Key Insights

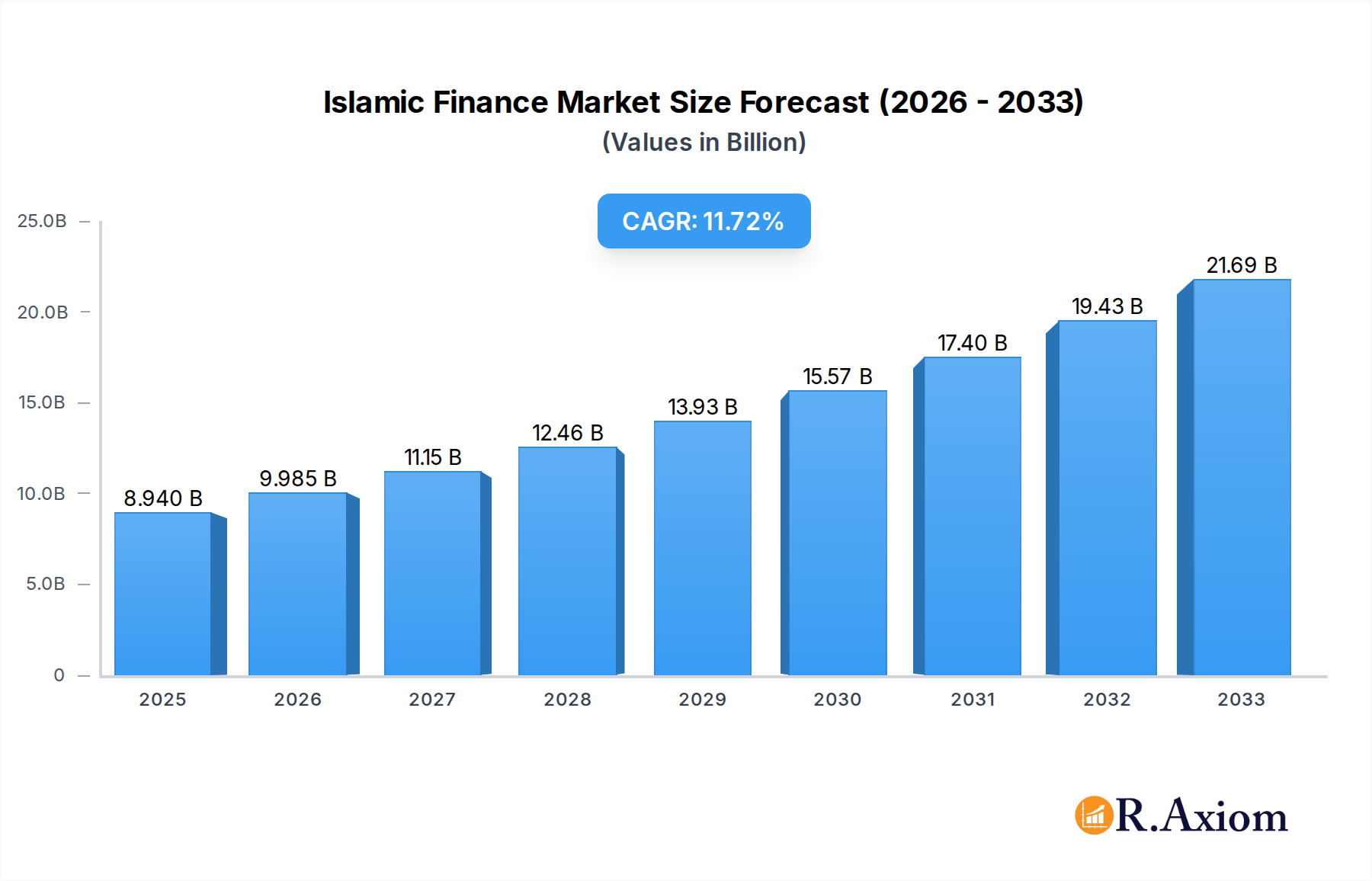

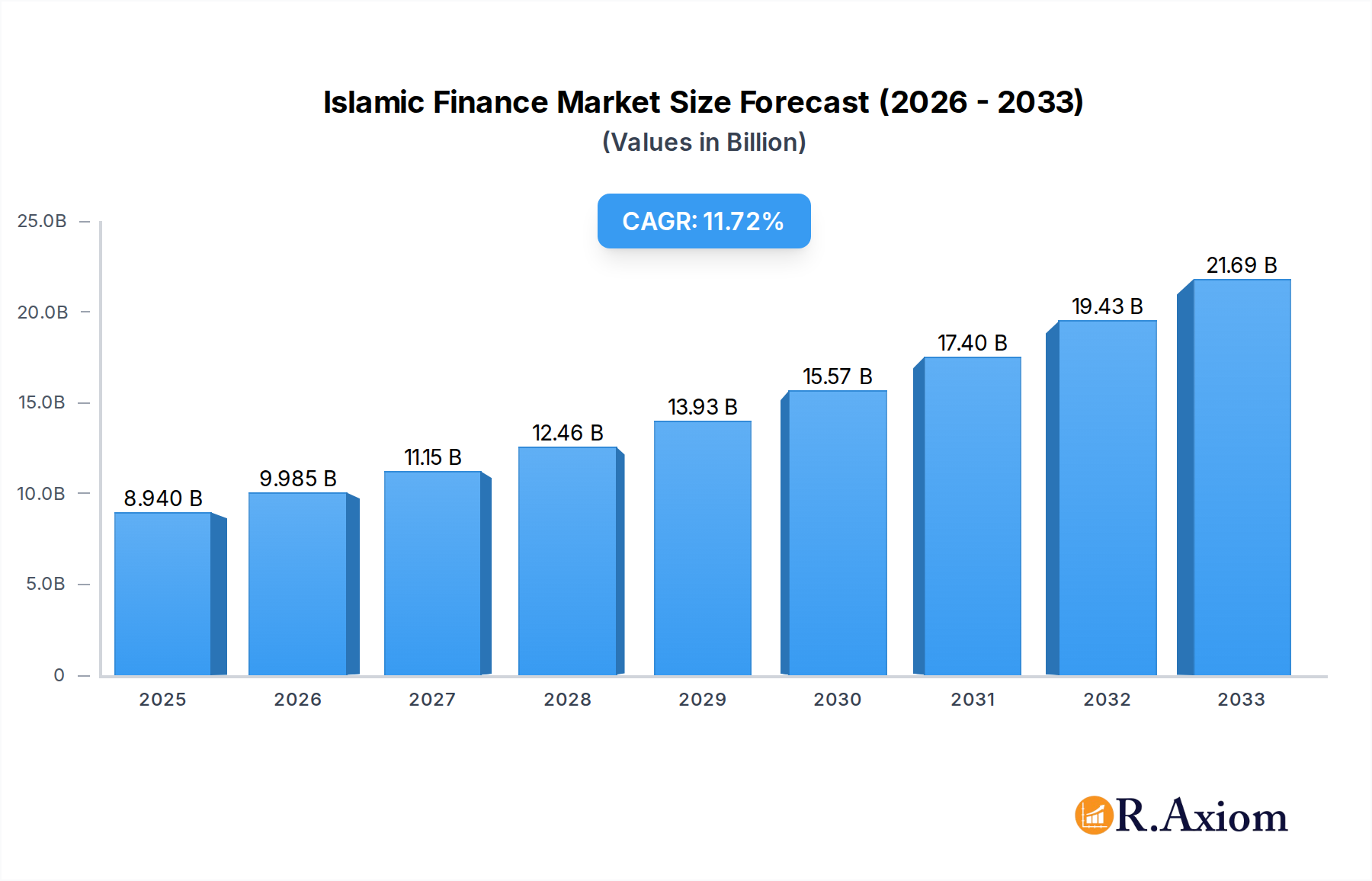

The Islamic finance market is poised for significant expansion, projected to reach USD 8.94 billion by 2025, driven by a robust CAGR of 11.8% and anticipated to continue its upward trajectory through 2033. This impressive growth is underpinned by increasing global demand for Sharia-compliant financial products and services, a trend amplified by rising awareness and acceptance of ethical investing principles. Key growth drivers include favorable government initiatives, the expansion of Islamic banking infrastructure, and a growing Muslim population seeking financial solutions aligned with their faith. Furthermore, technological advancements, such as the integration of FinTech in Islamic finance, are enhancing accessibility and product innovation, further stimulating market penetration. The market's resilience and adaptability are evident in its diversified segments, encompassing Islamic banking, Takaful (Islamic insurance), Sukuk (Islamic bonds), Islamic funds, and other financial institutions, each contributing to the overall market dynamism. The strategic focus on developing innovative Sharia-compliant instruments and expanding digital offerings will be crucial for sustained growth.

Islamic Finance Market Market Size (In Billion)

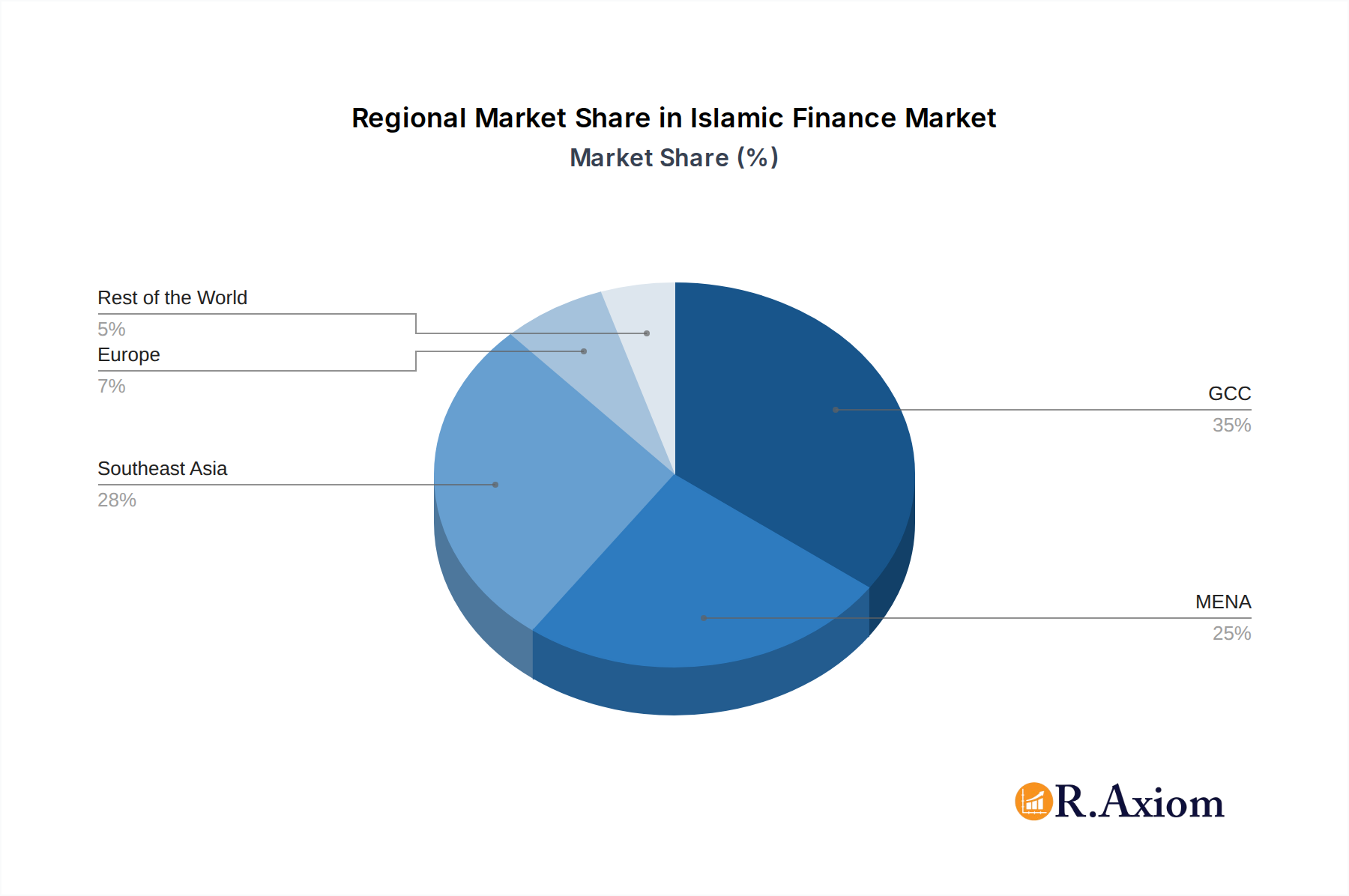

The Islamic finance market's expansion is further fueled by burgeoning economies and evolving consumer preferences. Emerging markets, particularly in Southeast Asia and the Middle East, are demonstrating substantial growth potential due to their large Muslim demographics and increasing disposable incomes. The GCC region, with established financial hubs like Saudi Arabia and the UAE, continues to be a dominant force, while MENA countries, including Iran and Egypt, are emerging as significant players. Southeast Asia, led by Malaysia and Indonesia, is also witnessing accelerated adoption, driven by supportive regulatory frameworks and a proactive approach to Islamic finance development. While the market enjoys strong growth, certain restraints, such as regulatory complexities in some regions and the need for greater standardization, require continuous attention. However, the overall outlook remains highly positive, with ongoing innovation and a commitment to ethical financial practices positioning Islamic finance for continued success and broader global integration.

Islamic Finance Market Company Market Share

This in-depth report provides a comprehensive analysis of the global Islamic Finance Market, offering critical insights into its present landscape and future trajectory. Covering the historical period from 2019 to 2024 and projecting through 2033 with a base year of 2025, this report is an indispensable resource for financial institutions, investors, regulators, and stakeholders seeking to understand and capitalize on the rapidly evolving Islamic finance sector. The study delves into market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and significant M&A activities, providing quantifiable metrics such as market share and M&A deal values.

The Islamic Finance Market is experiencing robust growth, driven by increasing awareness, a growing Muslim population, and a rising demand for Sharia-compliant financial products and services. This report forecasts significant expansion across key segments, including Islamic Banking, Islamic Insurance (Takaful), Islamic Bonds (Sukuk), Other Islamic Financial Institutions (OIFIs), and Islamic Funds. With a projected compound annual growth rate (CAGR) of XX%, the market is set to reach an estimated value of trillions of dollars by 2033. This analysis will equip industry professionals with actionable intelligence to navigate competitive dynamics, capitalize on emerging opportunities, and understand the impact of technological disruptions and evolving consumer preferences.

Islamic Finance Market Market Concentration & Innovation

The Islamic Finance Market exhibits a moderate to high degree of market concentration, particularly within established Islamic banking hubs. Leading players like Dubai Islamic Bank, National Commercial Bank Saudi Arabia, and Kuwait Finance House hold substantial market shares, often exceeding XX% in their respective regions. Innovation is a key differentiator, with financial institutions investing heavily in digital transformation, Sharia-compliant fintech solutions, and the development of novel Sharia-compliant products to cater to diverse customer needs. Regulatory frameworks, while evolving, play a crucial role in shaping market dynamics and ensuring Sharia compliance. The presence of product substitutes from conventional finance necessitates continuous innovation and value proposition enhancement within the Islamic finance ecosystem. Mergers and Acquisitions (M&A) activities are on the rise, with recent deals valued in the tens of billions of dollars, reflecting consolidation and strategic expansion efforts aimed at achieving economies of scale and enhancing competitive positioning.

- Market Share Metrics: Leading institutions command significant market share, with top banks holding over XX% in key geographies.

- Innovation Drivers: Digitalization, Sharia-compliant fintech, and product diversification are key innovation catalysts.

- Regulatory Frameworks: Harmonization and clarity in regulations are crucial for sustained growth.

- Product Substitutes: Continuous development of competitive Sharia-compliant alternatives to conventional products is essential.

- M&A Activities: Recent M&A deals reflect strategic consolidation and expansion, with valuations in the billions.

Islamic Finance Market Industry Trends & Insights

The Islamic Finance Market is witnessing an unprecedented surge in growth, propelled by a confluence of factors including a burgeoning global Muslim population, increasing ethical investment awareness, and favorable government initiatives promoting Sharia-compliant financial services. The market's expansion is further fueled by the growing acceptance and sophistication of Islamic financial products, moving beyond traditional banking to encompass a wide array of investment vehicles and insurance solutions. Technological disruptions, particularly in the realm of Islamic fintech, are revolutionizing customer accessibility and operational efficiency, enabling seamless digital transactions and personalized Sharia-compliant offerings. Consumer preferences are increasingly leaning towards ethical and socially responsible investments, aligning perfectly with the core principles of Islamic finance. This shift is creating a significant demand for sustainable and impact-driven financial products.

The competitive landscape is intensifying, with both established Islamic financial institutions and new market entrants vying for market share. Strategic partnerships between Islamic banks and fintech companies are becoming commonplace, fostering innovation and expanding the reach of Sharia-compliant services. The market penetration of Islamic finance is steadily increasing, especially in emerging economies within the Middle East, North Africa, and Southeast Asia. Furthermore, a growing number of non-Muslim investors are also exploring Islamic finance options due to its inherent ethical and risk-mitigation characteristics. The global Islamic finance market is projected to achieve a robust CAGR of XX% over the forecast period, driven by continued economic growth in key Islamic finance markets and the persistent demand for Sharia-compliant solutions across various financial sectors.

- Market Growth Drivers: Growing Muslim population, ethical investment demand, favorable government policies, and product diversification.

- Technological Disruptions: Rise of Islamic fintech, digital banking, and blockchain applications enhancing accessibility and efficiency.

- Consumer Preferences: Increasing demand for ethical, socially responsible, and Sharia-compliant financial products and services.

- Competitive Dynamics: Intensifying competition, strategic partnerships, and emergence of new market players.

- Market Penetration: Steadily increasing penetration in key regions, with significant potential in emerging markets.

Dominant Markets & Segments in Islamic Finance Market

The Islamic Finance Market is characterized by distinct dominant regions and segments, with the Middle East and North Africa (MENA) region, particularly Saudi Arabia and the UAE, emerging as the most prominent hubs. These countries benefit from strong government support, robust regulatory frameworks, and a high concentration of Muslim populations, fostering the growth of Islamic banking, Takaful, and Sukuk markets.

- Islamic Banking: This segment consistently dominates the Islamic finance landscape, driven by increasing adoption of Sharia-compliant banking services by individuals and corporations. Leading institutions like National Commercial Bank Saudi Arabia and Dubai Islamic Bank are at the forefront, offering a comprehensive suite of products from current accounts to complex financing solutions. The segment's dominance is supported by extensive branch networks and a growing focus on digital banking platforms, making Sharia-compliant banking accessible to a wider audience.

- Islamic Bonds (Sukuk): The Sukuk market has witnessed remarkable growth, becoming a crucial instrument for sovereign and corporate financing. Countries like Malaysia and Saudi Arabia are key players in this segment, issuing Sukuk for infrastructure development and government financing. The increasing demand for Sharia-compliant investment avenues and the diversification of funding sources for governments and corporations contribute to Sukuk's significant market share.

- Islamic Insurance (Takaful): The Takaful sector is experiencing steady expansion, driven by growing awareness of its ethical principles and its role as a Sharia-compliant alternative to conventional insurance. The segment's growth is further bolstered by increasing disposable incomes and a rising emphasis on financial protection among Muslim communities.

- Other Islamic Financial Institutions (OIFIs): This diverse segment includes Islamic investment firms, asset managers, and microfinance institutions. OIFIs play a vital role in providing specialized Sharia-compliant financial solutions, catering to niche markets and contributing to the overall diversification of the Islamic finance ecosystem.

- Islamic Funds: The Islamic Funds segment offers Sharia-compliant investment opportunities through various mutual funds, exchange-traded funds (ETFs), and private equity funds. Growing investor interest in ethical and socially responsible investing, coupled with the performance of Islamic equity and fixed-income funds, is driving the growth of this segment.

Islamic Finance Market Product Developments

Product innovation within the Islamic Finance Market is focused on enhancing accessibility, Sharia compliance, and competitive appeal. Recent developments include the launch of advanced Sharia-compliant digital banking platforms, offering seamless online and mobile banking experiences. The issuance of green Sukuk and sustainable finance instruments is gaining traction, aligning with global ESG (Environmental, Social, and Governance) trends. Furthermore, there is a growing emphasis on developing Sharia-compliant wealth management solutions and innovative Takaful products catering to specific life stages and needs. These developments aim to broaden the appeal of Islamic finance, attract new customer segments, and maintain a competitive edge against conventional financial products.

Report Scope & Segmentation Analysis

This report offers a comprehensive segmentation of the Islamic Finance Market, covering key areas crucial for strategic decision-making. The analysis includes detailed insights into:

- Islamic Banking: Projections for market size, growth rates, and competitive dynamics within the Islamic banking sector, including retail, corporate, and investment banking.

- Islamic Insurance (Takaful): An in-depth analysis of the Takaful market, covering life, health, and general Takaful, with a focus on growth potential and regulatory influences.

- Islamic Bonds (Sukuk): Detailed market size estimations, issuance trends, and investment opportunities within the global Sukuk market, including sovereign and corporate Sukuk.

- Other Islamic Financial Institutions (OIFIs): Analysis of the OIFI segment, encompassing Islamic asset management, private equity, and microfinance, highlighting their evolving roles and market contributions.

- Islamic Funds: Projections and competitive landscape of Islamic mutual funds, ETFs, and other Sharia-compliant investment funds, with a focus on asset class performance and investor demand.

Key Drivers of Islamic Finance Market Growth

The Islamic Finance Market is propelled by several key drivers, including a rapidly expanding global Muslim population seeking Sharia-compliant solutions, growing ethical investment awareness worldwide, and supportive government policies and regulatory frameworks in key Islamic finance jurisdictions. Technological advancements in Islamic fintech are enhancing accessibility and operational efficiency, while increasing disposable incomes in emerging economies are fueling demand for Islamic financial products.

- Demographic Shifts: The global Muslim population's growth directly translates to an increased demand for Sharia-compliant financial services.

- Ethical Investment Trends: A rising global consciousness towards ethical and socially responsible investing aligns perfectly with the principles of Islamic finance.

- Regulatory Support: Favorable government initiatives and evolving regulatory frameworks in key markets are crucial enablers of growth.

- Technological Adoption: Advancements in Islamic fintech are democratizing access to financial services and improving customer experience.

Challenges in the Islamic Finance Market Sector

Despite its robust growth, the Islamic Finance Market faces several challenges. Regulatory fragmentation across different jurisdictions can create complexities for international operations. A perceived lack of standardization in Sharia governance and product structures can sometimes lead to investor hesitancy. Competition from increasingly sophisticated conventional financial products and services also poses a significant challenge. Furthermore, a persistent need for greater public awareness and financial literacy regarding Islamic finance principles and products remains a critical barrier to broader market penetration.

- Regulatory Harmonization: Inconsistent regulations across regions hinder seamless international operations.

- Sharia Governance Standardization: Lack of universal standards in Sharia compliance can lead to market uncertainty.

- Competition: Intense competition from established conventional financial institutions requires continuous innovation.

- Awareness and Literacy: Educating the public about Islamic finance remains crucial for market expansion.

Emerging Opportunities in Islamic Finance Market

The Islamic Finance Market presents numerous emerging opportunities. The growing demand for green and sustainable finance, aligned with Islamic principles of justice and environmental stewardship, offers significant potential. The expansion of Islamic finance into new geographies, particularly in Africa and Asia, presents untapped markets. The integration of advanced technologies like AI and blockchain in Sharia-compliant fintech solutions is creating novel products and services. Furthermore, the increasing interest from non-Muslim investors seeking ethical investment options broadens the market's appeal and potential.

- Green Sukuk and Sustainable Finance: Growing demand for ethically aligned investments in environmental and social causes.

- Geographic Expansion: Untapped markets in Africa and Asia present substantial growth potential.

- Islamic Fintech Innovation: Leveraging technologies like AI and blockchain for innovative Sharia-compliant solutions.

- Non-Muslim Investor Interest: Increasing appeal of ethical and risk-mitigating financial products to a broader investor base.

Leading Players in the Islamic Finance Market Market

- Dubai Islamic Bank

- National Commercial Bank Saudi Arabia

- Bank Mellat Iran

- Bank Melli Iran

- Kuwait Finance House

- Bank Maskan Iran

- Qatar Islamic Bank

- Abu Dhabi Islamic Bank

- May Bank Islamic

- CIMB Islamic Bank

Key Developments in Islamic Finance Market Industry

- January 2023: Abu Dhabi Islamic Bank (ADIB) increased its ownership in ADIB Egypt to over 52%, acquiring 9.6 million shares from the National Investment Bank (NIB). This strategic move signifies consolidation and expansion within the Egyptian Islamic banking sector, enhancing ADIB UAE's control and influence.

- July 2022: Kuwait Finance House (KFH) agreed to acquire Bahrain-based peer Ahli United Bank (AUB) through a share swap deal. This landmark merger, creating a bank with an estimated 115 billion USD in assets, is poised to reshape the Gulf banking landscape, establishing the new entity as the seventh largest in the region and highlighting M&A as a significant growth strategy.

Strategic Outlook for Islamic Finance Market Market

The strategic outlook for the Islamic Finance Market remains exceptionally positive. The convergence of demographic trends, growing ethical investment preferences, and continuous technological innovation points towards sustained and accelerated growth. Key growth catalysts include the further development and standardization of Sharia-compliant financial instruments, particularly in areas like sustainable finance and digital banking. Expansion into new emerging markets, coupled with strategic collaborations between Islamic financial institutions and fintech innovators, will unlock significant untapped potential. The increasing institutional adoption and diversification of Islamic finance products beyond traditional banking will solidify its position as a mainstream and influential global financial system.

Islamic Finance Market Segmentation

-

1. Financial Sector

- 1.1. Islamic Banking

- 1.2. Islamic Insurance : Takaful

- 1.3. Islamic Bonds 'Sukuk'

- 1.4. Other Islamic Financial Institution (OIFI's)

- 1.5. Islamic Funds

Islamic Finance Market Segmentation By Geography

-

1. GCC

- 1.1. Saudi Arabia

- 1.2. UAE

- 1.3. Qatar

- 1.4. Kuwait

- 1.5. Bahrain

- 1.6. Oman

-

2. MENA

- 2.1. Iran

- 2.2. Egypt

- 2.3. Rest of Middle East

- 3. Southeast Asia

-

4. Malaysia

- 4.1. Indonesia

- 4.2. Brunei

- 4.3. Pakistan

- 4.4. Rest of Southeast Asia and Asia Pacific

-

5. Europe

- 5.1. United Kingdom

- 5.2. Ieland

- 5.3. Italy

- 5.4. Rest of Europe

- 6. Rest of the World

Islamic Finance Market Regional Market Share

Geographic Coverage of Islamic Finance Market

Islamic Finance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Financial Sector

- 5.1.1. Islamic Banking

- 5.1.2. Islamic Insurance : Takaful

- 5.1.3. Islamic Bonds 'Sukuk'

- 5.1.4. Other Islamic Financial Institution (OIFI's)

- 5.1.5. Islamic Funds

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. GCC

- 5.2.2. MENA

- 5.2.3. Southeast Asia

- 5.2.4. Malaysia

- 5.2.5. Europe

- 5.2.6. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Financial Sector

- 6. Islamic Finance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Financial Sector

- 6.1.1. Islamic Banking

- 6.1.2. Islamic Insurance : Takaful

- 6.1.3. Islamic Bonds 'Sukuk'

- 6.1.4. Other Islamic Financial Institution (OIFI's)

- 6.1.5. Islamic Funds

- 6.1. Market Analysis, Insights and Forecast - by Financial Sector

- 7. GCC Islamic Finance Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Financial Sector

- 7.1.1. Islamic Banking

- 7.1.2. Islamic Insurance : Takaful

- 7.1.3. Islamic Bonds 'Sukuk'

- 7.1.4. Other Islamic Financial Institution (OIFI's)

- 7.1.5. Islamic Funds

- 7.1. Market Analysis, Insights and Forecast - by Financial Sector

- 8. MENA Islamic Finance Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Financial Sector

- 8.1.1. Islamic Banking

- 8.1.2. Islamic Insurance : Takaful

- 8.1.3. Islamic Bonds 'Sukuk'

- 8.1.4. Other Islamic Financial Institution (OIFI's)

- 8.1.5. Islamic Funds

- 8.1. Market Analysis, Insights and Forecast - by Financial Sector

- 9. Southeast Asia Islamic Finance Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Financial Sector

- 9.1.1. Islamic Banking

- 9.1.2. Islamic Insurance : Takaful

- 9.1.3. Islamic Bonds 'Sukuk'

- 9.1.4. Other Islamic Financial Institution (OIFI's)

- 9.1.5. Islamic Funds

- 9.1. Market Analysis, Insights and Forecast - by Financial Sector

- 10. Malaysia Islamic Finance Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Financial Sector

- 10.1.1. Islamic Banking

- 10.1.2. Islamic Insurance : Takaful

- 10.1.3. Islamic Bonds 'Sukuk'

- 10.1.4. Other Islamic Financial Institution (OIFI's)

- 10.1.5. Islamic Funds

- 10.1. Market Analysis, Insights and Forecast - by Financial Sector

- 11. Europe Islamic Finance Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Financial Sector

- 11.1.1. Islamic Banking

- 11.1.2. Islamic Insurance : Takaful

- 11.1.3. Islamic Bonds 'Sukuk'

- 11.1.4. Other Islamic Financial Institution (OIFI's)

- 11.1.5. Islamic Funds

- 11.1. Market Analysis, Insights and Forecast - by Financial Sector

- 12. Rest of the World Islamic Finance Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Financial Sector

- 12.1.1. Islamic Banking

- 12.1.2. Islamic Insurance : Takaful

- 12.1.3. Islamic Bonds 'Sukuk'

- 12.1.4. Other Islamic Financial Institution (OIFI's)

- 12.1.5. Islamic Funds

- 12.1. Market Analysis, Insights and Forecast - by Financial Sector

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Dubai Islamic Bank

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 National Commercial Bank Saudi Arabia

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Bank Mellat Iran

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Bank Melli Iran

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Kuwait Finance House

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Bank Maskan Iran

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Qatar Islamic Bank

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Abu Dhabi Islamic Bank

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 May Bank Islamic

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 CIMB Islamic Bank**List Not Exhaustive

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Dubai Islamic Bank

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Islamic Finance Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Islamic Finance Market Share (%) by Company 2025

List of Tables

- Table 1: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 2: Islamic Finance Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 4: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Saudi Arabia Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: UAE Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Qatar Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Kuwait Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Bahrain Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Oman Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 12: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Iran Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Egypt Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Middle East Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 17: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 19: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Indonesia Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Brunei Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Pakistan Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Southeast Asia and Asia Pacific Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 25: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 26: United Kingdom Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Ieland Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Italy Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Islamic Finance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Islamic Finance Market Revenue billion Forecast, by Financial Sector 2020 & 2033

- Table 31: Islamic Finance Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Islamic Finance Market?

The projected CAGR is approximately 11.5%.

2. Which companies are prominent players in the Islamic Finance Market?

Key companies in the market include Dubai Islamic Bank, National Commercial Bank Saudi Arabia, Bank Mellat Iran, Bank Melli Iran, Kuwait Finance House, Bank Maskan Iran, Qatar Islamic Bank, Abu Dhabi Islamic Bank, May Bank Islamic, CIMB Islamic Bank**List Not Exhaustive.

3. What are the main segments of the Islamic Finance Market?

The market segments include Financial Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.46 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Malaysia is the top Score Value for Islamic Finance Development Indicator.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2023: Abu Dhabi Islamic Bank (ADIB) has increased its ownership in ADIB Egypt to more than 52%. The UAE-based bank has acquired 9.6 million shares from the National Investment Bank (NIB), representing 2.4% of ADIB Egypt's share capital, the bank told the Abu Dhabi Securities Exchange (ADX). The deal has raised ADIB UAE's ownership in the Egyptian unit to 52.607%.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Islamic Finance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Islamic Finance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Islamic Finance Market?

To stay informed about further developments, trends, and reports in the Islamic Finance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence