Key Insights

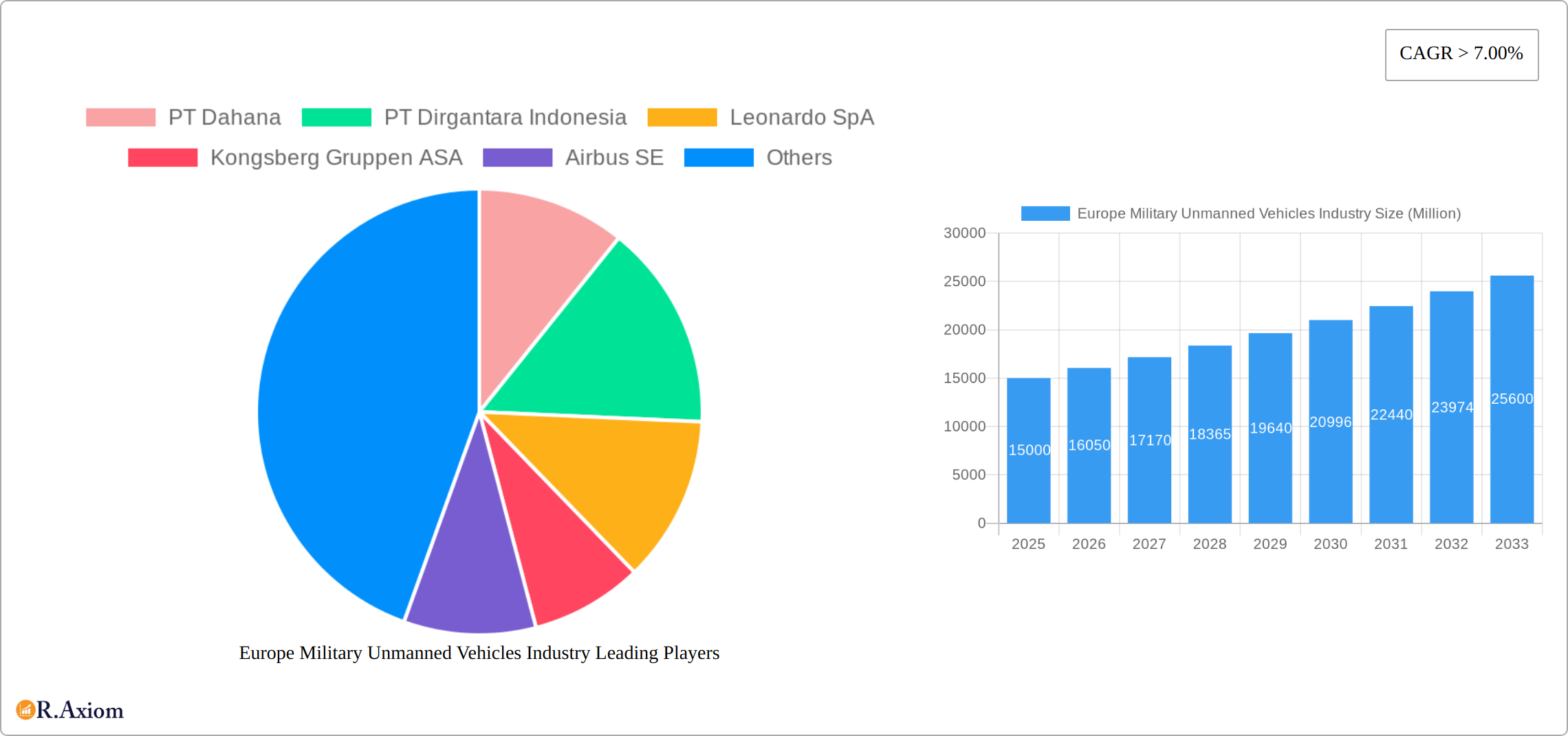

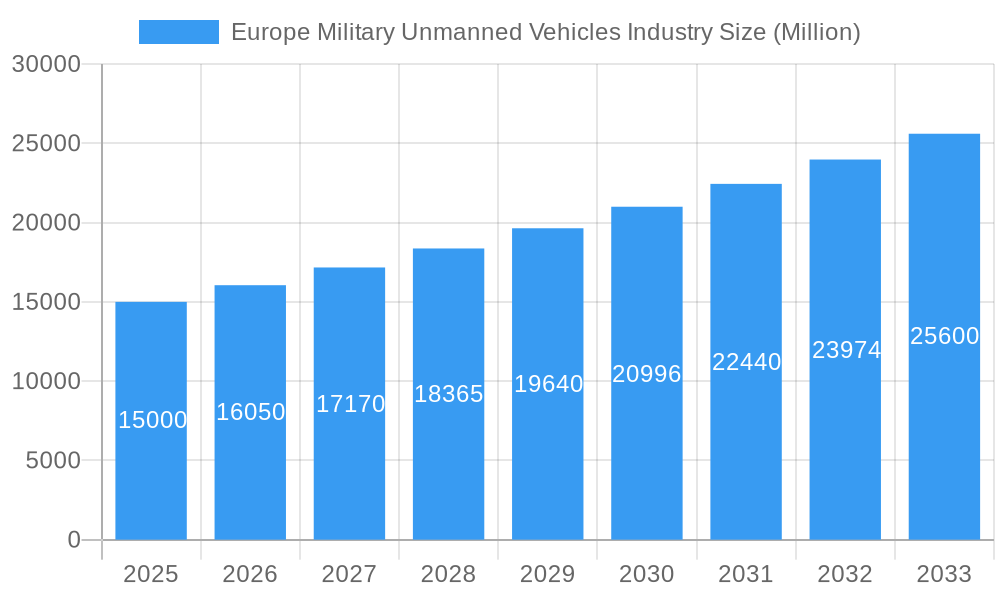

The European military unmanned vehicle (UV) market is experiencing significant expansion, propelled by increased defense spending, modernization efforts, and the inherent operational advantages of autonomous systems. The market, valued at $5.39 billion in 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.3% through 2033. Key growth drivers include the escalating demand for advanced surveillance and reconnaissance in challenging environments, and the expanding integration of Unmanned Aerial Vehicles (UAVs) for intelligence gathering and precision strikes. Furthermore, the adoption of Unmanned Ground Vehicles (UGVs) for critical tasks such as mine clearance, explosive ordnance disposal, and logistics support is accelerating. Ongoing advancements in autonomous system development, sensor technology, and platform interoperability are also contributing to this robust growth. Leading European defense nations, including Germany, France, the UK, and Italy, are instrumental in fostering innovation and investment within this vital sector. The competitive landscape features established defense giants like Airbus, Leonardo, and BAE Systems, alongside specialized regional manufacturers, fostering a dynamic environment.

Europe Military Unmanned Vehicles Industry Market Size (In Billion)

While UAVs currently lead the European military UV market share, Unmanned Ground Vehicles (UGVs) and Unmanned Maritime Vehicles (UMVs) are anticipated to witness substantial growth due to increased investment in autonomous navigation and enhanced payload capabilities. Potential market restraints include stringent regulations governing autonomous system deployment, cybersecurity vulnerabilities, and ethical considerations. However, continuous technological progress, rising military expenditures, and the demonstrable operational benefits of these systems are expected to surmount these challenges, ensuring sustained and significant growth for the European military unmanned vehicle industry throughout the forecast period.

Europe Military Unmanned Vehicles Industry Company Market Share

Europe Military Unmanned Vehicles Market Analysis: 2019-2033

This comprehensive report offers an in-depth analysis of the European military unmanned vehicles (UV) market from 2019 to 2033. It examines market size, segmentation, key players, growth drivers, challenges, and future opportunities, providing essential insights for stakeholders, investors, and policymakers. The analysis utilizes 2025 as the base year, with projections extending to 2033. The historical data covers the period from 2019 to 2024.

Europe Military Unmanned Vehicles Industry Market Concentration & Innovation

The European military unmanned vehicles market exhibits a moderately concentrated landscape, with a few major players holding significant market share. While precise figures are proprietary, we estimate that the top five companies collectively control approximately xx% of the market in 2025. This concentration is driven by high barriers to entry, including substantial R&D investment, stringent regulatory approvals, and the need for specialized expertise. However, the market also displays a high degree of innovation, spurred by advancements in artificial intelligence (AI), sensor technology, and autonomous navigation.

Regulatory frameworks, varying across European nations, significantly influence market dynamics. Harmonization efforts are ongoing, but inconsistencies remain, impacting market access and operational efficiency. Product substitution is limited, with specialized UVs catering to specific military needs. However, the emergence of more versatile, dual-use platforms is anticipated to increase substitutability in the forecast period. End-user trends reveal an increasing preference for autonomous and AI-powered systems, capable of operating in complex environments. Mergers and acquisitions (M&A) activities have played a role in shaping market concentration, with deal values in the range of xx Million in recent years. Notable acquisitions included [insert examples if available, otherwise state "xx acquisitions impacting market consolidation"].

Europe Military Unmanned Vehicles Industry Industry Trends & Insights

The European military unmanned vehicles market is experiencing robust growth, driven by increasing defense budgets across the region, a heightened focus on asymmetric warfare capabilities, and technological advancements. We project a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by several key factors: the rising adoption of UAVs for intelligence, surveillance, and reconnaissance (ISR) missions; increased demand for unmanned ground vehicles (UGVs) for mine clearance and other hazardous tasks; and the growing interest in unmanned surface and underwater vehicles (USVs/UUVs) for naval applications.

Technological disruptions, notably advancements in AI, machine learning, and sensor fusion, are significantly transforming the industry. These innovations enable greater autonomy, improved situational awareness, and enhanced operational effectiveness. Consumer preferences, reflecting military requirements, prioritize reliability, durability, payload capacity, and ease of operation. Competitive dynamics are intense, with established players focusing on innovation and expansion, while emerging companies challenge the status quo. Market penetration is steadily increasing across all vehicle types, with a particular surge in UAV adoption.

Dominant Markets & Segments in Europe Military Unmanned Vehicles Industry

The European military unmanned vehicle (UV) market is experiencing robust growth, although certain regions and segments are exhibiting more significant expansion than others. This dynamic landscape is shaped by a confluence of factors, including geopolitical instability, technological advancements, and evolving military doctrines.

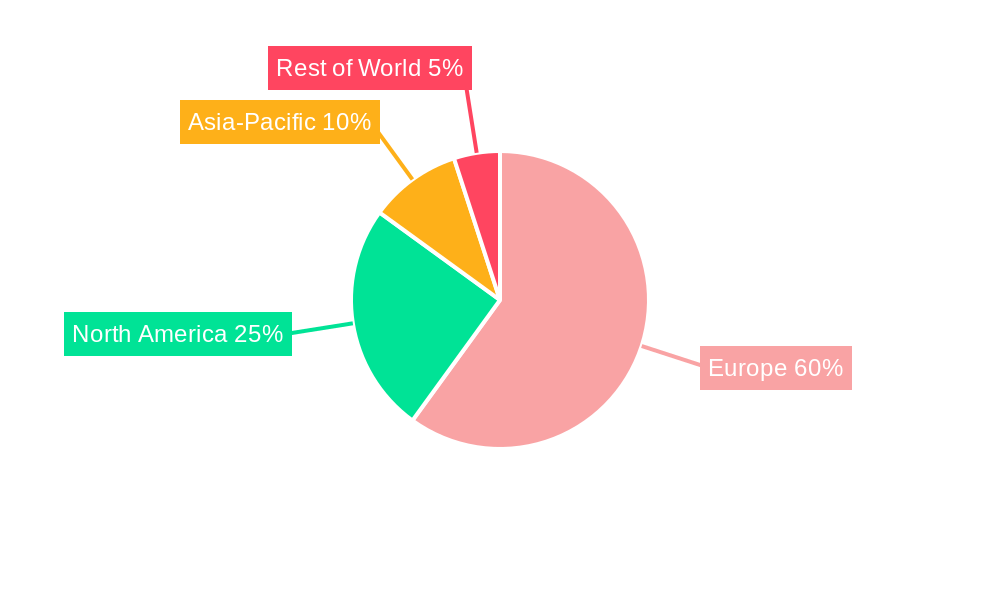

- Leading Region: Western Europe currently leads in military UV expenditure, driven by substantial defense budgets and heightened geopolitical concerns stemming from regional conflicts and global power dynamics. This region prioritizes technological superiority and invests heavily in research and development of advanced UV capabilities.

- Leading Country: The United Kingdom and France are vying for the top spot in terms of market share within Europe. The UK benefits from a strong domestic industry and significant defense spending, while France leverages its strategic geopolitical position and active participation in international collaborations to secure market dominance. Both nations actively support indigenous development and procurement of advanced UV systems.

Dominant Segments:

- Unmanned Aerial Vehicles (UAVs): This segment continues to dominate the European market, fueled by the versatile applications of UAVs across intelligence, surveillance, and reconnaissance (ISR), precision strikes, electronic warfare, and communications relay. Growth is driven by advancements in extended flight endurance, enhanced payload capacities, robust autonomous flight control systems, and the integration of advanced sensor technologies, including electro-optical/infrared (EO/IR), synthetic aperture radar (SAR), and hyperspectral imaging.

- Unmanned Ground Vehicles (UGVs): The UGV segment is experiencing rapid expansion, propelled by the increasing demand for autonomous systems in mine clearance, logistics, reconnaissance, and combat support roles. The development of AI-powered UGVs capable of navigating complex and hazardous terrains, coupled with improved payload integration, is accelerating market growth. Further growth is expected with integration of collaborative autonomy and swarm technologies.

- Unmanned Surface and Underwater Vehicles (USVs/UUVs): This segment showcases considerable growth potential, driven by the strategic importance of maritime security and the need for enhanced surveillance, mine countermeasures, and intelligence gathering capabilities. USVs are increasingly deployed for coastal surveillance and protection of critical maritime infrastructure, while UUVs play a crucial role in underwater warfare, intelligence gathering, and oceanographic research. The development of more robust and adaptable platforms for harsh marine environments is a key driver for market expansion.

Europe Military Unmanned Vehicles Industry Product Developments

Recent product innovations highlight a clear trend towards increased autonomy, improved sensor capabilities, and enhanced payload capacity across all UV types. AI-powered decision-making, enhanced communication systems, and swarm technologies are enhancing the effectiveness and adaptability of military UVs. These advancements offer significant competitive advantages, including improved operational efficiency, reduced risk to human personnel, and enhanced mission effectiveness.

Report Scope & Segmentation Analysis

This report segments the European military unmanned vehicles market based on vehicle type:

Unmanned Aerial Vehicles (UAVs): This segment includes fixed-wing, rotary-wing, and hybrid UAVs, with growth projections based on increasing demand for ISR and strike capabilities. Market size is projected to reach xx Million by 2033. Competitive dynamics are high, with established players facing increasing competition from smaller, innovative companies.

Unmanned Ground Vehicles (UGVs): This encompasses various types of UGVs, including robotic platforms for bomb disposal, reconnaissance, and logistics. Market size is estimated at xx Million in 2025, and expected to reach xx Million by 2033, driven by the need for autonomous systems in hazardous environments. Competition is expected to intensify as more companies enter the market.

Unmanned Surface and Underwater Vehicles (USVs/UUVs): This segment is projected to experience considerable growth due to increasing naval modernization efforts. Market size is expected to reach xx Million by 2033. Competitive dynamics are influenced by technological innovation and the integration of advanced sensor systems.

Key Drivers of Europe Military Unmanned Vehicles Industry Growth

The growth of the European military unmanned vehicle industry is propelled by several factors:

Increased Defense Spending: Rising geopolitical tensions and security concerns are leading to increased defense budgets across Europe, fueling demand for advanced military technologies, including UVs.

Technological Advancements: Innovations in AI, sensor technology, and autonomous navigation are enhancing the capabilities and operational effectiveness of UVs.

Operational Advantages: UVs offer numerous advantages over manned systems, including reduced risk to human personnel, increased operational flexibility, and cost-effectiveness in certain applications.

Challenges in the Europe Military Unmanned Vehicles Industry Sector

The European military unmanned vehicle market faces several challenges:

Regulatory Hurdles: Varying national regulations and standardization issues can hinder market access and create barriers for manufacturers.

Supply Chain Issues: Dependence on specific components and technologies can make the industry vulnerable to supply chain disruptions.

Cybersecurity Risks: The increasing connectivity of UVs raises concerns about cybersecurity vulnerabilities and potential threats.

Emerging Opportunities in Europe Military Unmanned Vehicles Industry

The European military unmanned vehicle market presents several significant opportunities:

Dual-Use Applications: The increasing versatility of UV technology opens doors to expanding into civilian applications, such as search and rescue, infrastructure inspection, and environmental monitoring.

Swarm Technologies: The development and deployment of swarm technologies, enabling coordinated operations of multiple UVs, present a significant opportunity for enhanced military effectiveness.

AI Integration: Further integration of AI and machine learning will dramatically improve the autonomy, situational awareness, and decision-making capabilities of UVs, driving market growth.

Leading Players in the Europe Military Unmanned Vehicles Industry Market

Key Developments in Europe Military Unmanned Vehicles Industry Industry

November 2021: The UK received a new General Atomics Aeronautical Systems Inc. (GA-ASI) MQ-9A Reaper UAV, signifying a significant investment in advanced UAV technology and enhancing the country's ISR capabilities.

June 2021: France announced plans to procure additional MQ-9 Reaper Block 5 UAVs, increasing its UAV fleet and expanding its precision strike capabilities. This demonstrates a commitment to modernizing its military with advanced UAV technology.

Strategic Outlook for Europe Military Unmanned Vehicles Industry Market

The future of the European military unmanned vehicle market appears bright, driven by sustained technological innovation, increasing defense budgets, and the growing recognition of UVs' operational advantages. The market is poised for substantial growth, with significant opportunities in the development and deployment of more autonomous, AI-powered systems. Continued advancements in sensor technology, communication systems, and swarm technologies will further enhance the capabilities and effectiveness of military UVs, shaping a more dynamic and technologically advanced defense landscape.

Europe Military Unmanned Vehicles Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Europe Military Unmanned Vehicles Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Military Unmanned Vehicles Industry Regional Market Share

Geographic Coverage of Europe Military Unmanned Vehicles Industry

Europe Military Unmanned Vehicles Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 6. Europe Military Unmanned Vehicles Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 PT Dahana

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 PT Dirgantara Indonesia

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Leonardo SpA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Kongsberg Gruppen ASA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Airbus SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Daewoo Shipbuilding & Marine Engineering Co Lt

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BAE Systems PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PT Pindad

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 SCYTALYS SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 PT Len Industri

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 FINCANTIERI SpA

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 PT PAL Indonesia

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 PT Dahana

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Military Unmanned Vehicles Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Military Unmanned Vehicles Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 2: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 8: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Europe Military Unmanned Vehicles Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Germany Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Netherlands Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Belgium Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Sweden Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Norway Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Poland Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Denmark Europe Military Unmanned Vehicles Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Military Unmanned Vehicles Industry?

The projected CAGR is approximately 15.3%.

2. Which companies are prominent players in the Europe Military Unmanned Vehicles Industry?

Key companies in the market include PT Dahana, PT Dirgantara Indonesia, Leonardo SpA, Kongsberg Gruppen ASA, Airbus SE, Daewoo Shipbuilding & Marine Engineering Co Lt, BAE Systems PLC, PT Pindad, SCYTALYS SA, PT Len Industri, FINCANTIERI SpA, PT PAL Indonesia.

3. What are the main segments of the Europe Military Unmanned Vehicles Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.39 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Number Of Air Passengers; Use Of Portable Electronic Devices.

6. What are the notable trends driving market growth?

Increasing Autonomy in Land Defense Vehicles.

7. Are there any restraints impacting market growth?

; High Cost Of Connectivity Equipments.

8. Can you provide examples of recent developments in the market?

In November 2021, the UK received a new General Atomics Aeronautical Systems Inc. (GA-ASI) MQ-9A Reaper unmanned aerial vehicle (UAV).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Military Unmanned Vehicles Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Military Unmanned Vehicles Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Military Unmanned Vehicles Industry?

To stay informed about further developments, trends, and reports in the Europe Military Unmanned Vehicles Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence