Key Insights

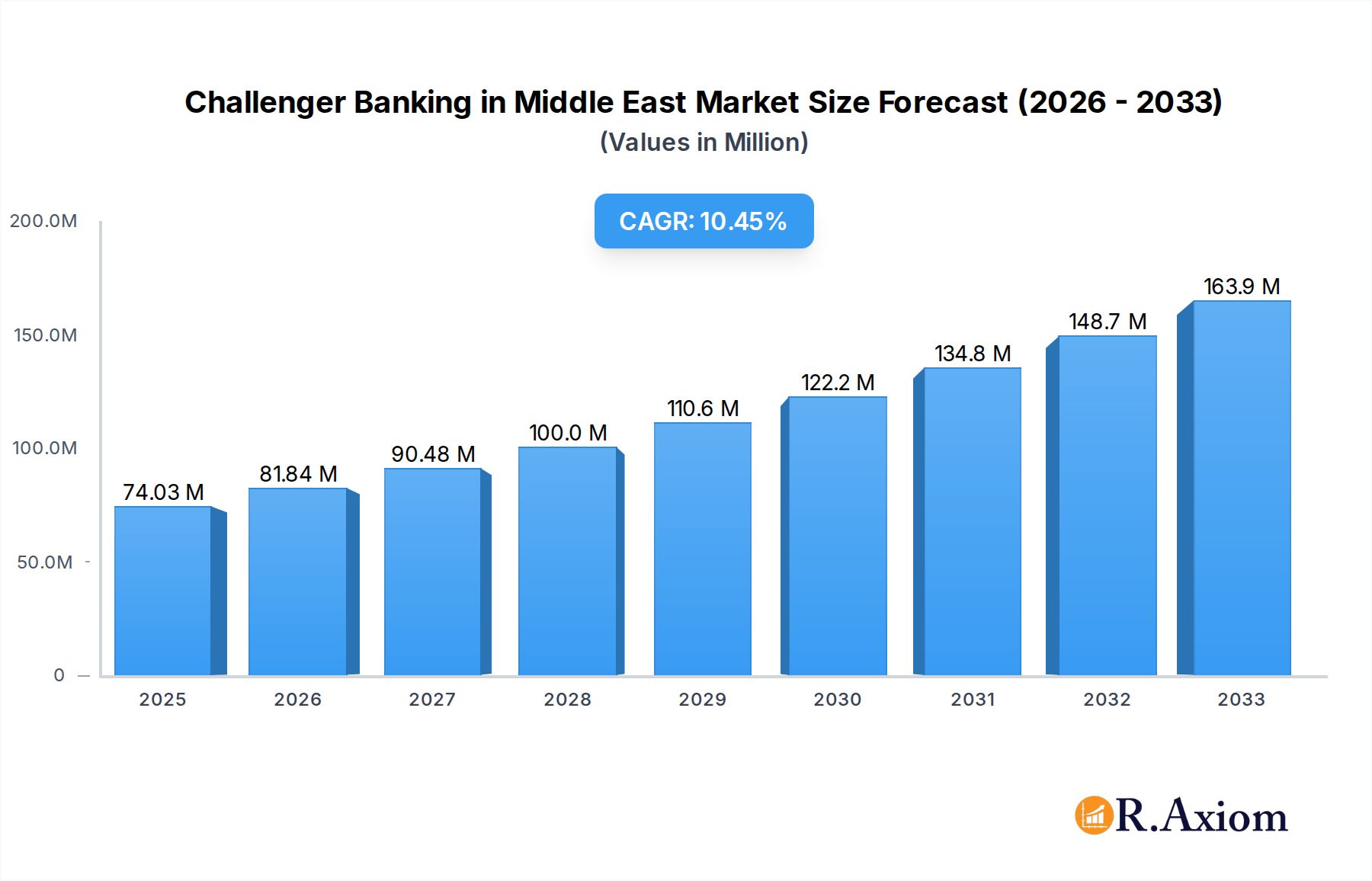

The Challenger Banking market in the Middle East & Africa is poised for significant expansion, with a current market size of $74.03 million and a projected Compound Annual Growth Rate (CAGR) of 10.50% through 2033. This robust growth is fueled by increasing digital adoption, a burgeoning young population eager for innovative financial solutions, and a growing dissatisfaction with traditional banking services that often lack agility and customer-centricity. Key drivers include the proliferation of smartphones and internet penetration across the region, enabling greater access to digital banking platforms. Furthermore, regulatory bodies are increasingly supportive of fintech innovation, creating a more conducive environment for challenger banks to thrive. The demand for seamless, mobile-first banking experiences, particularly for payments, savings, and consumer credit, is escalating.

Challenger Banking in Middle East & Africa Market Market Size (In Million)

The market is segmented by service type, with Payments, Savings Products, and Consumer Credit emerging as dominant categories. On the end-user front, both the Business Segment and the Personal Segment are exhibiting strong demand, indicating broad market appeal. Emerging trends point towards greater personalization of financial services, the integration of AI for enhanced customer support and fraud detection, and the development of Sharia-compliant digital banking solutions to cater to the specific needs of the region. However, challenges such as low financial literacy in certain areas, intense competition from established banks launching their own digital offerings, and evolving regulatory frameworks require strategic navigation. Despite these hurdles, the fundamental shift towards digital financial services in the Middle East & Africa presents a compelling growth narrative for challenger banks.

Challenger Banking in Middle East & Africa Market Company Market Share

Here is the SEO-optimized, detailed report description for Challenger Banking in the Middle East & Africa Market:

Challenger Banking in Middle East & Africa Market Market Concentration & Innovation

This section delves into the intricate market concentration and innovation landscape of challenger banking across the Middle East and Africa. We analyze key innovation drivers, including the rapid adoption of digital technologies and a burgeoning unbanked and underbanked population seeking accessible financial solutions. The evolving regulatory frameworks, such as sandbox initiatives and digital banking licenses, are critically examined for their impact on market entry and competitive dynamics. We assess product substitutes offered by traditional banks and fintech companies, and dissect end-user trends that favor digital-first banking experiences. Mergers and acquisitions (M&A) activities, a significant indicator of market consolidation and strategic growth, are quantified. For instance, the market is projected to see M&A deal values reach $500 Million by 2033, signifying a move towards larger, more integrated digital banking entities. Market share for leading challenger banks is estimated to be around 15% of the digital banking segment by 2025, with significant growth potential. Key innovation hubs are identified, with a focus on countries fostering fintech ecosystems.

- Innovation Drivers: Mobile penetration, smartphone adoption, youth demographics, demand for seamless digital experiences.

- Regulatory Frameworks: Fintech sandboxes, digital banking licenses, cross-border payment regulations.

- Product Substitutes: Mobile money services, digital wallets, peer-to-peer lending platforms.

- End-User Trends: Convenience, lower fees, personalized services, financial inclusion.

- M&A Activities: Strategic acquisitions to gain market share, technology, or customer base; consolidation of smaller players.

Challenger Banking in Middle East & Africa Market Industry Trends & Insights

The Middle East & Africa challenger banking market is experiencing unprecedented growth, driven by a confluence of technological advancements, evolving consumer behavior, and supportive regulatory environments. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22% from 2025 to 2033, indicating a robust expansion trajectory. This surge is fueled by the increasing demand for convenient, affordable, and accessible financial services, particularly in regions with a high proportion of unbanked and underbanked populations. The penetration of digital financial services is expected to reach 60% by 2033, a significant leap from historical levels. Technological disruptions, such as the widespread adoption of AI, machine learning, blockchain, and cloud computing, are reshaping service delivery and customer engagement models. Challenger banks are leveraging these technologies to offer personalized financial advice, streamline onboarding processes, and enhance security. Consumer preferences are shifting towards digital-first banking, with a strong emphasis on mobile accessibility, user-friendly interfaces, and transparent fee structures. Traditional banks are increasingly facing competition from these agile digital players, leading to a dynamic competitive landscape characterized by innovation and strategic partnerships. The rise of Neobanks and platform banking models signifies a paradigm shift, moving beyond traditional branch-based operations to offer a more integrated and holistic financial ecosystem. Key industry insights point towards a future where challenger banks play a pivotal role in driving financial inclusion and economic development across the region. The market is currently valued at $10 Billion and is expected to reach $45 Billion by 2033.

Dominant Markets & Segments in Challenger Banking in Middle East & Africa Market

The Middle East & Africa challenger banking market exhibits distinct regional and segmental dominance, with specific countries and service types emerging as key growth engines. The United Arab Emirates stands out as a leading market, owing to its advanced digital infrastructure, supportive regulatory sandbox, and a significant expatriate population seeking modern banking solutions. This dominance is further bolstered by the presence of innovative challenger banks and a receptive consumer base.

In terms of Service Type, Payments and Current Accounts are currently the most dominant segments. The widespread adoption of mobile payments, facilitated by the increasing smartphone penetration and a growing e-commerce landscape, has propelled the payments sector. Challenger banks are offering competitive transaction fees and seamless integration with popular payment platforms. Similarly, the demand for user-friendly and accessible current accounts, often with integrated digital tools and loyalty programs, is driving the growth of this segment. By 2033, the payments segment is projected to command 30% of the challenger banking market share, followed by current accounts at 25%.

The Personal Segment of End-User Type is currently the largest, driven by individual consumers seeking more convenient and tailored banking experiences. This segment is characterized by a younger demographic, tech-savvy individuals, and those who are underserved by traditional banking institutions. However, the Business Segment is rapidly gaining traction, with challenger banks increasingly offering specialized solutions for SMEs, including simplified business accounts, streamlined invoicing, and access to working capital. This segment is expected to exhibit a higher CAGR of 25% compared to the personal segment's 20% in the forecast period.

- Leading Country: United Arab Emirates.

- Key Drivers: Robust digital infrastructure, supportive fintech regulations, significant expatriate population, high disposable income.

- Dominant Service Type: Payments.

- Key Drivers: Growing e-commerce, high mobile penetration, demand for instant transfers, attractive transaction fees.

- Dominant Service Type: Current Accounts.

- Key Drivers: Demand for digital-first banking, integrated financial management tools, low-fee alternatives to traditional accounts.

- Dominant End-User Type: Personal Segment.

- Key Drivers: Youth demographics, tech-savviness, financial inclusion needs, desire for personalized banking.

- Emerging End-User Type: Business Segment (SMEs).

- Key Drivers: Need for simplified business banking, access to capital, digital invoicing and accounting tools, cost-effective solutions.

Challenger Banking in Middle East & Africa Market Product Developments

Challenger banks in the Middle East & Africa are rapidly innovating to meet evolving customer demands. Recent product developments focus on enhancing user experience through AI-powered chatbots for customer support, personalized financial insights, and simplified onboarding processes. Applications range from advanced budgeting tools and investment platforms to micro-lending and cross-border remittance solutions. Competitive advantages are being carved out through hyper-personalization, integration with super-apps, and the offering of niche financial products tailored to specific segments like freelancers or SMEs. The emphasis is on building seamless digital ecosystems that go beyond traditional banking, fostering customer loyalty and capturing a larger share of wallet.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Challenger Banking in Middle East & Africa Market across various crucial segments, providing comprehensive insights and projections. The segmentation encompasses:

- Service Type: This includes detailed analysis of Payments, Savings Products, Current Accounts, Consumer Credit, and Loans. Each sub-segment's market size, growth trajectory, and competitive landscape is explored. For instance, the Payments segment is projected to reach $13.5 Billion by 2033, with a CAGR of 23%.

- End-User Type: The report distinguishes between the Business Segment and the Personal Segment. The market size for the personal segment is estimated at $6 Billion in 2025, while the business segment is projected to grow from $4 Billion in 2025 to $22.5 Billion by 2033, exhibiting a strong CAGR of 25%. Competitive dynamics within each end-user type are also examined.

Key Drivers of Challenger Banking in Middle East & Africa Market Growth

The growth of challenger banking in the Middle East & Africa is propelled by several interconnected factors. Technological advancements, particularly widespread smartphone penetration and high internet access, form the bedrock of this growth, enabling seamless digital service delivery. Supportive regulatory environments, including fintech sandboxes and digital banking licenses, have encouraged innovation and market entry. Furthermore, a substantial unbanked and underbanked population presents a significant opportunity for financial inclusion, with challenger banks offering accessible and affordable alternatives to traditional financial institutions. The increasing demand for convenience, personalization, and lower fees from consumers also plays a crucial role.

Challenges in the Challenger Banking in Middle East & Africa Market Sector

Despite its robust growth, the challenger banking sector in the Middle East & Africa faces several significant challenges. Regulatory hurdles and evolving compliance requirements can be complex and resource-intensive, especially for smaller players. Intense competition from both established banks launching digital initiatives and other fintech startups necessitates continuous innovation and customer acquisition strategies, impacting profitability. Customer trust and adoption, particularly among older demographics or in more conservative markets, can be a slow process, requiring extensive education and reassurance. Cybersecurity threats and data privacy concerns are paramount, demanding significant investment in robust security infrastructure. Supply chain issues, while less direct, can impact the availability of specialized hardware or software components necessary for digital infrastructure.

Emerging Opportunities in Challenger Banking in Middle East & Africa Market

Emerging opportunities in the Middle East & Africa challenger banking market are abundant and diverse. The significant underserved rural populations offer vast potential for financial inclusion through mobile-first solutions. The rapid growth of SME sectors across the region presents a lucrative opportunity for specialized business banking services, including seamless payment gateways and accessible credit lines. Emerging technologies like Open Banking and APIs are fostering greater collaboration and innovation, enabling challenger banks to integrate with a wider range of services and data sources. The increasing demand for Sharia-compliant digital financial products in certain markets opens up a unique niche for specialized offerings. Furthermore, the ongoing digital transformation of governments and businesses across the region provides fertile ground for B2B digital banking solutions.

Leading Players in the Challenger Banking in Middle East & Africa Market Market

- Pepper

- Clearly

- Liv Bank

- Xpence

- Mashreq Neo

- Meem Bank

- CBD Now

- Hala

- MoneySmart

- Bank ABC

Key Developments in Challenger Banking in Middle East & Africa Market Industry

- September 2022: New challenger Wio Bank launched in the UAE. Wio Bank, the region's first platform bank, officially launched operations in the UAE, with its headquarters in Abu Dhabi.

- July 2022: Mashreq launched a new supply-chain finance platform. Part of Titan, a digital corporate banking platform, lets business clients onboard their entire vendor base.

Strategic Outlook for Challenger Banking in Middle East & Africa Market Market

The strategic outlook for the challenger banking market in the Middle East & Africa is exceptionally positive, characterized by continued innovation and significant expansion. The market is poised for substantial growth driven by the increasing adoption of digital financial services, a large unbanked and underbanked population, and evolving consumer preferences for convenience and affordability. Key growth catalysts include the expansion of Open Banking initiatives, fostering greater collaboration and product diversification. Strategic partnerships between challenger banks and established financial institutions, as well as technology providers, will be crucial for scaling operations and enhancing service offerings. Investments in cutting-edge technologies like AI and blockchain will further differentiate players and improve customer experiences. The ongoing focus on financial inclusion and the burgeoning digital economy across the region ensures a sustained demand for the agile and customer-centric solutions offered by challenger banks, solidifying their position as key players in the future of finance.

Challenger Banking in Middle East & Africa Market Segmentation

-

1. Service Type

- 1.1. Payments

- 1.2. Savings Products

- 1.3. Current Accounts

- 1.4. Consumer Credit

- 1.5. Loans

- 1.6. Other Service Types

-

2. End-User Type

- 2.1. Business Segment

- 2.2. Personal Segment

Challenger Banking in Middle East & Africa Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

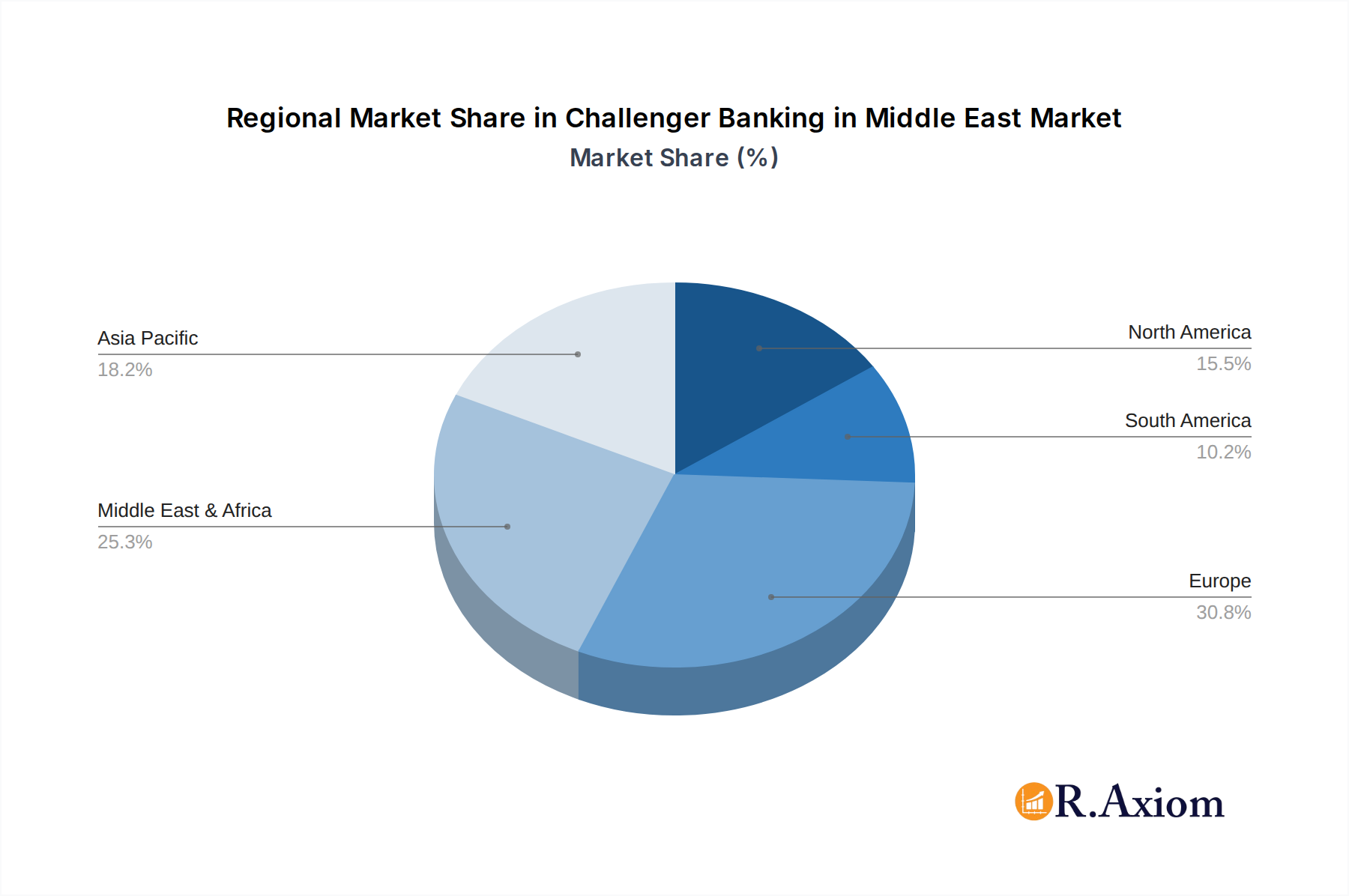

Challenger Banking in Middle East & Africa Market Regional Market Share

Geographic Coverage of Challenger Banking in Middle East & Africa Market

Challenger Banking in Middle East & Africa Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Payments

- 5.1.2. Savings Products

- 5.1.3. Current Accounts

- 5.1.4. Consumer Credit

- 5.1.5. Loans

- 5.1.6. Other Service Types

- 5.2. Market Analysis, Insights and Forecast - by End-User Type

- 5.2.1. Business Segment

- 5.2.2. Personal Segment

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Global Challenger Banking in Middle East & Africa Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Payments

- 6.1.2. Savings Products

- 6.1.3. Current Accounts

- 6.1.4. Consumer Credit

- 6.1.5. Loans

- 6.1.6. Other Service Types

- 6.2. Market Analysis, Insights and Forecast - by End-User Type

- 6.2.1. Business Segment

- 6.2.2. Personal Segment

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. North America Challenger Banking in Middle East & Africa Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Payments

- 7.1.2. Savings Products

- 7.1.3. Current Accounts

- 7.1.4. Consumer Credit

- 7.1.5. Loans

- 7.1.6. Other Service Types

- 7.2. Market Analysis, Insights and Forecast - by End-User Type

- 7.2.1. Business Segment

- 7.2.2. Personal Segment

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. South America Challenger Banking in Middle East & Africa Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Payments

- 8.1.2. Savings Products

- 8.1.3. Current Accounts

- 8.1.4. Consumer Credit

- 8.1.5. Loans

- 8.1.6. Other Service Types

- 8.2. Market Analysis, Insights and Forecast - by End-User Type

- 8.2.1. Business Segment

- 8.2.2. Personal Segment

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Europe Challenger Banking in Middle East & Africa Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Payments

- 9.1.2. Savings Products

- 9.1.3. Current Accounts

- 9.1.4. Consumer Credit

- 9.1.5. Loans

- 9.1.6. Other Service Types

- 9.2. Market Analysis, Insights and Forecast - by End-User Type

- 9.2.1. Business Segment

- 9.2.2. Personal Segment

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Middle East & Africa Challenger Banking in Middle East & Africa Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 10.1.1. Payments

- 10.1.2. Savings Products

- 10.1.3. Current Accounts

- 10.1.4. Consumer Credit

- 10.1.5. Loans

- 10.1.6. Other Service Types

- 10.2. Market Analysis, Insights and Forecast - by End-User Type

- 10.2.1. Business Segment

- 10.2.2. Personal Segment

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 11. Asia Pacific Challenger Banking in Middle East & Africa Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 11.1.1. Payments

- 11.1.2. Savings Products

- 11.1.3. Current Accounts

- 11.1.4. Consumer Credit

- 11.1.5. Loans

- 11.1.6. Other Service Types

- 11.2. Market Analysis, Insights and Forecast - by End-User Type

- 11.2.1. Business Segment

- 11.2.2. Personal Segment

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pepper

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Clearly

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Liv Bank

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Xpence

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Mashreq Neo

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Meem Bank

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 CBD Now

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hala

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MoneySmart

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Bank ABC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Pepper

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Challenger Banking in Middle East & Africa Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Challenger Banking in Middle East & Africa Market Revenue (Million), by Service Type 2025 & 2033

- Figure 3: North America Challenger Banking in Middle East & Africa Market Revenue Share (%), by Service Type 2025 & 2033

- Figure 4: North America Challenger Banking in Middle East & Africa Market Revenue (Million), by End-User Type 2025 & 2033

- Figure 5: North America Challenger Banking in Middle East & Africa Market Revenue Share (%), by End-User Type 2025 & 2033

- Figure 6: North America Challenger Banking in Middle East & Africa Market Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Challenger Banking in Middle East & Africa Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Challenger Banking in Middle East & Africa Market Revenue (Million), by Service Type 2025 & 2033

- Figure 9: South America Challenger Banking in Middle East & Africa Market Revenue Share (%), by Service Type 2025 & 2033

- Figure 10: South America Challenger Banking in Middle East & Africa Market Revenue (Million), by End-User Type 2025 & 2033

- Figure 11: South America Challenger Banking in Middle East & Africa Market Revenue Share (%), by End-User Type 2025 & 2033

- Figure 12: South America Challenger Banking in Middle East & Africa Market Revenue (Million), by Country 2025 & 2033

- Figure 13: South America Challenger Banking in Middle East & Africa Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Challenger Banking in Middle East & Africa Market Revenue (Million), by Service Type 2025 & 2033

- Figure 15: Europe Challenger Banking in Middle East & Africa Market Revenue Share (%), by Service Type 2025 & 2033

- Figure 16: Europe Challenger Banking in Middle East & Africa Market Revenue (Million), by End-User Type 2025 & 2033

- Figure 17: Europe Challenger Banking in Middle East & Africa Market Revenue Share (%), by End-User Type 2025 & 2033

- Figure 18: Europe Challenger Banking in Middle East & Africa Market Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Challenger Banking in Middle East & Africa Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue (Million), by Service Type 2025 & 2033

- Figure 21: Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue Share (%), by Service Type 2025 & 2033

- Figure 22: Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue (Million), by End-User Type 2025 & 2033

- Figure 23: Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue Share (%), by End-User Type 2025 & 2033

- Figure 24: Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Challenger Banking in Middle East & Africa Market Revenue (Million), by Service Type 2025 & 2033

- Figure 27: Asia Pacific Challenger Banking in Middle East & Africa Market Revenue Share (%), by Service Type 2025 & 2033

- Figure 28: Asia Pacific Challenger Banking in Middle East & Africa Market Revenue (Million), by End-User Type 2025 & 2033

- Figure 29: Asia Pacific Challenger Banking in Middle East & Africa Market Revenue Share (%), by End-User Type 2025 & 2033

- Figure 30: Asia Pacific Challenger Banking in Middle East & Africa Market Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Challenger Banking in Middle East & Africa Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Service Type 2020 & 2033

- Table 2: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by End-User Type 2020 & 2033

- Table 3: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Service Type 2020 & 2033

- Table 5: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by End-User Type 2020 & 2033

- Table 6: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Service Type 2020 & 2033

- Table 11: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by End-User Type 2020 & 2033

- Table 12: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Service Type 2020 & 2033

- Table 17: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by End-User Type 2020 & 2033

- Table 18: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Service Type 2020 & 2033

- Table 29: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by End-User Type 2020 & 2033

- Table 30: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Service Type 2020 & 2033

- Table 38: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by End-User Type 2020 & 2033

- Table 39: Global Challenger Banking in Middle East & Africa Market Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Challenger Banking in Middle East & Africa Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Challenger Banking in Middle East & Africa Market?

The projected CAGR is approximately 10.50%.

2. Which companies are prominent players in the Challenger Banking in Middle East & Africa Market?

Key companies in the market include Pepper, Clearly, Liv Bank, Xpence, Mashreq Neo, Meem Bank, CBD Now, Hala, MoneySmart, Bank ABC.

3. What are the main segments of the Challenger Banking in Middle East & Africa Market?

The market segments include Service Type, End-User Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 74.03 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Smartphone Penetration.

6. What are the notable trends driving market growth?

Large Unbanked Population in the region.

7. Are there any restraints impacting market growth?

Competition from Traditional Banks is Restraining the Market.

8. Can you provide examples of recent developments in the market?

September 2022: New challenger Wio Bank launched in the UAE. Wio Bank, the region's first platform bank, officially launched operations in the UAE, with its headquarters in Abu Dhabi.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Challenger Banking in Middle East & Africa Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Challenger Banking in Middle East & Africa Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Challenger Banking in Middle East & Africa Market?

To stay informed about further developments, trends, and reports in the Challenger Banking in Middle East & Africa Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence