Key Insights

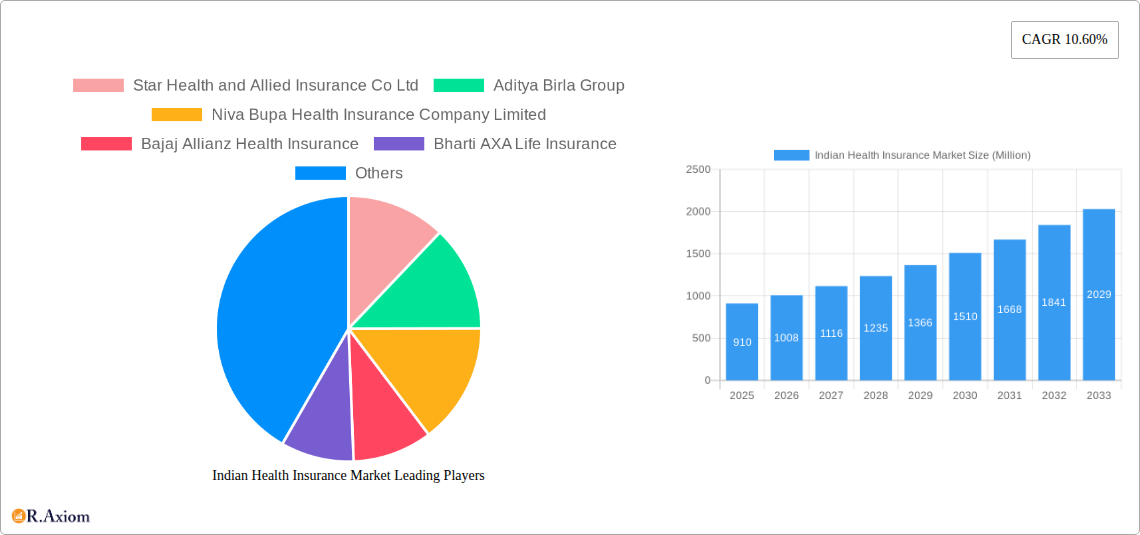

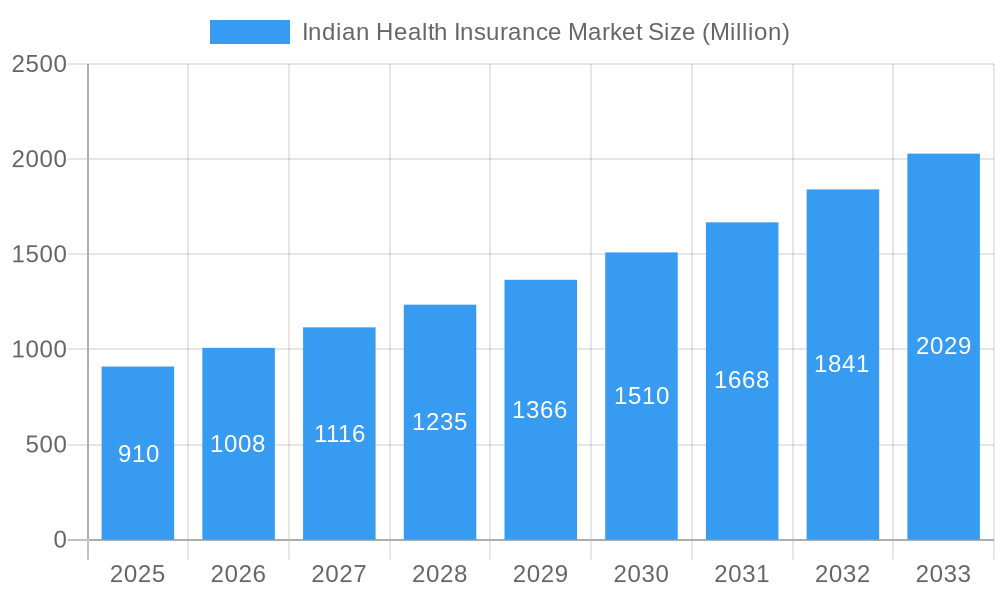

The Indian health insurance market, valued at $0.91 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 10.60% from 2025 to 2033. This surge is driven by several factors. Rising healthcare costs, increasing awareness of health insurance benefits, and government initiatives promoting health insurance coverage are key drivers. A growing middle class with increased disposable income is also fueling demand. Furthermore, the rise of telemedicine and digital health platforms is enhancing accessibility and convenience, contributing to market expansion. However, challenges remain, including low insurance penetration, particularly in rural areas, and a lack of understanding about policy benefits among the population. Competition within the sector is fierce, with major players like Star Health and Allied Insurance, Aditya Birla Group, and ICICI Lombard vying for market share. This competitive landscape is further intensified by the entry of new players and innovative product offerings. The market is segmented based on factors such as insurance type (individual vs. family, etc.), coverage level, and distribution channels. Addressing the challenges of affordability and accessibility will be critical for sustained growth in this dynamic market.

Indian Health Insurance Market Market Size (In Million)

The forecast period from 2025 to 2033 anticipates continued expansion, with the market size projected to exceed $2.5 billion by 2033 based on the 10.6% CAGR. This growth trajectory is expected to be influenced by factors including increasing public and private sector investments in healthcare infrastructure, innovative product development focused on affordability and digital accessibility, and potential government policies aimed at expanding health insurance coverage. However, factors such as fluctuating economic conditions and the potential for regulatory changes could influence the market's growth rate. Maintaining sustainable growth requires addressing issues such as fraud and claims management effectively. The Indian health insurance market is poised for significant expansion, but sustained success depends on proactive adaptation to evolving market dynamics and a consistent focus on consumer needs.

Indian Health Insurance Market Company Market Share

Indian Health Insurance Market: A Comprehensive Report (2019-2033)

This detailed report provides a comprehensive analysis of the Indian health insurance market, covering its growth trajectory, competitive landscape, and future outlook from 2019 to 2033. The study period spans 2019-2024 (historical period), with 2025 as the base and estimated year, and 2025-2033 as the forecast period. The report uses Million (M) as the unit for all monetary values.

Indian Health Insurance Market Concentration & Innovation

This section analyzes the market concentration, examining the market share held by key players and assessing the impact of mergers and acquisitions (M&A) activities. It also delves into the drivers of innovation, regulatory frameworks shaping the industry, the presence of product substitutes, evolving end-user trends, and recent M&A activity. The Indian health insurance market exhibits a moderately concentrated structure with a few large players commanding significant market share. For example, ICICI Lombard and HDFC Ergo collectively hold an estimated xx% of the market share in 2025 (estimated). However, the market is also characterized by a significant number of smaller players, leading to intense competition.

- Market Share (2025, Estimated): ICICI Lombard and HDFC Ergo (xx%), Star Health and Allied Insurance Co Ltd (xx%), Aditya Birla Health Insurance (xx%), Others (xx%).

- M&A Activity: While precise M&A deal values are difficult to obtain comprehensively without access to private deal data, the recent investment of Rs 665 crores (approximately xx Million USD) by the Abu Dhabi Investment Authority in Aditya Birla Health Insurance indicates substantial capital inflow and potential consolidation within the sector.

- Innovation Drivers: Technological advancements (telemedicine, AI-driven claims processing), changing consumer preferences (demand for comprehensive coverage), and government initiatives (Ayushman Bharat) are key innovation drivers.

- Regulatory Framework: IRDAI regulations significantly influence product offerings and market practices.

- Product Substitutes: Traditional healthcare financing methods pose a competitive challenge.

Indian Health Insurance Market Industry Trends & Insights

This section examines the growth drivers, technological disruptions, consumer behavior, and competitive forces shaping the Indian health insurance market. The market exhibits a robust Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), driven by rising healthcare costs, increasing health awareness, and expanding access to insurance products. Market penetration is estimated at xx% in 2025 (estimated), with significant growth potential in under-penetrated segments. The rising middle class, along with government initiatives to promote health insurance coverage, significantly contributes to market expansion. Technological disruptions, such as digital platforms and telemedicine, are transforming how insurance services are delivered, boosting efficiency and customer reach. Consumer preference is shifting towards comprehensive coverage, digital convenience, and value-added services.

Dominant Markets & Segments in Indian Health Insurance Market

This section identifies the leading regions, segments, and their drivers. While granular data on regional dominance may require further research to establish precise dominance, the analysis is based on available information and industry trends.

Key Drivers of Dominance:

- Urban Areas: Higher disposable incomes, better awareness, and access to insurance products.

- Private Sector: Innovation, customer focus, and wider distribution networks.

- Individual Health Insurance: Growing demand for personalized health cover.

Dominance Analysis: The urban areas, specifically in major metropolitan cities, are expected to lead the market, followed by rapidly developing tier-2 and tier-3 cities. The private sector, with its greater capacity for innovation and customer-centric offerings, dominates the market share. Similarly, the individual health insurance segment shows the highest growth and dominance due to rising awareness and demand for personalized coverage.

Indian Health Insurance Market Product Developments

Product innovation is driven by technological advancements, resulting in digital platforms for policy purchase and claims processing, telemedicine integration, and personalized health management tools. These innovations enhance customer experience, improve operational efficiency, and cater to evolving market demands. Competitive advantages arise from offering unique value propositions, including customized plans, preventive healthcare programs, and seamless digital integration.

Report Scope & Segmentation Analysis

This report segments the Indian health insurance market based on various factors including product type (individual, family, group), coverage (basic, comprehensive), distribution channel (online, offline), and region. Each segment is projected to exhibit distinct growth rates, market sizes, and competitive dynamics. Precise figures are subject to further market research due to the complexity and dynamic nature of the data.

- Product Type: The individual health insurance segment is expected to maintain its dominance.

- Coverage: Comprehensive health insurance plans are projected to exhibit rapid growth due to increasing demand.

- Distribution Channel: The online channel demonstrates significant growth potential.

- Region: Metropolitan cities are predicted to maintain high growth rates, followed by Tier II and Tier III cities.

Key Drivers of Indian Health Insurance Market Growth

Several factors fuel the growth of the Indian health insurance market, including:

- Rising Healthcare Costs: Inflationary pressures on medical expenses drive demand for health coverage.

- Increasing Health Awareness: Growing awareness of health risks promotes proactive insurance adoption.

- Government Initiatives: Government schemes like Ayushman Bharat aim to expand insurance access.

- Technological Advancements: Digital platforms and telemedicine improve accessibility and efficiency.

Challenges in the Indian Health Insurance Market Sector

The sector faces several challenges:

- Low Insurance Penetration: A large portion of the population remains uninsured.

- High Claims Ratio: Medical inflation affects the profitability of insurers.

- Regulatory Hurdles: Complex regulations create compliance costs.

- Fraud and Misrepresentation: These activities can negatively affect the insurer’s solvency.

Emerging Opportunities in Indian Health Insurance Market

Emerging opportunities abound in the Indian health insurance market, including:

- Expansion into Rural Areas: Untapped potential exists in under-served regions.

- Growth of Health Tech: Technological innovations can enhance efficiency and personalization.

- Focus on Preventive Care: Insurers can profit from promoting wellness and disease prevention.

Leading Players in the Indian Health Insurance Market Market

- Star Health and Allied Insurance Co Ltd

- Aditya Birla Group

- Niva Bupa Health Insurance Company Limited

- Bajaj Allianz Health Insurance

- Bharti AXA Life Insurance

- Religare

- HDFC Ergo

- Oriental Insurance

- ICICI Lombard

- United India Insurance

- Reliance Health Insurance

- New India Assurance

- National Assurance

- Cigna TTK

Key Developments in Indian Health Insurance Market Industry

- August 2022: Aditya Birla Health Insurance secured a Rs 665 crore investment from the Abu Dhabi Investment Authority, boosting its growth potential.

- July 2022: Bajaj Allianz Life Insurance partnered with City Union Bank, expanding its distribution network and customer reach.

Strategic Outlook for Indian Health Insurance Market Market

The Indian health insurance market is poised for sustained growth, fueled by rising healthcare costs, expanding insurance awareness, and supportive government policies. Technological advancements and innovative product offerings present significant opportunities for insurers to capture market share and enhance profitability. The focus on preventive healthcare, digitalization, and expansion into underserved areas will shape the future of the industry.

Indian Health Insurance Market Segmentation

-

1. Type of Insurance Provider

- 1.1. Public Sector Insurers

- 1.2. Private Sector Insurers

- 1.3. Standalone Health Insurance Companies

-

2. Type of Customer

- 2.1. Non-Corporate

-

3. Type of Coverage

- 3.1. Individual Insurance Coverage

- 3.2. Family or Floater (Group)Insurance Coverage

-

4. Product Type

- 4.1. Disease- specific Insurance

- 4.2. General Insurance

-

5. Demographics

- 5.1. Minors

- 5.2. Adults

- 5.3. Senior Citizens

-

6. Distribution Channel

- 6.1. Direct to Customers

- 6.2. Brokers

- 6.3. Individual Agents

- 6.4. Corporate Agents

- 6.5. Online

- 6.6. Bancassurance

- 6.7. Other Distribution Channels

Indian Health Insurance Market Segmentation By Geography

- 1. India

Indian Health Insurance Market Regional Market Share

Geographic Coverage of Indian Health Insurance Market

Indian Health Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Insurance Provider

- 5.1.1. Public Sector Insurers

- 5.1.2. Private Sector Insurers

- 5.1.3. Standalone Health Insurance Companies

- 5.2. Market Analysis, Insights and Forecast - by Type of Customer

- 5.2.1. Non-Corporate

- 5.3. Market Analysis, Insights and Forecast - by Type of Coverage

- 5.3.1. Individual Insurance Coverage

- 5.3.2. Family or Floater (Group)Insurance Coverage

- 5.4. Market Analysis, Insights and Forecast - by Product Type

- 5.4.1. Disease- specific Insurance

- 5.4.2. General Insurance

- 5.5. Market Analysis, Insights and Forecast - by Demographics

- 5.5.1. Minors

- 5.5.2. Adults

- 5.5.3. Senior Citizens

- 5.6. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.6.1. Direct to Customers

- 5.6.2. Brokers

- 5.6.3. Individual Agents

- 5.6.4. Corporate Agents

- 5.6.5. Online

- 5.6.6. Bancassurance

- 5.6.7. Other Distribution Channels

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type of Insurance Provider

- 6. Indian Health Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Insurance Provider

- 6.1.1. Public Sector Insurers

- 6.1.2. Private Sector Insurers

- 6.1.3. Standalone Health Insurance Companies

- 6.2. Market Analysis, Insights and Forecast - by Type of Customer

- 6.2.1. Non-Corporate

- 6.3. Market Analysis, Insights and Forecast - by Type of Coverage

- 6.3.1. Individual Insurance Coverage

- 6.3.2. Family or Floater (Group)Insurance Coverage

- 6.4. Market Analysis, Insights and Forecast - by Product Type

- 6.4.1. Disease- specific Insurance

- 6.4.2. General Insurance

- 6.5. Market Analysis, Insights and Forecast - by Demographics

- 6.5.1. Minors

- 6.5.2. Adults

- 6.5.3. Senior Citizens

- 6.6. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.6.1. Direct to Customers

- 6.6.2. Brokers

- 6.6.3. Individual Agents

- 6.6.4. Corporate Agents

- 6.6.5. Online

- 6.6.6. Bancassurance

- 6.6.7. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type of Insurance Provider

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Star Health and Allied Insurance Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Aditya Birla Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Niva Bupa Health Insurance Company Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bajaj Allianz Health Insurance

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bharti AXA Life Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Religare

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 HDFC Ergo

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Oriental Insurance

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ICICI Lombard

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 United India Insurance

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Reliance Health Insurance

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 New India Assurance

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 National Assurance

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Cigna TTK**List Not Exhaustive

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 Star Health and Allied Insurance Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian Health Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Indian Health Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Indian Health Insurance Market Revenue Million Forecast, by Type of Insurance Provider 2020 & 2033

- Table 2: Indian Health Insurance Market Volume Trillion Forecast, by Type of Insurance Provider 2020 & 2033

- Table 3: Indian Health Insurance Market Revenue Million Forecast, by Type of Customer 2020 & 2033

- Table 4: Indian Health Insurance Market Volume Trillion Forecast, by Type of Customer 2020 & 2033

- Table 5: Indian Health Insurance Market Revenue Million Forecast, by Type of Coverage 2020 & 2033

- Table 6: Indian Health Insurance Market Volume Trillion Forecast, by Type of Coverage 2020 & 2033

- Table 7: Indian Health Insurance Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: Indian Health Insurance Market Volume Trillion Forecast, by Product Type 2020 & 2033

- Table 9: Indian Health Insurance Market Revenue Million Forecast, by Demographics 2020 & 2033

- Table 10: Indian Health Insurance Market Volume Trillion Forecast, by Demographics 2020 & 2033

- Table 11: Indian Health Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 12: Indian Health Insurance Market Volume Trillion Forecast, by Distribution Channel 2020 & 2033

- Table 13: Indian Health Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 14: Indian Health Insurance Market Volume Trillion Forecast, by Region 2020 & 2033

- Table 15: Indian Health Insurance Market Revenue Million Forecast, by Type of Insurance Provider 2020 & 2033

- Table 16: Indian Health Insurance Market Volume Trillion Forecast, by Type of Insurance Provider 2020 & 2033

- Table 17: Indian Health Insurance Market Revenue Million Forecast, by Type of Customer 2020 & 2033

- Table 18: Indian Health Insurance Market Volume Trillion Forecast, by Type of Customer 2020 & 2033

- Table 19: Indian Health Insurance Market Revenue Million Forecast, by Type of Coverage 2020 & 2033

- Table 20: Indian Health Insurance Market Volume Trillion Forecast, by Type of Coverage 2020 & 2033

- Table 21: Indian Health Insurance Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 22: Indian Health Insurance Market Volume Trillion Forecast, by Product Type 2020 & 2033

- Table 23: Indian Health Insurance Market Revenue Million Forecast, by Demographics 2020 & 2033

- Table 24: Indian Health Insurance Market Volume Trillion Forecast, by Demographics 2020 & 2033

- Table 25: Indian Health Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 26: Indian Health Insurance Market Volume Trillion Forecast, by Distribution Channel 2020 & 2033

- Table 27: Indian Health Insurance Market Revenue Million Forecast, by Country 2020 & 2033

- Table 28: Indian Health Insurance Market Volume Trillion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Health Insurance Market?

The projected CAGR is approximately 10.60%.

2. Which companies are prominent players in the Indian Health Insurance Market?

Key companies in the market include Star Health and Allied Insurance Co Ltd, Aditya Birla Group, Niva Bupa Health Insurance Company Limited, Bajaj Allianz Health Insurance, Bharti AXA Life Insurance, Religare, HDFC Ergo, Oriental Insurance, ICICI Lombard, United India Insurance, Reliance Health Insurance, New India Assurance, National Assurance, Cigna TTK**List Not Exhaustive.

3. What are the main segments of the Indian Health Insurance Market?

The market segments include Type of Insurance Provider, Type of Customer, Type of Coverage, Product Type, Demographics, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.91 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Government Subsidized Health Insurance Schemes is Boosting the Sales of Health and Medical Insurance Policies.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

August 2022 : the boards of Aditya Birla Capital Ltd and its subsidiary Aditya Birla Health Insurance Co. Ltd approved an investment of Rs 665 crores by Abu Dhabi Investment Authority in the health insurer on Friday (ADIA). The funds will be used to fuel the growth of the health insurer.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Trillion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Health Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Health Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Health Insurance Market?

To stay informed about further developments, trends, and reports in the Indian Health Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence