Key Insights

The mobile phone semiconductor industry, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by several key factors. The increasing demand for high-performance smartphones with advanced features like 5G connectivity, improved cameras, and enhanced processing power fuels the need for sophisticated semiconductors. Innovation in areas such as Artificial Intelligence (AI) and machine learning within mobile devices further contributes to this growth. The consistent introduction of new smartphone models with improved specifications necessitates continuous upgrades in semiconductor technology, creating a strong demand for higher-capacity memory chips, faster processors, and more efficient power management ICs. While supply chain disruptions and geopolitical uncertainties could pose temporary challenges, the long-term outlook remains positive, fueled by emerging markets and increasing smartphone penetration globally. Segment-wise, mobile processors and memory chips are anticipated to dominate the market, with a significant contribution from Logic chips. Key players like Qualcomm, Samsung, and MediaTek are expected to maintain their leading positions, while smaller companies continue to innovate and carve out niche markets. The 7.49% CAGR projected until 2033 signifies a sustained period of expansion.

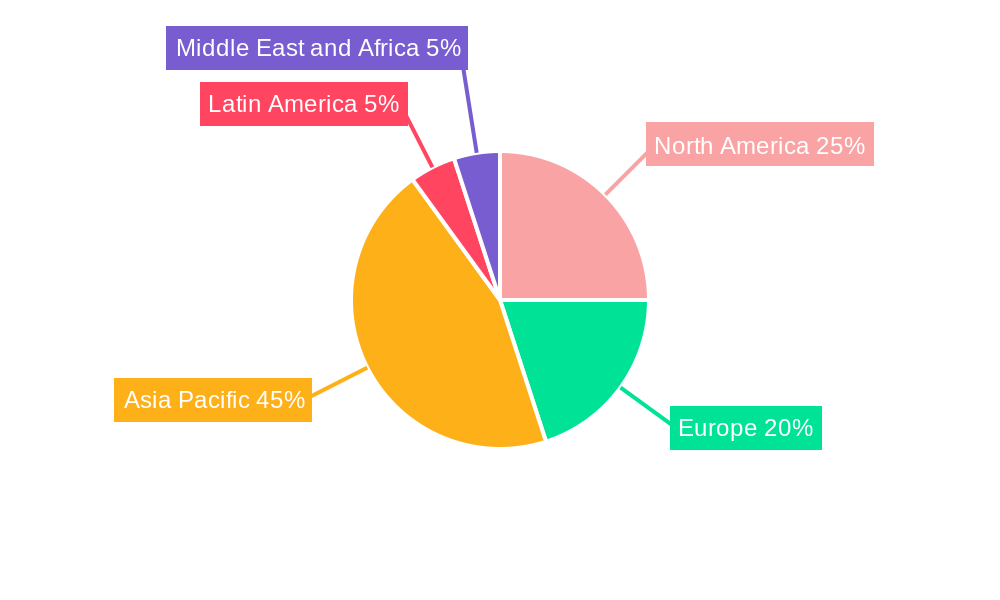

The geographical distribution of the market reveals a strong presence in Asia Pacific, driven by high smartphone manufacturing and consumption in regions like China and India. North America and Europe are also significant markets, with established consumer bases and a preference for premium smartphone models. However, emerging markets in Latin America, the Middle East, and Africa present significant growth opportunities due to increasing smartphone adoption rates and rising disposable incomes. Competitive pressures among manufacturers drive innovation and cost reductions, leading to more affordable and advanced smartphones, which, in turn, expand the overall market. Furthermore, the growing Internet of Things (IoT) ecosystem indirectly benefits the mobile phone semiconductor market, as many IoT devices utilize similar components. While component shortages and increasing material costs could cause temporary fluctuations, the overall market trend suggests a continuously expanding sector with significant potential for both established players and emerging innovators.

Mobile Phone Semiconductor Industry: A Comprehensive Market Analysis (2019-2033)

This comprehensive report provides a detailed analysis of the mobile phone semiconductor industry, encompassing market trends, competitive dynamics, technological advancements, and future growth prospects from 2019 to 2033. The study period covers the historical period (2019-2024), the base year (2025), and the forecast period (2025-2033), with an estimated year of 2025. Key players such as NXP Semiconductors N V, Samsung Electronics, Micron Technology Inc, Skyworks Solutions Inc, Broadcom Inc, Qorvo Inc, Qualcomm Technologies Inc, Huawei Technologies Co Ltd, MediaTek Inc, and Intel Corporation are analyzed, though the list is not exhaustive. The report segments the market by component type: Mobile Processors, Memory, Logic Chips, and Analog.

Mobile Phone Semiconductor Industry Market Concentration & Innovation

The mobile phone semiconductor market exhibits a high degree of concentration, with a few dominant players controlling significant market share. Samsung Electronics and Qualcomm Technologies Inc consistently hold leading positions, driven by their strong technological capabilities and extensive patent portfolios. The market share of these top players has fluctuated slightly over the past five years, ranging from xx% to xx%, indicating a relatively stable competitive landscape, with xx Million in M&A deal values observed in the past few years, primarily driven by consolidation efforts to acquire technological capabilities and expand market presence.

Innovation is a key driver in this industry, with continuous advancements in processing power, memory capacity, and energy efficiency. Stringent regulatory frameworks, particularly regarding data privacy and security, significantly influence product development and market access. The emergence of alternative technologies, such as advanced packaging and heterogeneous integration, is disrupting traditional manufacturing processes. Furthermore, evolving consumer preferences towards higher performance, longer battery life, and advanced features are driving the demand for more sophisticated semiconductor components. The industry sees frequent M&A activities, further shaping the competitive landscape.

- Key Innovation Drivers: Enhanced processing power, improved energy efficiency, miniaturization, 5G connectivity, AI integration.

- Regulatory Landscape: Data privacy regulations (GDPR, CCPA), trade restrictions, intellectual property rights.

- M&A Activity: Consolidation among players to achieve economies of scale and expand market share.

Mobile Phone Semiconductor Industry Industry Trends & Insights

The mobile phone semiconductor industry is experiencing robust growth, driven by several factors. The increasing adoption of smartphones globally, particularly in emerging markets, fuels demand for advanced semiconductor components. Technological disruptions, such as the transition to 5G networks and the rise of artificial intelligence (AI), are driving the need for higher processing power and improved data handling capabilities. Consumer preferences for premium features, such as high-resolution displays, advanced camera systems, and improved battery life, further contribute to the market expansion. The industry's CAGR is projected to be xx% during the forecast period (2025-2033), with market penetration reaching approximately xx% by 2033. Competitive dynamics are shaped by continuous product innovation, aggressive pricing strategies, and strategic partnerships.

Dominant Markets & Segments in Mobile Phone Semiconductor Industry

The Asia-Pacific region, particularly China, holds a dominant position in the mobile phone semiconductor market. This dominance is attributed to several key drivers:

- Large and rapidly growing smartphone market: High demand for smartphones fuels the need for semiconductor components.

- Government support and investment: Significant financial incentives for semiconductor manufacturing.

- Robust supply chain: Well-established ecosystem for component manufacturing and assembly.

The Mobile Processors segment is the largest contributor to the market's revenue, driven by the increasing demand for high-performance mobile computing. The Memory segment is experiencing strong growth due to the need for more storage capacity in smartphones, while the Analog segment demonstrates consistent growth, driven by the increasing complexity of smartphone functionalities. The Logic Chips segment witnesses moderate growth, supporting the increasing computational power required by various smartphone applications.

Mobile Phone Semiconductor Industry Product Developments

Recent innovations in mobile phone semiconductors include advancements in 5G modem technology, improved image signal processors (ISPs), and the integration of AI accelerators. These advancements enhance smartphone capabilities, providing faster data speeds, superior image quality, and improved performance in AI-powered applications. The focus is on miniaturization, power efficiency, and cost reduction, leading to increased competitiveness and diverse product offerings that better meet market demands.

Report Scope & Segmentation Analysis

This report segments the mobile phone semiconductor market by component type:

Mobile Processors: This segment comprises central processing units (CPUs) and graphics processing units (GPUs), with projected growth driven by advancements in processing power and AI capabilities. Market size is estimated at xx Million in 2025.

Memory: This segment includes DRAM and flash memory, with anticipated growth driven by the rising demand for higher storage capacities and faster data access speeds. Market size is estimated at xx Million in 2025.

Logic Chips: This segment encompasses various integrated circuits responsible for specific smartphone functionalities. Market growth is moderate, driven by increased feature complexity and integration. Market size is estimated at xx Million in 2025.

Analog: This segment encompasses various analog components that support the smartphone's various functionalities. The market size is estimated at xx Million in 2025, and growth is consistent with the increase in smartphone features.

Key Drivers of Mobile Phone Semiconductor Industry Growth

The mobile phone semiconductor industry's growth is fueled by several factors:

- Technological advancements: Continuous innovations in processing power, memory capacity, and energy efficiency.

- Increased smartphone adoption: Growing global smartphone penetration, particularly in emerging markets.

- 5G rollout: The widespread adoption of 5G networks drives demand for advanced semiconductor components.

- AI integration: Increasing integration of AI capabilities into smartphones fuels demand for high-performance processors.

Challenges in the Mobile Phone Semiconductor Industry Sector

The industry faces significant challenges:

- Supply chain disruptions: Geopolitical uncertainties and natural disasters can disrupt the supply chain, leading to component shortages and price volatility.

- Intense competition: High competitive pressure among major players necessitates continuous innovation and cost optimization.

- Regulatory hurdles: Stringent regulatory frameworks regarding data privacy and security impose compliance costs.

Emerging Opportunities in Mobile Phone Semiconductor Industry

Emerging trends and opportunities include:

- Expansion in emerging markets: Untapped potential in developing countries with growing smartphone adoption.

- New applications: Expansion into new areas such as augmented reality (AR), virtual reality (VR), and the Internet of Things (IoT).

- Advanced packaging technologies: Potential for cost reduction and improved performance through advanced packaging techniques.

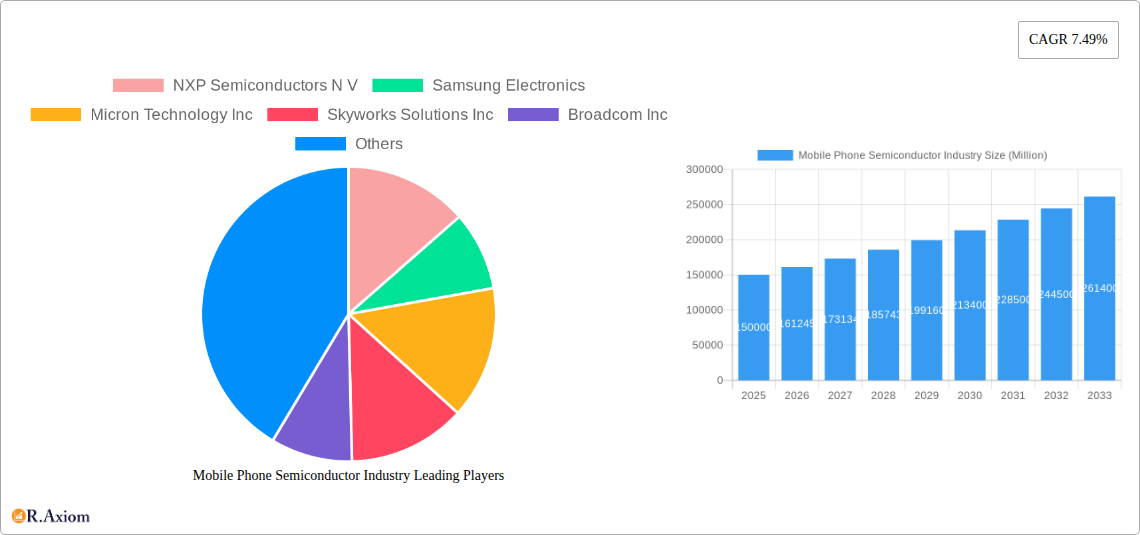

Leading Players in the Mobile Phone Semiconductor Industry Market

- NXP Semiconductors N V

- Samsung Electronics

- Micron Technology Inc

- Skyworks Solutions Inc

- Broadcom Inc

- Qorvo Inc

- Qualcomm Technologies Inc

- Huawei Technologies Co Ltd

- MediaTek Inc

- Intel Corporation

Key Developments in Mobile Phone Semiconductor Industry Industry

November 2022: Micron Technology launched its 1-beta DRAM, aiming for a 15% improvement in power efficiency and a 35% increase in bit density. This launch signals a significant advancement in memory technology, enhancing smartphone performance and battery life.

October 2022: Polymatech, a semiconductor chip manufacturer, initiated production of Opto-semiconductors and memory modules, representing a USD 1 billion investment in semiconductor chip manufacturing and marking significant expansion in the market.

Strategic Outlook for Mobile Phone Semiconductor Industry Market

The mobile phone semiconductor market presents substantial growth opportunities. Continued technological advancements, the expansion of 5G networks, and the increasing integration of AI capabilities will drive demand for high-performance, energy-efficient components. Strategic partnerships, mergers and acquisitions, and aggressive R&D investments will be crucial for companies seeking to capitalize on the market's potential. The focus on innovative materials and processes will further lead to substantial growth.

Mobile Phone Semiconductor Industry Segmentation

-

1. Component Type

- 1.1. Mobile Processors

- 1.2. Memory

- 1.3. Logic Chips

- 1.4. Analog

Mobile Phone Semiconductor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Mobile Phone Semiconductor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

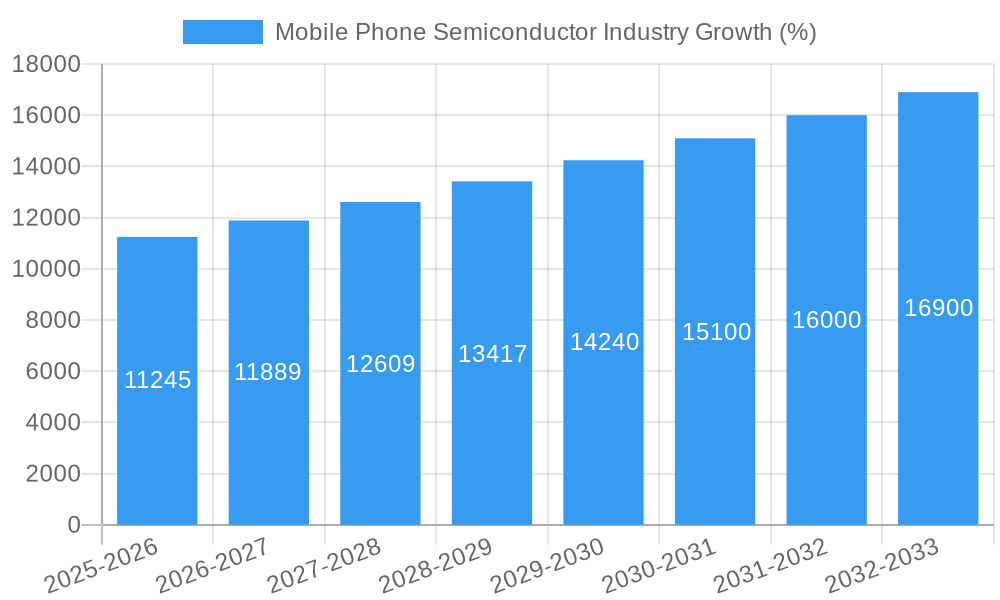

| Growth Rate | CAGR of 7.49% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Rapid Introduction of Next-generation Mobile-communications Standard

- 3.2.2 LTE or 4G; Emergence of 'Multicom' Solutions

- 3.3. Market Restrains

- 3.3.1. Complexity Regarding Manufacturing; Consumer Demand Exceeding Factory Capacity

- 3.4. Market Trends

- 3.4.1. Memory to Significantly Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 5.1.1. Mobile Processors

- 5.1.2. Memory

- 5.1.3. Logic Chips

- 5.1.4. Analog

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component Type

- 6. North America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 6.1.1. Mobile Processors

- 6.1.2. Memory

- 6.1.3. Logic Chips

- 6.1.4. Analog

- 6.1. Market Analysis, Insights and Forecast - by Component Type

- 7. Europe Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 7.1.1. Mobile Processors

- 7.1.2. Memory

- 7.1.3. Logic Chips

- 7.1.4. Analog

- 7.1. Market Analysis, Insights and Forecast - by Component Type

- 8. Asia Pacific Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 8.1.1. Mobile Processors

- 8.1.2. Memory

- 8.1.3. Logic Chips

- 8.1.4. Analog

- 8.1. Market Analysis, Insights and Forecast - by Component Type

- 9. Latin America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 9.1.1. Mobile Processors

- 9.1.2. Memory

- 9.1.3. Logic Chips

- 9.1.4. Analog

- 9.1. Market Analysis, Insights and Forecast - by Component Type

- 10. Middle East and Africa Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 10.1.1. Mobile Processors

- 10.1.2. Memory

- 10.1.3. Logic Chips

- 10.1.4. Analog

- 10.1. Market Analysis, Insights and Forecast - by Component Type

- 11. North America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East and Africa Mobile Phone Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 NXP Semiconductors N V

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Samsung Electronics

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Micron Technology Inc

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Skyworks Solutions Inc

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Broadcom Inc

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Qorvo Inc *List Not Exhaustive

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Qualcomm Technologies Inc

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Huawei Technologies Co Ltd

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 MediaTek Inc

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Intel Corporation

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 NXP Semiconductors N V

List of Figures

- Figure 1: Global Mobile Phone Semiconductor Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2024 & 2032

- Figure 13: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2024 & 2032

- Figure 14: North America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: North America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2024 & 2032

- Figure 17: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2024 & 2032

- Figure 18: Europe Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: Europe Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2024 & 2032

- Figure 21: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2024 & 2032

- Figure 22: Asia Pacific Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Asia Pacific Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2024 & 2032

- Figure 25: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2024 & 2032

- Figure 26: Latin America Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Latin America Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Component Type 2024 & 2032

- Figure 29: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Component Type 2024 & 2032

- Figure 30: Middle East and Africa Mobile Phone Semiconductor Industry Revenue (Million), by Country 2024 & 2032

- Figure 31: Middle East and Africa Mobile Phone Semiconductor Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 3: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Mobile Phone Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Mobile Phone Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Mobile Phone Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Mobile Phone Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: Mobile Phone Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 15: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 17: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 19: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 21: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Component Type 2019 & 2032

- Table 23: Global Mobile Phone Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Phone Semiconductor Industry?

The projected CAGR is approximately 7.49%.

2. Which companies are prominent players in the Mobile Phone Semiconductor Industry?

Key companies in the market include NXP Semiconductors N V, Samsung Electronics, Micron Technology Inc, Skyworks Solutions Inc, Broadcom Inc, Qorvo Inc *List Not Exhaustive, Qualcomm Technologies Inc, Huawei Technologies Co Ltd, MediaTek Inc, Intel Corporation.

3. What are the main segments of the Mobile Phone Semiconductor Industry?

The market segments include Component Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Introduction of Next-generation Mobile-communications Standard. LTE or 4G; Emergence of 'Multicom' Solutions.

6. What are the notable trends driving market growth?

Memory to Significantly Drive the Market.

7. Are there any restraints impacting market growth?

Complexity Regarding Manufacturing; Consumer Demand Exceeding Factory Capacity.

8. Can you provide examples of recent developments in the market?

November 2022 - Micron Technology launched its 1-beta DRAM with an aim to improve power efficiency by 15% and bit density by 35% for memory chips. The new DRAM chips would underpin a new generation of memory chips for Micron.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Phone Semiconductor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Phone Semiconductor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Phone Semiconductor Industry?

To stay informed about further developments, trends, and reports in the Mobile Phone Semiconductor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence