Key Insights

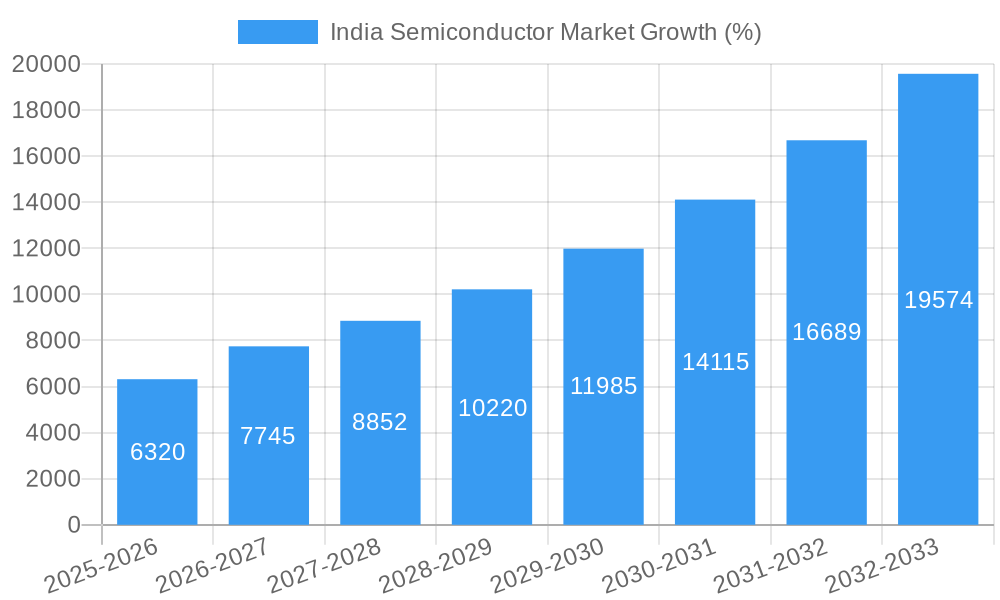

The India semiconductor market, valued at $39.5 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 16% from 2025 to 2033. This surge is driven by several key factors. The government's strong push for "Make in India" initiatives, aiming to boost domestic manufacturing and reduce reliance on imports, is a significant catalyst. Furthermore, the burgeoning demand for electronics across various sectors – from smartphones and automobiles to industrial automation and defense – fuels the market's expansion. Increased investments in research and development, coupled with the establishment of semiconductor fabrication plants by both domestic and international players, are also contributing to this growth trajectory. The presence of a large and skilled workforce further enhances India's competitiveness in this sector. However, challenges remain, including the need for significant infrastructure development, the high capital expenditure involved in semiconductor manufacturing, and the potential for global economic fluctuations to impact market growth.

Despite these challenges, the long-term outlook for the Indian semiconductor market remains positive. The government's strategic interventions, including the production-linked incentive (PLI) scheme and the development of semiconductor parks, are designed to mitigate risks and accelerate growth. The influx of foreign investment and collaborations between Indian and international companies are creating a vibrant ecosystem. The market segmentation, while not fully detailed in the provided data, likely includes memory chips, logic chips, integrated circuits, and other specialized semiconductor components, each exhibiting its own growth trajectory based on specific applications and technological advancements. This dynamic landscape suggests a promising future for India's semiconductor industry, positioning it as a key player in the global semiconductor value chain.

India Semiconductor Market: A Comprehensive Report (2019-2033)

This detailed report provides a comprehensive analysis of the India Semiconductor Market, covering the period from 2019 to 2033. It offers invaluable insights into market trends, growth drivers, challenges, and opportunities, empowering stakeholders to make informed strategic decisions. The report leverages extensive data analysis and incorporates the latest industry developments to present a future-ready outlook on this rapidly evolving sector. The Base Year for this report is 2025, with estimations for 2025 and forecasts extending to 2033, building upon historical data from 2019-2024. All values are expressed in Millions.

India Semiconductor Market Market Concentration & Innovation

The Indian semiconductor market exhibits a diverse landscape with varying degrees of concentration across different segments. While global giants like Intel Corporation, Qualcomm Incorporated, and Texas Instruments Incorporated hold significant market share, the emergence of domestic players like Tata Group and Vedanta Semiconductors Private Limited (VSPL) is reshaping the competitive dynamics. Market concentration is influenced by factors such as government initiatives, foreign direct investment (FDI), and the availability of skilled labor. Innovation is driven by the growing demand for advanced semiconductor technologies in various sectors, including consumer electronics, automotive, and telecommunications. Regulatory frameworks, including the government's Production-Linked Incentive (PLI) scheme, are designed to stimulate domestic manufacturing and innovation. The market experiences continuous technological advancements, with a notable emphasis on energy-efficient designs and specialized applications. The absence of readily available data prevents the provision of precise market share figures and M&A deal values at this time. However, future iterations of this report will include more detailed analysis. Substitutes for traditional silicon-based semiconductors are emerging, including gallium nitride (GaN) and silicon carbide (SiC) technologies, particularly for power electronics applications. The end-user preferences are consistently shifting towards higher performance, lower power consumption, and smaller form factors. Mergers and acquisitions (M&A) activities in the semiconductor industry are expected to remain significant, further shaping the market concentration. These activities can range from collaborations for joint development to outright acquisitions to expand market reach and gain access to crucial technologies.

India Semiconductor Market Industry Trends & Insights

The Indian semiconductor market is witnessing robust growth, driven by a surge in demand from various sectors, including consumer electronics, automotive, and telecommunications. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is estimated to be xx%. This growth is fueled by factors such as increasing smartphone adoption, the expanding automotive electronics market, and the government's push for digitalization. Technological disruptions, including the rise of artificial intelligence (AI) and the Internet of Things (IoT), are further stimulating demand for advanced semiconductor technologies. Consumer preferences are evolving towards more energy-efficient and feature-rich devices, pushing manufacturers to develop innovative semiconductor solutions. The competitive landscape is highly dynamic, with both established global players and emerging domestic companies vying for market share. Market penetration of advanced semiconductor technologies, like 5G and AI-specific chips, is expected to see a significant increase over the forecast period, although specific numbers are unavailable at this time and require further research.

Dominant Markets & Segments in India Semiconductor Market

While granular regional data needs further refinement, the overall market is experiencing widespread growth. Several states are emerging as hubs for semiconductor manufacturing and design, driven by supportive government policies and infrastructure development. The specific dominant regions and segments are still under analysis. However, the factors contributing to dominance will be analyzed in the final report and include:

- Economic Policies: Government initiatives like the PLI scheme are key drivers, offering substantial financial incentives to boost domestic semiconductor manufacturing.

- Infrastructure: Investments in infrastructure, including power and water supply, are crucial for attracting semiconductor manufacturers.

- Skilled Workforce: Availability of skilled engineers and technicians is essential for successful semiconductor operations.

The dominance analysis will delve deeper into specific regions and segments once complete data is accessible and analyzed.

India Semiconductor Market Product Developments

The Indian semiconductor market is witnessing significant product innovations, driven by the rising demand for advanced technologies like AI, 5G, and IoT. Companies are focusing on developing energy-efficient, high-performance chips catering to diverse applications, including smartphones, automobiles, and industrial automation. These innovations are enhancing the capabilities of devices and systems across various industries, leading to improved performance, efficiency, and functionality. A competitive advantage is gained through superior design, manufacturing capabilities, and strategic partnerships.

Report Scope & Segmentation Analysis

This report comprehensively segments the Indian semiconductor market based on several factors, enabling a granular understanding of market dynamics. The segments include detailed analysis of various semiconductor types, applications, end-users, and geographical regions. Each segment will have projected growth rates, market size estimations, and analysis of competitive intensity. The detailed segmentation will be presented in the full report, which is currently under development and will include precise market sizing and projections.

Key Drivers of India Semiconductor Market Growth

The growth of the Indian semiconductor market is propelled by several key factors:

- Government Initiatives: The Indian government's focus on promoting domestic manufacturing through initiatives like the PLI scheme significantly drives investment and production.

- Technological Advancements: The rapid advancement of technologies like AI, 5G, and IoT boosts demand for sophisticated semiconductor components.

- Economic Growth: India's sustained economic growth fuels demand across various sectors, contributing to the increased need for semiconductors.

Challenges in the India Semiconductor Market Sector

The Indian semiconductor sector faces certain challenges:

- Supply Chain Disruptions: Dependence on global supply chains makes the industry vulnerable to disruptions caused by geopolitical instability or natural disasters.

- Talent Acquisition: Finding and retaining skilled professionals remains a crucial hurdle for companies operating in this specialized field.

- High Capital Investment: The semiconductor manufacturing sector requires large upfront investments in state-of-the-art infrastructure and technology.

Emerging Opportunities in India Semiconductor Market

The Indian semiconductor market presents several compelling opportunities:

- Growth of Domestic Manufacturing: Government incentives and rising demand create significant opportunities for local semiconductor manufacturers.

- Focus on Specialized Chips: Demand for specialized chips for AI, 5G, and IoT applications presents a major growth area.

- Expansion into Emerging Markets: India's large and growing market provides opportunities for companies to penetrate new consumer segments.

Leading Players in the India Semiconductor Market Market

- Tata Group

- Bharat Electronics Limited

- Moschip Semiconductor Technologies

- Vedanta Semiconductors Private Limited (VSPL)

- HCL Technologies

- ASM Technologies Ltd

- Applied Materials India Pvt Ltd

- Hon Hai Technology Group (Foxconn)

- Broadcom Inc

- NXP Semiconductors

- ROHM Semiconductor

- Infineon Technologies

- Renesas Electronics

- STMicroelectronics

- Powerchip Semiconductor Manufacturing Corp (PSMC)

- AMD Group

- Intel Corporation

- Samsung Electronics Co Ltd

- Qualcomm Incorporated

- Micron Technology Inc

- Texas Instruments Incorporated

- Mediatek Inc

Key Developments in India Semiconductor Market Industry

July 2024: AMD partnered with SINE at IIT Bombay, providing grants to startups developing energy-efficient SNN chips. Numelo Technologies received the first grant. This signifies a significant boost to the innovation ecosystem within India's semiconductor industry.

July 2024: Horiba, a USD 2.5 billion company, considered establishing a unit in India to serve the burgeoning fab plants, OSAT, and ATMP players. This indicates growing confidence in India's semiconductor manufacturing capabilities and expanding global market access.

Strategic Outlook for India Semiconductor Market Market

The Indian semiconductor market holds immense potential for future growth, fueled by government support, technological advancements, and strong domestic demand. The increasing adoption of advanced technologies like AI, 5G, and IoT will further drive market expansion. Strategic partnerships between domestic and international players will be instrumental in shaping the future landscape. The market is poised for significant expansion, driven by both domestic consumption and the increasing role of India in the global semiconductor supply chain.

India Semiconductor Market Segmentation

-

1. Semiconductor Device Type

- 1.1. Discrete Semiconductor

- 1.2. Optoelectronics

- 1.3. Sensors and Actuators

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Micro

- 1.4.3. Logic

- 1.4.4. Memory

-

2. End-user Industry

- 2.1. Computer

- 2.2. Communication (Includes Wireline and Wireless)

- 2.3. Automotive

- 2.4. Consumer

- 2.5. Other En

India Semiconductor Market Segmentation By Geography

- 1. India

India Semiconductor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 16.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Automotive Industry and EV Demand; Smartphone and Consumer Electronics Demand Growth; Growing Telecom Infrastructure Augmented by 5G and Fixed Internet Connections

- 3.3. Market Restrains

- 3.3.1. Growing Automotive Industry and EV Demand; Smartphone and Consumer Electronics Demand Growth; Growing Telecom Infrastructure Augmented by 5G and Fixed Internet Connections

- 3.4. Market Trends

- 3.4.1. The Sensors and Actuators Segment is Expected to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Semiconductor Device Type

- 5.1.1. Discrete Semiconductor

- 5.1.2. Optoelectronics

- 5.1.3. Sensors and Actuators

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Micro

- 5.1.4.3. Logic

- 5.1.4.4. Memory

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Computer

- 5.2.2. Communication (Includes Wireline and Wireless)

- 5.2.3. Automotive

- 5.2.4. Consumer

- 5.2.5. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Semiconductor Device Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Tata Group

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Bharat Electronics Limited

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Moschip Semiconductor Technologies

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Vedanta Semiconductors Private Limited (VSPL)

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 HCL Technologies

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 ASM Technologies Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Applied Materials India Pvt Ltd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Hon Hai Technology Group (Foxconn)

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Broadcom Inc

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 NXP Semiconductors

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 ROHM Semiconductor

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Infineon Technologies

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Renesas Electronics

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 STMicroelectronics

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Powerchip Semiconductor Manufacturing Corp (PSMC)

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 AMD Group

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 Intel Corporation

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 Samsung Electronics Co Ltd

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Qualcomm Incorporated

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Micron Technology Inc

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.21 Texas Instruments Incorporated

- 6.2.21.1. Overview

- 6.2.21.2. Products

- 6.2.21.3. SWOT Analysis

- 6.2.21.4. Recent Developments

- 6.2.21.5. Financials (Based on Availability)

- 6.2.22 Mediatek Inc

- 6.2.22.1. Overview

- 6.2.22.2. Products

- 6.2.22.3. SWOT Analysis

- 6.2.22.4. Recent Developments

- 6.2.22.5. Financials (Based on Availability)

- 6.2.1 Tata Group

List of Figures

- Figure 1: India Semiconductor Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Semiconductor Market Share (%) by Company 2024

List of Tables

- Table 1: India Semiconductor Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Semiconductor Market Volume Billion Forecast, by Region 2019 & 2032

- Table 3: India Semiconductor Market Revenue Million Forecast, by Semiconductor Device Type 2019 & 2032

- Table 4: India Semiconductor Market Volume Billion Forecast, by Semiconductor Device Type 2019 & 2032

- Table 5: India Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 6: India Semiconductor Market Volume Billion Forecast, by End-user Industry 2019 & 2032

- Table 7: India Semiconductor Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: India Semiconductor Market Volume Billion Forecast, by Region 2019 & 2032

- Table 9: India Semiconductor Market Revenue Million Forecast, by Semiconductor Device Type 2019 & 2032

- Table 10: India Semiconductor Market Volume Billion Forecast, by Semiconductor Device Type 2019 & 2032

- Table 11: India Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 12: India Semiconductor Market Volume Billion Forecast, by End-user Industry 2019 & 2032

- Table 13: India Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 14: India Semiconductor Market Volume Billion Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Semiconductor Market?

The projected CAGR is approximately 16.00%.

2. Which companies are prominent players in the India Semiconductor Market?

Key companies in the market include Tata Group, Bharat Electronics Limited, Moschip Semiconductor Technologies, Vedanta Semiconductors Private Limited (VSPL), HCL Technologies, ASM Technologies Ltd, Applied Materials India Pvt Ltd, Hon Hai Technology Group (Foxconn), Broadcom Inc, NXP Semiconductors, ROHM Semiconductor, Infineon Technologies, Renesas Electronics, STMicroelectronics, Powerchip Semiconductor Manufacturing Corp (PSMC), AMD Group, Intel Corporation, Samsung Electronics Co Ltd, Qualcomm Incorporated, Micron Technology Inc, Texas Instruments Incorporated, Mediatek Inc.

3. What are the main segments of the India Semiconductor Market?

The market segments include Semiconductor Device Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.5 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Automotive Industry and EV Demand; Smartphone and Consumer Electronics Demand Growth; Growing Telecom Infrastructure Augmented by 5G and Fixed Internet Connections.

6. What are the notable trends driving market growth?

The Sensors and Actuators Segment is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Growing Automotive Industry and EV Demand; Smartphone and Consumer Electronics Demand Growth; Growing Telecom Infrastructure Augmented by 5G and Fixed Internet Connections.

8. Can you provide examples of recent developments in the market?

July 2024: AMD announced a partnership with the Society for Innovation and Entrepreneurship (SINE) at IIT Bombay. Through this collaboration, AMD will provide grants to startups incubated at IIT Bombay focused on developing energy-efficient Spiking Neural Network (SNN) chips. These startups will be working on innovative ways to decrease the energy consumption of traditional neural networks. As part of this partnership, Numelo Technologies was awarded the first grant to develop SNN chips using ultralow power quantum tunneling on silicon-on-insulator (SOI) technology.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Semiconductor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Semiconductor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Semiconductor Market?

To stay informed about further developments, trends, and reports in the India Semiconductor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence