Key Insights

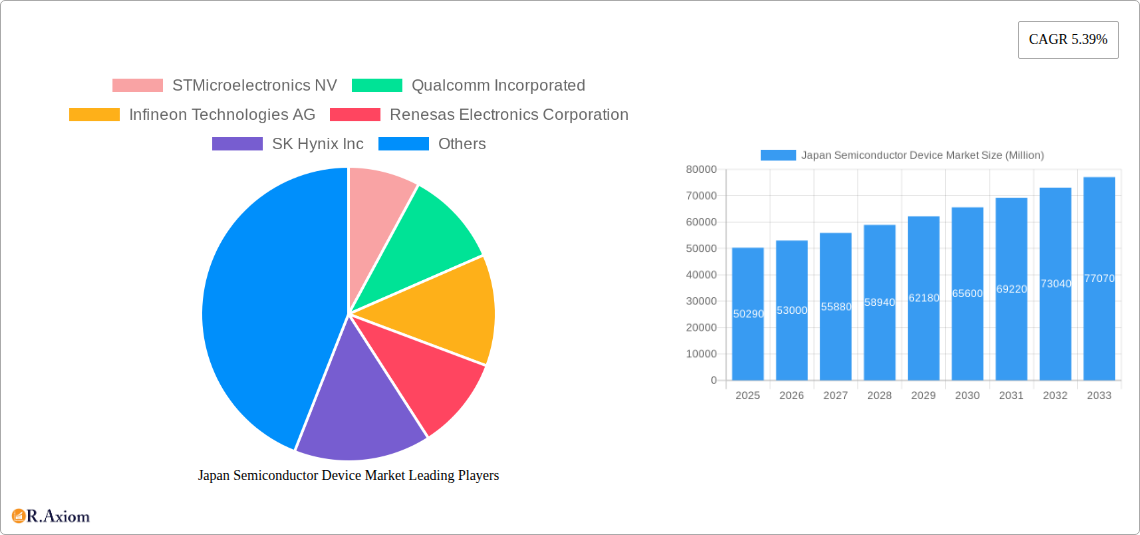

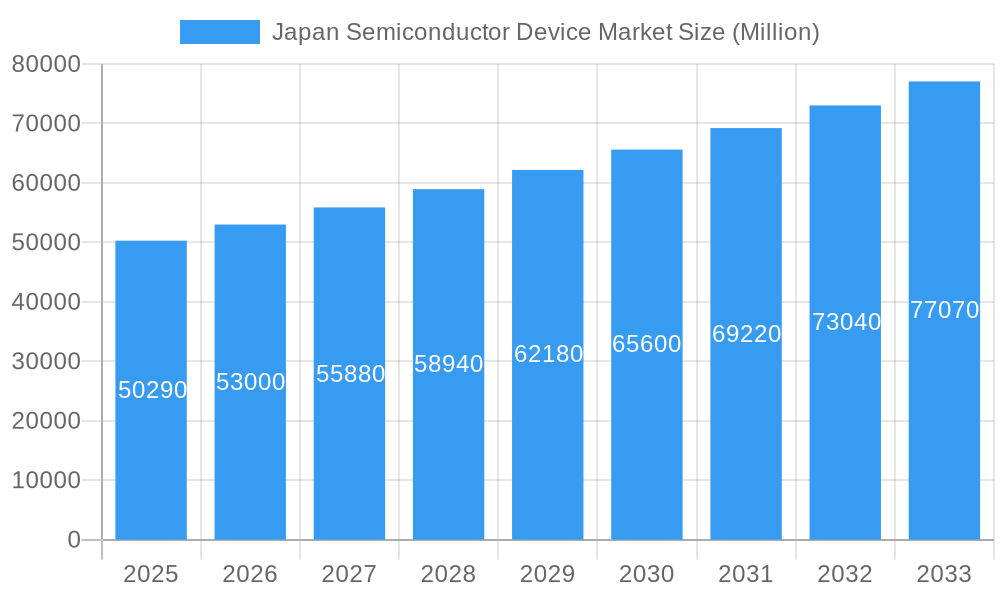

The Japan semiconductor device market, valued at $50.29 billion in 2025, is projected to experience robust growth, driven by the nation's advanced technological prowess and significant investments in research and development. A Compound Annual Growth Rate (CAGR) of 5.39% is anticipated from 2025 to 2033, indicating a substantial expansion. Key drivers include the burgeoning automotive sector's demand for sophisticated electronic components, the rapid proliferation of 5G and other advanced wireless communication technologies, and the increasing adoption of semiconductor devices in consumer electronics, from smartphones to smart home appliances. Furthermore, the growth of the industrial automation sector and the expanding data center infrastructure in Japan contribute significantly to market expansion. While supply chain vulnerabilities and potential global economic fluctuations pose some restraints, the continuous innovation in semiconductor technology, particularly in areas like AI and IoT, is expected to offset these challenges and fuel sustained market growth. The market segmentation reveals a diverse landscape, with integrated circuits and microprocessors holding prominent positions within the device type segment, while the automotive and communication sectors dominate the end-user vertical. Major players like STMicroelectronics, Qualcomm, and Renesas Electronics are key contributors to this dynamic market, shaping its trajectory through continuous innovation and strategic partnerships.

Japan Semiconductor Device Market Market Size (In Billion)

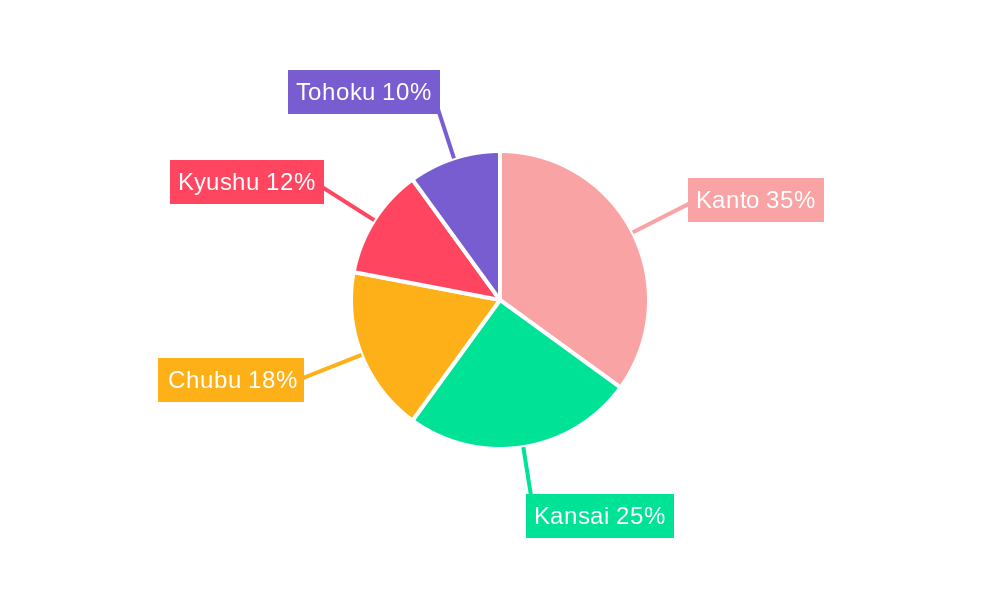

The regional distribution within Japan showcases a concentration of activity in regions like Kanto, Kansai, and Chubu, reflective of established industrial hubs and technological centers. The forecast period (2025-2033) promises to witness the emergence of new technologies and applications for semiconductor devices, driving further segmentation and specialization. While specific regional breakdowns beyond the mentioned Japanese prefectures are unavailable, a strong correlation can be expected between regional economic activity and semiconductor device adoption. The historical period (2019-2024) served as a foundation for current growth, with trends from this period informing the positive outlook for the coming decade.

Japan Semiconductor Device Market Company Market Share

Japan Semiconductor Device Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Japan semiconductor device market, offering valuable insights for industry stakeholders, investors, and strategic decision-makers. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages historical data (2019-2024) and expert projections to deliver a clear picture of market dynamics and future trends. The market is segmented by device type (Discrete Semiconductors, Optoelectronics, Sensors, Integrated Circuits, Microprocessors (MPU), Microcontrollers (MCU), Digital Signal Processors) and end-user vertical (Automotive, Communication, Consumer Electronics, Industrial, Computing/Data Storage, Other). Key players analyzed include STMicroelectronics NV, Qualcomm Incorporated, Infineon Technologies AG, Renesas Electronics Corporation, SK Hynix Inc, Rohm Co Ltd, Advanced Semiconductor Engineering Inc, ON Semiconductor Corporation, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Kyocera Corporation, Xilinx Inc, Texas Instruments Inc, Nvidia Corporation, Samsung Electronics Co Ltd, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Intel Corporation, Fujitsu Semiconductor Ltd, and Broadcom Inc.

Japan Semiconductor Device Market Market Concentration & Innovation

The Japanese semiconductor device market exhibits a moderately concentrated landscape, with a few dominant players commanding significant market share. Renesas Electronics Corporation and Toshiba Corporation, for instance, hold substantial positions, driven by their strong domestic presence and established technological capabilities. However, the market also features numerous smaller players specializing in niche segments. The market concentration ratio (CR4 or CR8) for 2024 is estimated at xx%, indicating a moderate level of concentration.

Innovation within the market is fueled by ongoing advancements in materials science, process technology, and miniaturization. The government's investment in R&D and supportive regulatory framework further encourage innovation. Product substitutions, particularly the adoption of new materials and device architectures, also impact market dynamics. Mergers and acquisitions (M&A) play a critical role in shaping the competitive landscape. Over the past five years, the total value of M&A deals in the Japanese semiconductor sector has reached approximately xx Million. Key M&A drivers include expansion into new market segments and technological capabilities, as well as achieving economies of scale.

- Key Innovation Drivers: Advancements in AI, IoT, 5G, and automotive electronics.

- Regulatory Landscape: Government initiatives aimed at strengthening domestic semiconductor manufacturing.

- Product Substitutions: Shift from older technologies to newer, more energy-efficient alternatives.

- M&A Activity: Consolidation among players, leading to increased market concentration.

Japan Semiconductor Device Market Industry Trends & Insights

The Japan semiconductor device market is experiencing robust growth, driven by increased demand from various end-user verticals. The market size is projected to reach xx Million by 2025 and is expected to grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Several factors contribute to this growth, including technological advancements, growing adoption of sophisticated electronic devices, and the rise of industries like automotive and communication. Market penetration of advanced semiconductor technologies, especially in the automotive and IoT segments, is rapidly increasing, creating opportunities for growth. However, the market faces certain challenges including the global semiconductor shortage and rising geopolitical tensions impacting supply chain stability. The market is becoming increasingly competitive, with both domestic and international players vying for market share. Consumer preferences are shifting towards higher-performance, energy-efficient, and more compact devices.

Dominant Markets & Segments in Japan Semiconductor Device Market

The Japanese automotive sector remains a dominant end-user vertical for semiconductor devices, driven by the increasing electronic content in vehicles and the adoption of advanced driver-assistance systems (ADAS). The Integrated Circuits segment holds a significant market share within the device type category due to its widespread applications across various electronics.

- Key Drivers for Automotive Dominance: Growth in electric vehicles (EVs), increasing ADAS adoption, and stringent emission regulations.

- Key Drivers for Integrated Circuits Dominance: Wide applicability across various electronic devices and systems.

Within regional markets, the Kanto region (including Tokyo) dominates due to its concentration of manufacturing facilities and a large pool of skilled labor. Government support and robust infrastructure further solidify this region’s dominance. However, other regions are witnessing growth driven by investments in infrastructure and supportive government policies.

Japan Semiconductor Device Market Product Developments

Recent product innovations have focused on enhancing performance, energy efficiency, and miniaturization of semiconductor devices. Companies are investing heavily in developing advanced technologies like AI-powered chips, high-speed data processing units, and energy-efficient power semiconductors. These developments cater to the growing demand for sophisticated electronic devices across various sectors, offering competitive advantages through improved performance, lower energy consumption, and higher reliability. The successful integration of these technologies in applications like autonomous vehicles, 5G networks, and data centers fuels further growth in the market.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Japanese semiconductor device market based on device type and end-user vertical. The Device Type segment includes Discrete Semiconductors, Optoelectronics, Sensors, and Integrated Circuits, further categorized into microprocessors (MPU), microcontrollers (MCU), and digital signal processors (DSP). Each segment exhibits unique growth trajectories, shaped by technological advancements and specific application demands. For example, the Integrated Circuits segment is projected to grow at a CAGR of xx% due to its versatility, while the sensor segment displays a CAGR of xx% driven by the growing adoption of IoT and smart devices. The End-user Vertical segment includes Automotive, Communication, Consumer Electronics, Industrial, Computing/Data Storage, and Other. The Automotive segment is anticipated to showcase strong growth (CAGR of xx%) due to rising vehicle automation. Competitive dynamics vary across segments; some exhibit intense competition, while others show a more concentrated market structure.

Key Drivers of Japan Semiconductor Device Market Growth

Several factors are driving the growth of the Japanese semiconductor device market. These include increasing demand for advanced electronics across various sectors, government initiatives aimed at boosting domestic semiconductor manufacturing, and rapid advancements in semiconductor technology that enable miniaturization, higher performance, and reduced energy consumption. The development of advanced technologies like AI, IoT, and 5G is also a significant growth driver. Further bolstering this growth is a strong emphasis on technological innovation backed by substantial investments in R&D.

Challenges in the Japan Semiconductor Device Market Sector

The Japanese semiconductor device market faces several challenges. These include supply chain disruptions, intense global competition, high manufacturing costs, and the dependence on imported raw materials. The rising cost of advanced chip manufacturing equipment and skilled labor adds further complexity. The global semiconductor shortage in recent years highlighted the vulnerability of the supply chain, leading to capacity constraints and price increases. These challenges pose significant threats to the market's sustainable growth. Addressing these issues through strategic investments in domestic manufacturing, diversification of supply chains, and fostering collaborations is crucial.

Emerging Opportunities in Japan Semiconductor Device Market

The Japanese semiconductor device market presents several emerging opportunities. The growing adoption of AI and IoT technologies across various sectors creates a significant demand for high-performance and specialized semiconductor devices. The expansion of 5G networks also presents a substantial opportunity for growth. Furthermore, advancements in automotive electronics, including the rise of electric vehicles and autonomous driving technologies, are driving demand for innovative semiconductor solutions. This presents opportunities to expand into new markets and create novel device applications.

Leading Players in the Japan Semiconductor Device Market Market

- STMicroelectronics NV

- Qualcomm Incorporated

- Infineon Technologies AG

- Renesas Electronics Corporation

- SK Hynix Inc

- Rohm Co Ltd

- Advanced Semiconductor Engineering Inc

- ON Semiconductor Corporation

- NXP Semiconductors NV

- Toshiba Corporation

- Micron Technology Inc

- Kyocera Corporation

- Xilinx Inc

- Texas Instruments Inc

- Nvidia Corporation

- Samsung Electronics Co Ltd

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- Intel Corporation

- Fujitsu Semiconductor Ltd

- Broadcom Inc

Key Developments in Japan Semiconductor Device Market Industry

May 2024: Toshiba completed a new 300-millimeter wafer fabrication facility for power semiconductors and an office building in Ishikawa Prefecture, Japan. Mass production is slated to begin in the second half of fiscal year 2024. This expansion significantly boosts Toshiba's power semiconductor production capacity, impacting market supply and competition.

May 2024: SK Hynix unveiled ZUFS 4.0, an on-device AI solution for mobile devices, primarily smartphones. This launch strengthens SK Hynix's position in AI memory, leveraging its success in high-speed DRAM. The new technology could significantly enhance the performance of mobile AI applications.

Strategic Outlook for Japan Semiconductor Device Market Market

The Japanese semiconductor device market is poised for continued growth, driven by technological advancements, increasing demand from various sectors, and government support for domestic manufacturing. Future market potential lies in the expansion of high-growth segments like automotive electronics, AI, and IoT. Companies that invest in R&D, leverage advanced technologies, and adopt strategic partnerships will be well-positioned to capitalize on these opportunities and achieve sustainable growth in the dynamic Japanese semiconductor landscape.

Japan Semiconductor Device Market Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

-

1.4.4. Micro

- 1.4.4.1. Microprocessors (MPU)

- 1.4.4.2. Microcontrollers (MCU)

- 1.4.4.3. Digital Signal Processors

-

2. End-user Vertical

- 2.1. Automotive

- 2.2. Communication (Wired and Wireless)

- 2.3. Consumer Electronics

- 2.4. Industrial

- 2.5. Computing/Data Storage

- 2.6. Other End-user Verticals

Japan Semiconductor Device Market Segmentation By Geography

- 1. Japan

Japan Semiconductor Device Market Regional Market Share

Geographic Coverage of Japan Semiconductor Device Market

Japan Semiconductor Device Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro

- 5.1.4.4.1. Microprocessors (MPU)

- 5.1.4.4.2. Microcontrollers (MCU)

- 5.1.4.4.3. Digital Signal Processors

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Automotive

- 5.2.2. Communication (Wired and Wireless)

- 5.2.3. Consumer Electronics

- 5.2.4. Industrial

- 5.2.5. Computing/Data Storage

- 5.2.6. Other End-user Verticals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Japan Semiconductor Device Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. Discrete Semiconductors

- 6.1.2. Optoelectronics

- 6.1.3. Sensors

- 6.1.4. Integrated Circuits

- 6.1.4.1. Analog

- 6.1.4.2. Logic

- 6.1.4.3. Memory

- 6.1.4.4. Micro

- 6.1.4.4.1. Microprocessors (MPU)

- 6.1.4.4.2. Microcontrollers (MCU)

- 6.1.4.4.3. Digital Signal Processors

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. Automotive

- 6.2.2. Communication (Wired and Wireless)

- 6.2.3. Consumer Electronics

- 6.2.4. Industrial

- 6.2.5. Computing/Data Storage

- 6.2.6. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Qualcomm Incorporated

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Infineon Technologies AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Renesas Electronics Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 SK Hynix Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Rohm Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Advanced Semiconductor Engineering Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ON Semiconductor Corporation*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 NXP Semiconductors NV

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Toshiba Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Micron Technology Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Kyocera Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Xilinx Inc

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Texas Instruments Inc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Nvidia Corporation

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Samsung Electronics Co Ltd

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Intel Corporation

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Fujitsu Semiconductor Ltd

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 Broadcom Inc

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.1 STMicroelectronics NV

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Semiconductor Device Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Semiconductor Device Market Share (%) by Company 2025

List of Tables

- Table 1: Japan Semiconductor Device Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 2: Japan Semiconductor Device Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 3: Japan Semiconductor Device Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Japan Semiconductor Device Market Revenue Million Forecast, by Device Type 2020 & 2033

- Table 5: Japan Semiconductor Device Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: Japan Semiconductor Device Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Semiconductor Device Market?

The projected CAGR is approximately 5.39%.

2. Which companies are prominent players in the Japan Semiconductor Device Market?

Key companies in the market include STMicroelectronics NV, Qualcomm Incorporated, Infineon Technologies AG, Renesas Electronics Corporation, SK Hynix Inc, Rohm Co Ltd, Advanced Semiconductor Engineering Inc, ON Semiconductor Corporation*List Not Exhaustive, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Kyocera Corporation, Xilinx Inc, Texas Instruments Inc, Nvidia Corporation, Samsung Electronics Co Ltd, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Intel Corporation, Fujitsu Semiconductor Ltd, Broadcom Inc.

3. What are the main segments of the Japan Semiconductor Device Market?

The market segments include Device Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.29 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Technologies like IoT and AI; Increased Deployment of 5G and Rising Demand for 5G Smartphones.

6. What are the notable trends driving market growth?

Automotive is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Supply Chain Disruptions Resulting in Semiconductor Chip Shortage.

8. Can you provide examples of recent developments in the market?

May 2024: Toshiba marked the completion of a new 300-millimeter wafer fabrication facility for power semiconductors and an office building at KagaToshiba Electronics Corporation in Ishikawa Prefecture, Japan, one of Toshiba’s key group companies. Toshiba will now proceed with equipment installation, toward starting mass production in the second half of fiscal year 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Semiconductor Device Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Semiconductor Device Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Semiconductor Device Market?

To stay informed about further developments, trends, and reports in the Japan Semiconductor Device Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence