.2. Hydrogel

- 6.2.3. PMMA

- 6.2.4. Hydrophilic Acrylate

- 6.2.5. Hydrophobic Acrylate

- 6.2.6. Fluorosilicone Acrylate

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Contact Intraocular Lens Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Contact Lenses

- 7.1.2. Intraocular Lenses

- 7.1.3. Orthokeratology Lenses

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Silicone Hydrogel

- 7.2.2. Hydrogel

- 7.2.3. PMMA

- 7.2.4. Hydrophilic Acrylate

- 7.2.5. Hydrophobic Acrylate

- 7.2.6. Fluorosilicone Acrylate

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Contact Intraocular Lens Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Contact Lenses

- 8.1.2. Intraocular Lenses

- 8.1.3. Orthokeratology Lenses

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Silicone Hydrogel

- 8.2.2. Hydrogel

- 8.2.3. PMMA

- 8.2.4. Hydrophilic Acrylate

- 8.2.5. Hydrophobic Acrylate

- 8.2.6. Fluorosilicone Acrylate

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Contact Intraocular Lens Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Contact Lenses

- 9.1.2. Intraocular Lenses

- 9.1.3. Orthokeratology Lenses

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Silicone Hydrogel

- 9.2.2. Hydrogel

- 9.2.3. PMMA

- 9.2.4. Hydrophilic Acrylate

- 9.2.5. Hydrophobic Acrylate

- 9.2.6. Fluorosilicone Acrylate

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Contact Intraocular Lens Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Contact Lenses

- 10.1.2. Intraocular Lenses

- 10.1.3. Orthokeratology Lenses

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Silicone Hydrogel

- 10.2.2. Hydrogel

- 10.2.3. PMMA

- 10.2.4. Hydrophilic Acrylate

- 10.2.5. Hydrophobic Acrylate

- 10.2.6. Fluorosilicone Acrylate

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Contact Intraocular Lens Materials Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Contact Lenses

- 11.1.2. Intraocular Lenses

- 11.1.3. Orthokeratology Lenses

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Silicone Hydrogel

- 11.2.2. Hydrogel

- 11.2.3. PMMA

- 11.2.4. Hydrophilic Acrylate

- 11.2.5. Hydrophobic Acrylate

- 11.2.6. Fluorosilicone Acrylate

- 11.2.7. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Contamac

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Menicon

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Paragon

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bausch & Lomb

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 STAAR Surgical

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Acuity Polymers

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BenQ Materials

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Aishenghua (Suzhou) Optics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Pharnorcia

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Contamac

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Contact Intraocular Lens Materials Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Contact Intraocular Lens Materials Revenue (million), by Application 2025 & 2033

- Figure 3: North America Contact Intraocular Lens Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Contact Intraocular Lens Materials Revenue (million), by Type 2025 & 2033

- Figure 5: North America Contact Intraocular Lens Materials Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Contact Intraocular Lens Materials Revenue (million), by Country 2025 & 2033

- Figure 7: North America Contact Intraocular Lens Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Contact Intraocular Lens Materials Revenue (million), by Application 2025 & 2033

- Figure 9: South America Contact Intraocular Lens Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Contact Intraocular Lens Materials Revenue (million), by Type 2025 & 2033

- Figure 11: South America Contact Intraocular Lens Materials Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Contact Intraocular Lens Materials Revenue (million), by Country 2025 & 2033

- Figure 13: South America Contact Intraocular Lens Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Contact Intraocular Lens Materials Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Contact Intraocular Lens Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Contact Intraocular Lens Materials Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Contact Intraocular Lens Materials Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Contact Intraocular Lens Materials Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Contact Intraocular Lens Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Contact Intraocular Lens Materials Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Contact Intraocular Lens Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Contact Intraocular Lens Materials Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Contact Intraocular Lens Materials Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Contact Intraocular Lens Materials Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Contact Intraocular Lens Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Contact Intraocular Lens Materials Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Contact Intraocular Lens Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Contact Intraocular Lens Materials Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Contact Intraocular Lens Materials Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Contact Intraocular Lens Materials Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Contact Intraocular Lens Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Contact Intraocular Lens Materials Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Contact Intraocular Lens Materials Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Contact Intraocular Lens Materials Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Contact Intraocular Lens Materials Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Contact Intraocular Lens Materials Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Contact Intraocular Lens Materials Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Contact Intraocular Lens Materials Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Contact Intraocular Lens Materials Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Contact Intraocular Lens Materials Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Contact Intraocular Lens Materials Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Contact Intraocular Lens Materials Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Contact Intraocular Lens Materials Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Contact Intraocular Lens Materials Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Contact Intraocular Lens Materials Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Contact Intraocular Lens Materials Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Contact Intraocular Lens Materials Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Contact Intraocular Lens Materials Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Contact Intraocular Lens Materials Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Contact Intraocular Lens Materials Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Contact Intraocular Lens Materials?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the Contact Intraocular Lens Materials?

Key companies in the market include Contamac, Menicon, Paragon, Bausch & Lomb, STAAR Surgical, Acuity Polymers, BenQ Materials, Aishenghua (Suzhou) Optics, Pharnorcia.

3. What are the main segments of the Contact Intraocular Lens Materials?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8635 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Contact Intraocular Lens Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Contact Intraocular Lens Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Contact Intraocular Lens Materials?

To stay informed about further developments, trends, and reports in the Contact Intraocular Lens Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence