Key Insights

The Kuwaiti retail sector is projected for significant expansion, with a projected Compound Annual Growth Rate (CAGR) of 7.5% from 2024 to 2033. The market is estimated at $12.5 billion in 2024, driven by a young, affluent demographic with a taste for international brands, and government efforts to diversify the economy. Investments in modern retail infrastructure, including shopping malls and e-commerce, alongside high smartphone and internet penetration, are accelerating growth. This expansion is further supported by evolving consumer behaviors prioritizing convenience and digital accessibility.

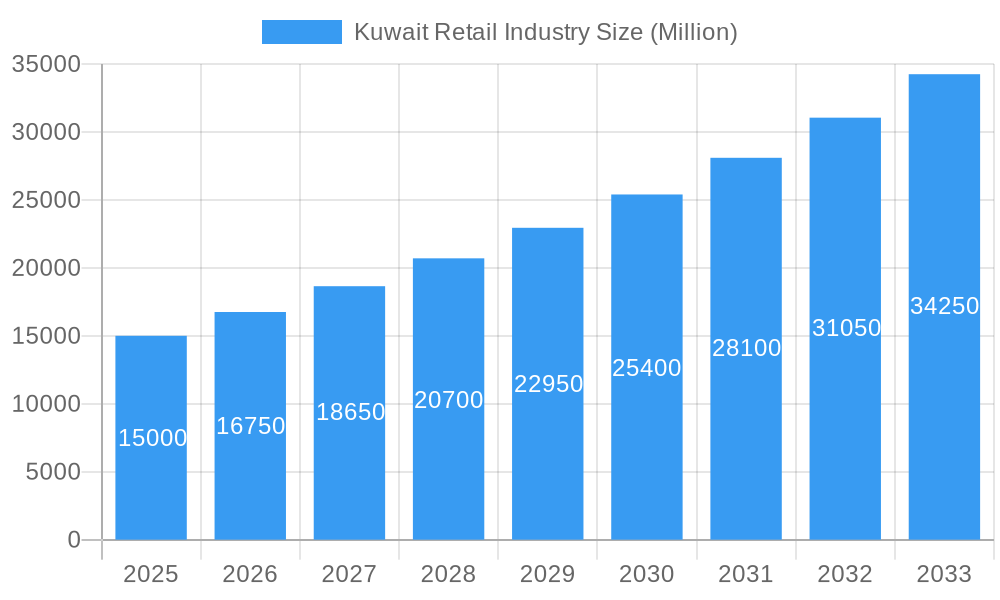

Kuwait Retail Industry Market Size (In Billion)

Market segmentation highlights steady demand in "Food and Beverage and Tobacco Products," with robust growth expected in "Electronic and Household Appliances" and "Personal and Household Care" due to rising living standards. E-commerce is rapidly becoming a dominant distribution channel, capturing market share from traditional retail as consumers embrace online convenience, wider selections, and competitive pricing. Despite potential challenges such as regional geopolitical factors and commodity price volatility, the strategic importance of retail for Kuwait's economic diversification, and the presence of established and emerging players, indicate a resilient market.

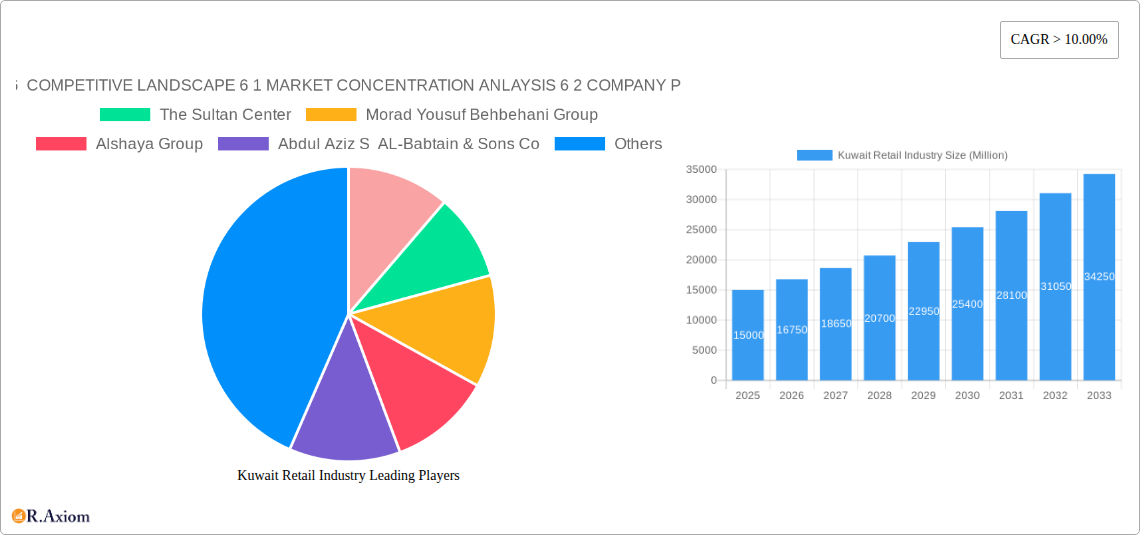

Kuwait Retail Industry Company Market Share

Kuwait Retail Industry Market Concentration & Innovation

This comprehensive report delves into the Kuwaiti retail landscape, analyzing its market concentration, key innovation drivers, and the evolving regulatory frameworks. The market exhibits a moderate concentration with 6 key players identified, including giants like Alshaya Group and Morad Yousuf Behbehani Group, who collectively hold a significant market share estimated at 55% within key segments. Innovation is primarily driven by digital transformation, with e-commerce adoption surging. The report examines the impact of product substitutes, such as the increasing availability of private label brands and online-only retailers, on traditional brick-and-mortar stores. End-user trends highlight a growing demand for convenience, personalized experiences, and sustainable products. Mergers and acquisitions (M&A) activity is on the rise, with an estimated 300 Million invested in strategic partnerships and acquisitions over the historical period (2019-2024) to consolidate market position and expand service offerings.

Kuwait Retail Industry Industry Trends & Insights

The Kuwait retail industry is poised for substantial growth, driven by a robust economic environment and a young, digitally-savvy population. The market is projected to expand at a Compound Annual Growth Rate (CAGR) of 8.5% from 2025 to 2033, reaching an estimated market size of 75,000 Million by the end of the forecast period. Technological disruptions are reshaping the industry, with significant investments in AI-powered personalization, contactless payment solutions, and sophisticated supply chain management systems. E-commerce penetration, already at a healthy 25% in the base year of 2025, is expected to climb steadily, driven by enhanced online platforms and efficient last-mile delivery networks. Consumer preferences are shifting towards experiential retail, where shopping is combined with entertainment and social interaction. This trend is fueling the growth of hypermarkets and specialized concept stores. Competitive dynamics are intensifying, with both established players and new entrants vying for market share. Foreign direct investment continues to play a crucial role, bringing in international brands and best practices. The report further explores the influence of evolving consumer lifestyles, including a growing emphasis on health and wellness, which is boosting demand for organic foods and sustainable personal care products. The government's initiatives to diversify the economy and promote digital adoption are also significant growth catalysts.

Dominant Markets & Segments in Kuwait Retail Industry

The Kuwait retail industry is characterized by the dominance of specific segments and distribution channels. Within the Product segmentation, Food and Beverage and Tobacco Products and Apparel, Footwear, and Accessories emerge as the largest segments, collectively accounting for an estimated 45% of the total market value in 2025. The Electronic and Household Appliances segment also demonstrates robust performance, driven by increasing disposable incomes and a high adoption rate of smart home technologies.

- Key Drivers for Dominant Segments:

- Food and Beverage and Tobacco Products: High population density, changing dietary habits, and the convenience of hypermarket shopping contribute to its sustained growth.

- Apparel, Footwear, and Accessories: A young demographic with a keen interest in fashion trends, coupled with the presence of international brands, drives this segment.

- Electronic and Household Appliances: Government initiatives promoting technological advancement and a growing demand for smart and energy-efficient products.

In terms of Distribution Channels, Stored-b (traditional brick-and-mortar stores, including hypermarkets, supermarkets, and department stores) currently holds the largest market share, estimated at 60% in 2025. However, E-commerce is the fastest-growing channel, projected to witness a CAGR of 15% during the forecast period, driven by convenience and a wider product selection. The "Other Di" category, which includes specialized retail formats and direct selling, is also showing promising growth, indicating a diversification of shopping preferences. Economic policies promoting consumer spending and infrastructure development supporting efficient logistics further bolster the dominance of these channels.

Kuwait Retail Industry Product Developments

Product innovation in Kuwait's retail sector is largely focused on enhancing customer experience and convenience. The integration of smart technologies in electronics, such as AI-powered appliances and connected devices, is a significant trend, offering enhanced functionality and personalized usage. In the Food and Beverage segment, there's a notable rise in demand for organic, healthy, and locally sourced products, reflecting a growing consumer consciousness towards well-being and sustainability. The apparel sector is witnessing a surge in demand for fast fashion alongside an increasing interest in sustainable and ethically produced clothing. These developments are driven by technological advancements in manufacturing and design, coupled with evolving consumer preferences. The competitive advantage lies in offering unique product assortments, leveraging data analytics for personalized recommendations, and ensuring seamless omnichannel experiences that bridge the gap between online and offline retail.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the Kuwait retail industry, meticulously segmented to offer actionable insights. The Product segments covered include: Food and Beverage and Tobacco Products, Personal and Household Care, Apparel, Footwear, and Accessories, Furniture, Toys, and Hobby, Industrial and Automotive, Electronic and Household Appliances, Pharmaceuticals, Luxury Goods, and Other Products. The Distribution Channel segments encompass: Stored-b (traditional retail), Direct Selling, E-commerce, and Other Di (specialty retail). The Food and Beverage segment is projected to maintain its leading position with an estimated market size of 18,000 Million in 2025. E-commerce is expected to experience the highest growth rate, with projections indicating a market size of 12,000 Million by 2033. Luxury Goods, though a smaller segment, demonstrates significant potential due to a high-net-worth population.

Key Drivers of Kuwait Retail Industry Growth

The Kuwait retail industry's growth is propelled by several interconnected factors. A burgeoning young population, coupled with increasing disposable incomes, fuels consumer spending. The government's commitment to economic diversification and its supportive policies for private sector development create a favorable business environment. Furthermore, the rapid adoption of digital technologies and the increasing penetration of e-commerce are revolutionizing shopping habits, driving online sales. Investments in infrastructure, including logistics and transportation networks, enhance operational efficiency and expand market reach. The growing appetite for international brands and diverse product offerings also contributes significantly to market expansion.

Challenges in the Kuwait Retail Industry Sector

Despite its growth trajectory, the Kuwait retail industry faces several challenges. Intense competition, both from local players and international brands, puts pressure on profit margins. Regulatory hurdles and complex import/export procedures can sometimes hinder smooth operations and expansion plans. Supply chain disruptions, exacerbated by global events, can lead to stockouts and increased costs. The ongoing shift towards e-commerce necessitates significant investment in digital infrastructure and logistics, which can be a barrier for smaller retailers. Furthermore, evolving consumer expectations for personalized experiences and sustainable practices require constant adaptation and innovation, posing a challenge for businesses unable to keep pace.

Emerging Opportunities in Kuwait Retail Industry

Emerging opportunities in the Kuwait retail industry lie in the burgeoning e-commerce sector, particularly in niche markets and specialized product categories. The increasing demand for sustainable and ethically sourced products presents a significant growth avenue for businesses aligning with these values. The rise of the "experience economy" also opens doors for innovative retail concepts that blend shopping with entertainment and personalized services. Leveraging big data and AI for hyper-personalization of customer journeys is another key opportunity. Furthermore, cross-border e-commerce and the potential for regional expansion offer attractive prospects for ambitious retailers. The government's focus on digitalization and supporting SMEs also presents a fertile ground for new ventures and collaborations.

Leading Players in the Kuwait Retail Industry Market

- The Sultan Center

- Morad Yousuf Behbehani Group

- Alshaya Group

- Abdul Aziz S AL-Babtain & Sons Co

- Gulf Franchising Company

- Future Communication Company Global

- Villa Moda

- Musaed Bader Al Sayer Group

- YIACO Medical Company

- SAFWAN's Pharma

Key Developments in Kuwait Retail Industry Industry

- 2023/10: Alshaya Group expands its e-commerce presence with new online store launches for popular fashion brands, boosting omnichannel capabilities.

- 2023/07: Morad Yousuf Behbehani Group invests in advanced supply chain technology to improve inventory management and delivery efficiency for electronics.

- 2022/12: The Sultan Center pioneers a new loyalty program integrating mobile app technology for personalized discounts and rewards, enhancing customer engagement.

- 2022/08: Future Communication Company Global launches a new range of smart home devices, catering to the growing demand for connected living solutions.

- 2021/05: Villa Moda introduces an exclusive collection of sustainable luxury fashion, aligning with global eco-conscious consumer trends.

Strategic Outlook for Kuwait Retail Industry Market

The strategic outlook for the Kuwait retail industry is exceptionally positive, characterized by sustained growth fueled by a dynamic consumer base and supportive economic policies. The increasing adoption of advanced technologies, particularly in e-commerce and data analytics, will be crucial for competitive advantage. Retailers that can effectively blend online and offline experiences, offer personalized services, and cater to the growing demand for sustainable products are best positioned for success. Strategic investments in supply chain optimization, customer relationship management, and innovative retail formats will be key growth catalysts. The market's evolution points towards a more integrated, technology-driven, and customer-centric retail ecosystem.

Kuwait Retail Industry Segmentation

-

1. Product

- 1.1. Food and Beverage and Tobacco Products

- 1.2. Personal and Household Care

- 1.3. Apparel, Footwear, and Accessories

- 1.4. Furniture, Toys, and Hobby

- 1.5. Industrial and Automotive

- 1.6. Electronic and Household Appliances

- 1.7. Pharmaceuticals, Luxury Goods, and Other Products

-

2. Distribution Channel

- 2.1. Stored-b

- 2.2. Direct Selling

- 2.3. E-commerce

- 2.4. Other Di

Kuwait Retail Industry Segmentation By Geography

- 1. Kuwait

Kuwait Retail Industry Regional Market Share

Geographic Coverage of Kuwait Retail Industry

Kuwait Retail Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Food and Beverage and Tobacco Products

- 5.1.2. Personal and Household Care

- 5.1.3. Apparel, Footwear, and Accessories

- 5.1.4. Furniture, Toys, and Hobby

- 5.1.5. Industrial and Automotive

- 5.1.6. Electronic and Household Appliances

- 5.1.7. Pharmaceuticals, Luxury Goods, and Other Products

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Stored-b

- 5.2.2. Direct Selling

- 5.2.3. E-commerce

- 5.2.4. Other Di

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Kuwait

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Kuwait Retail Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Food and Beverage and Tobacco Products

- 6.1.2. Personal and Household Care

- 6.1.3. Apparel, Footwear, and Accessories

- 6.1.4. Furniture, Toys, and Hobby

- 6.1.5. Industrial and Automotive

- 6.1.6. Electronic and Household Appliances

- 6.1.7. Pharmaceuticals, Luxury Goods, and Other Products

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Stored-b

- 6.2.2. Direct Selling

- 6.2.3. E-commerce

- 6.2.4. Other Di

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 6 COMPETITIVE LANDSCAPE 6 1 MARKET CONCENTRATION ANLAYSIS 6 2 COMPANY PROFILES

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 The Sultan Center

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Morad Yousuf Behbehani Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Alshaya Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Abdul Aziz S AL-Babtain & Sons Co

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Gulf Franchsing Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Future Communication Company Global

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Villa Moda

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Musaed Bader Al Sayer Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 YIACO Medical Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 SAFWAN's Pharma*List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 6 COMPETITIVE LANDSCAPE 6 1 MARKET CONCENTRATION ANLAYSIS 6 2 COMPANY PROFILES

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Kuwait Retail Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Kuwait Retail Industry Share (%) by Company 2025

List of Tables

- Table 1: Kuwait Retail Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Kuwait Retail Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Kuwait Retail Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Kuwait Retail Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 5: Kuwait Retail Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Kuwait Retail Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Kuwait Retail Industry?

The projected CAGR is approximately 7.5%.

2. Which companies are prominent players in the Kuwait Retail Industry?

Key companies in the market include 6 COMPETITIVE LANDSCAPE 6 1 MARKET CONCENTRATION ANLAYSIS 6 2 COMPANY PROFILES, The Sultan Center, Morad Yousuf Behbehani Group, Alshaya Group, Abdul Aziz S AL-Babtain & Sons Co, Gulf Franchsing Company, Future Communication Company Global, Villa Moda, Musaed Bader Al Sayer Group, YIACO Medical Company, SAFWAN's Pharma*List Not Exhaustive.

3. What are the main segments of the Kuwait Retail Industry?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increase in the population is Driving the Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Kuwait Retail Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Kuwait Retail Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Kuwait Retail Industry?

To stay informed about further developments, trends, and reports in the Kuwait Retail Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence