Key Insights

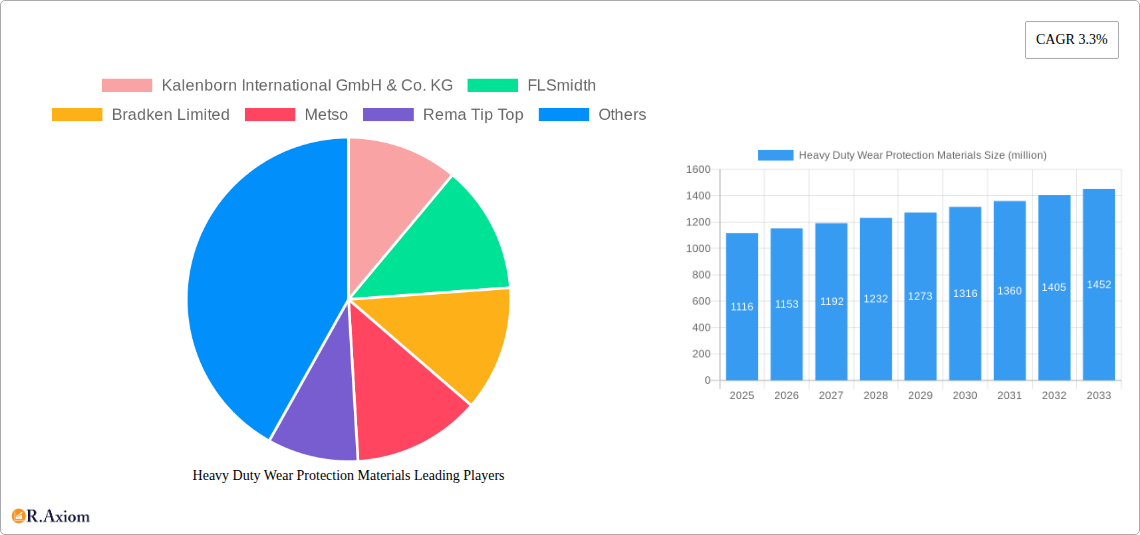

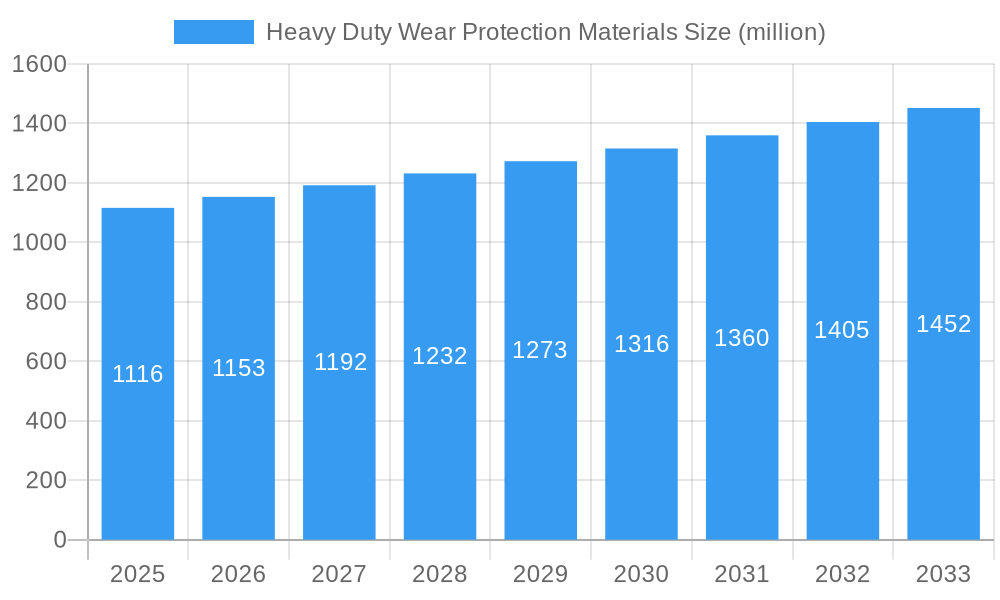

The global market for Heavy Duty Wear Protection Materials is projected to reach $1116 million by 2025, exhibiting a steady Compound Annual Growth Rate (CAGR) of 3.3% throughout the forecast period of 2025-2033. This robust growth is fueled by the increasing demand for advanced wear-resistant solutions across a wide spectrum of heavy industries. Key drivers include the escalating need for enhanced equipment lifespan and reduced maintenance costs in sectors such as mining, metallurgy, and concrete production. The continuous development of innovative materials, such as advanced ceramics and high-performance polymers, is also playing a pivotal role in expanding the market. Furthermore, stringent regulations aimed at improving industrial safety and operational efficiency are compelling manufacturers to adopt superior wear protection technologies, thereby stimulating market expansion.

Heavy Duty Wear Protection Materials Market Size (In Billion)

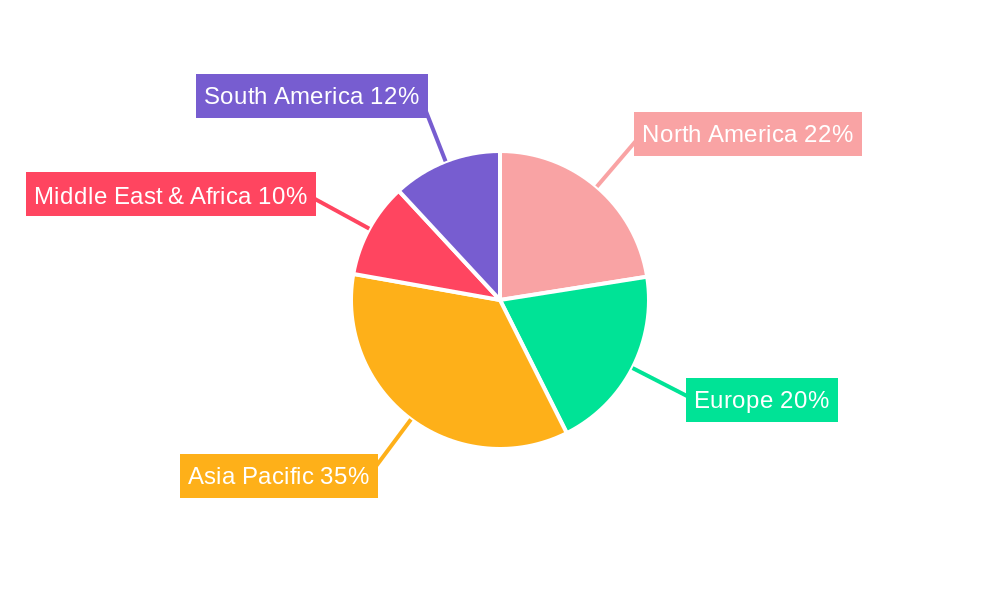

The market is segmented by application and type, reflecting diverse industrial needs. Application segments like Mining Plants, Metallurgical Plants, and Concrete and Cement Plants represent significant demand centers due to the abrasive nature of their operations. Similarly, the Type segments, including Metallic Lining, Ceramic Lining, and Rubber Lining, offer tailored solutions for various environmental and operational challenges. Geographically, the Asia Pacific region is expected to witness substantial growth, driven by rapid industrialization and infrastructure development in countries like China and India. North America and Europe remain mature markets with a consistent demand for high-quality wear protection materials, supported by established industrial bases and technological advancements. Key players are actively engaged in research and development, strategic partnerships, and market expansion initiatives to capitalize on these growth opportunities.

Heavy Duty Wear Protection Materials Company Market Share

Heavy Duty Wear Protection Materials Market Concentration & Innovation

The global Heavy Duty Wear Protection Materials market is characterized by a moderate to high concentration, with key players like Kalenborn International GmbH & Co. KG, FLSmidth, Bradken Limited, Metso, and Rema Tip Top holding significant market share, estimated to be over 60% collectively. Innovation is a primary driver, fueled by the increasing demand for advanced materials capable of withstanding extreme conditions in sectors such as mining, power generation, and waste incineration. Regulatory frameworks, particularly those concerning environmental protection and workplace safety, are influencing material development towards more durable and sustainable solutions. Product substitutes, while present, often fall short in performance for the most demanding applications. End-user trends point towards a preference for tailored solutions, emphasizing extended service life, reduced maintenance, and improved operational efficiency. Mergers and acquisitions (M&A) activity is a notable aspect of market dynamics, with recent deals valued in the tens of millions to hundreds of millions of dollars, reflecting consolidation and strategic expansion efforts. For example, recent M&A deal values are estimated to be in the range of xx million to xx million.

Heavy Duty Wear Protection Materials Industry Trends & Insights

The Heavy Duty Wear Protection Materials industry is poised for robust growth, driven by escalating industrialization and the continuous need to protect critical infrastructure from abrasive, erosive, and corrosive wear. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, reaching an estimated market size of over $15,000 million by the end of the forecast period. This expansion is largely propelled by significant investments in mining exploration and extraction activities, particularly for critical minerals essential for the green energy transition. Technological disruptions are playing a pivotal role, with advancements in material science leading to the development of novel composites, high-performance ceramics, and enhanced metallic alloys. These innovations offer superior wear resistance, higher temperature tolerance, and increased lifespan, thereby reducing downtime and operational costs for end-users. Consumer preferences are shifting towards sustainable and eco-friendly wear protection solutions, prompting manufacturers to focus on materials with lower environmental impact and longer serviceability. The competitive dynamics are intense, with established global players continuously investing in research and development to maintain their market edge. Companies like Sandvik Group and Trelleborg are at the forefront of these technological advancements. The market penetration for advanced wear protection materials is increasing across various industrial segments, as businesses recognize the long-term economic benefits of investing in high-quality protective solutions. The global market volume for heavy-duty wear protection materials is projected to reach over 2.5 million metric tons by 2033. Emerging economies, with their rapidly expanding industrial bases, represent significant growth pockets, further fueling the demand for these essential materials. The increasing focus on asset longevity and maintenance cost reduction across industries such as power plants and chemical plants is also a key contributor to market expansion.

Dominant Markets & Segments in Heavy Duty Wear Protection Materials

The Mining Plants segment is the dominant force within the Heavy Duty Wear Protection Materials market, driven by the inherently abrasive nature of ore extraction and processing. Global demand from this sector is estimated to account for over 35% of the total market revenue, projected to exceed $5,250 million by 2033. Key drivers for this dominance include:

- Infrastructure Development: Continuous global investment in mining infrastructure, from exploration to material handling, necessitates robust wear protection for equipment like crushers, conveyors, chutes, and screens. Countries with significant mining operations, such as Australia, China, and Canada, are major contributors to this demand, with market sizes in these regions estimated to be in the range of $700 million to $1,200 million respectively.

- Economic Policies: Favorable government policies and subsidies aimed at boosting mineral production and resource extraction significantly stimulate the demand for wear protection solutions.

- Technological Advancements in Mining: The adoption of more efficient and larger-scale mining operations requires wear-resistant materials capable of handling higher volumes and tougher materials.

Within the Type segmentation, Metallic Lining emerges as the leading category, commanding a substantial market share estimated at over 30%, valued at approximately $4,500 million by 2033. This dominance is attributed to the inherent strength, durability, and cost-effectiveness of metallic solutions in high-impact and high-abrasion environments found in mining and metallurgical plants. Companies like Bradken Limited and Metso are key players in this segment.

Metallurgical Plants represent another significant segment, with an estimated market share of 25%, projected to reach over $3,750 million by 2033. The high-temperature and corrosive environments involved in metal processing, smelting, and refining create a persistent need for advanced wear protection materials.

The Concrete and Cement Plants segment, while smaller than mining, is a vital contributor, with an estimated market share of 15% and a projected value of over $2,250 million by 2033. The abrasion from cement clinker, aggregates, and machinery operation drives the demand for specialized wear-resistant linings in grinding mills, mixers, and transport systems.

Power Plants, particularly those utilizing coal or waste incineration, also represent a substantial application area, estimated at 10% of the market, reaching over $1,500 million by 2033. The abrasive ash, flue gases, and high temperatures necessitate durable wear protection for components like boilers, scrubbers, and pipelines.

The Chemical Plants segment, though facing specific challenges related to chemical corrosion, still accounts for a notable market share of approximately 8%, projected to be over $1,200 million by 2033. Specialized materials are crucial for protecting equipment in the production of various chemicals, fertilizers, and petrochemicals.

The Others segment, encompassing applications in industries like sugar processing, pulp and paper, and general heavy industry, contributes the remaining market share, estimated at 7%, valued at over $1,050 million by 2033.

Heavy Duty Wear Protection Materials Product Developments

The Heavy Duty Wear Protection Materials market is experiencing a surge in product innovation. Companies are focusing on developing advanced ceramic composites with enhanced hardness and thermal shock resistance, as well as novel polymer-based linings offering superior flexibility and chemical resistance. Metallic lining technologies are evolving with the introduction of specialized alloys and wear plates designed for extreme abrasion and impact. These developments are driven by the need for longer service life, reduced maintenance downtime, and improved operational efficiency across demanding applications such as mining, power generation, and waste incineration. Competitive advantages are being gained through materials that offer superior performance under specific harsh conditions, a trend exemplified by the offerings from CeramTec and ITW Performance Polymers.

Report Scope & Segmentation Analysis

This report meticulously analyzes the global Heavy Duty Wear Protection Materials market across key application and type segments. The Application segmentation includes Mining Plants, Metallurgical Plants, Concrete and Cement Plants, Chemical Plants, Power Plants, Waste Incineration Plants, and Others, each offering unique wear challenges and material requirements. Growth projections for these segments range from 6% to 8.5% CAGR over the forecast period. The Type segmentation encompasses Metallic Lining, Ceramic Lining, Mineral Lining, Rubber Lining, and Others, providing insights into the prevalent material technologies and their market penetration. Market sizes for individual segments are estimated to range from $1,000 million to over $5,000 million, with competitive dynamics varying based on technological maturity and end-user industry growth.

Key Drivers of Heavy Duty Wear Protection Materials Growth

The growth of the Heavy Duty Wear Protection Materials market is propelled by several interconnected factors. Economic expansion and increasing industrial output, particularly in emerging economies, are driving higher demand for durable equipment and infrastructure, necessitating robust wear protection. Technological advancements in material science are yielding superior performing linings, offering extended lifespan and reduced maintenance costs. Furthermore, stringent regulations concerning equipment longevity and operational efficiency in industries like power generation and waste management are compelling businesses to invest in high-quality wear solutions. The transition towards renewable energy sources and the increased demand for critical minerals further amplify the need for advanced wear protection in mining operations, with an estimated xx million tons of materials processed annually requiring such protection.

Challenges in the Heavy Duty Wear Protection Materials Sector

The Heavy Duty Wear Protection Materials sector faces several significant challenges. High initial investment costs for advanced wear protection materials can be a barrier for some businesses, particularly SMEs. The complexity of material selection for highly specialized applications requires significant technical expertise, posing a challenge for end-users without dedicated engineering teams. Supply chain disruptions, influenced by raw material availability and geopolitical factors, can impact production timelines and costs, with potential cost increases of up to xx% for certain raw materials. Moreover, the stringent performance requirements and long service life expectations in some industries lead to extended product development cycles, slowing down the adoption of novel solutions.

Emerging Opportunities in Heavy Duty Wear Protection Materials

Emerging opportunities in the Heavy Duty Wear Protection Materials market are abundant, driven by the growing demand for sustainable solutions and the expanding scope of industrial applications. The circular economy trend is fostering innovation in recyclable and reusable wear protection materials. The rapid development of new energy technologies, such as advanced battery manufacturing and hydrogen production, presents new frontiers for specialized wear-resistant materials. Furthermore, the increasing focus on digitalization and smart manufacturing is creating opportunities for intelligent wear monitoring systems and predictive maintenance solutions integrated with wear protection materials. The burgeoning waste-to-energy sector and the ongoing need for infrastructure upgrades in developing nations also offer significant growth potential, with market expansion estimated at over $500 million in these regions.

Leading Players in the Heavy Duty Wear Protection Materials Market

- Kalenborn International GmbH & Co. KG

- FLSmidth

- Bradken Limited

- Metso

- Rema Tip Top

- Belzona

- Sandvik Group

- Trelleborg

- TEGA Industries

- CeramTec

- ITW Performance Polymers

- Oerlikon Metco

- Corrosion Engineering, Inc

- AGC Plibrico Co.,Ltd.

- Multotec

- GermanBelt Systems GmbH

- NewGen Group

- Scholten GmbH

- Guanxi Jushi Chemical Co., Ltd.

Key Developments in Heavy Duty Wear Protection Materials Industry

- 2024 February: Metso launches a new line of ceramic wear parts for high-abrasion crushing applications, enhancing equipment lifespan by an estimated 30%.

- 2023 December: Sandvik Group acquires a specialized wear protection solutions provider, strengthening its composite material portfolio. Deal value estimated at xx million.

- 2023 October: Rema Tip Top develops a new generation of rubber linings with improved chemical resistance for the chemical processing industry.

- 2023 August: Kalenborn International introduces a modular wear protection system for conveyor belt transfer points, reducing installation time by 20%.

- 2022 November: FLSmidth announces significant R&D investment in advanced metallic alloys for extreme wear environments in mining.

Strategic Outlook for Heavy Duty Wear Protection Materials Market

The strategic outlook for the Heavy Duty Wear Protection Materials market remains exceptionally positive, driven by persistent global industrial activity and the ongoing pursuit of operational efficiency and asset longevity. Key growth catalysts include the accelerating demand for raw materials for renewable energy technologies, necessitating advanced wear solutions in mining, and the continued need for robust protection in critical infrastructure sectors like power generation and waste management. Strategic focus will likely be on developing sustainable materials, expanding into emerging markets, and integrating digital solutions for enhanced wear monitoring and predictive maintenance. Investments in R&D for next-generation materials with superior performance characteristics will be crucial for maintaining competitive advantage. The market is projected to continue its upward trajectory, with opportunities for innovation and expansion valued at over $20,000 million by 2033.

Heavy Duty Wear Protection Materials Segmentation

-

1. Application

- 1.1. Mining Plants

- 1.2. Metallurgical Plants

- 1.3. Concrete and Cement Plants

- 1.4. Chemical Plants

- 1.5. Power Plants

- 1.6. Waste Incineration Plants

- 1.7. Others

-

2. Type

- 2.1. Metallic Lining

- 2.2. Ceramic Lining

- 2.3. Mineral Lining

- 2.4. Rubber Lining

- 2.5. Others

Heavy Duty Wear Protection Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Heavy Duty Wear Protection Materials Regional Market Share

Geographic Coverage of Heavy Duty Wear Protection Materials

Heavy Duty Wear Protection Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Mining Plants

- 5.1.2. Metallurgical Plants

- 5.1.3. Concrete and Cement Plants

- 5.1.4. Chemical Plants

- 5.1.5. Power Plants

- 5.1.6. Waste Incineration Plants

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Metallic Lining

- 5.2.2. Ceramic Lining

- 5.2.3. Mineral Lining

- 5.2.4. Rubber Lining

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Heavy Duty Wear Protection Materials Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Mining Plants

- 6.1.2. Metallurgical Plants

- 6.1.3. Concrete and Cement Plants

- 6.1.4. Chemical Plants

- 6.1.5. Power Plants

- 6.1.6. Waste Incineration Plants

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Metallic Lining

- 6.2.2. Ceramic Lining

- 6.2.3. Mineral Lining

- 6.2.4. Rubber Lining

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Heavy Duty Wear Protection Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Mining Plants

- 7.1.2. Metallurgical Plants

- 7.1.3. Concrete and Cement Plants

- 7.1.4. Chemical Plants

- 7.1.5. Power Plants

- 7.1.6. Waste Incineration Plants

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Metallic Lining

- 7.2.2. Ceramic Lining

- 7.2.3. Mineral Lining

- 7.2.4. Rubber Lining

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Heavy Duty Wear Protection Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Mining Plants

- 8.1.2. Metallurgical Plants

- 8.1.3. Concrete and Cement Plants

- 8.1.4. Chemical Plants

- 8.1.5. Power Plants

- 8.1.6. Waste Incineration Plants

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Metallic Lining

- 8.2.2. Ceramic Lining

- 8.2.3. Mineral Lining

- 8.2.4. Rubber Lining

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Heavy Duty Wear Protection Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Mining Plants

- 9.1.2. Metallurgical Plants

- 9.1.3. Concrete and Cement Plants

- 9.1.4. Chemical Plants

- 9.1.5. Power Plants

- 9.1.6. Waste Incineration Plants

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Metallic Lining

- 9.2.2. Ceramic Lining

- 9.2.3. Mineral Lining

- 9.2.4. Rubber Lining

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Heavy Duty Wear Protection Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Mining Plants

- 10.1.2. Metallurgical Plants

- 10.1.3. Concrete and Cement Plants

- 10.1.4. Chemical Plants

- 10.1.5. Power Plants

- 10.1.6. Waste Incineration Plants

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Metallic Lining

- 10.2.2. Ceramic Lining

- 10.2.3. Mineral Lining

- 10.2.4. Rubber Lining

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Heavy Duty Wear Protection Materials Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Mining Plants

- 11.1.2. Metallurgical Plants

- 11.1.3. Concrete and Cement Plants

- 11.1.4. Chemical Plants

- 11.1.5. Power Plants

- 11.1.6. Waste Incineration Plants

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Metallic Lining

- 11.2.2. Ceramic Lining

- 11.2.3. Mineral Lining

- 11.2.4. Rubber Lining

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Kalenborn International GmbH & Co. KG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FLSmidth

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bradken Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Metso

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rema Tip Top

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Belzona

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sandvik Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Trelleborg

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 TEGA Industries

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 CeramTec

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ITW Performance Polymers

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Oerlikon Metco

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Corrosion Engineering Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 AGC Plibrico Co.Ltd.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Multotec

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 GermanBelt Systems GmbH

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 NewGen Group

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Scholten GmbH

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Guanxi Jushi Chemical Co. Ltd.

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 Kalenborn International GmbH & Co. KG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Heavy Duty Wear Protection Materials Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Heavy Duty Wear Protection Materials Revenue (million), by Application 2025 & 2033

- Figure 3: North America Heavy Duty Wear Protection Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Heavy Duty Wear Protection Materials Revenue (million), by Type 2025 & 2033

- Figure 5: North America Heavy Duty Wear Protection Materials Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Heavy Duty Wear Protection Materials Revenue (million), by Country 2025 & 2033

- Figure 7: North America Heavy Duty Wear Protection Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Heavy Duty Wear Protection Materials Revenue (million), by Application 2025 & 2033

- Figure 9: South America Heavy Duty Wear Protection Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Heavy Duty Wear Protection Materials Revenue (million), by Type 2025 & 2033

- Figure 11: South America Heavy Duty Wear Protection Materials Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Heavy Duty Wear Protection Materials Revenue (million), by Country 2025 & 2033

- Figure 13: South America Heavy Duty Wear Protection Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Heavy Duty Wear Protection Materials Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Heavy Duty Wear Protection Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Heavy Duty Wear Protection Materials Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Heavy Duty Wear Protection Materials Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Heavy Duty Wear Protection Materials Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Heavy Duty Wear Protection Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Heavy Duty Wear Protection Materials Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Heavy Duty Wear Protection Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Heavy Duty Wear Protection Materials Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Heavy Duty Wear Protection Materials Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Heavy Duty Wear Protection Materials Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Heavy Duty Wear Protection Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Heavy Duty Wear Protection Materials Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Heavy Duty Wear Protection Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Heavy Duty Wear Protection Materials Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Heavy Duty Wear Protection Materials Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Heavy Duty Wear Protection Materials Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Heavy Duty Wear Protection Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Heavy Duty Wear Protection Materials Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Heavy Duty Wear Protection Materials Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Heavy Duty Wear Protection Materials?

The projected CAGR is approximately 3.3%.

2. Which companies are prominent players in the Heavy Duty Wear Protection Materials?

Key companies in the market include Kalenborn International GmbH & Co. KG, FLSmidth, Bradken Limited, Metso, Rema Tip Top, Belzona, Sandvik Group, Trelleborg, TEGA Industries, CeramTec, ITW Performance Polymers, Oerlikon Metco, Corrosion Engineering, Inc, AGC Plibrico Co.,Ltd., Multotec, GermanBelt Systems GmbH, NewGen Group, Scholten GmbH, Guanxi Jushi Chemical Co., Ltd..

3. What are the main segments of the Heavy Duty Wear Protection Materials?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1116 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Heavy Duty Wear Protection Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Heavy Duty Wear Protection Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Heavy Duty Wear Protection Materials?

To stay informed about further developments, trends, and reports in the Heavy Duty Wear Protection Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence