Key Insights

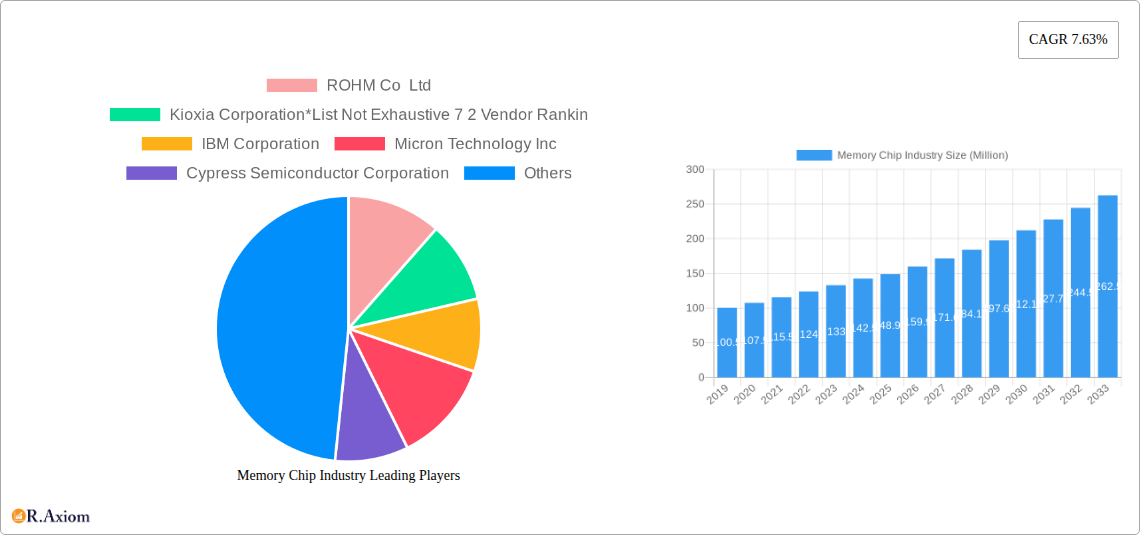

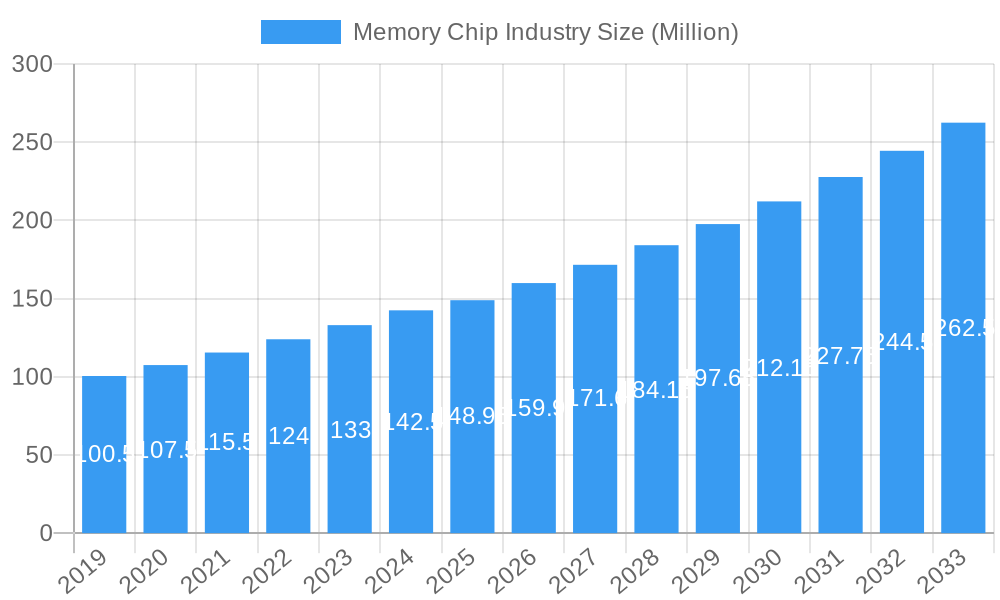

The global Memory Chip Industry is poised for robust expansion, projected to reach an impressive market size of USD 148.95 million by 2025. This growth is fueled by an estimated Compound Annual Growth Rate (CAGR) of 7.63% during the study period of 2019-2033. This sustained upward trajectory is largely driven by the insatiable demand for advanced computing power and data storage across a multitude of applications. Consumer electronics, the primary application segment, continues to be a significant contributor, with the proliferation of smartphones, tablets, and smart home devices requiring increasingly sophisticated memory solutions. Furthermore, the burgeoning data center industry, essential for cloud computing and big data analytics, represents a substantial growth engine, demanding high-capacity and high-performance memory chips. The PC and laptop market, while mature, also contributes to this demand, as devices become more powerful and capable of handling complex tasks.

Memory Chip Industry Market Size (In Million)

The industry's growth is further propelled by key trends such as the advancement of Artificial Intelligence (AI) and Machine Learning (ML), which necessitate larger and faster memory capacities to process vast datasets. The automotive sector's increasing integration of in-car infotainment systems, advanced driver-assistance systems (ADAS), and autonomous driving technologies is also a significant catalyst, requiring specialized memory solutions for real-time data processing and storage. Emerging applications in the Internet of Things (IoT) and wearable technology are also contributing to market expansion, albeit with potentially smaller individual memory requirements per device, their sheer volume creates substantial demand. While the market is robust, potential restraints such as intense competition among leading players like Samsung Electronics, SK Hynix, and Micron Technology, and the cyclical nature of semiconductor pricing could pose challenges. However, the continuous innovation in memory technologies, including the development of DRAM, NAND Flash, and NOR Flash solutions, coupled with increasing global digital transformation initiatives, will continue to drive market penetration and value.

Memory Chip Industry Company Market Share

Here is a detailed, SEO-optimized report description for the Memory Chip Industry, incorporating high-traffic keywords and designed for immediate use:

Memory Chip Industry Market Concentration & Innovation

The global memory chip industry, a critical component of the digital economy, is characterized by a high degree of market concentration driven by substantial R&D investments and the intricate nature of semiconductor manufacturing. Key players like Samsung Electronics Co Ltd and SK Hynix Inc dominate market share, collectively holding over 70% of the DRAM market. Innovation is the primary catalyst for growth, with ongoing advancements in fabrication technologies such as Extreme Ultraviolet (EUV) lithography and novel memory architectures like High Bandwidth Memory (HBM) pushing performance boundaries. Regulatory frameworks, particularly concerning intellectual property and trade policies, significantly influence market dynamics. Product substitutes, while evolving, struggle to match the performance and density of established memory types. End-user trends increasingly demand higher storage capacities and faster access speeds, fueling demand for cutting-edge memory solutions. Mergers and acquisitions (M&A) remain a strategic tool for consolidation and expansion, with significant deal values often exceeding several million dollars as companies seek to acquire advanced technologies or expand their market reach. For instance, the acquisition of Cypress Semiconductor Corporation by Infineon Technologies aimed to bolster its presence in the automotive and industrial sectors.

Memory Chip Industry Industry Trends & Insights

The memory chip industry is poised for robust growth, driven by an insatiable demand for data storage and processing power across virtually every sector of the global economy. The compound annual growth rate (CAGR) is projected to be around 7.5% over the forecast period, translating into a market valuation expected to surpass 250 million dollars by 2033. This expansion is fueled by several key trends. Firstly, the proliferation of Artificial Intelligence (AI) and Machine Learning (ML) applications necessitates high-performance memory, particularly advanced NAND Flash and DRAM, to handle vast datasets and complex computations. This is evident in the exponential growth of data centers, which are increasingly deploying cutting-edge memory modules to enhance processing efficiency. Secondly, the burgeoning Internet of Things (IoT) ecosystem, encompassing smart home devices, wearable technology, and industrial sensors, creates a consistent demand for embedded memory solutions, including NOR Flash and smaller capacity NAND Flash chips. The continuous evolution of consumer electronics, such as smartphones, tablets, and high-definition gaming consoles, also plays a pivotal role, with consumers demanding greater storage and faster load times. The automotive industry's transition towards advanced driver-assistance systems (ADAS) and autonomous driving technology is another significant growth driver, requiring substantial onboard memory for sensor data processing and AI algorithms. Furthermore, the ongoing digital transformation across enterprises, including cloud computing adoption and big data analytics, underpins the sustained demand for enterprise-grade memory solutions. The competitive landscape remains dynamic, with intense R&D efforts and strategic partnerships shaping market share. Companies are investing heavily in next-generation memory technologies like Resistive RAM (ReRAM) and Phase-Change Memory (PCM) to address future performance and power efficiency requirements. Market penetration of these advanced technologies is expected to increase as manufacturing costs decrease and performance benefits become more pronounced.

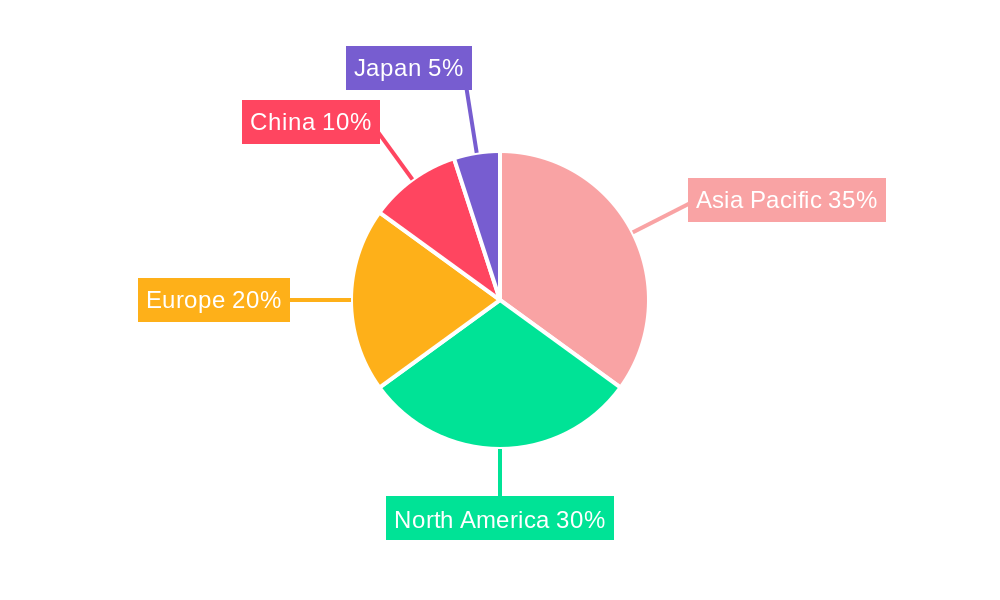

Dominant Markets & Segments in Memory Chip Industry

The global memory chip industry is dominated by Asia-Pacific, particularly South Korea and Taiwan, owing to the presence of leading manufacturers like Samsung Electronics Co Ltd and SK Hynix Inc. These regions benefit from robust government support, advanced technological infrastructure, and a highly skilled workforce dedicated to semiconductor fabrication. The United States also holds significant sway through companies like Micron Technology Inc, contributing to innovation and market competitiveness.

Segments by Type:

- NAND Flash: This segment exhibits strong dominance, driven by its widespread application in solid-state drives (SSDs) for PCs, smartphones, data centers, and consumer electronics. The increasing demand for higher storage capacities and faster data transfer speeds in these devices directly translates to robust growth for NAND Flash. The ongoing development of 3D NAND technology, such as Kioxia Corporation's BiCS FLASH™, further solidifies its market leadership by enabling increased density and improved performance.

- DRAM: As the backbone of computing, DRAM remains a critical segment, primarily driven by the PC/Laptop and Data Center applications. The burgeoning cloud computing sector and the ever-increasing data generated by AI and big data analytics are major catalysts for DRAM demand. Economic policies supporting digital infrastructure development and the continuous need for faster processing in high-performance computing environments contribute to its sustained dominance.

- NOR Flash: This segment finds significant application in embedded systems, automotive electronics, and consumer devices requiring boot code storage and fast read access. The growing complexity of automotive infotainment systems and the proliferation of IoT devices with firmware requirements fuel its market penetration.

- SRAM: Primarily used in cache memory for processors and high-speed applications, SRAM's market is closely tied to the performance demands of CPUs and GPUs in PCs, servers, and high-end consumer electronics.

Segments by Application:

- Data Center: This application segment is a major growth engine, accounting for a substantial portion of the market. The exponential rise of cloud computing, big data analytics, and AI/ML workloads necessitates vast quantities of high-speed and high-density memory, making it a key driver for both DRAM and NAND Flash. Government initiatives promoting digital transformation and the expansion of hyperscale data centers worldwide contribute to this dominance.

- Smartphone/Tablet: This segment continues to be a significant consumer of memory chips, especially NAND Flash for storage and DRAM for performance. The constant innovation in mobile device capabilities, including advanced camera features, AI integration, and immersive gaming experiences, drives the demand for higher memory specifications.

- PC/Laptop: While mature, the PC/Laptop segment remains a substantial market for DRAM and NAND Flash, especially with the increasing trend of remote work and the demand for higher-performance computing for gaming and content creation.

- Consumer Products: This broad category, encompassing smart TVs, gaming consoles, wearables, and other electronic gadgets, collectively represents a significant demand for various memory types, particularly NAND Flash and NOR Flash.

- Automotive: The automotive sector is a rapidly growing application for memory chips, driven by the increasing integration of ADAS, infotainment systems, and connectivity features. NOR Flash and NAND Flash are crucial for these applications, with demand projected to surge as autonomous driving technology matures.

Memory Chip Industry Product Developments

Product innovation in the memory chip industry is relentlessly focused on enhancing performance, increasing density, and reducing power consumption. Samsung Electronics Co Ltd continues to push the boundaries of NAND Flash technology with advancements in vertical stacking, aiming for terabyte-level capacities in smaller form factors. Micron Technology Inc is at the forefront of developing next-generation DRAM with higher bandwidth and lower latency, crucial for AI and high-performance computing. The development of new memory types like ReRAM and MRAM promises to revolutionize embedded systems and IoT devices by offering non-volatility with DRAM-like speeds. These advancements are critical for maintaining competitive advantages in rapidly evolving markets such as automotive electronics and advanced data centers.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the global memory chip industry, segmenting the market by product type and application. The Type segmentation includes DRAM, SRAM, NOR Flash, NAND Flash, ROM & EPROM, and Others. The Application segmentation covers Consumer Products, PC/Laptop, Smartphone/Tablet, Data Center, Automotive, and Other Applications. Each segment's market size, growth projections, and competitive dynamics are thoroughly examined. For instance, the NAND Flash segment is projected to experience a CAGR of over 8% due to its critical role in data storage solutions. The Automotive segment, driven by ADAS and infotainment, is expected to witness the highest growth rate, albeit from a smaller base.

Key Drivers of Memory Chip Industry Growth

Several interconnected factors are driving the sustained growth of the memory chip industry. Technologically, the insatiable demand for data generated by AI, big data, and cloud computing necessitates constant innovation in memory capacity and speed. Economic factors, such as global digitalization initiatives and the expansion of the IoT ecosystem, create pervasive demand across diverse sectors. Regulatory frameworks that support semiconductor manufacturing and R&D, alongside increasing government investments in digital infrastructure, further bolster growth. For example, the CHIPS Act in the United States aims to bolster domestic semiconductor production and innovation. The increasing complexity of end-user applications, from advanced gaming to autonomous vehicles, also acts as a significant growth catalyst.

Challenges in the Memory Chip Industry Sector

Despite robust growth, the memory chip industry faces significant challenges. High capital expenditure required for advanced fabrication facilities and R&D presents a substantial barrier to entry. Intense global competition and cyclical market dynamics, characterized by periods of oversupply and price volatility, can impact profitability. Supply chain disruptions, exacerbated by geopolitical tensions and natural disasters, pose a continuous risk to production and timely delivery. Furthermore, the constant need to innovate and keep pace with technological advancements requires continuous, substantial investment, which can be a strain for smaller players. Intellectual property disputes and stringent environmental regulations also add layers of complexity to operations.

Emerging Opportunities in Memory Chip Industry

Emerging opportunities within the memory chip industry are abundant, driven by technological advancements and evolving consumer needs. The rapid growth of AI and machine learning presents a significant opportunity for high-bandwidth memory solutions. The expanding IoT market demands specialized, low-power embedded memory chips. The increasing adoption of electric vehicles (EVs) and autonomous driving technologies is creating a substantial demand for automotive-grade memory. Furthermore, the development of novel memory technologies such as ReRAM and MRAM offers the potential for disruptive innovation, enabling entirely new applications in areas like edge computing and advanced wearables.

Leading Players in the Memory Chip Industry Market

- ROHM Co Ltd

- Kioxia Corporation

- IBM Corporation

- Micron Technology Inc

- Cypress Semiconductor Corporation

- Samsung Electronics Co Ltd

- STMicroelectronics NV

- SK Hynix Inc

- Nvidia Corporation

- Maxim Integrated Products Inc

- Intel Corporation

Key Developments in Memory Chip Industry Industry

- March 2022 - Kioxia Corporation, a provider of memory solutions, announced it would start construction of an advanced new fabrication facility at its Kitakami Plant in Japan for the possible expansion of manufacturing of its proprietary 3D Flash memory BiCS FLASH™. Construction of this facility is planned to commence in April 2022 and is expected to be completed in 2023.

- December 2021 - Micron Technology announced plans for its new memory design center in Midtown Atlanta, the United States, expanding the company's reach into the Southeast United States. Micron aims to establish strong partnerships with many institutions in the region including Georgia Tech, Emory University, Spelman College, Morehouse College, and the University of Georgia.

Strategic Outlook for Memory Chip Industry Market

The strategic outlook for the memory chip industry is overwhelmingly positive, driven by the fundamental role semiconductors play in the global digital economy. Growth catalysts include the accelerating adoption of 5G technology, the continued expansion of data centers and cloud services, and the burgeoning demand from the automotive sector for advanced driver-assistance systems and infotainment. Emerging trends such as edge computing and the metaverse will further necessitate sophisticated memory solutions. Companies investing in advanced manufacturing processes, next-generation memory architectures, and strategic partnerships are best positioned to capitalize on these opportunities, ensuring continued innovation and market leadership in the years to come.

Memory Chip Industry Segmentation

-

1. Type

- 1.1. DRAM

- 1.2. SRAM

- 1.3. NOR Flash

- 1.4. NAND Flash

- 1.5. ROM & EPROM

- 1.6. Others

-

2. Application

- 2.1. Consumer Products

- 2.2. PC/Laptop

- 2.3. Smartphone/Tablet

- 2.4. Data Center

- 2.5. Automotive

- 2.6. Other Applications

Memory Chip Industry Segmentation By Geography

- 1. Americas

- 2. Europe

- 3. China

- 4. Japan

- 5. Asia Pacific

Memory Chip Industry Regional Market Share

Geographic Coverage of Memory Chip Industry

Memory Chip Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. DRAM

- 5.1.2. SRAM

- 5.1.3. NOR Flash

- 5.1.4. NAND Flash

- 5.1.5. ROM & EPROM

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Consumer Products

- 5.2.2. PC/Laptop

- 5.2.3. Smartphone/Tablet

- 5.2.4. Data Center

- 5.2.5. Automotive

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Americas

- 5.3.2. Europe

- 5.3.3. China

- 5.3.4. Japan

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Memory Chip Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. DRAM

- 6.1.2. SRAM

- 6.1.3. NOR Flash

- 6.1.4. NAND Flash

- 6.1.5. ROM & EPROM

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Consumer Products

- 6.2.2. PC/Laptop

- 6.2.3. Smartphone/Tablet

- 6.2.4. Data Center

- 6.2.5. Automotive

- 6.2.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Americas Memory Chip Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. DRAM

- 7.1.2. SRAM

- 7.1.3. NOR Flash

- 7.1.4. NAND Flash

- 7.1.5. ROM & EPROM

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Consumer Products

- 7.2.2. PC/Laptop

- 7.2.3. Smartphone/Tablet

- 7.2.4. Data Center

- 7.2.5. Automotive

- 7.2.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Memory Chip Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. DRAM

- 8.1.2. SRAM

- 8.1.3. NOR Flash

- 8.1.4. NAND Flash

- 8.1.5. ROM & EPROM

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Consumer Products

- 8.2.2. PC/Laptop

- 8.2.3. Smartphone/Tablet

- 8.2.4. Data Center

- 8.2.5. Automotive

- 8.2.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. China Memory Chip Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. DRAM

- 9.1.2. SRAM

- 9.1.3. NOR Flash

- 9.1.4. NAND Flash

- 9.1.5. ROM & EPROM

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Consumer Products

- 9.2.2. PC/Laptop

- 9.2.3. Smartphone/Tablet

- 9.2.4. Data Center

- 9.2.5. Automotive

- 9.2.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Japan Memory Chip Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. DRAM

- 10.1.2. SRAM

- 10.1.3. NOR Flash

- 10.1.4. NAND Flash

- 10.1.5. ROM & EPROM

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Consumer Products

- 10.2.2. PC/Laptop

- 10.2.3. Smartphone/Tablet

- 10.2.4. Data Center

- 10.2.5. Automotive

- 10.2.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific Memory Chip Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. DRAM

- 11.1.2. SRAM

- 11.1.3. NOR Flash

- 11.1.4. NAND Flash

- 11.1.5. ROM & EPROM

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Consumer Products

- 11.2.2. PC/Laptop

- 11.2.3. Smartphone/Tablet

- 11.2.4. Data Center

- 11.2.5. Automotive

- 11.2.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ROHM Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Kioxia Corporation*List Not Exhaustive 7 2 Vendor Rankin

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Micron Technology Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cypress Semiconductor Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Samsung Electronics Co Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 STMicroelectronics NV

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SK Hynix Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nvidia Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Maxim Integrated Products Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Intel Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 ROHM Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Memory Chip Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Americas Memory Chip Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: Americas Memory Chip Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Americas Memory Chip Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: Americas Memory Chip Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Americas Memory Chip Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: Americas Memory Chip Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Memory Chip Industry Revenue (Million), by Type 2025 & 2033

- Figure 9: Europe Memory Chip Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Memory Chip Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: Europe Memory Chip Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Memory Chip Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Memory Chip Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: China Memory Chip Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: China Memory Chip Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: China Memory Chip Industry Revenue (Million), by Application 2025 & 2033

- Figure 17: China Memory Chip Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: China Memory Chip Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: China Memory Chip Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Japan Memory Chip Industry Revenue (Million), by Type 2025 & 2033

- Figure 21: Japan Memory Chip Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Japan Memory Chip Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Japan Memory Chip Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Japan Memory Chip Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Japan Memory Chip Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Memory Chip Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Asia Pacific Memory Chip Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific Memory Chip Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Asia Pacific Memory Chip Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Memory Chip Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Memory Chip Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Memory Chip Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Memory Chip Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Memory Chip Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Memory Chip Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Global Memory Chip Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Memory Chip Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Memory Chip Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Memory Chip Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 9: Global Memory Chip Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Memory Chip Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Global Memory Chip Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Memory Chip Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Memory Chip Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Memory Chip Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 15: Global Memory Chip Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Memory Chip Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Global Memory Chip Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 18: Global Memory Chip Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Memory Chip Industry?

The projected CAGR is approximately 7.63%.

2. Which companies are prominent players in the Memory Chip Industry?

Key companies in the market include ROHM Co Ltd, Kioxia Corporation*List Not Exhaustive 7 2 Vendor Rankin, IBM Corporation, Micron Technology Inc, Cypress Semiconductor Corporation, Samsung Electronics Co Ltd, STMicroelectronics NV, SK Hynix Inc, Nvidia Corporation, Maxim Integrated Products Inc, Intel Corporation.

3. What are the main segments of the Memory Chip Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 148.95 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Penetration of 5G and IoT Devices; Growing Memory Requirement in Data Centers; Rising Demand from Consumer Electronics and Automotive Sectors.

6. What are the notable trends driving market growth?

Consumer Products is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Short battery Life.

8. Can you provide examples of recent developments in the market?

March 2022 - KioxiaCorporation, a provider of memory solutions, announced it would start construction of an advanced new fabrication facility at its KitakamiPlant in Japan for the possible expansion of manufacturing of its proprietary 3D Flash memory BiCSFLASHTM. Construction of this facility is planned to commence in April 2022 and is expected to be completed in 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Memory Chip Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Memory Chip Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Memory Chip Industry?

To stay informed about further developments, trends, and reports in the Memory Chip Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence