Key Insights

The Europe Mandatory Motor Third-Party Liability Insurance Market is projected to experience robust growth, reaching an estimated market size of $76.18 million by 2025, driven by a compound annual growth rate (CAGR) of 7.24% throughout the forecast period. This sustained expansion is primarily fueled by increasingly stringent government regulations mandating third-party liability coverage for all motor vehicles across European nations, alongside a consistent rise in vehicle ownership and road traffic. Key drivers include enhanced public awareness regarding the financial protection offered by this insurance against accident-related damages and injuries to third parties. Furthermore, the growing complexity of vehicle technology and the potential for higher repair costs and medical expenses also contribute to the demand for comprehensive third-party liability coverage. The market is segmented into Bodily Injury Liability and Property Damage Liability, with a notable emphasis on Bodily Injury Liability due to its potentially higher claim values and societal impact.

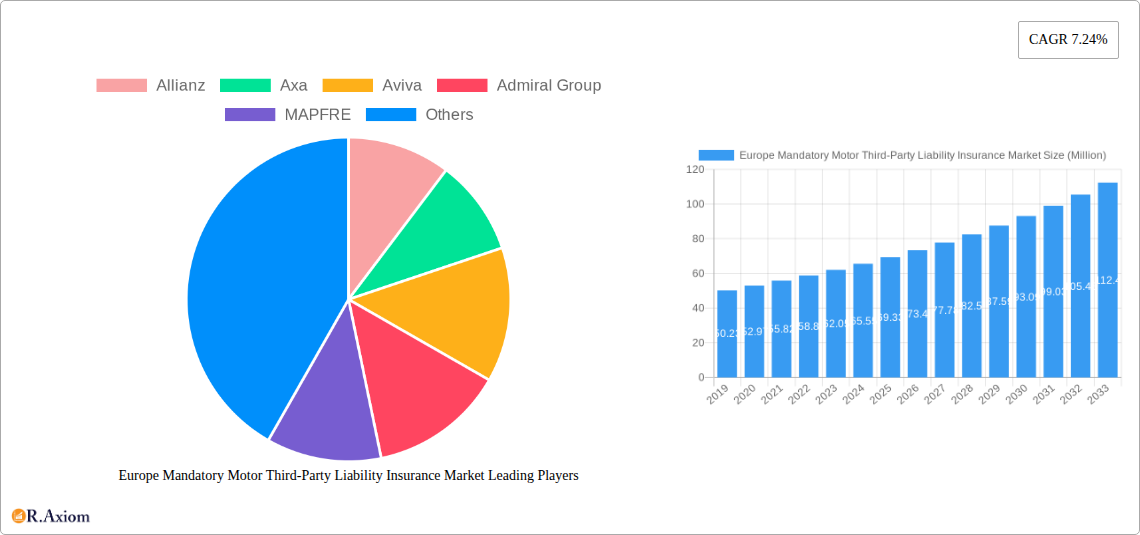

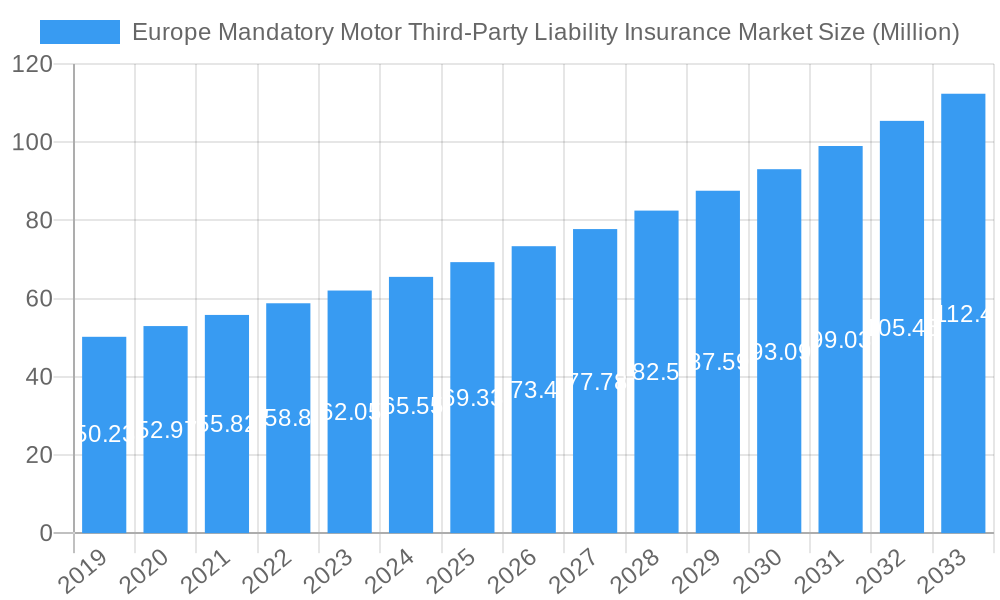

Europe Mandatory Motor Third-Party Liability Insurance Market Market Size (In Million)

The market's growth trajectory is further supported by evolving distribution channels, with direct sales and online platforms gaining traction alongside traditional independent agents and brokers, offering greater accessibility and convenience to consumers. Banks are also playing an increasingly important role by integrating insurance offerings with vehicle financing. The application segment is broadly divided into personal and commercial use, with both segments demonstrating steady demand. While the overall outlook is positive, potential restraints such as intense price competition among insurers and the impact of economic downturns that might reduce disposable income could pose challenges. However, proactive initiatives by regulatory bodies to promote insurance penetration and the continuous development of innovative insurance products are expected to mitigate these risks, ensuring the market's continued upward trend.

Europe Mandatory Motor Third-Party Liability Insurance Market Company Market Share

Europe Mandatory Motor Third-Party Liability Insurance Market: Comprehensive Analysis and Forecasts (2019-2033)

This in-depth market report provides a detailed examination of the Europe Mandatory Motor Third-Party Liability Insurance Market, a critical sector within the automotive and insurance industries. Leveraging comprehensive data from 2019 to 2024, with a robust forecast extending to 2033 and a base year of 2025, this analysis offers invaluable insights for insurers, automotive manufacturers, regulatory bodies, and investment firms. We delve into market concentration, industry trends, dominant segments, product innovations, growth drivers, challenges, and emerging opportunities, alongside a thorough player analysis and a strategic outlook. This report is your definitive guide to navigating the dynamic landscape of mandatory motor insurance in Europe.

Europe Mandatory Motor Third-Party Liability Insurance Market Market Concentration & Innovation

The Europe Mandatory Motor Third-Party Liability Insurance Market exhibits a moderate to high level of market concentration, with a few key players dominating the landscape. Leading entities such as Allianz, Axa, Aviva, Admiral Group, MAPFRE, Chubb Limited, and Generali Group command significant market shares, driven by extensive distribution networks, strong brand recognition, and a broad product portfolio. Innovation in this market is primarily focused on enhancing customer experience, streamlining claims processing, and developing more personalized pricing models. Regulatory frameworks, spearheaded by bodies like BaFin, play a crucial role in shaping market dynamics and ensuring consumer protection. While direct product substitutes are limited due to the mandatory nature of third-party liability insurance, innovations in telematics and Usage-Based Insurance (UBI) are indirectly influencing market behavior by offering more accurate risk assessment. End-user trends are shifting towards digital channels and demand for transparent, competitive pricing. Mergers and acquisitions (M&A) are a significant feature of market consolidation. Notably, in April 2024, Aviva PLC acquired AIG Life Limited for EUR 453 Million (USD 497.95 Million), and in March 2024, Allianz finalized its acquisition of Tua Assicurazioni for EUR 280 Million (USD 307.78 Million), highlighting a trend towards consolidation and expansion by major players. These M&A activities underscore the strategic importance of expanding market reach and product offerings within the European insurance sector.

Europe Mandatory Motor Third-Party Liability Insurance Market Industry Trends & Insights

The Europe Mandatory Motor Third-Party Liability Insurance Market is experiencing robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% between 2025 and 2033. This growth is fueled by increasing vehicle ownership across various European nations and the consistent regulatory mandates requiring third-party liability coverage. Technological disruptions are profoundly reshaping the industry. The integration of telematics and Artificial Intelligence (AI) is enabling insurers to offer more dynamic and personalized premium calculations based on driving behavior, mileage, and risk profiles. This shift towards data-driven underwriting allows for more accurate risk assessment and reduces the potential for fraudulent claims, leading to improved profitability and enhanced customer satisfaction.

Consumer preferences are evolving rapidly, with a growing demand for seamless digital experiences. Customers expect online policy management, instant quotes, and streamlined claims settlement processes. Insurers are investing heavily in digital platforms and mobile applications to cater to these demands. Furthermore, there is an increasing awareness among consumers regarding the importance of adequate third-party liability coverage, especially with rising vehicle repair costs and medical expenses associated with accidents.

The competitive landscape is characterized by intense rivalry among established insurers, complemented by the emergence of InsurTech startups that are challenging traditional models with innovative digital solutions. Key players are focusing on customer retention through superior service, competitive pricing, and value-added services. The market penetration of motor third-party liability insurance remains high across most European countries, as it is a legal requirement for vehicle registration and operation. However, variations exist, with emerging markets showing higher growth potential due to increasing motorization rates. The increasing adoption of electric vehicles (EVs) and autonomous driving technologies presents both challenges and opportunities, requiring insurers to adapt their risk models and product offerings to account for new types of liabilities and repair costs. The ongoing digitalization of the automotive sector, coupled with evolving regulatory landscapes, will continue to drive innovation and shape the competitive dynamics of the Europe Mandatory Motor Third-Party Liability Insurance Market in the coming years.

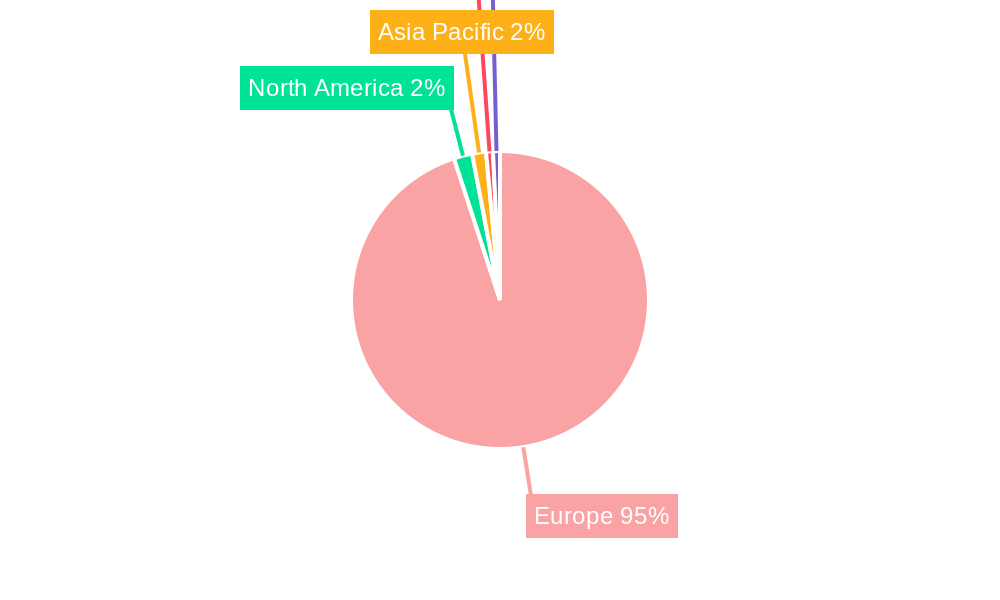

Dominant Markets & Segments in Europe Mandatory Motor Third-Party Liability Insurance Market

The Europe Mandatory Motor Third-Party Liability Insurance Market is characterized by several dominant regions and segments that dictate the overall market trajectory. Germany, France, the United Kingdom, and Italy consistently represent the largest markets due to their significant vehicle fleets and well-established insurance infrastructures.

Dominant Countries:

- Germany: Possesses a large, affluent population with a high vehicle penetration rate. Strict regulatory enforcement and a mature insurance market contribute to its dominance. Economic stability and advanced automotive industry further bolster this position.

- France: Benefits from a substantial number of registered vehicles and a strong emphasis on consumer protection, driving demand for comprehensive third-party liability insurance. Government incentives for new vehicle purchases also contribute to market growth.

- United Kingdom: A highly competitive market with a well-developed insurance sector. Regulatory changes and an increasing focus on customer-centric products drive market evolution. High road traffic density necessitates robust third-party liability coverage.

- Italy: While facing economic fluctuations, Italy maintains a significant vehicle parc. The extensive network of independent agents and brokers plays a crucial role in market penetration. Growing awareness of insurance benefits is a key driver.

Dominant Segments:

- Type: Bodily Injury Liability: This segment consistently holds the largest market share due to the severe financial implications and legal ramifications associated with personal injuries resulting from vehicle accidents. The prioritization of human safety in regulatory frameworks and public consciousness drives its dominance. High compensation payouts for medical expenses, rehabilitation, and lost earnings make this coverage essential.

- Distribution Channel: Independent Agents/Brokers: Despite the rise of direct sales, independent agents and brokers remain a dominant force, particularly in countries like Italy and Germany. Their ability to offer personalized advice, compare multiple insurer options, and build long-term customer relationships is highly valued. Their extensive networks ensure broad market reach and cater to a significant portion of the population seeking expert guidance.

- Application: Personal: The vast majority of motor third-party liability insurance policies are for personal vehicles. This segment is driven by widespread individual car ownership across Europe. Factors such as increasing disposable incomes, demand for personal mobility, and demographic trends in urbanization and suburbanization contribute to its significant market share.

Property Damage Liability, while crucial, typically accounts for a smaller share compared to bodily injury liability due to the often lower average cost of property repairs versus medical expenses and long-term care. The Direct Sales and Banks distribution channels are gaining traction due to digitalization and convenience, but they have yet to surpass the reach and trust associated with traditional intermediaries for complex insurance products. The Commercial application segment, while growing with fleet management and business vehicle use, is still secondary to the overwhelming volume of personal vehicle policies.

Europe Mandatory Motor Third-Party Liability Insurance Market Product Developments

Product developments in the Europe Mandatory Motor Third-Party Liability Insurance Market are increasingly focused on leveraging technology for enhanced risk assessment and customer engagement. Telematics-based policies, offering pay-as-you-drive or pay-how-you-drive options, are gaining traction, allowing for more personalized premiums based on actual usage and driving habits. Insurers are also developing integrated digital platforms that streamline policy acquisition, management, and claims processing, providing a seamless customer experience. Competitive advantages are being built through faster claims settlement, enhanced fraud detection capabilities powered by AI, and the introduction of value-added services such as roadside assistance and accident management. The adaptation of insurance products to accommodate the specific needs of electric vehicles and connected cars represents a significant area of innovation, addressing new risk profiles and repair complexities.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Europe Mandatory Motor Third-Party Liability Insurance Market from 2019 to 2033, with a base year of 2025. The market is segmented by Type into Bodily Injury Liability and Property Damage Liability. Bodily Injury Liability is projected to maintain its leading position due to higher risk and potential claim values. Property Damage Liability, while smaller, is expected to see steady growth.

By Distribution Channel, the market is segmented into Independent Agents/Brokers, Direct Sales, and Banks. Independent Agents/Brokers are expected to continue to hold a significant share, reflecting customer preference for personalized advice, while Direct Sales and Banks are anticipated to grow as digital adoption accelerates.

The Application segmentation includes Personal and Commercial. The Personal segment is expected to dominate due to the larger volume of individual vehicle owners, while the Commercial segment is projected for steady growth driven by evolving business needs and fleet expansion.

Key Drivers of Europe Mandatory Motor Third-Party Liability Insurance Market Growth

Several key factors are driving the growth of the Europe Mandatory Motor Third-Party Liability Insurance Market. Firstly, stringent regulatory mandates across all European nations make third-party liability insurance a legal prerequisite for vehicle operation, ensuring a consistent baseline demand. Secondly, increasing vehicle ownership and motorization rates, particularly in emerging European economies, directly translate to a larger addressable market. Economically, rising disposable incomes enable more consumers to afford insurance premiums. Furthermore, technological advancements, such as telematics and AI, are fostering innovation, leading to more competitive pricing and personalized products that attract a wider customer base. The increasing cost of vehicle repairs and medical treatments also necessitates higher coverage limits, contributing to market value growth.

Challenges in the Europe Mandatory Motor Third-Party Liability Insurance Market Sector

Despite robust growth, the Europe Mandatory Motor Third-Party Liability Insurance Market faces several significant challenges. Intense price competition among insurers, driven by the commoditized nature of the product and the ease of comparison for consumers, puts pressure on profit margins. Evolving regulatory landscapes can also present complexities, with varying requirements and compliance standards across different European countries. The increasing sophistication of vehicle technology, including advanced driver-assistance systems (ADAS) and autonomous driving features, poses challenges in accurately assessing and pricing new risks. Fraudulent claims remain a persistent concern, requiring continuous investment in detection and prevention measures. Additionally, economic uncertainties and fluctuating inflation rates can impact consumer affordability and the cost of claims, creating volatility in the market.

Emerging Opportunities in Europe Mandatory Motor Third-Party Liability Insurance Market

The Europe Mandatory Motor Third-Party Liability Insurance Market presents several promising emerging opportunities. The transition to electric vehicles (EVs) is creating a demand for specialized insurance products that account for battery replacement costs, charging infrastructure risks, and unique repair procedures. The increasing adoption of connected car technology and telematics offers opportunities for data-driven product innovation, including usage-based insurance (UBI) and personalized risk management solutions. The growing demand for digital insurance platforms and seamless customer experiences is paving the way for InsurTech companies and traditional insurers to invest in advanced digital tools and mobile applications. Furthermore, emerging markets within Europe, with increasing vehicle adoption rates and developing insurance sectors, offer significant untapped potential for growth. The focus on sustainability and green mobility also presents opportunities for insurers to develop products that incentivize eco-friendly driving habits.

Leading Players in the Europe Mandatory Motor Third-Party Liability Insurance Market Market

- Allianz

- Axa

- Aviva

- Admiral Group

- MAPFRE

- Chubb Limited

- Generali Group

- BaFin (Regulatory Body, not a direct player)

- Ergo Insurance

- SCOR

Key Developments in Europe Mandatory Motor Third-Party Liability Insurance Market Industry

- April 2024: Aviva PLC ("Aviva") announced the acquisition of AIG Life Limited ("AIG Life UK") from Corebridge Financial Inc., a subsidiary of American International Group Inc. After receiving all requisite approvals, the acquisition was finalized for EUR 453 Million (USD 497.95 Million), significantly expanding Aviva's market presence.

- March 2024: Allianz finalized its acquisition of Tua Assicurazioni in Italy. Allianz SpA confirmed the successful acquisition of Tua Assicurazioni SpA from Assicurazioni Generali SpA. The deal was sealed for EUR 280 Million (USD 307.78 Million). Tua Assicurazioni boasts a robust property and casualty (P/C) insurance portfolio, generating approximately EUR 280 Million (USD 307.78 Million) in gross written premiums in 2022. Notably, this was largely facilitated through its extensive network of nearly 500 agents, indicating a strategic move to bolster Allianz's distribution capabilities and P&C offerings in the Italian market.

Strategic Outlook for Europe Mandatory Motor Third-Party Liability Insurance Market Market

The Europe Mandatory Motor Third-Party Liability Insurance Market is poised for continued expansion, driven by a combination of persistent regulatory requirements and evolving consumer needs. Strategic imperatives for market players will revolve around digital transformation, focusing on enhancing customer journey through intuitive online platforms and mobile applications for policy management and claims. Leveraging telematics and AI for personalized pricing and fraud detection will be crucial for maintaining competitiveness and profitability. Insurers will need to adapt their product portfolios to address the unique risks associated with electric and connected vehicles, potentially unlocking new revenue streams. Consolidation through strategic M&A, as evidenced by recent developments, is likely to continue as companies seek to achieve economies of scale, expand geographic reach, and acquire innovative capabilities. The emphasis on customer-centricity, coupled with efficient claims handling and transparent communication, will be paramount for building customer loyalty and ensuring long-term success in this dynamic market.

Europe Mandatory Motor Third-Party Liability Insurance Market Segmentation

-

1. Type

- 1.1. Bodily Injury Liability

- 1.2. Property Damage Liability

-

2. Distribution Channel

- 2.1. Independent Agents/Brokers

- 2.2. Direct Sales

- 2.3. Banks

-

3. Application

- 3.1. Personal

- 3.2. Commercial

Europe Mandatory Motor Third-Party Liability Insurance Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Mandatory Motor Third-Party Liability Insurance Market Regional Market Share

Geographic Coverage of Europe Mandatory Motor Third-Party Liability Insurance Market

Europe Mandatory Motor Third-Party Liability Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.24% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Bodily Injury Liability

- 5.1.2. Property Damage Liability

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Independent Agents/Brokers

- 5.2.2. Direct Sales

- 5.2.3. Banks

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Personal

- 5.3.2. Commercial

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Mandatory Motor Third-Party Liability Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Bodily Injury Liability

- 6.1.2. Property Damage Liability

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Independent Agents/Brokers

- 6.2.2. Direct Sales

- 6.2.3. Banks

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Personal

- 6.3.2. Commercial

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Allianz

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Axa

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Aviva

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Admiral Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 MAPFRE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Chubb Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Generali Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BaFin

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ergo Insurance

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 SCOR**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Allianz

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Mandatory Motor Third-Party Liability Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Type 2020 & 2033

- Table 3: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Application 2020 & 2033

- Table 7: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Type 2020 & 2033

- Table 11: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 12: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 13: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Application 2020 & 2033

- Table 15: Europe Mandatory Motor Third-Party Liability Insurance Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Europe Mandatory Motor Third-Party Liability Insurance Market Volume Billion Forecast, by Country 2020 & 2033

- Table 17: United Kingdom Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United Kingdom Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Germany Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: France Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: France Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Italy Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Spain Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Spain Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: Netherlands Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Netherlands Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Belgium Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Belgium Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Sweden Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Sweden Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Norway Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Norway Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Poland Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Poland Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 37: Denmark Europe Mandatory Motor Third-Party Liability Insurance Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Denmark Europe Mandatory Motor Third-Party Liability Insurance Market Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Mandatory Motor Third-Party Liability Insurance Market?

The projected CAGR is approximately 7.24%.

2. Which companies are prominent players in the Europe Mandatory Motor Third-Party Liability Insurance Market?

Key companies in the market include Allianz, Axa, Aviva, Admiral Group, MAPFRE, Chubb Limited, Generali Group, BaFin, Ergo Insurance, SCOR**List Not Exhaustive.

3. What are the main segments of the Europe Mandatory Motor Third-Party Liability Insurance Market?

The market segments include Type, Distribution Channel, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 76.18 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Ownership.

6. What are the notable trends driving market growth?

Increasing Number of Vehicles on the Road to Drive Market Growth.

7. Are there any restraints impacting market growth?

Increasing Vehicle Ownership.

8. Can you provide examples of recent developments in the market?

April 2024: Aviva PLC ("Aviva") announced the acquisition of AIG Life Limited ("AIG Life UK") from Corebridge Financial Inc., a subsidiary of American International Group Inc. After receiving all requisite approvals, the acquisition was finalized for EUR 453 million (USD 497.95 million).March 2024: Allianz finalized its acquisition of Tua Assicurazioni in Italy. Allianz SpA confirmed the successful acquisition of Tua Assicurazioni SpA from Assicurazioni Generali SpA. The deal was sealed for EUR 280 million (USD 307.78 million). Tua Assicurazioni boasts a robust property and casualty (P/C) insurance portfolio, generating approximately EUR 280 million (USD 307.78 million) in gross written premiums in 2022. Notably, this was largely facilitated through its extensive network of nearly 500 agents.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Mandatory Motor Third-Party Liability Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Mandatory Motor Third-Party Liability Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Mandatory Motor Third-Party Liability Insurance Market?

To stay informed about further developments, trends, and reports in the Europe Mandatory Motor Third-Party Liability Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence