Key Insights

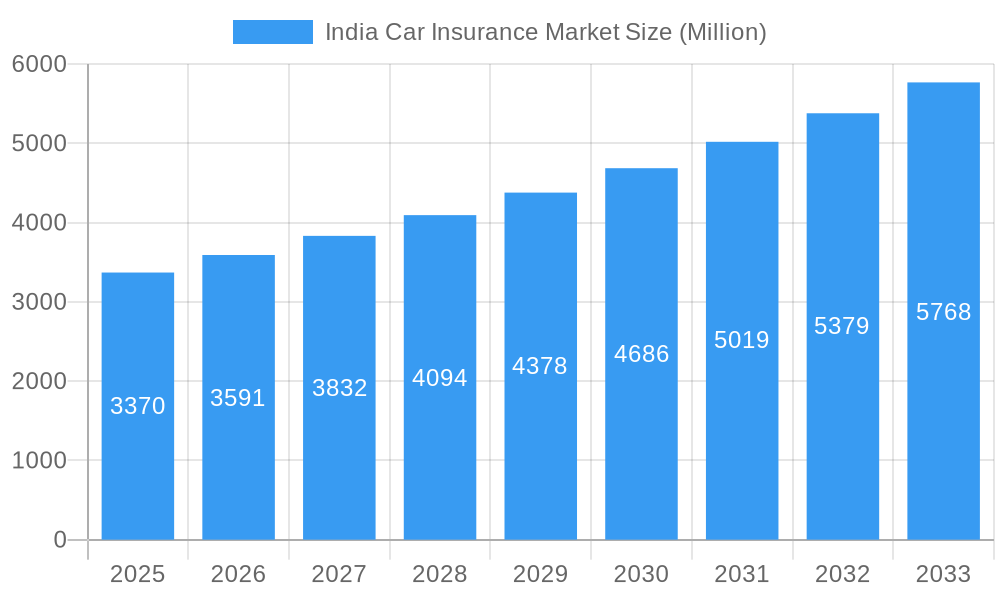

The India car insurance market, valued at $3.37 billion in 2025, is projected to experience robust growth, driven by rising vehicle ownership, increasing middle-class disposable incomes, and government initiatives promoting road safety. The market's Compound Annual Growth Rate (CAGR) of 6.56% from 2025 to 2033 indicates a significant expansion opportunity. Key growth drivers include the increasing affordability of vehicles, mandatory insurance regulations, and a growing awareness of the importance of financial protection against accidents and damages. The market is segmented by coverage type (Third-Party Liability, Comprehensive), vehicle type (Personal, Commercial), and distribution channels (Direct Sales, Agents, Brokers, Online). The dominance of established players like The New India Assurance, HDFC ERGO, and ICICI Lombard reflects the competitive landscape, although the rising popularity of online distribution channels is creating space for new entrants and fostering innovation in product offerings and customer service. Growth restraints include the prevalence of uninsured vehicles, challenges in claims processing, and the fluctuating cost of repairs. However, technological advancements, particularly in telematics and AI-powered risk assessment, are expected to mitigate these challenges and further propel market growth. The Asia-Pacific region, particularly India, presents a significant market opportunity due to its large and expanding car ownership base.

India Car Insurance Market Market Size (In Billion)

The forecast period (2025-2033) suggests a substantial increase in market value, driven by factors such as improved infrastructure, government regulations promoting insurance penetration, and evolving consumer preferences. While precise regional breakdowns within India are unavailable, it's reasonable to anticipate higher growth in urban areas compared to rural regions. Future market developments will likely center around the adoption of advanced technologies, greater use of data analytics for pricing and risk management, and competitive pricing strategies from both established and emerging insurers. The increasing emphasis on customer experience and digitalization of processes are also key factors influencing market dynamics. The market will continue to see competition among players, driving innovation and improved service offerings.

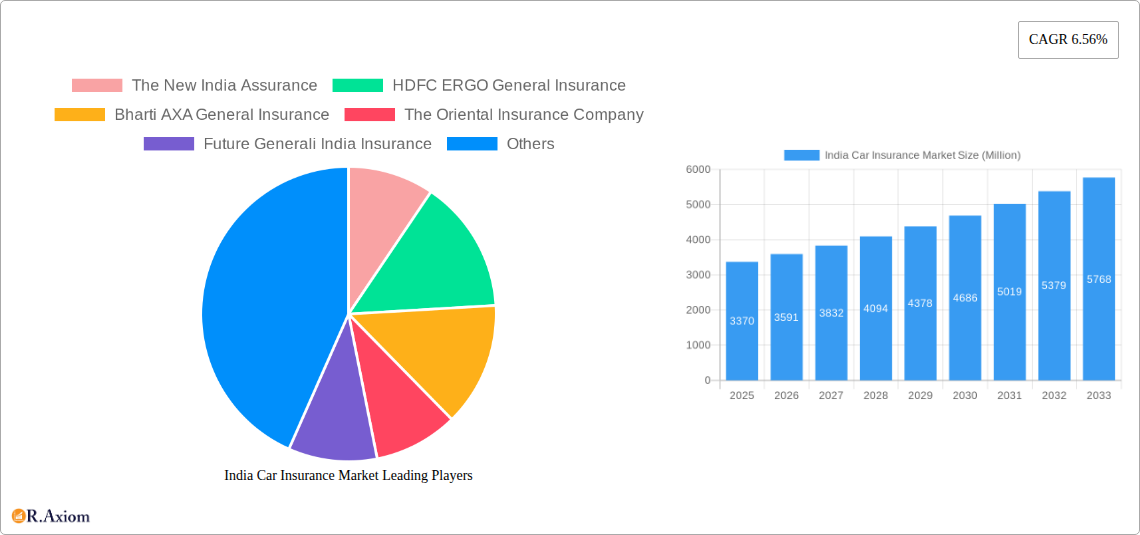

India Car Insurance Market Company Market Share

This comprehensive report provides a detailed analysis of the India car insurance market, offering valuable insights for industry stakeholders, investors, and strategic decision-makers. The report covers the period 2019-2033, with a focus on the base year 2025 and a forecast period of 2025-2033. Leveraging extensive market research, the report presents a granular view of market size, growth drivers, challenges, opportunities, and competitive landscape. High-traffic keywords such as "India car insurance market," "motor insurance India," "car insurance growth India," "Indian automobile insurance," and "insurtech India" are strategically incorporated throughout the report to enhance search engine optimization (SEO).

India Car Insurance Market Concentration & Innovation

This section analyzes the competitive intensity of the Indian car insurance market, highlighting key trends in innovation and market consolidation. The market is characterized by a mix of established players and emerging Insurtech companies, leading to a dynamic competitive landscape. The report examines market share distribution among leading players such as The New India Assurance, HDFC ERGO General Insurance, Bharti AXA General Insurance, The Oriental Insurance Company, Future Generali India Insurance, Tata AIG General Insurance, Universal Sompo General Insurance, IFFCO Tokio General Insurance, ICICI Lombard General Insurance, Royal Sundaram General Insurance, Bajaj Allianz General Insurance, and SBI General Insurance (list not exhaustive). Metrics like market concentration ratios (e.g., CR4, CR8) and Herfindahl-Hirschman Index (HHI) will quantify market concentration. Furthermore, the report will analyze the impact of mergers and acquisitions (M&A) activity on market dynamics, including deal values and their influence on market share. Analysis will cover innovation drivers such as technological advancements (telematics, AI-powered claims processing), regulatory changes, and evolving consumer preferences. The influence of product substitutes (e.g., alternative risk transfer mechanisms) and end-user trends (e.g., increasing digital adoption) will also be examined. The report will delve into the regulatory framework governing the Indian car insurance sector, including its impact on market structure and competition. This section concludes with a detailed overview of the recent M&A activities in the Indian car insurance sector, analyzing their implications for market consolidation and innovation. The total M&A deal value for the period 2019-2024 is estimated at xx Million.

India Car Insurance Market Industry Trends & Insights

This section delves into the key trends shaping the India car insurance market. The report will examine the Compound Annual Growth Rate (CAGR) for the historical period (2019-2024) and project the CAGR for the forecast period (2025-2033), providing insights into the market's growth trajectory. Market penetration rates for different car insurance products will also be analyzed. A detailed analysis of market growth drivers will be provided, focusing on factors such as rising car ownership, increasing disposable incomes, government regulations mandating car insurance, and growth in the commercial vehicle segment. This analysis will also explore the disruptive impact of technological advancements, including the rise of Insurtech companies and the adoption of digital distribution channels (online platforms, mobile apps). An examination of evolving consumer preferences, including the demand for customized insurance products and improved customer service, will be included. The competitive dynamics within the market will be analyzed, highlighting the strategies employed by leading players to gain market share. Specific examples of successful strategies and their impacts will be showcased. The role of government policies and regulations in shaping the market's growth trajectory will be explored in detail. The total market size in 2025 is estimated at xx Million.

Dominant Markets & Segments in India Car Insurance Market

This section identifies the dominant segments within the India car insurance market. The analysis is segmented across coverage (Third-Party Liability Coverage, Collision/Comprehensive/Other Optional Coverage), application (Personal Vehicles, Commercial Vehicles), and distribution channel (Direct Sales, Individual Agents, Brokers, Banks, Online, Other Distribution Channels).

By Coverage:

- Third-Party Liability Coverage: This segment is expected to dominate due to mandatory regulations. Key drivers include affordability and legal requirements.

- Collision/Comprehensive/Other Optional Coverage: Growth is driven by increasing awareness of comprehensive coverage benefits and rising vehicle values.

By Application:

- Personal Vehicles: This segment is the largest, driven by rising car ownership and disposable incomes. Key drivers include increasing urbanization and young population.

- Commercial Vehicles: This segment shows significant growth potential due to the expansion of logistics and e-commerce sectors. Key drivers include robust economic growth and infrastructure development.

By Distribution Channel:

- Individual Agents: This channel maintains dominance due to its strong personal relationships and wide reach.

- Online: This channel experiences rapid growth due to increased internet penetration and consumer preference for online convenience.

- Brokers: Brokers serve as intermediaries between insurers and customers, facilitating business.

- Banks: Banks act as distributors and offer bundled financial products.

- Direct Sales: Insurers leverage their online platforms and call centers for direct sales.

The report will provide a detailed analysis of the market share of each segment and forecast their growth prospects for the forecast period. Economic policies promoting vehicle ownership and infrastructure development play a crucial role in shaping the dominance of specific segments.

India Car Insurance Market Product Developments

The Indian car insurance market is witnessing significant product innovation, driven by technological advancements and evolving consumer needs. Insurers are increasingly offering customized policies with features tailored to individual customer profiles and driving behaviors. The introduction of 'Pay as You Drive' policies by companies like New India Assurance exemplifies this trend. Telematics technology is being integrated into insurance products, enabling usage-based pricing and risk assessment. The adoption of artificial intelligence (AI) and machine learning (ML) for fraud detection, claims processing, and customer service is enhancing efficiency and customer experience. These innovations are creating competitive advantages for insurers and improving the overall customer experience. These developments will be analyzed in the context of their market fit and long-term impact.

Report Scope & Segmentation Analysis

This report segments the Indian car insurance market based on coverage type (Third-Party Liability, Comprehensive), vehicle type (Personal, Commercial), and distribution channel (Direct Sales, Agents, Brokers, Banks, Online, Others). Each segment's market size, growth projections, and competitive dynamics are analyzed separately. The report projects a xx Million market size for Third-Party Liability Coverage in 2033, while Comprehensive coverage is projected to reach xx Million. Similarly, the report provides granular analysis for Personal and Commercial vehicle segments, along with a breakdown of market share across distribution channels.

Key Drivers of India Car Insurance Market Growth

Several factors fuel the growth of the India car insurance market. These include the rising number of vehicles on Indian roads, driven by increased purchasing power and government initiatives promoting vehicle ownership. Technological advancements, including the use of telematics and AI, are optimizing risk assessment and claims processing, driving efficiency and product innovation. Stringent regulatory frameworks mandating insurance coverage contribute significantly to market expansion. Furthermore, supportive government policies aimed at improving infrastructure and boosting economic activity positively impact the industry's growth.

Challenges in the India Car Insurance Market Sector

The India car insurance market faces several challenges. These include high claims ratios, resulting in higher premiums and lower profitability for insurers. Fraudulent claims remain a significant issue, impacting the financial health of the industry. The penetration of insurance in rural areas remains low, representing an untapped market but also posing challenges in terms of outreach and customer education. The intense competition among insurers creates pricing pressures. Additionally, stringent regulatory norms and compliance requirements present operational challenges. The impact of these challenges is reflected in the comparatively lower profit margins experienced by some companies.

Emerging Opportunities in India Car Insurance Market

Despite the challenges, significant opportunities exist in the India car insurance market. The burgeoning Insurtech sector offers immense potential for innovation, with the opportunity to deliver personalized, digital-first insurance experiences. Expansion into untapped rural markets presents significant growth potential. The increasing use of telematics offers avenues for usage-based insurance products and improved risk management. Partnerships between Insurtech companies and traditional insurers can foster growth and innovation. Furthermore, the rising adoption of electric vehicles opens new opportunities for specialized insurance products catering to this emerging segment.

Leading Players in the India Car Insurance Market Market

- The New India Assurance

- HDFC ERGO General Insurance

- Bharti AXA General Insurance

- The Oriental Insurance Company

- Future Generali India Insurance

- Tata AIG General Insurance

- Universal Sompo General Insurance

- IFFCO Tokio General Insurance

- ICICI Lombard General Insurance

- Royal Sundaram General Insurance

- Bajaj Allianz General Insurance

- SBI General Insurance

Key Developments in India Car Insurance Market Industry

- October 2022: Turtlefin partnered with Droom Technologies to offer motor insurance services to online car buyers. This expanded Turtlefin’s reach and broadened its customer base within the online car sales market.

- January 2023: New India Assurance launched a ‘Pay as You Drive’ policy, a usage-based insurance model. This innovation responds to consumer demand for more customized and cost-effective insurance options.

Strategic Outlook for India Car Insurance Market Market

The India car insurance market is poised for continued growth, driven by sustained economic development, increasing vehicle ownership, and the adoption of innovative technologies. The expansion of the Insurtech sector and evolving consumer preferences will shape the market's future. Strategic partnerships and product diversification will be key success factors for insurers in this dynamic environment. The market's potential is vast, with opportunities for both established players and new entrants to capture significant market share.

India Car Insurance Market Segmentation

-

1. Coverage

- 1.1. Third-Party Liability Coverage

- 1.2. Collision/Comprehensive/Other Optional Coverage

-

2. Application

- 2.1. Personal Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Direct Sales

- 3.2. Individual Agents

- 3.3. Brokers

- 3.4. Banks

- 3.5. Online

- 3.6. Other Distribution Channels

India Car Insurance Market Segmentation By Geography

- 1. India

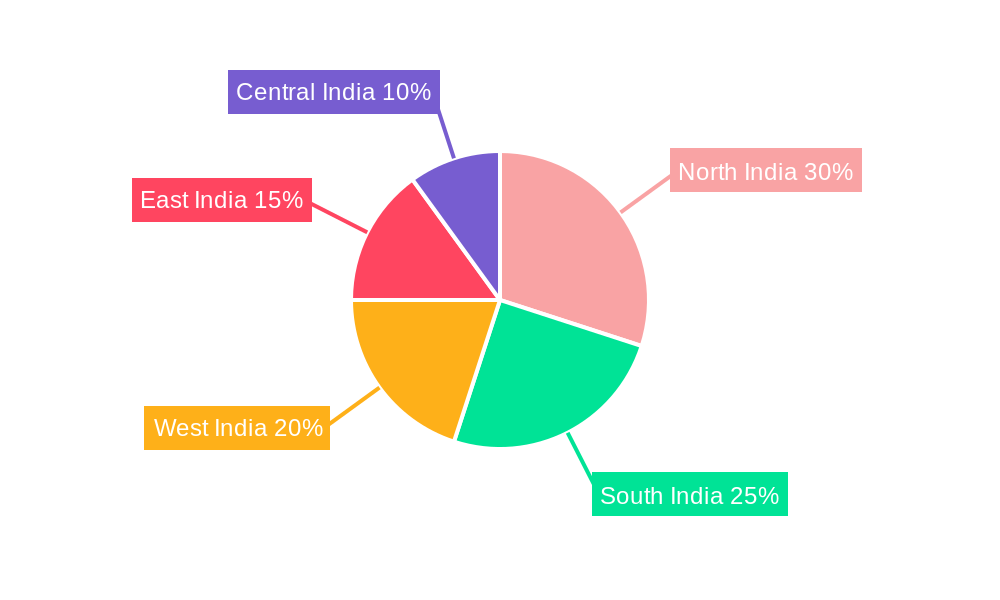

India Car Insurance Market Regional Market Share

Geographic Coverage of India Car Insurance Market

India Car Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 5.1.1. Third-Party Liability Coverage

- 5.1.2. Collision/Comprehensive/Other Optional Coverage

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct Sales

- 5.3.2. Individual Agents

- 5.3.3. Brokers

- 5.3.4. Banks

- 5.3.5. Online

- 5.3.6. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 6. India Car Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 6.1.1. Third-Party Liability Coverage

- 6.1.2. Collision/Comprehensive/Other Optional Coverage

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Personal Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Direct Sales

- 6.3.2. Individual Agents

- 6.3.3. Brokers

- 6.3.4. Banks

- 6.3.5. Online

- 6.3.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 The New India Assurance

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 HDFC ERGO General Insurance

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Bharti AXA General Insurance

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 The Oriental Insurance Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Future Generali India Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Tata AIG General Insurance

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Universal Sompo General Insurance

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 IFFCO Tokio General Insurance

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ICICI Lombard General Insurance**List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Royal Sundaram General Insurance

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Bajaj Allianz General Insurance

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 SBI General Insurance

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 The New India Assurance

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Car Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Car Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: India Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 2: India Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: India Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: India Car Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: India Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 6: India Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 7: India Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 8: India Car Insurance Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Car Insurance Market?

The projected CAGR is approximately 6.56%.

2. Which companies are prominent players in the India Car Insurance Market?

Key companies in the market include The New India Assurance, HDFC ERGO General Insurance, Bharti AXA General Insurance, The Oriental Insurance Company, Future Generali India Insurance, Tata AIG General Insurance, Universal Sompo General Insurance, IFFCO Tokio General Insurance, ICICI Lombard General Insurance**List Not Exhaustive, Royal Sundaram General Insurance, Bajaj Allianz General Insurance, SBI General Insurance.

3. What are the main segments of the India Car Insurance Market?

The market segments include Coverage, Application, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.37 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Sales of Cars in the India; Increase in Road Traffic Accidents.

6. What are the notable trends driving market growth?

Rise in Car Sales.

7. Are there any restraints impacting market growth?

Increase in Cost of Claims Made; Increase in False Claims and Scams.

8. Can you provide examples of recent developments in the market?

October 2022: Turtlefin, existing as India's insurtech company, partnered with Droom Technologies, an automobile e-commerce platform dealing with the buying and selling of used and new vehicles, to provide motor vehicle insurance services. The partnership expanded Turtlefin's options of providing motor insurance products to Droom’s customers purchasing four-wheelers online.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Car Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Car Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Car Insurance Market?

To stay informed about further developments, trends, and reports in the India Car Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence