Key Insights

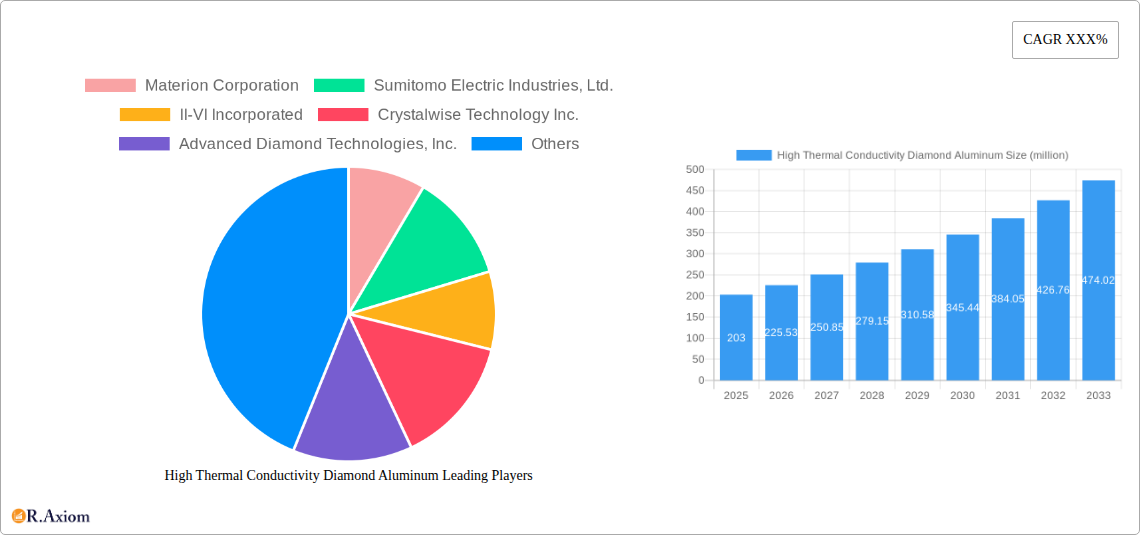

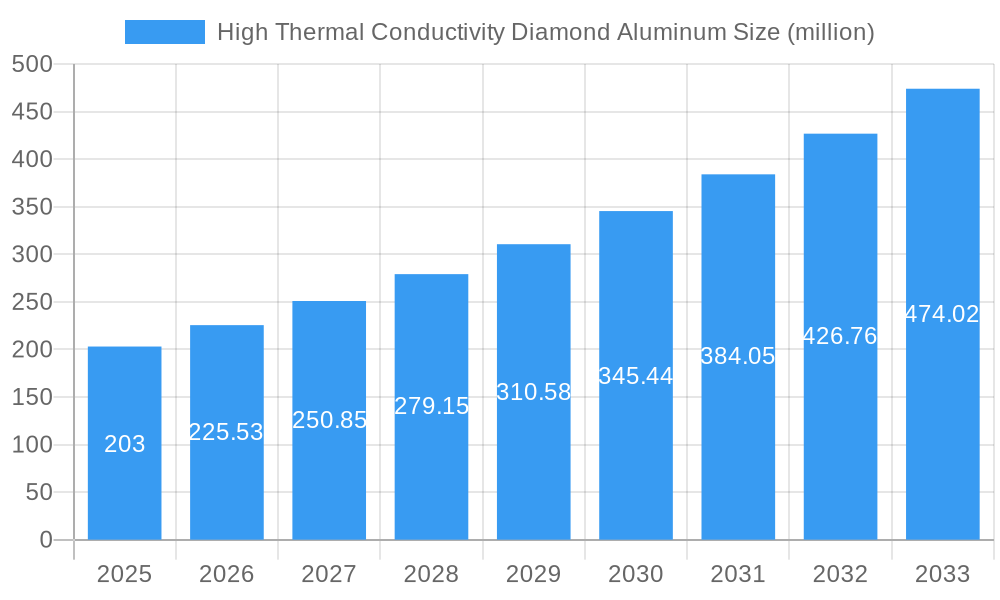

The High Thermal Conductivity Diamond Aluminum market is poised for significant expansion, driven by its exceptional heat dissipation capabilities critical for advanced electronic, aerospace, and energy applications. With a projected market size of $203 million in 2025, the industry is set to witness robust growth. This upward trajectory is fueled by the increasing demand for high-performance materials that can withstand extreme thermal conditions, enabling smaller, more powerful, and more efficient devices. Key drivers include the miniaturization of electronics, the development of next-generation aerospace components, and the growing adoption of advanced cooling solutions in high-power energy systems. The market's dynamism is further underscored by a compelling CAGR of 11.1%, indicating a strong and sustained expansion over the forecast period of 2025-2033.

High Thermal Conductivity Diamond Aluminum Market Size (In Million)

The market is segmented into various applications, with the Electronics Industry, Aerospace Industry, and Automotive Industry emerging as the dominant segments due to their continuous need for superior thermal management. The HTCDA Board and HTCDA Coating types are expected to see substantial demand, supporting the integration of these materials into diverse product designs. While the market benefits from strong growth drivers, potential restraints such as high manufacturing costs and the need for specialized fabrication techniques could influence the pace of adoption. However, ongoing technological advancements and increasing economies of scale are anticipated to mitigate these challenges. Key players like Materion Corporation, Sumitomo Electric Industries, Ltd., and II-VI Incorporated are actively investing in research and development, further stimulating innovation and market competitiveness, particularly across North America and Asia Pacific regions.

High Thermal Conductivity Diamond Aluminum Company Market Share

High Thermal Conductivity Diamond Aluminum Market Concentration & Innovation

The High Thermal Conductivity Diamond Aluminum (HTCDA) market exhibits a moderate to high concentration, with a few key players dominating technological advancements and market share. Materion Corporation, Sumitomo Electric Industries, Ltd., and II-VI Incorporated are prominent entities actively driving innovation through significant R&D investments. The pursuit of enhanced thermal management solutions across sectors like electronics, aerospace, and automotive fuels this innovation landscape. Regulatory frameworks, particularly those concerning material safety and environmental impact in advanced manufacturing, are beginning to shape development pathways, encouraging the adoption of more sustainable and efficient HTCDA formulations. Product substitutes, while present in the form of other advanced thermal interface materials, often fall short in delivering the synergistic benefits of diamond's superior thermal conductivity combined with aluminum's mechanical properties and cost-effectiveness. End-user trends are increasingly leaning towards miniaturization, higher power densities, and extended product lifecycles, all of which demand superior thermal dissipation capabilities, thus favoring HTCDA solutions. Merger and acquisition (M&A) activities, although not at exceptionally high values, are strategically focused on acquiring specialized technological expertise or expanding geographical reach. For instance, acquisitions of smaller, innovative material science firms by larger conglomerates have been observed, aiming to consolidate market position and accelerate product integration. While specific market share percentages are dynamic, the top 3-5 players collectively hold an estimated 60-70% of the advanced HTCDA market. M&A deal values, while not publicly disclosed for every transaction, are estimated to range from tens of millions to hundreds of millions of dollars for significant strategic acquisitions.

High Thermal Conductivity Diamond Aluminum Industry Trends & Insights

The High Thermal Conductivity Diamond Aluminum (HTCDA) industry is poised for significant expansion, driven by an escalating demand for superior thermal management solutions across a diverse range of high-growth sectors. The projected Compound Annual Growth Rate (CAGR) for the HTCDA market is estimated at a robust xx%, indicating substantial market penetration and sustained upward trajectory from the base year of 2025 through to 2033. This growth is fundamentally fueled by the relentless pursuit of higher performance and miniaturization in electronic devices, where efficient heat dissipation is paramount to preventing component failure and improving operational efficiency. The automotive industry, with the rapid electrification of vehicles and the integration of advanced driver-assistance systems (ADAS), presents a critical application area for HTCDA, particularly in battery thermal management and power electronics cooling. Similarly, the aerospace industry's stringent requirements for reliability and performance under extreme conditions necessitate advanced materials like HTCDA for critical components. The energy industry, encompassing renewable energy systems and advanced grid infrastructure, also benefits from HTCDA's ability to manage heat generated by high-power components.

Technological disruptions are continuously shaping the HTCDA landscape. Advancements in diamond synthesis, including Chemical Vapor Deposition (CVD) techniques, are leading to the production of higher quality and more uniform diamond particles, enhancing the thermal conductivity and mechanical integrity of HTCDA composites. Innovations in material processing and manufacturing are enabling the creation of novel HTCDA board and coating formats, tailored for specific application needs. The development of advanced bonding technologies is also crucial, ensuring optimal thermal transfer between diamond particles and the aluminum matrix. Consumer preferences, while indirectly influencing the HTCDA market, are driving the demand for more powerful, efficient, and durable electronic gadgets, which in turn necessitates better thermal management. Competitive dynamics are characterized by a blend of established material science giants and emerging specialized firms. Companies are investing heavily in R&D to develop proprietary technologies and secure intellectual property, aiming to gain a competitive edge. The market penetration of HTCDA is gradually increasing as awareness of its benefits grows and production costs become more competitive, allowing it to displace less efficient thermal management solutions. The estimated market penetration for HTCDA in its core applications is expected to reach xx% by 2033.

Dominant Markets & Segments in High Thermal Conductivity Diamond Aluminum

The Electronics Industry stands out as the most dominant market for High Thermal Conductivity Diamond Aluminum (HTCDA), propelled by the relentless evolution of consumer electronics, high-performance computing, and telecommunications. Within this vast segment, specific applications such as advanced semiconductor packaging, high-power LEDs, and liquid crystal displays (LCDs) are significant consumers of HTCDA. The relentless demand for faster, smaller, and more energy-efficient electronic devices directly translates into a critical need for superior thermal management, making HTCDA an indispensable material. Economic policies that encourage technological innovation and manufacturing growth further bolster this segment's dominance. The sheer volume of production and the continuous introduction of new electronic products create a consistent and growing demand for HTCDA.

The Aerospace Industry represents another significant, albeit more niche, dominant market for HTCDA. Here, the emphasis is on extreme reliability, weight reduction, and performance under harsh operating conditions. HTCDA finds applications in critical components such as avionic systems, power electronics for aircraft, and thermal management systems for spacecraft. The stringent safety regulations and the high cost of failure in this sector necessitate the use of advanced materials that offer unparalleled thermal performance and durability. Infrastructure development in advanced manufacturing and research facilities dedicated to aerospace materials indirectly supports the growth of HTCDA in this segment.

In terms of Type, the HTCDA Board segment currently holds the largest market share due to its versatility and widespread adoption in electronic assemblies and heat sinks. These boards provide a robust and integrated solution for thermal dissipation, offering excellent mechanical strength and ease of integration. The HTCDA Coating segment is experiencing rapid growth, driven by its application in enhancing the thermal performance of existing components and surfaces, offering a cost-effective way to improve thermal management. The HTCDA Powder segment, while smaller in current market size, is crucial as a foundational material for various composite manufacturing processes and is expected to see significant growth with advancements in additive manufacturing and material science.

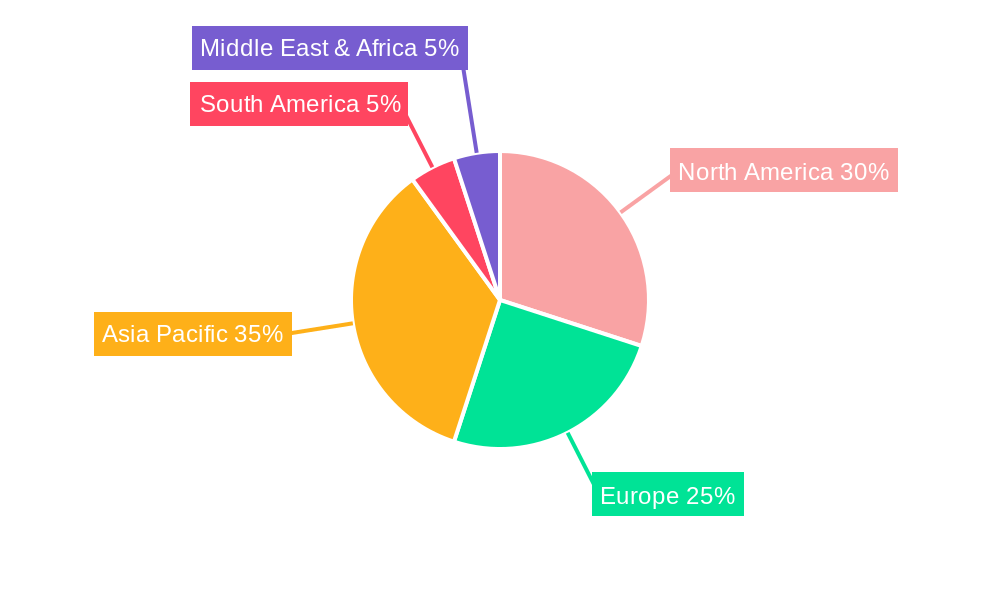

Geographically, North America and Asia-Pacific are the leading regions in the HTCDA market. North America's dominance is fueled by its strong presence in the aerospace, defense, and advanced electronics sectors, coupled with substantial R&D investments. Asia-Pacific, particularly countries like China, South Korea, and Japan, leads in high-volume electronics manufacturing, driving significant demand for HTCDA in consumer electronics, telecommunications, and automotive applications. Government initiatives supporting high-tech manufacturing and substantial investments in infrastructure development in these regions are key drivers.

High Thermal Conductivity Diamond Aluminum Product Developments

Recent product developments in High Thermal Conductivity Diamond Aluminum (HTCDA) have focused on enhancing thermal conductivity, improving material processability, and expanding application ranges. Innovations include novel composite formulations with higher diamond loading and optimized particle size distributions, leading to improved heat dissipation capabilities. The development of advanced HTCDA coatings with superior adhesion and wear resistance caters to specialized applications requiring robust thermal management on complex geometries. Furthermore, advancements in manufacturing techniques are enabling the creation of customized HTCDA boards with tailored thermal pathways and enhanced mechanical properties, meeting the specific demands of high-performance electronics and aerospace components. These developments underscore the market's commitment to pushing the boundaries of thermal management solutions.

Report Scope & Segmentation Analysis

This report meticulously segments the High Thermal Conductivity Diamond Aluminum (HTCDA) market across its key application areas and product types. The Electronics Industry segment, projected to reach a market size of approximately $xx million by 2033, encompasses applications from consumer electronics to high-performance computing, driven by miniaturization and increased power densities. The Aerospace Industry segment, estimated at $xx million by 2033, focuses on critical components requiring extreme reliability and thermal performance. The Automotive Industry segment, anticipated to grow at a CAGR of xx%, is driven by the electrification of vehicles and advanced power electronics. The Energy Industry, valued at $xx million by 2033, includes applications in renewable energy systems and advanced grid infrastructure. The Medical Industry segment, though smaller, is projected to expand due to the need for efficient cooling in advanced medical devices.

Within product types, the HTCDA Board segment is expected to hold the largest market share, estimated at $xx million by 2033, due to its widespread use in heat sinks and electronic assemblies. The HTCDA Coating segment, projected to reach $xx million by 2033, offers solutions for enhancing thermal performance on various surfaces and is witnessing robust growth. The HTCDA Powder segment, valued at $xx million by 2033, serves as a crucial precursor for composite manufacturing and is expected to see significant expansion with advancements in additive manufacturing. Competitive dynamics within each segment are influenced by technological innovation, cost-effectiveness, and application-specific performance requirements.

Key Drivers of High Thermal Conductivity Diamond Aluminum Growth

The growth of the High Thermal Conductivity Diamond Aluminum (HTCDA) market is primarily driven by several interconnected factors. Firstly, the relentless miniaturization and increasing power density of electronic devices across consumer electronics, telecommunications, and computing necessitate advanced thermal management solutions that can effectively dissipate heat. Secondly, the rapid electrification of the automotive industry, particularly electric vehicles (EVs), demands sophisticated thermal management systems for batteries, power electronics, and charging infrastructure, where HTCDA plays a crucial role. Thirdly, the aerospace and defense sectors' unyielding requirement for high reliability and performance under extreme conditions fuels the demand for HTCDA in critical avionics and power systems. Furthermore, advancements in diamond synthesis and composite manufacturing technologies are continuously improving the performance characteristics and cost-effectiveness of HTCDA, making it a more attractive option for a broader range of applications.

Challenges in the High Thermal Conductivity Diamond Aluminum Sector

Despite its significant growth potential, the High Thermal Conductivity Diamond Aluminum (HTCDA) sector faces several challenges. High production costs, particularly for high-purity synthetic diamond materials, remain a barrier to widespread adoption in cost-sensitive applications. The complex manufacturing processes involved in creating high-performance HTCDA composites also contribute to higher overall costs compared to conventional thermal management materials. Supply chain disruptions, especially concerning the availability of specialized diamond precursors, can impact production volumes and lead times. Additionally, the development of novel, highly efficient thermal interface materials by competitors poses an ongoing threat, requiring continuous innovation and product differentiation within the HTCDA market. Regulatory hurdles related to material sourcing, processing, and end-of-life management, while not currently a major restraint, could evolve and necessitate adaptation.

Emerging Opportunities in High Thermal Conductivity Diamond Aluminum

The High Thermal Conductivity Diamond Aluminum (HTCDA) market is ripe with emerging opportunities. The accelerating adoption of 5G technology and the development of next-generation communication infrastructure are creating a demand for HTCDA in high-frequency power amplifiers and base stations. The expansion of data centers and the growing need for efficient cooling of servers and networking equipment present a substantial opportunity. Furthermore, advancements in additive manufacturing (3D printing) are opening new avenues for creating complex, customized HTCDA components with optimized thermal pathways, catering to highly specialized applications in aerospace, defense, and medical devices. The increasing focus on energy efficiency in industrial processes and the development of advanced power electronics for renewable energy integration also represent significant growth prospects for HTCDA.

Leading Players in the High Thermal Conductivity Diamond Aluminum Market

- Materion Corporation

- Sumitomo Electric Industries, Ltd.

- II-VI Incorporated

- Crystalwise Technology Inc.

- Advanced Diamond Technologies, Inc.

- Element Six Limited

- Fraunhofer-Gesellschaft

- NanoDiamond Products Limited

- MDC Vacuum Products, LLC

- Ray Techniques Ltd.

- Crystallume Corporation

- Diamond Materials GmbH

- Henan Huanghe Whirlwind Co., Ltd.

- Scio Diamond Technology Corporation

- SP3 Diamond Technologies, Inc.

Key Developments in High Thermal Conductivity Diamond Aluminum Industry

- 2023/09: Materion Corporation announces advancements in its diamond-based thermal management materials, offering enhanced thermal conductivity for demanding electronic applications.

- 2023/07: Sumitomo Electric Industries, Ltd. unveils new HTCDA coatings designed for improved durability and thermal performance in automotive power electronics.

- 2022/12: II-VI Incorporated expands its portfolio of advanced materials, including new HTCDA solutions tailored for high-performance computing and telecommunications.

- 2022/05: Crystalwise Technology Inc. demonstrates novel methods for synthesizing high-quality diamond for advanced composite applications, boosting HTCDA potential.

- 2021/11: Advanced Diamond Technologies, Inc. secures new patents for its proprietary HTCDA manufacturing processes, enhancing its competitive edge.

- 2021/06: Element Six Limited introduces new grades of synthetic diamond powders optimized for thermal management applications.

Strategic Outlook for High Thermal Conductivity Diamond Aluminum Market

The strategic outlook for the High Thermal Conductivity Diamond Aluminum (HTCDA) market is exceptionally positive, fueled by ongoing technological advancements and increasing demand across critical industries. Growth catalysts include the persistent need for superior thermal management in ever-evolving electronics, the burgeoning electric vehicle market, and the stringent requirements of the aerospace and defense sectors. Continued investment in R&D for next-generation diamond synthesis and composite fabrication will be crucial for unlocking new application areas and improving material performance. Strategic partnerships and collaborations between material suppliers and end-users will foster innovation and accelerate the adoption of HTCDA solutions, solidifying its position as a key enabler of future technological progress.

High Thermal Conductivity Diamond Aluminum Segmentation

-

1. Application

- 1.1. Electronics Industry

- 1.2. Aerospace Industry

- 1.3. Automotive Industry

- 1.4. Energy Industry

- 1.5. Medical Industry

-

2. Type

- 2.1. HTCDA Board

- 2.2. HTCDA Coating

- 2.3. HTCDA Powder

High Thermal Conductivity Diamond Aluminum Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Thermal Conductivity Diamond Aluminum Regional Market Share

Geographic Coverage of High Thermal Conductivity Diamond Aluminum

High Thermal Conductivity Diamond Aluminum REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electronics Industry

- 5.1.2. Aerospace Industry

- 5.1.3. Automotive Industry

- 5.1.4. Energy Industry

- 5.1.5. Medical Industry

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. HTCDA Board

- 5.2.2. HTCDA Coating

- 5.2.3. HTCDA Powder

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global High Thermal Conductivity Diamond Aluminum Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electronics Industry

- 6.1.2. Aerospace Industry

- 6.1.3. Automotive Industry

- 6.1.4. Energy Industry

- 6.1.5. Medical Industry

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. HTCDA Board

- 6.2.2. HTCDA Coating

- 6.2.3. HTCDA Powder

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America High Thermal Conductivity Diamond Aluminum Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electronics Industry

- 7.1.2. Aerospace Industry

- 7.1.3. Automotive Industry

- 7.1.4. Energy Industry

- 7.1.5. Medical Industry

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. HTCDA Board

- 7.2.2. HTCDA Coating

- 7.2.3. HTCDA Powder

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America High Thermal Conductivity Diamond Aluminum Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electronics Industry

- 8.1.2. Aerospace Industry

- 8.1.3. Automotive Industry

- 8.1.4. Energy Industry

- 8.1.5. Medical Industry

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. HTCDA Board

- 8.2.2. HTCDA Coating

- 8.2.3. HTCDA Powder

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe High Thermal Conductivity Diamond Aluminum Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electronics Industry

- 9.1.2. Aerospace Industry

- 9.1.3. Automotive Industry

- 9.1.4. Energy Industry

- 9.1.5. Medical Industry

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. HTCDA Board

- 9.2.2. HTCDA Coating

- 9.2.3. HTCDA Powder

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa High Thermal Conductivity Diamond Aluminum Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electronics Industry

- 10.1.2. Aerospace Industry

- 10.1.3. Automotive Industry

- 10.1.4. Energy Industry

- 10.1.5. Medical Industry

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. HTCDA Board

- 10.2.2. HTCDA Coating

- 10.2.3. HTCDA Powder

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific High Thermal Conductivity Diamond Aluminum Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Electronics Industry

- 11.1.2. Aerospace Industry

- 11.1.3. Automotive Industry

- 11.1.4. Energy Industry

- 11.1.5. Medical Industry

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. HTCDA Board

- 11.2.2. HTCDA Coating

- 11.2.3. HTCDA Powder

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Materion Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sumitomo Electric Industries Ltd.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 II-VI Incorporated

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Crystalwise Technology Inc.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Advanced Diamond Technologies Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Element Six Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Fraunhofer-Gesellschaft

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NanoDiamond Products Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MDC Vacuum Products LLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ray Techniques Ltd.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Crystallume Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Diamond Materials GmbH

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Henan Huanghe Whirlwind Co. Ltd.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Scio Diamond Technology Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 SP3 Diamond Technologies Inc.

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Materion Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Thermal Conductivity Diamond Aluminum Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global High Thermal Conductivity Diamond Aluminum Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Thermal Conductivity Diamond Aluminum Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Thermal Conductivity Diamond Aluminum?

The projected CAGR is approximately 3.51%.

2. Which companies are prominent players in the High Thermal Conductivity Diamond Aluminum?

Key companies in the market include Materion Corporation, Sumitomo Electric Industries, Ltd., II-VI Incorporated, Crystalwise Technology Inc., Advanced Diamond Technologies, Inc., Element Six Limited, Fraunhofer-Gesellschaft, NanoDiamond Products Limited, MDC Vacuum Products, LLC, Ray Techniques Ltd., Crystallume Corporation, Diamond Materials GmbH, Henan Huanghe Whirlwind Co., Ltd., Scio Diamond Technology Corporation, SP3 Diamond Technologies, Inc..

3. What are the main segments of the High Thermal Conductivity Diamond Aluminum?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Thermal Conductivity Diamond Aluminum," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Thermal Conductivity Diamond Aluminum report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Thermal Conductivity Diamond Aluminum?

To stay informed about further developments, trends, and reports in the High Thermal Conductivity Diamond Aluminum, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence