Key Insights

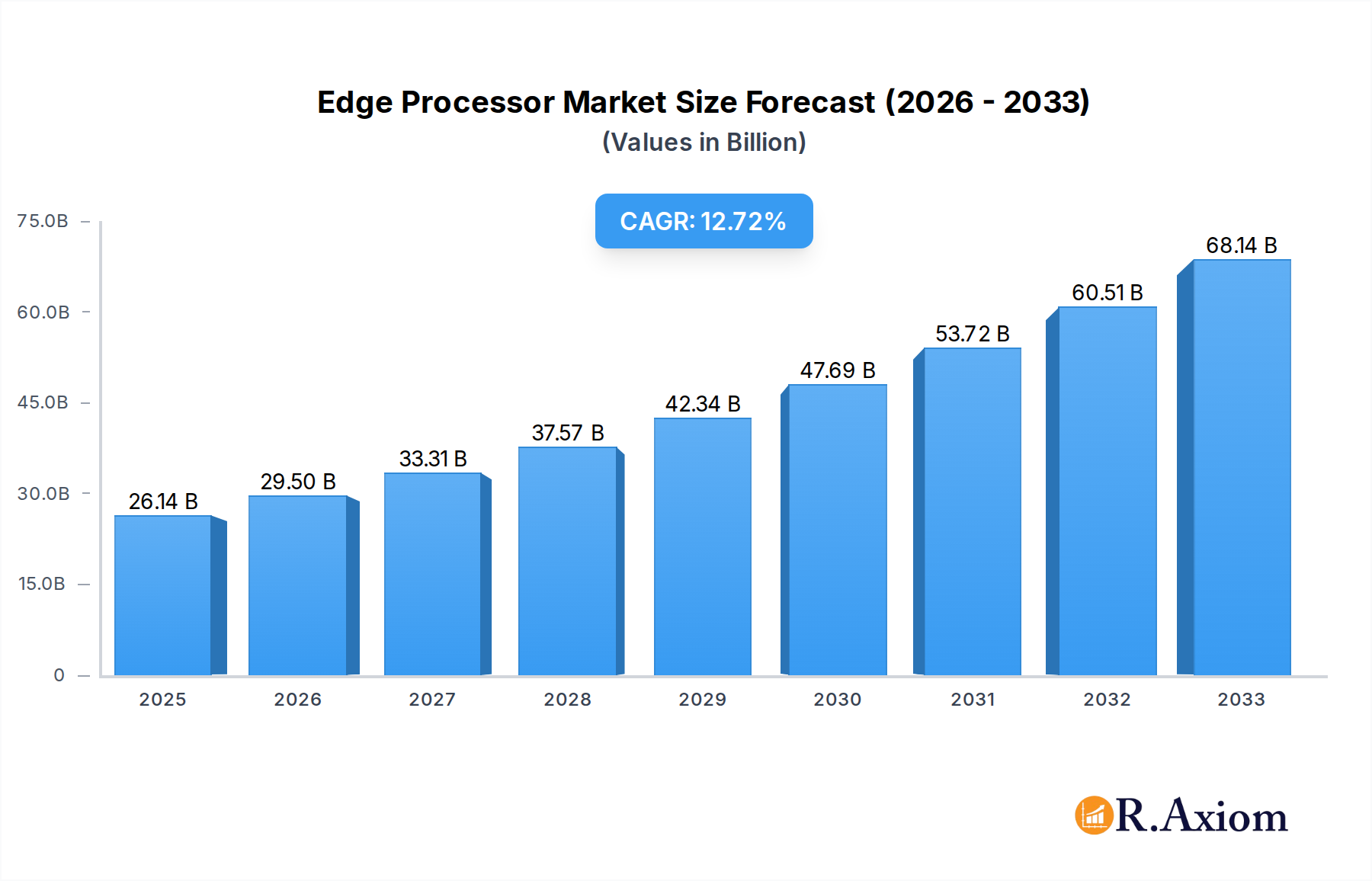

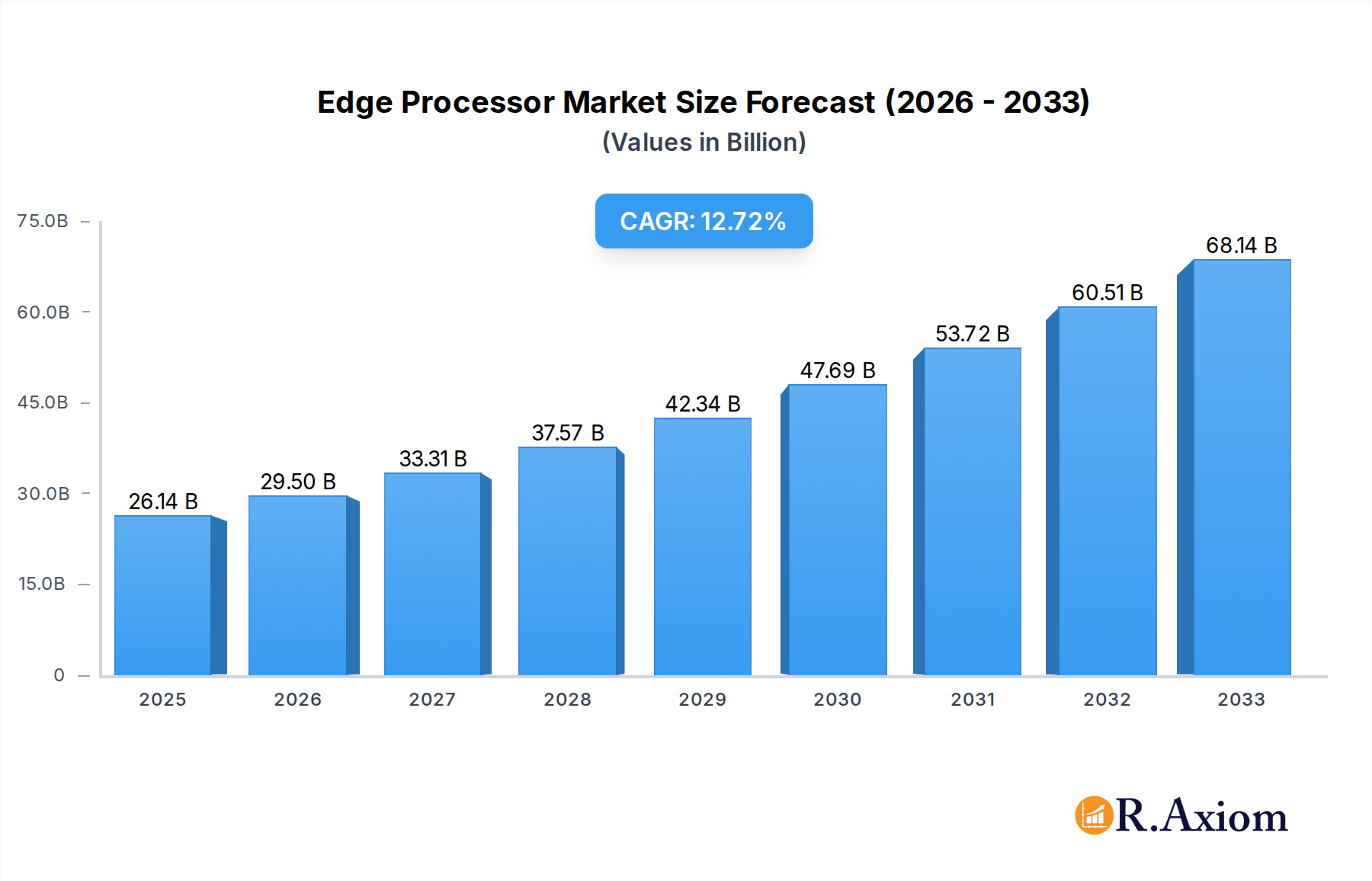

The global Edge Processor market is poised for substantial expansion, projected to reach USD 26.14 billion in 2025 and experience a robust Compound Annual Growth Rate (CAGR) of 12.9% throughout the forecast period of 2025-2033. This remarkable growth is fueled by the escalating demand for real-time data processing and low-latency applications across a multitude of industries. The proliferation of IoT devices, coupled with the increasing adoption of AI and machine learning at the edge, are primary drivers. Sectors such as manufacturing are leveraging edge processors for predictive maintenance and process optimization, while retail benefits from enhanced customer analytics and personalized experiences. The financial services and healthcare industries are embracing edge computing for secure and immediate data handling, and the burgeoning smart cities initiatives are relying on edge processors for efficient management of urban infrastructure and services. The "Others" segment, encompassing emerging applications and niche markets, also contributes significantly to this dynamic growth trajectory.

Edge Processor Market Size (In Billion)

The market is characterized by continuous innovation in processor design, with a strong focus on developing specialized chips like embedding edge computing chips, and integrated solutions combining edge computing processors with 5G and AI capabilities. These advancements are crucial in overcoming the inherent challenges of edge deployments, such as power consumption and processing power limitations. While the market demonstrates immense potential, certain restraints such as the initial investment costs for edge infrastructure and the complexity of managing distributed edge networks need careful consideration. However, the strategic importance of edge processors in enabling advanced functionalities and driving digital transformation across industries ensures their sustained and significant market penetration. Leading technology giants and specialized chip manufacturers are actively investing in research and development, further accelerating market evolution and competitive landscape.

Edge Processor Company Market Share

Edge Processor Market: Comprehensive Growth Analysis & Future Projections (2019-2033)

This in-depth report provides a strategic analysis of the global Edge Processor market, offering critical insights into its evolution, key drivers, and future trajectory. Spanning from 2019 to 2033, with a deep dive into the Base Year 2025 and an extensive Forecast Period of 2025–2033, this research is indispensable for stakeholders seeking to understand market dynamics, competitive landscapes, and emerging opportunities. The study meticulously examines historical trends (2019–2024) to lay the foundation for accurate projections and actionable strategies in a market projected to reach billions in value by 2033.

Edge Processor Market Concentration & Innovation

The global Edge Processor market exhibits a dynamic concentration landscape, characterized by the presence of both established technology giants and innovative specialized players. Key companies like Intel, NVIDIA, and Qualcomm hold significant market shares due to their extensive research and development capabilities, established distribution networks, and robust intellectual property portfolios. Innovation is a primary driver, fueled by the ever-increasing demand for low-latency processing, enhanced security, and AI at the edge. This includes advancements in AI accelerators, power-efficient architectures, and integrated connectivity solutions for 5G and beyond. Regulatory frameworks, while generally supportive of technological advancement, can introduce complexities, particularly concerning data privacy and cross-border data flows, impacting processor design and deployment strategies. Product substitutes, such as cloud-based processing or traditional embedded systems, are being increasingly challenged by the superior performance and real-time capabilities of edge processors. End-user trends are strongly leaning towards decentralized intelligence, enabling applications in industrial IoT, autonomous systems, and smart infrastructure, thus pushing the demand for specialized edge processors. Mergers and acquisitions (M&A) activity is a significant indicator of market consolidation and strategic growth. Recent M&A deals in the edge computing space, valued in the billions, highlight the strategic importance of acquiring specialized technology and talent to bolster competitive positions. For instance, the acquisition of X by Y for an estimated $x billion signals a move towards integrated hardware-software solutions at the edge. The market share distribution is shifting, with increasing influence from companies focusing on specialized AI at the edge and 5G integration.

Edge Processor Industry Trends & Insights

The Edge Processor industry is experiencing a period of unprecedented growth and transformation, driven by a confluence of technological advancements, evolving consumer preferences, and increasing industry adoption. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately xx% over the forecast period, reaching a market size valued in the billions by 2033. This surge is primarily fueled by the escalating demand for real-time data processing, analytics, and decision-making capabilities directly at the data source, bypassing the latency associated with centralized cloud computing. Key growth drivers include the widespread deployment of 5G networks, which enable ultra-low latency and high bandwidth for edge applications, and the proliferation of the Internet of Things (IoT) devices, generating massive amounts of data that require immediate processing. Technological disruptions are a constant, with advancements in AI and machine learning hardware specifically designed for edge deployment, alongside the development of specialized processors for embedded systems and secure edge computing. Consumer preferences are increasingly shaping the market, with a growing expectation for responsive, personalized, and intelligent experiences across various sectors, from smart homes to connected vehicles. This necessitates powerful, energy-efficient processors at the edge. Competitive dynamics are intensifying, with a race to develop more powerful, cost-effective, and application-specific edge processors. Companies are investing heavily in R&D to integrate advanced features like AI accelerators, specialized security modules, and enhanced connectivity options. Market penetration is rapidly increasing across diverse industries, as organizations recognize the tangible benefits of edge processing, including reduced operational costs, improved efficiency, enhanced data security, and new revenue streams. The move towards edge AI, in particular, is transforming industries like manufacturing and healthcare by enabling on-site predictive maintenance, real-time diagnostics, and personalized patient monitoring. The increasing sophistication of edge AI models requires processors capable of handling complex computations locally, driving innovation in specialized AI chip design. Furthermore, the growing adoption of smart city initiatives globally is creating substantial demand for edge processors to manage vast networks of sensors, intelligent traffic systems, and public safety applications. This broad adoption across multiple verticals underscores the fundamental shift towards a more distributed and intelligent computing paradigm.

Dominant Markets & Segments in Edge Processor

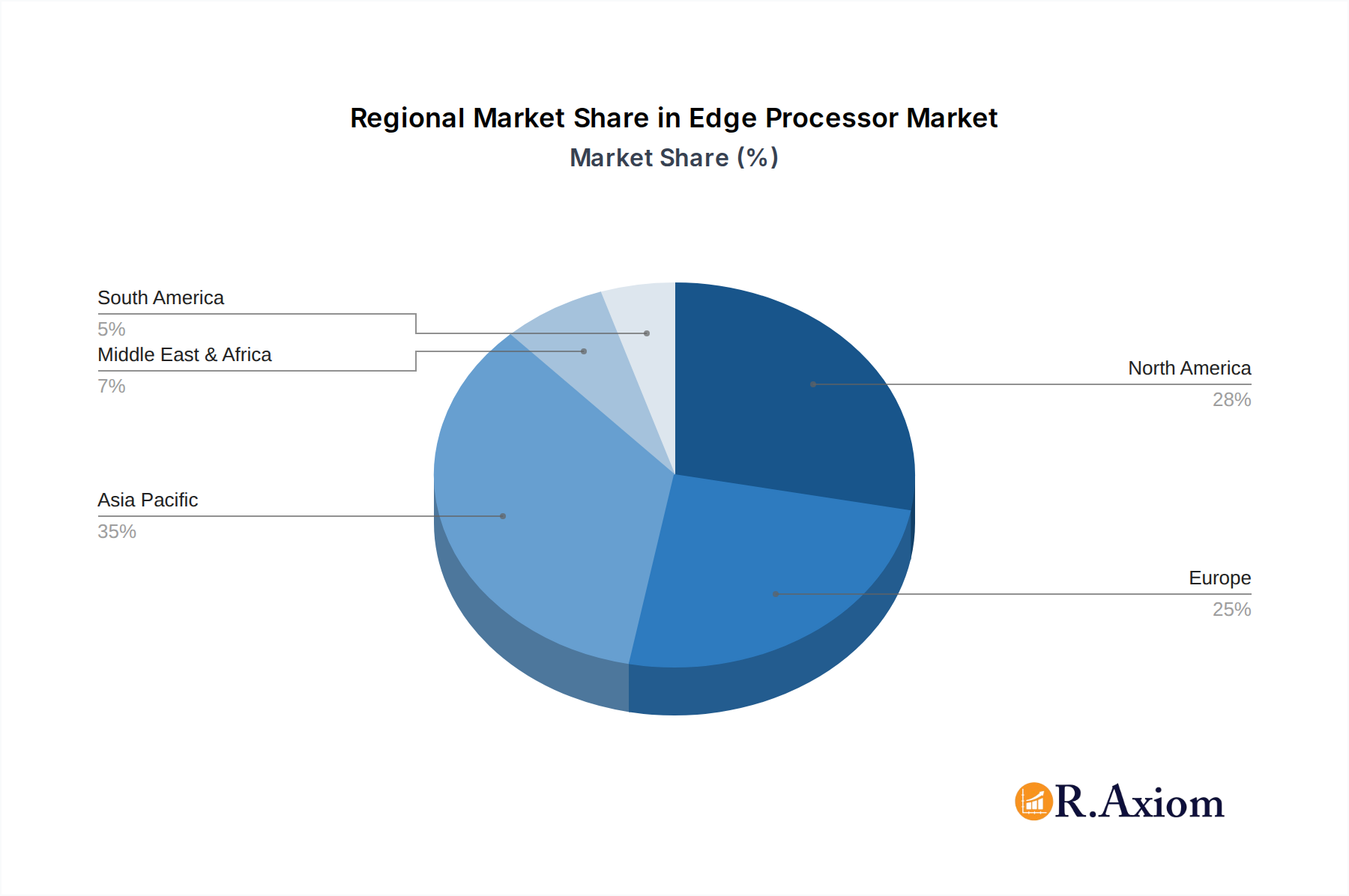

The Edge Processor market's dominance is strategically distributed across key regions and segments, driven by distinct application needs and technological advancements. North America, particularly the United States, stands as a leading region, fueled by significant investments in smart city initiatives, advanced manufacturing, and the burgeoning healthcare technology sector. The United States benefits from a robust innovation ecosystem, a strong presence of major technology companies, and supportive government policies promoting technological adoption. Within the Application segmentation, Manufacturing emerges as a dominant segment, leveraging edge processors for real-time industrial automation, predictive maintenance, and quality control. The ability to process data locally on the factory floor minimizes downtime and optimizes production lines, contributing to significant cost savings and efficiency gains. The Smart Cities segment is rapidly gaining traction, with cities worldwide investing in intelligent infrastructure for traffic management, public safety, and environmental monitoring, all of which heavily rely on edge computing. The Healthcare sector is also a significant contributor, utilizing edge processors for real-time patient monitoring, medical imaging analysis, and remote diagnostics, enhancing patient care and operational efficiency. In terms of Types, Edge computing processors and AI represent a rapidly growing and dominant category. The integration of Artificial Intelligence capabilities directly into edge devices is revolutionizing applications, enabling devices to learn, adapt, and make intelligent decisions locally. This is particularly critical for autonomous systems, computer vision, and natural language processing at the edge. Embedding edge computing chips is another fundamental segment, underpinning the vast array of IoT devices and embedded systems that require localized processing power. Key drivers for this segment include the increasing miniaturization of devices, the demand for low-power consumption, and the need for cost-effective processing solutions. Economic policies in leading nations that encourage technological innovation and digital transformation further bolster the growth of these dominant segments. The increasing deployment of 5G infrastructure also acts as a significant catalyst, enabling new use cases and driving demand for processors capable of handling the enhanced connectivity. The competitive landscape within these dominant segments is characterized by a high level of innovation, with companies continuously striving to offer more powerful, energy-efficient, and specialized solutions to meet the specific demands of each application.

Edge Processor Product Developments

Recent product developments in the Edge Processor market are characterized by a relentless pursuit of higher performance, lower power consumption, and enhanced AI capabilities for embedded applications. Manufacturers are introducing processors with integrated AI accelerators, enabling on-device machine learning for tasks such as image recognition, natural language processing, and anomaly detection. These advancements allow for real-time insights and decision-making at the edge, crucial for industries like autonomous vehicles, smart surveillance, and industrial IoT. Furthermore, there's a strong emphasis on power efficiency, with new architectures designed to optimize performance per watt, extending battery life in mobile and remote deployments. The integration of advanced connectivity features, including support for 5G and Wi-Fi 6, is also a significant trend, facilitating seamless and high-speed data transfer between edge devices and the network. Competitive advantages are being carved out through specialized designs catering to specific market needs, such as ultra-rugged processors for harsh industrial environments or low-latency processors for critical control systems.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Edge Processor market, meticulously segmenting it across key areas to offer granular insights. The segmentation includes: Application: covering Manufacturing, Retail, Banking, Hotel, Healthcare, Smart Cities, and Others. Each application segment is analyzed for its specific demand for edge processing, market size, and growth projections. For instance, the Manufacturing segment is projected to reach $xx billion by 2033, driven by Industry 4.0 initiatives. Types: encompasses Embedding edge computing chips, Edge computing processors and 5G chips, Edge computing processors and AI, and Transceivers for Edge Computing. This detailed breakdown allows for an understanding of the market share and competitive dynamics within each technological category. The Edge computing processors and AI segment, in particular, is expected to witness substantial growth, estimated at xx% CAGR, due to the increasing integration of AI at the edge.

Key Drivers of Edge Processor Growth

The explosive growth of the Edge Processor market is propelled by a synergistic interplay of technological advancements, economic imperatives, and evolving regulatory landscapes. The relentless expansion of the Internet of Things (IoT) ecosystem, generating unprecedented volumes of data at the edge, serves as a primary catalyst. This data deluge necessitates localized processing for immediate insights and action, driving demand for powerful yet energy-efficient edge processors. The widespread deployment of 5G networks is another significant driver, unlocking the potential for ultra-low latency and high-bandwidth applications that are inherently suited for edge computing, such as autonomous vehicles and real-time industrial control. Economic factors like the pursuit of operational efficiency and cost reduction across industries are paramount; edge processing minimizes cloud data transfer costs and improves responsiveness. Furthermore, the increasing demand for enhanced data security and privacy compliance, with sensitive data processed locally rather than transmitted to the cloud, is a strong growth stimulant.

Challenges in the Edge Processor Sector

Despite its robust growth trajectory, the Edge Processor sector faces several formidable challenges that can impede its full potential. Regulatory hurdles, particularly concerning data privacy and security standards across different jurisdictions, can complicate processor design and deployment, requiring adherence to diverse compliance frameworks. Supply chain disruptions, as evidenced by recent global events, pose a significant risk, impacting the availability and cost of essential components for processor manufacturing. Intense competitive pressures among established players and emerging startups can lead to price wars and necessitate continuous, high-stakes R&D investments to maintain market share. The complexity of integrating and managing a distributed network of edge devices and processors also presents a considerable challenge for businesses. Furthermore, the evolving threat landscape necessitates robust security features in edge processors, adding to development costs and complexity.

Emerging Opportunities in Edge Processor

The Edge Processor market is ripe with emerging opportunities, driven by nascent technologies and evolving consumer and industry demands. The accelerating adoption of Artificial Intelligence at the edge is creating substantial demand for specialized AI-powered edge processors, enabling on-device machine learning for a vast array of applications. The continued expansion of smart city initiatives globally presents a significant market for edge processors in intelligent infrastructure, public safety, and environmental monitoring. The growth of the metaverse and augmented/virtual reality (AR/VR) applications will necessitate low-latency, high-performance edge processing for immersive experiences. Furthermore, the increasing focus on sustainability and energy efficiency in computing is opening avenues for low-power, high-performance edge processors in battery-operated devices and remote deployments. The expansion of edge AI in healthcare for remote diagnostics and personalized treatment also offers substantial growth potential.

Leading Players in the Edge Processor Market

- Intel

- NVIDIA

- Qualcomm

- Samsung

- Apple

- Microchip Technology

- Micron

- Huawei

- Kontron

Key Developments in Edge Processor Industry

- 2023 September: NVIDIA announces new Jetson Orin Nano series for scalable edge AI.

- 2023 August: Intel launches new processors optimized for edge computing and AI inference.

- 2023 July: Qualcomm introduces advanced mobile platforms with enhanced edge AI capabilities.

- 2023 June: Apple's M2 Ultra chip demonstrates powerful edge processing capabilities for its ecosystem.

- 2022 December: Samsung unveils next-generation Exynos processors with integrated AI accelerators for edge devices.

- 2022 November: Google introduces new Tensor Processing Units (TPUs) for efficient edge AI workloads.

- 2022 October: Huawei launches its Ascend AI processors, targeting edge computing deployments.

- 2022 September: Microchip Technology expands its microcontroller portfolio for embedded edge applications.

- 2022 August: Micron announces new solutions for edge computing, focusing on memory and storage.

- 2022 July: Kontron introduces ruggedized edge computers for industrial applications.

Strategic Outlook for Edge Processor Market

The strategic outlook for the Edge Processor market is exceptionally positive, characterized by sustained high growth and continuous innovation. The market's trajectory is significantly influenced by the indispensable role edge computing is playing in enabling next-generation technologies like autonomous systems, the metaverse, and advanced IoT deployments. As 5G penetration deepens and AI capabilities become more sophisticated, the demand for powerful, low-latency, and energy-efficient edge processors will only escalate. Strategic investments in R&D focused on specialized AI acceleration, enhanced security features, and power optimization will be crucial for market leaders. Furthermore, strategic partnerships and acquisitions will continue to shape the competitive landscape, fostering integrated hardware and software solutions that address the complex needs of various industry verticals. The ongoing digital transformation across industries, coupled with the increasing volume of data generated at the edge, solidifies the long-term growth potential of the edge processor market.

Edge Processor Segmentation

-

1. Application

- 1.1. Manufacturing

- 1.2. Retail

- 1.3. Banking

- 1.4. Hotel

- 1.5. Healthcare

- 1.6. Smart Cities

- 1.7. Others

-

2. Types

- 2.1. Embedding edge computing chips

- 2.2. Edge computing processors and 5G chips

- 2.3. Edge computing processors and AI

- 2.4. Transceivers for Edge Computing

Edge Processor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Edge Processor Regional Market Share

Geographic Coverage of Edge Processor

Edge Processor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Manufacturing

- 5.1.2. Retail

- 5.1.3. Banking

- 5.1.4. Hotel

- 5.1.5. Healthcare

- 5.1.6. Smart Cities

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Embedding edge computing chips

- 5.2.2. Edge computing processors and 5G chips

- 5.2.3. Edge computing processors and AI

- 5.2.4. Transceivers for Edge Computing

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Edge Processor Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Manufacturing

- 6.1.2. Retail

- 6.1.3. Banking

- 6.1.4. Hotel

- 6.1.5. Healthcare

- 6.1.6. Smart Cities

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Embedding edge computing chips

- 6.2.2. Edge computing processors and 5G chips

- 6.2.3. Edge computing processors and AI

- 6.2.4. Transceivers for Edge Computing

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Edge Processor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Manufacturing

- 7.1.2. Retail

- 7.1.3. Banking

- 7.1.4. Hotel

- 7.1.5. Healthcare

- 7.1.6. Smart Cities

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Embedding edge computing chips

- 7.2.2. Edge computing processors and 5G chips

- 7.2.3. Edge computing processors and AI

- 7.2.4. Transceivers for Edge Computing

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Edge Processor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Manufacturing

- 8.1.2. Retail

- 8.1.3. Banking

- 8.1.4. Hotel

- 8.1.5. Healthcare

- 8.1.6. Smart Cities

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Embedding edge computing chips

- 8.2.2. Edge computing processors and 5G chips

- 8.2.3. Edge computing processors and AI

- 8.2.4. Transceivers for Edge Computing

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Edge Processor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Manufacturing

- 9.1.2. Retail

- 9.1.3. Banking

- 9.1.4. Hotel

- 9.1.5. Healthcare

- 9.1.6. Smart Cities

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Embedding edge computing chips

- 9.2.2. Edge computing processors and 5G chips

- 9.2.3. Edge computing processors and AI

- 9.2.4. Transceivers for Edge Computing

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Edge Processor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Manufacturing

- 10.1.2. Retail

- 10.1.3. Banking

- 10.1.4. Hotel

- 10.1.5. Healthcare

- 10.1.6. Smart Cities

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Embedding edge computing chips

- 10.2.2. Edge computing processors and 5G chips

- 10.2.3. Edge computing processors and AI

- 10.2.4. Transceivers for Edge Computing

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Edge Processor Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Manufacturing

- 11.1.2. Retail

- 11.1.3. Banking

- 11.1.4. Hotel

- 11.1.5. Healthcare

- 11.1.6. Smart Cities

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Embedding edge computing chips

- 11.2.2. Edge computing processors and 5G chips

- 11.2.3. Edge computing processors and AI

- 11.2.4. Transceivers for Edge Computing

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Apple

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Dell

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Google

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Samsung

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Huawei

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Intel

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kontron

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Microchip Technology

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Micron

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 NVIDIA

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Apple

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Edge Processor Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Edge Processor Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Edge Processor Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Edge Processor Volume (K), by Application 2025 & 2033

- Figure 5: North America Edge Processor Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Edge Processor Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Edge Processor Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Edge Processor Volume (K), by Types 2025 & 2033

- Figure 9: North America Edge Processor Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Edge Processor Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Edge Processor Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Edge Processor Volume (K), by Country 2025 & 2033

- Figure 13: North America Edge Processor Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Edge Processor Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Edge Processor Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Edge Processor Volume (K), by Application 2025 & 2033

- Figure 17: South America Edge Processor Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Edge Processor Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Edge Processor Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Edge Processor Volume (K), by Types 2025 & 2033

- Figure 21: South America Edge Processor Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Edge Processor Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Edge Processor Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Edge Processor Volume (K), by Country 2025 & 2033

- Figure 25: South America Edge Processor Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Edge Processor Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Edge Processor Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Edge Processor Volume (K), by Application 2025 & 2033

- Figure 29: Europe Edge Processor Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Edge Processor Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Edge Processor Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Edge Processor Volume (K), by Types 2025 & 2033

- Figure 33: Europe Edge Processor Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Edge Processor Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Edge Processor Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Edge Processor Volume (K), by Country 2025 & 2033

- Figure 37: Europe Edge Processor Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Edge Processor Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Edge Processor Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Edge Processor Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Edge Processor Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Edge Processor Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Edge Processor Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Edge Processor Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Edge Processor Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Edge Processor Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Edge Processor Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Edge Processor Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Edge Processor Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Edge Processor Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Edge Processor Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Edge Processor Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Edge Processor Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Edge Processor Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Edge Processor Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Edge Processor Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Edge Processor Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Edge Processor Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Edge Processor Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Edge Processor Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Edge Processor Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Edge Processor Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Edge Processor Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Edge Processor Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Edge Processor Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Edge Processor Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Edge Processor Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Edge Processor Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Edge Processor Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Edge Processor Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Edge Processor Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Edge Processor Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Edge Processor Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Edge Processor Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Edge Processor Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Edge Processor Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Edge Processor Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Edge Processor Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Edge Processor Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Edge Processor Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Edge Processor Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Edge Processor Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Edge Processor Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Edge Processor Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Edge Processor Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Edge Processor Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Edge Processor Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Edge Processor Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Edge Processor Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Edge Processor Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Edge Processor Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Edge Processor Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Edge Processor Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Edge Processor Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Edge Processor Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Edge Processor Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Edge Processor Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Edge Processor Volume K Forecast, by Country 2020 & 2033

- Table 79: China Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Edge Processor Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Edge Processor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Edge Processor Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Edge Processor?

The projected CAGR is approximately 12.9%.

2. Which companies are prominent players in the Edge Processor?

Key companies in the market include Apple, Dell, Google, Samsung, Huawei, Intel, Kontron, Microchip Technology, Micron, NVIDIA.

3. What are the main segments of the Edge Processor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Edge Processor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Edge Processor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Edge Processor?

To stay informed about further developments, trends, and reports in the Edge Processor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence