Key Insights

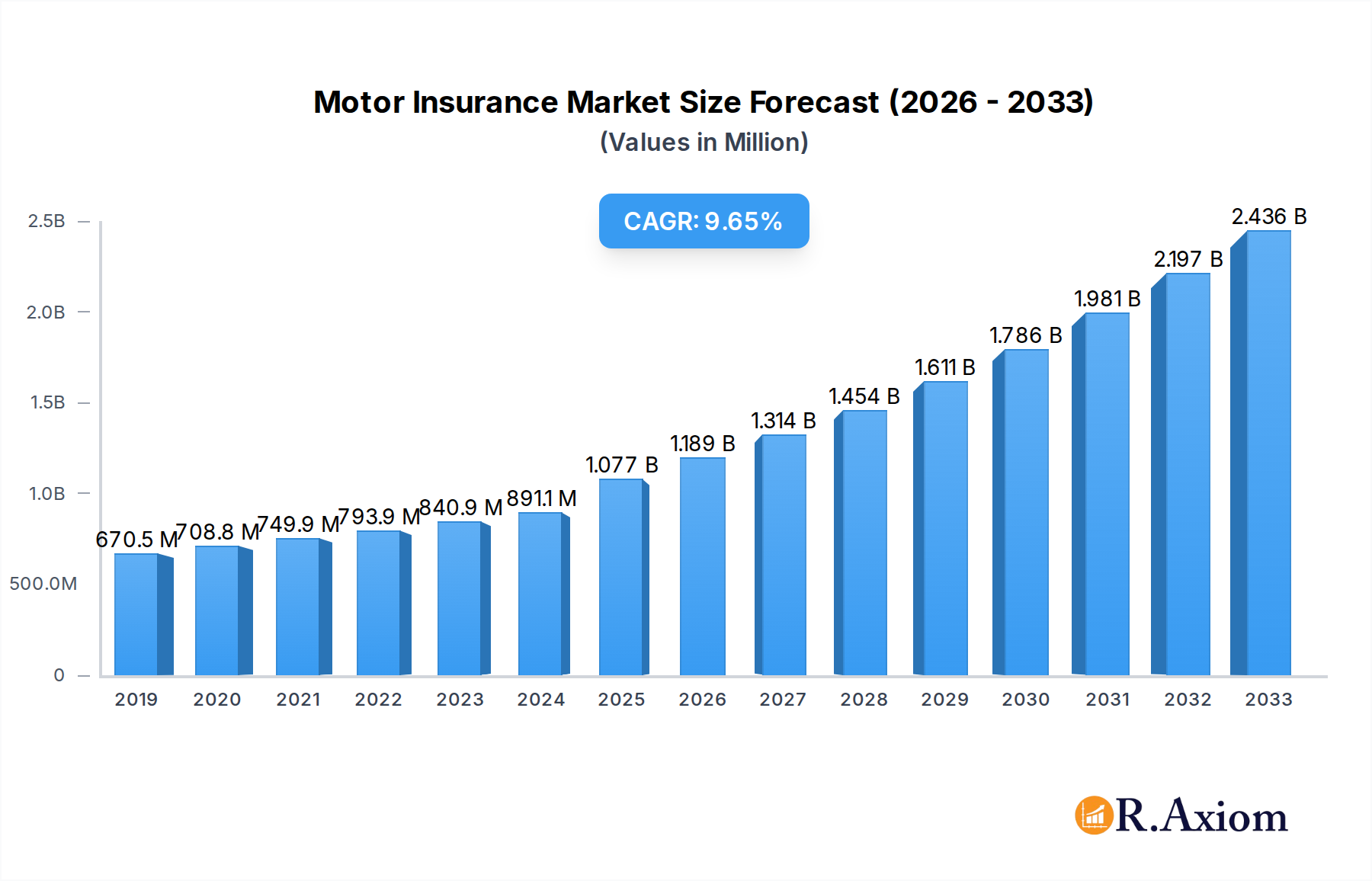

The global Motor Insurance Market is poised for robust expansion, projected to reach $1077.47 billion by 2025, driven by a compelling CAGR of 10.44% through 2033. This significant growth is underpinned by a confluence of factors. Increasing vehicle ownership worldwide, particularly in emerging economies, forms a fundamental driver. As more individuals and businesses acquire vehicles, the demand for essential motor insurance coverage naturally escalates. Furthermore, evolving regulatory landscapes and a heightened awareness among consumers and businesses regarding the financial risks associated with vehicle ownership are compelling greater adoption of insurance policies. Technological advancements are also playing a transformative role. The integration of telematics and AI is enabling more personalized insurance products, incentivizing safer driving behaviors through usage-based insurance (UBI) models, and streamlining claims processing. This innovation fosters customer loyalty and attracts new policyholders.

Motor Insurance Market Market Size (In Million)

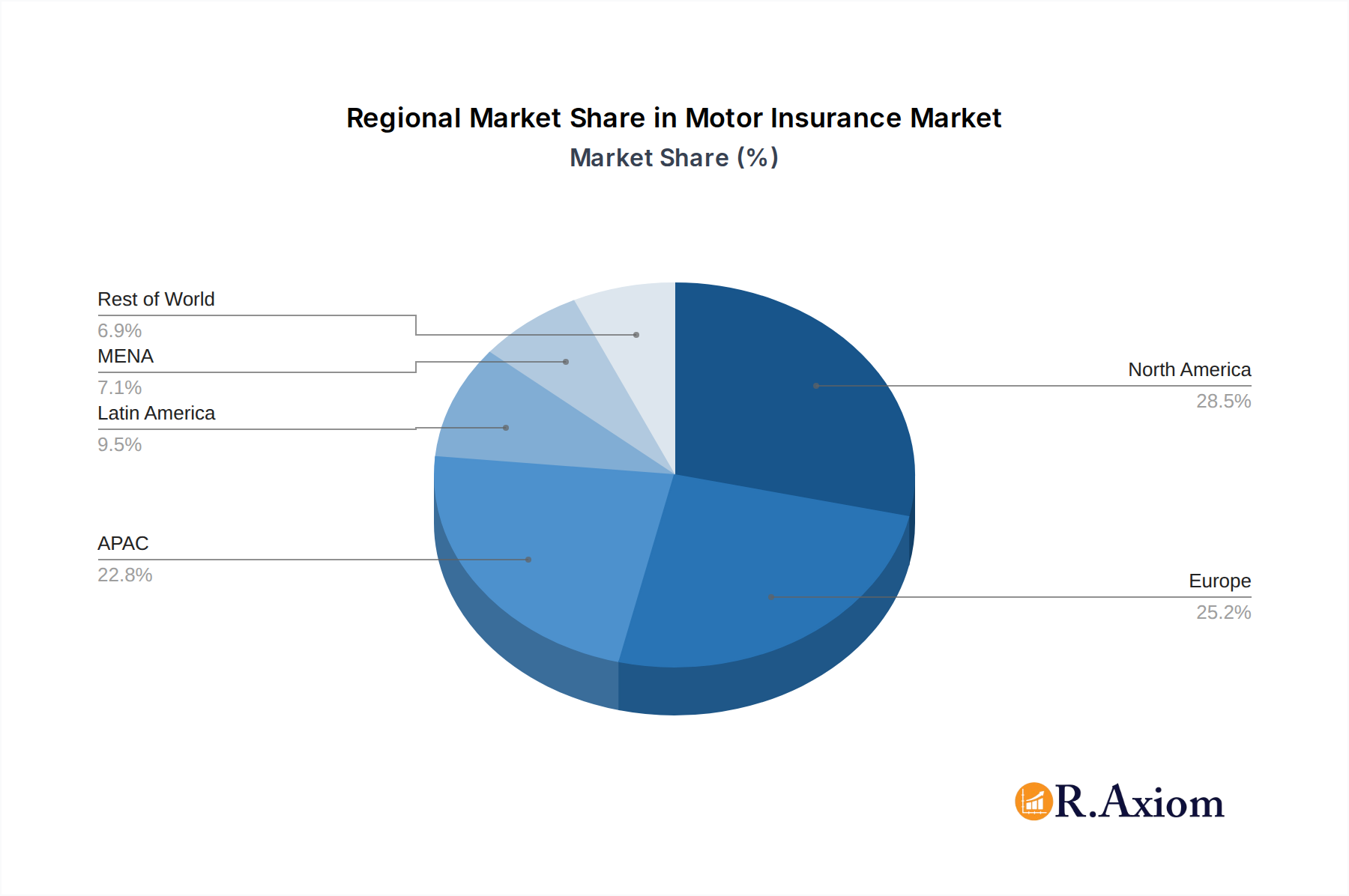

The market's dynamism is further shaped by key segmentation and regional developments. In terms of users, both Personal Motor Insurance and Commercial Motor Insurance segments are expected to witness steady growth, reflecting the diverse needs of individual car owners and fleet operators alike. Policy types such as Third Party, Third Party, Fire & Theft, and Comprehensive Motor Insurance cater to a broad spectrum of risk appetites and regulatory requirements. Geographically, North America and Europe currently represent significant markets, with established insurance infrastructures and high vehicle penetration. However, the APAC region, particularly China and India, is emerging as a high-growth area, fueled by rapid economic development, urbanization, and a burgeoning middle class. The MENA region also presents substantial untapped potential. Leading companies like Ping An Insurance, AXA SA, and Bajaj Finserv are actively investing in innovation and expanding their reach to capitalize on these global opportunities and navigate the evolving competitive landscape.

Motor Insurance Market Company Market Share

Motor Insurance Market Market Concentration & Innovation

The global motor insurance market is characterized by a moderate to high concentration, with a significant portion of the market share held by a few dominant players. Key companies like Ping An Insurance, AXA SA, Zurich AG, Bajaj Finserv, Allianz SE, GEICO, PICC Property & Casualty Co Ltd, Assicurazioni Generali, State Farm, and AllState are actively shaping the competitive landscape through strategic initiatives and innovation. The market concentration is influenced by substantial capital requirements, economies of scale in claims processing, and the need for extensive distribution networks. Innovation in this sector is primarily driven by the burgeoning adoption of InsurTech, leading to advancements in pricing algorithms, personalized policy offerings, and streamlined claims management. Regulatory frameworks worldwide play a crucial role, often dictating minimum coverage requirements and influencing market entry barriers. Product substitutes, such as extended warranties or self-insurance for specific vehicle types, pose a minor threat, but the fundamental need for third-party liability coverage remains paramount. End-user trends are leaning towards digital-first engagement and demand for flexible, usage-based insurance (UBI) models. Mergers and acquisitions (M&A) activities, valued in the billions of dollars, continue to consolidate market power and expand geographical reach. For instance, significant M&A deals worth over $5 billion in the past two years underscore the ongoing consolidation and strategic realignment within the industry. This dynamic environment fosters continuous innovation to meet evolving customer needs and regulatory demands.

Motor Insurance Market Industry Trends & Insights

The global motor insurance market is poised for substantial growth, driven by a confluence of technological advancements, evolving consumer preferences, and increasing vehicle parc. The Compound Annual Growth Rate (CAGR) for the forecast period 2025–2033 is estimated at a robust 6.5%, projecting the market value to exceed $3.5 trillion by 2033. Technological disruptions are at the forefront, with the integration of Artificial Intelligence (AI) and Machine Learning (ML) revolutionizing underwriting, claims processing, and fraud detection. Telematics, powered by IoT devices, enables personalized pricing based on driving behavior, fostering a shift towards Usage-Based Insurance (UBI). This trend is significantly impacting market penetration, with UBI adoption projected to reach over 30% of the market by 2030. Consumer preferences are increasingly demanding greater transparency, convenience, and personalized experiences. Digital channels and mobile applications are becoming the preferred touchpoints for policy purchase, claims filing, and customer service. The rising middle class in emerging economies, coupled with increasing vehicle ownership, presents a vast untapped market. Furthermore, the growing adoption of electric vehicles (EVs) and autonomous driving technology necessitates the development of specialized insurance products, opening new avenues for growth. Competitive dynamics are intensifying, with traditional insurers investing heavily in digital transformation and InsurTech startups challenging established players with agile and innovative solutions. Strategic partnerships, such as the one between GEICO and Tractable, exemplify the industry's commitment to leveraging AI for faster and more efficient claims assessments. The ongoing integration of data analytics is enabling insurers to gain deeper insights into customer behavior and risk profiles, leading to more accurate pricing and targeted product development. The market is also witnessing a growing emphasis on cybersecurity to protect sensitive customer data in an increasingly digitalized environment.

Dominant Markets & Segments in Motor Insurance Market

The global motor insurance market exhibits distinct dominance across various regions and segments, driven by a complex interplay of economic policies, infrastructure development, and regulatory landscapes.

Leading Region & Country Dominance

- Asia-Pacific: This region is emerging as a dominant force in the motor insurance market, primarily driven by China and India. Rapid economic growth, increasing disposable incomes, and a burgeoning middle class have led to a significant surge in vehicle ownership. Government initiatives promoting road safety and mandatory insurance policies further bolster market growth. China's motor insurance market alone is projected to reach over $800 billion by 2033. The rapid expansion of road infrastructure and urbanization in these countries significantly increases the demand for motor insurance.

- North America: Remains a mature yet substantial market, characterized by high vehicle penetration and a well-established insurance industry. The United States leads this segment, with a strong focus on comprehensive coverage and a mature regulatory framework. Economic stability and a large existing vehicle fleet contribute to its sustained market presence.

- Europe: While a mature market, Europe continues to be a significant player, with countries like Germany, the UK, and France exhibiting substantial market share. Stringent safety regulations and a high concentration of advanced vehicle technologies influence product demand.

Segment Dominance by User

- Personal Motor Insurance: This segment constitutes the largest share of the global motor insurance market, driven by the sheer volume of individual vehicle owners worldwide. Factors such as rising disposable incomes, urbanization, and the increasing desire for personal mobility fuel its dominance. The market size for personal motor insurance is estimated to be over $2.8 trillion by 2033.

- Key Drivers:

- Increasing vehicle ownership across emerging economies.

- Demand for enhanced safety and convenience features in vehicles.

- Mandatory insurance regulations in most countries.

- Growth of ride-sharing services, which often require commercial insurance for drivers, but indirectly boosts personal vehicle usage.

- Key Drivers:

- Commercial Motor Insurance: This segment, while smaller than personal motor insurance, is growing at a faster pace. It caters to businesses that operate fleets of vehicles, including logistics companies, delivery services, and corporate fleets. The expansion of e-commerce and the logistics industry significantly contributes to the growth of this segment. The commercial motor insurance market is expected to reach over $700 billion by 2033.

- Key Drivers:

- Growth in global trade and logistics.

- Increasing adoption of fleet management technologies for efficiency and risk reduction.

- Stringent regulatory compliance for commercial vehicle operators.

- The need for robust coverage against higher liability risks associated with commercial operations.

- Key Drivers:

Segment Dominance by Policy Type

- Comprehensive Motor Insurance: This policy type is dominant in developed markets where consumers have higher disposable incomes and a greater appreciation for complete vehicle protection. It offers the broadest coverage, including damage to the policyholder's own vehicle, theft, and third-party liabilities. The increasing value of vehicles, especially with advanced technology, further drives demand for comprehensive policies.

- Key Drivers:

- Higher purchasing power of consumers in developed economies.

- Increasing vehicle theft rates in certain regions.

- Technological advancements in vehicles leading to higher repair costs.

- Consumer preference for peace of mind and complete protection.

- Key Drivers:

- Third Party Motor Insurance: This is the most basic and legally mandated type of motor insurance in many countries, covering only the damage caused to third-party property or injury to third-party individuals. Its dominance is particularly pronounced in developing economies where affordability is a primary concern. However, regulatory mandates are pushing for higher levels of coverage.

- Key Drivers:

- Legal requirement in most jurisdictions.

- Affordability for lower-income segments.

- Basic risk mitigation for potential accidents.

- Key Drivers:

- Third Party, Fire & Theft Motor Insurance: This policy type offers a middle ground, covering third-party liabilities along with damage due to fire and theft of the insured vehicle. It is popular in markets where comprehensive coverage might be too expensive, but basic protection against these specific risks is desired.

Motor Insurance Market Product Developments

The motor insurance market is witnessing a surge in product innovations driven by technological advancements and evolving customer needs. Key developments include the proliferation of Usage-Based Insurance (UBI) policies, which leverage telematics data to offer personalized premiums based on actual driving behavior, mileage, and time of travel. This not only benefits safe drivers with lower costs but also provides insurers with richer data for risk assessment and fraud detection. Furthermore, insurers are developing specialized products for emerging vehicle technologies, such as electric vehicles (EVs) and connected cars, addressing unique risks like battery degradation and cybersecurity vulnerabilities. InsurTech collaborations are enabling faster and more efficient claims processing, exemplified by AI-powered damage assessment tools that can significantly reduce repair timelines and costs. The competitive advantage lies in offering flexible, digitally accessible, and value-added insurance solutions that cater to the modern consumer's demand for convenience and customization.

Report Scope & Segmentation Analysis

The global motor insurance market is meticulously segmented to provide granular insights into its various facets.

- User Segmentation: The market is broadly segmented into Personal Motor Insurance, catering to individual vehicle owners, and Commercial Motor Insurance, serving businesses with vehicle fleets. The Personal Motor Insurance segment is projected to maintain its dominance due to widespread vehicle ownership, while the Commercial Motor Insurance segment is expected to witness robust growth driven by the expansion of logistics and e-commerce sectors.

- Policy Type Segmentation: Further segmentation includes Third Party Motor Insurance, which covers liabilities to others; Third Party, Fire & Theft Motor Insurance, adding protection against fire and theft; and Comprehensive Motor Insurance, offering the broadest coverage for the policyholder's vehicle and third-party liabilities. Comprehensive Motor Insurance is anticipated to see steady growth in developed economies, while Third Party insurance remains crucial in emerging markets.

Key Drivers of Motor Insurance Market Growth

The motor insurance market is propelled by several key growth drivers:

- Increasing Vehicle Parc: A rising global vehicle population, particularly in emerging economies, directly translates to a larger addressable market for motor insurance.

- Technological Advancements: The integration of AI, telematics, and IoT enables personalized pricing, efficient claims processing, and the development of innovative products like Usage-Based Insurance (UBI).

- Favorable Regulatory Frameworks: Mandatory third-party liability insurance laws in most countries create a baseline demand for motor insurance products.

- Growing Middle Class & Disposable Income: Increased purchasing power in developing nations allows more individuals to own vehicles and afford insurance coverage.

- Urbanization: Expanding urban areas often lead to increased traffic density and a higher incidence of accidents, driving the need for insurance.

Challenges in the Motor Insurance Market Sector

Despite its growth, the motor insurance market faces several significant challenges:

- Intense Competition & Price Wars: The market is highly competitive, leading to price sensitivity among consumers and pressure on profit margins for insurers.

- Rising Claims Costs: Factors such as increasing vehicle repair costs, advancements in vehicle technology, and the frequency of severe weather events contribute to escalating claims expenses.

- Fraudulent Claims: Motor insurance is susceptible to fraudulent claims, which significantly impact insurer profitability and can lead to higher premiums for legitimate policyholders.

- Regulatory Hurdles & Compliance: Navigating diverse and evolving regulatory landscapes across different jurisdictions requires significant investment in compliance and can sometimes stifle innovation.

- Cybersecurity Threats: The increasing digitization of insurance operations and customer data exposes insurers to cybersecurity risks, requiring substantial investment in protective measures.

Emerging Opportunities in Motor Insurance Market

The motor insurance market is ripe with emerging opportunities:

- Growth in Electric Vehicles (EVs) & Autonomous Driving: The shift towards EVs and the development of autonomous vehicles present a need for new, specialized insurance products to cover unique risks and technologies.

- Usage-Based Insurance (UBI) Expansion: The continued adoption of telematics and UBI offers significant potential for personalized pricing, customer engagement, and data-driven underwriting.

- InsurTech Innovations: Collaborations with InsurTech firms can unlock opportunities for streamlined claims processing, enhanced customer experiences, and the development of novel distribution channels.

- Emerging Markets: Untapped potential in developing economies with rising vehicle ownership and increasing insurance awareness offers substantial growth prospects.

- Data Analytics & AI: Leveraging advanced analytics and AI can lead to more accurate risk assessment, predictive modeling, and personalized product offerings, creating a competitive edge.

Leading Players in the Motor Insurance Market Market

- Ping An Insurance

- AXA SA

- Zurich AG

- Bajaj Finserv

- Allianz SE

- GEICO

- PICC Property & Casualty Co Lt

- Assicurazioni Generali

- State Farm

- AllState

Key Developments in Motor Insurance Market Industry

- August 2021: AXA S.A. introduced STeP, a new digital claims solution aimed at simplifying the motor insurance process for customers. This innovation drastically reduced the time from customer notification to repair or salvage arrangement to mere minutes.

- May 2021: GEICO partnered with AI technology company Tractable to accelerate its auto claim and repair processes. Tractable's computer vision technology, trained on millions of historical claims, allows for rapid assessment of vehicle damage from photos, enabling GEICO to review estimates within seconds and reduce administrative overhead.

Strategic Outlook for Motor Insurance Market Market

The strategic outlook for the motor insurance market is one of dynamic evolution and sustained growth, fueled by technological integration and shifting consumer demands. The continued expansion of the global vehicle parc, particularly in emerging economies, will remain a fundamental growth catalyst. Insurers are expected to prioritize investments in InsurTech solutions, including AI-powered claims automation, telematics for Usage-Based Insurance (UBI), and digital customer engagement platforms, to enhance efficiency and customer satisfaction. The rise of electric and autonomous vehicles will necessitate the development of specialized insurance products, presenting significant innovation opportunities. Strategic partnerships and potential mergers and acquisitions will continue to shape the competitive landscape, as companies seek to expand their market reach and technological capabilities. Ultimately, success will hinge on the ability of market players to offer personalized, transparent, and seamless insurance experiences, leveraging data analytics and cutting-edge technology to navigate an increasingly complex and evolving automotive ecosystem.

Motor Insurance Market Segmentation

-

1. User

- 1.1. Personal Motor Insurance

- 1.2. Commercial Motor Insurance

-

2. Policy Type

- 2.1. Third Party Motor Insurance

- 2.2. Third Party, Fire & Theft Motor Insurance

- 2.3. Comprehensive Motor Insurance

Motor Insurance Market Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. UK

- 1.3. France

- 1.4. Switzerland

- 1.5. Rest Of Europe

-

2. North America

- 2.1. USA

- 2.2. Canada

-

3. Latin America

- 3.1. Brazil

- 3.2. Argentina

-

4. APAC

- 4.1. China

- 4.2. India

- 4.3. Japan

- 4.4. South Korea

- 4.5. Indonesia

- 4.6. Rest of APAC

-

5. MENA

- 5.1. UAE

- 5.2. Saudi Arabia

- 5.3. Lebanon

- 5.4. Rest of North Africa

Motor Insurance Market Regional Market Share

Geographic Coverage of Motor Insurance Market

Motor Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by User

- 5.1.1. Personal Motor Insurance

- 5.1.2. Commercial Motor Insurance

- 5.2. Market Analysis, Insights and Forecast - by Policy Type

- 5.2.1. Third Party Motor Insurance

- 5.2.2. Third Party, Fire & Theft Motor Insurance

- 5.2.3. Comprehensive Motor Insurance

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.3.2. North America

- 5.3.3. Latin America

- 5.3.4. APAC

- 5.3.5. MENA

- 5.1. Market Analysis, Insights and Forecast - by User

- 6. Global Motor Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by User

- 6.1.1. Personal Motor Insurance

- 6.1.2. Commercial Motor Insurance

- 6.2. Market Analysis, Insights and Forecast - by Policy Type

- 6.2.1. Third Party Motor Insurance

- 6.2.2. Third Party, Fire & Theft Motor Insurance

- 6.2.3. Comprehensive Motor Insurance

- 6.1. Market Analysis, Insights and Forecast - by User

- 7. Europe Motor Insurance Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by User

- 7.1.1. Personal Motor Insurance

- 7.1.2. Commercial Motor Insurance

- 7.2. Market Analysis, Insights and Forecast - by Policy Type

- 7.2.1. Third Party Motor Insurance

- 7.2.2. Third Party, Fire & Theft Motor Insurance

- 7.2.3. Comprehensive Motor Insurance

- 7.1. Market Analysis, Insights and Forecast - by User

- 8. North America Motor Insurance Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by User

- 8.1.1. Personal Motor Insurance

- 8.1.2. Commercial Motor Insurance

- 8.2. Market Analysis, Insights and Forecast - by Policy Type

- 8.2.1. Third Party Motor Insurance

- 8.2.2. Third Party, Fire & Theft Motor Insurance

- 8.2.3. Comprehensive Motor Insurance

- 8.1. Market Analysis, Insights and Forecast - by User

- 9. Latin America Motor Insurance Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by User

- 9.1.1. Personal Motor Insurance

- 9.1.2. Commercial Motor Insurance

- 9.2. Market Analysis, Insights and Forecast - by Policy Type

- 9.2.1. Third Party Motor Insurance

- 9.2.2. Third Party, Fire & Theft Motor Insurance

- 9.2.3. Comprehensive Motor Insurance

- 9.1. Market Analysis, Insights and Forecast - by User

- 10. APAC Motor Insurance Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by User

- 10.1.1. Personal Motor Insurance

- 10.1.2. Commercial Motor Insurance

- 10.2. Market Analysis, Insights and Forecast - by Policy Type

- 10.2.1. Third Party Motor Insurance

- 10.2.2. Third Party, Fire & Theft Motor Insurance

- 10.2.3. Comprehensive Motor Insurance

- 10.1. Market Analysis, Insights and Forecast - by User

- 11. MENA Motor Insurance Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by User

- 11.1.1. Personal Motor Insurance

- 11.1.2. Commercial Motor Insurance

- 11.2. Market Analysis, Insights and Forecast - by Policy Type

- 11.2.1. Third Party Motor Insurance

- 11.2.2. Third Party, Fire & Theft Motor Insurance

- 11.2.3. Comprehensive Motor Insurance

- 11.1. Market Analysis, Insights and Forecast - by User

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ping An Insurance

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 AXA SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Zurich AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bajaj Finserv

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Allianz SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GEICO

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 PICC Property & Casualty Co Lt

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Assicurazioni Generali

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 State Farm

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AllState

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Ping An Insurance

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Motor Insurance Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Europe Motor Insurance Market Revenue (billion), by User 2025 & 2033

- Figure 3: Europe Motor Insurance Market Revenue Share (%), by User 2025 & 2033

- Figure 4: Europe Motor Insurance Market Revenue (billion), by Policy Type 2025 & 2033

- Figure 5: Europe Motor Insurance Market Revenue Share (%), by Policy Type 2025 & 2033

- Figure 6: Europe Motor Insurance Market Revenue (billion), by Country 2025 & 2033

- Figure 7: Europe Motor Insurance Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Motor Insurance Market Revenue (billion), by User 2025 & 2033

- Figure 9: North America Motor Insurance Market Revenue Share (%), by User 2025 & 2033

- Figure 10: North America Motor Insurance Market Revenue (billion), by Policy Type 2025 & 2033

- Figure 11: North America Motor Insurance Market Revenue Share (%), by Policy Type 2025 & 2033

- Figure 12: North America Motor Insurance Market Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Motor Insurance Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Motor Insurance Market Revenue (billion), by User 2025 & 2033

- Figure 15: Latin America Motor Insurance Market Revenue Share (%), by User 2025 & 2033

- Figure 16: Latin America Motor Insurance Market Revenue (billion), by Policy Type 2025 & 2033

- Figure 17: Latin America Motor Insurance Market Revenue Share (%), by Policy Type 2025 & 2033

- Figure 18: Latin America Motor Insurance Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Latin America Motor Insurance Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: APAC Motor Insurance Market Revenue (billion), by User 2025 & 2033

- Figure 21: APAC Motor Insurance Market Revenue Share (%), by User 2025 & 2033

- Figure 22: APAC Motor Insurance Market Revenue (billion), by Policy Type 2025 & 2033

- Figure 23: APAC Motor Insurance Market Revenue Share (%), by Policy Type 2025 & 2033

- Figure 24: APAC Motor Insurance Market Revenue (billion), by Country 2025 & 2033

- Figure 25: APAC Motor Insurance Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: MENA Motor Insurance Market Revenue (billion), by User 2025 & 2033

- Figure 27: MENA Motor Insurance Market Revenue Share (%), by User 2025 & 2033

- Figure 28: MENA Motor Insurance Market Revenue (billion), by Policy Type 2025 & 2033

- Figure 29: MENA Motor Insurance Market Revenue Share (%), by Policy Type 2025 & 2033

- Figure 30: MENA Motor Insurance Market Revenue (billion), by Country 2025 & 2033

- Figure 31: MENA Motor Insurance Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Motor Insurance Market Revenue billion Forecast, by User 2020 & 2033

- Table 2: Global Motor Insurance Market Revenue billion Forecast, by Policy Type 2020 & 2033

- Table 3: Global Motor Insurance Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Motor Insurance Market Revenue billion Forecast, by User 2020 & 2033

- Table 5: Global Motor Insurance Market Revenue billion Forecast, by Policy Type 2020 & 2033

- Table 6: Global Motor Insurance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Germany Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: UK Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Switzerland Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest Of Europe Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Motor Insurance Market Revenue billion Forecast, by User 2020 & 2033

- Table 13: Global Motor Insurance Market Revenue billion Forecast, by Policy Type 2020 & 2033

- Table 14: Global Motor Insurance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 15: USA Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Global Motor Insurance Market Revenue billion Forecast, by User 2020 & 2033

- Table 18: Global Motor Insurance Market Revenue billion Forecast, by Policy Type 2020 & 2033

- Table 19: Global Motor Insurance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Brazil Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Argentina Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Motor Insurance Market Revenue billion Forecast, by User 2020 & 2033

- Table 23: Global Motor Insurance Market Revenue billion Forecast, by Policy Type 2020 & 2033

- Table 24: Global Motor Insurance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 25: China Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: South Korea Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of APAC Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Global Motor Insurance Market Revenue billion Forecast, by User 2020 & 2033

- Table 32: Global Motor Insurance Market Revenue billion Forecast, by Policy Type 2020 & 2033

- Table 33: Global Motor Insurance Market Revenue billion Forecast, by Country 2020 & 2033

- Table 34: UAE Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Saudi Arabia Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Lebanon Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of North Africa Motor Insurance Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Motor Insurance Market?

The projected CAGR is approximately 5.85%.

2. Which companies are prominent players in the Motor Insurance Market?

Key companies in the market include Ping An Insurance, AXA SA, Zurich AG, Bajaj Finserv, Allianz SE, GEICO, PICC Property & Casualty Co Lt, Assicurazioni Generali, State Farm, AllState.

3. What are the main segments of the Motor Insurance Market?

The market segments include User, Policy Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 442.7 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Sales of Cars in Europe Drives The Market; Increase in Road Traffic Accidents Drives The Market.

6. What are the notable trends driving market growth?

Usage-based Insurance and Insurance Telematics in Motor Insurance is on Rise.

7. Are there any restraints impacting market growth?

Increase in Cost of Claims Made; Increase in False Claims and Scams.

8. Can you provide examples of recent developments in the market?

In August 2021, the insurance giant AXA S.A has introduced STeP, a new digital claims solution to help customers simplify their motor insurance process. AXA claimed that through STeP the time taken from customer notification to partners arranging repair or salvage is now down to minutes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Motor Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Motor Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Motor Insurance Market?

To stay informed about further developments, trends, and reports in the Motor Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence