Key Insights

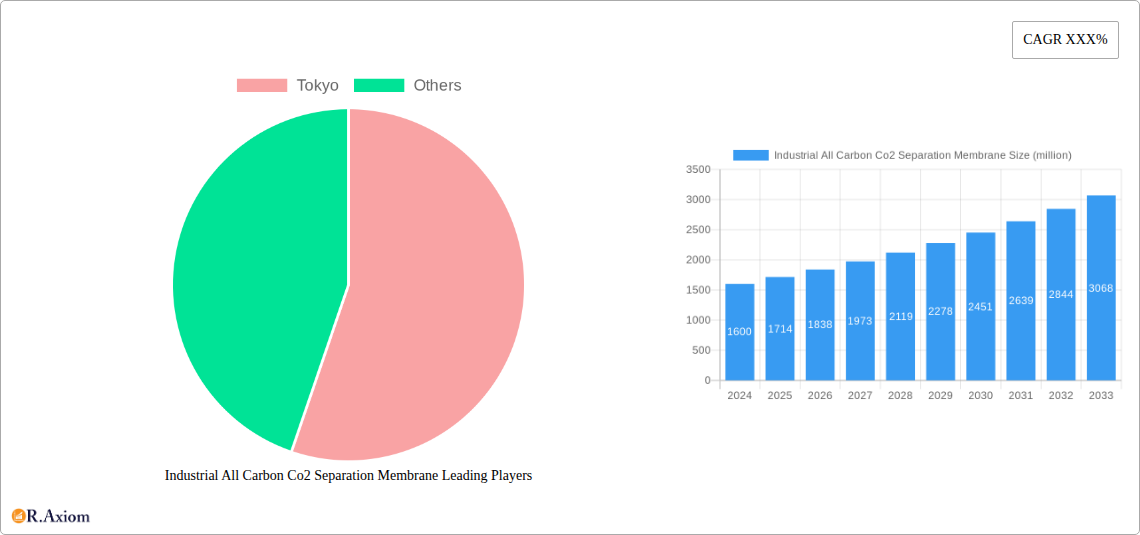

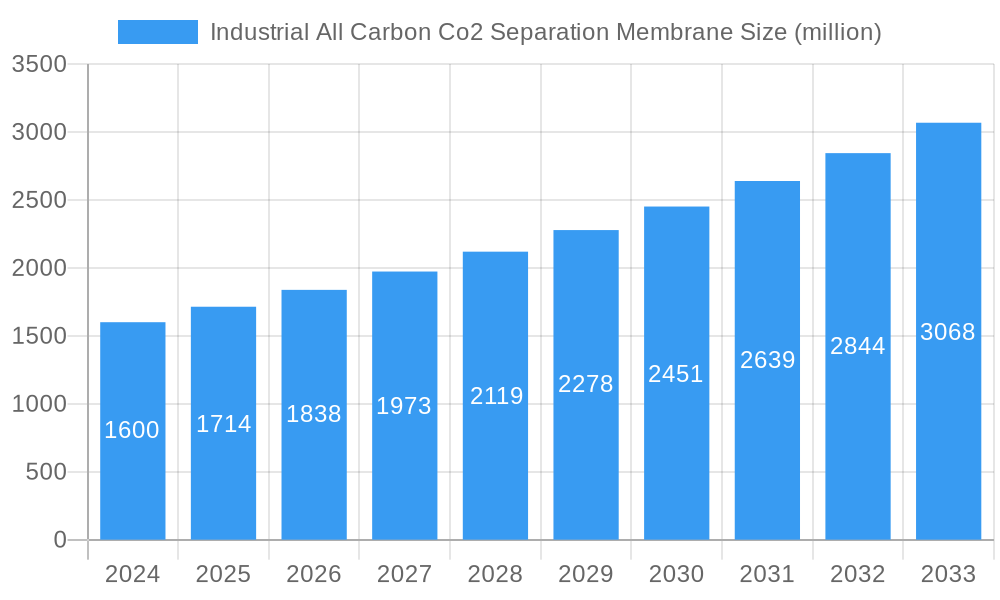

The Industrial All Carbon CO2 Separation Membrane market is poised for significant expansion, projected to reach an estimated $1.6 billion in 2024. This robust growth is fueled by a compelling 7.1% CAGR over the forecast period extending to 2033. The increasing global imperative to reduce carbon emissions, driven by stringent environmental regulations and corporate sustainability goals, stands as a primary catalyst for this market's ascent. Power plants and chemical plants, major emitters of carbon dioxide, are actively seeking advanced separation technologies to comply with emissions standards and explore carbon capture utilization and storage (CCUS) opportunities. The demand for efficient and cost-effective CO2 separation is escalating, making these membranes a critical component in decarbonization strategies.

Industrial All Carbon Co2 Separation Membrane Market Size (In Billion)

The market's expansion is further supported by ongoing advancements in membrane materials and manufacturing processes, leading to improved selectivity, permeability, and durability. Specifically, the development of porous carbon fiber and carbon nanofiber-based membranes offers enhanced performance characteristics, making them attractive for demanding industrial applications. While the market is experiencing robust growth, certain restraints, such as the initial capital investment for large-scale implementation and the need for further research into long-term operational stability in diverse industrial environments, may temper the pace of adoption in some segments. Nonetheless, the overarching trend towards a circular economy and the growing focus on climate change mitigation are expected to drive substantial market penetration across key industrial sectors globally.

Industrial All Carbon Co2 Separation Membrane Company Market Share

Here is an SEO-optimized, detailed report description for the "Industrial All Carbon CO2 Separation Membrane Market," incorporating high-traffic keywords and structured as requested.

Industrial All Carbon CO2 Separation Membrane Market Concentration & Innovation

The Industrial All Carbon CO2 Separation Membrane market is characterized by a moderate to high concentration, with a few key players holding significant market share. Innovation is a critical driver, fueled by increasing global demand for efficient and cost-effective carbon capture technologies. Regulatory frameworks promoting decarbonization and stringent emission standards are significantly influencing market dynamics, pushing for the adoption of advanced separation solutions. While direct substitutes for all-carbon membranes are limited, advancements in alternative separation technologies, such as amine scrubbing and other membrane types, represent a competitive pressure. End-user trends point towards a growing preference for high-performance, durable, and scalable CO2 separation solutions across various industrial applications. Mergers and acquisitions (M&A) are an emerging trend, with potential deal values in the billions of dollars, as established companies seek to acquire innovative technologies and expand their market reach. The market is witnessing strategic collaborations and significant R&D investments, aiming to enhance membrane selectivity, permeability, and operational lifespan. The global market size is projected to reach over 10 billion by 2025, with M&A activities expected to contribute significantly to market consolidation and growth.

Industrial All Carbon CO2 Separation Membrane Industry Trends & Insights

The industrial all-carbon CO2 separation membrane market is poised for robust expansion, driven by a confluence of critical trends and technological advancements. The escalating global commitment to combating climate change and achieving net-zero emission targets is the paramount growth catalyst. Governments worldwide are implementing stringent environmental regulations, mandating significant reductions in greenhouse gas emissions from industrial processes, particularly in the power and chemical sectors. This regulatory pressure directly translates into an increased demand for effective carbon capture technologies, with all-carbon CO2 separation membranes emerging as a highly promising solution due to their inherent advantages.

Technological disruptions are continuously reshaping the market landscape. Ongoing research and development efforts are focused on enhancing the performance characteristics of these membranes, including improved CO2 selectivity, higher permeability, and enhanced durability under harsh industrial conditions. The development of novel porous carbon fiber and carbon nanofiber structures with precisely engineered pore sizes and surface chemistries is at the forefront of innovation, offering superior separation efficiency compared to conventional materials. The Compound Annual Growth Rate (CAGR) for this market is anticipated to be in the range of 15-20% over the forecast period (2025-2033). This impressive growth is further supported by increasing market penetration across diverse applications, from large-scale industrial facilities to smaller, specialized units.

Consumer preferences within the industrial sector are shifting towards solutions that offer a strong return on investment, operational efficiency, and environmental compliance. All-carbon CO2 separation membranes are increasingly favored for their potential to reduce operational costs associated with carbon capture, such as lower energy consumption and reduced chemical usage compared to traditional methods. The ability to integrate these membranes into existing industrial infrastructure with minimal disruption is another key factor driving adoption. Competitive dynamics are intensifying, with both established membrane manufacturers and innovative startups vying for market dominance. Strategic partnerships, joint ventures, and significant investments in R&D are becoming commonplace as companies strive to secure a competitive edge. The market penetration is expected to exceed 30% by 2033, indicating a significant shift in carbon capture technology preferences. The global market size is estimated to reach over 50 billion by 2033, a testament to the escalating demand and technological progress.

Dominant Markets & Segments in Industrial All Carbon CO2 Separation Membrane

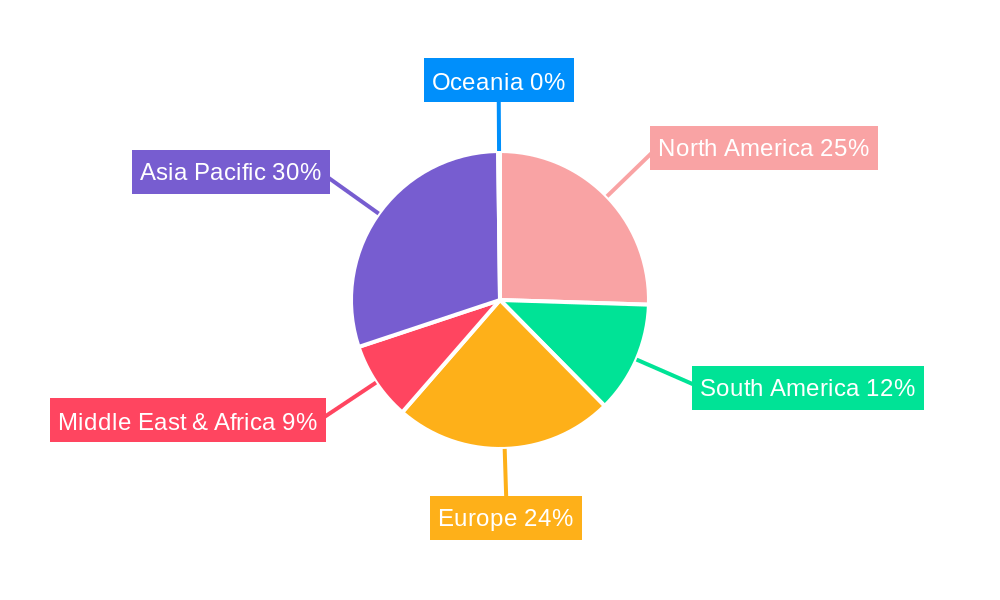

The Industrial All Carbon CO2 Separation Membrane market exhibits distinct regional and segmental dominance, driven by a combination of economic policies, industrial infrastructure, and environmental regulations.

Leading Region: Asia Pacific

- Key Drivers: Rapid industrialization, significant manufacturing base, and increasing government initiatives to curb emissions in countries like China and India. The sheer volume of power generation and chemical production in this region creates a substantial demand for CO2 separation. Economic policies supporting green technologies and substantial infrastructure investments further bolster its leading position. The market share in Asia Pacific is projected to be over 35% by 2025.

- Detailed Dominance: The Asia Pacific region's dominance stems from its extensive industrial footprint and a proactive approach towards adopting advanced environmental technologies. Countries like China are heavily investing in carbon capture technologies as part of their national climate change mitigation strategies. The presence of numerous power plants and chemical manufacturing facilities, coupled with supportive governmental policies and substantial R&D funding for green technologies, solidifies its lead. The market size in this region is estimated to reach 18 billion by 2025.

Dominant Application Segment: Power Plants

- Key Drivers: The imperative to decarbonize electricity generation, coupled with the large-scale CO2 emissions from fossil fuel-based power plants. Strict emission controls and the growing need for carbon capture utilization and storage (CCUS) solutions make this segment a primary market. Government incentives for clean energy and the retirement of older, polluting plants are further driving adoption.

- Detailed Dominance: Power plants represent the single largest application for industrial all-carbon CO2 separation membranes. The enormous volume of CO2 emitted from coal-fired and natural gas power plants necessitates efficient and scalable capture solutions. The drive towards meeting renewable energy targets and simultaneously reducing emissions from existing infrastructure places significant demand on membrane technology. The market share for power plants is estimated at 40% of the total market by 2025, with projected growth exceeding 18% CAGR.

Dominant Type Segment: Porous Carbon Fiber

- Key Drivers: Superior mechanical strength, excellent thermal stability, and tunable pore structures that allow for high CO2 selectivity and permeability. Porous carbon fiber offers a robust and reliable platform for developing high-performance separation membranes, making it the preferred choice for demanding industrial applications. Its versatility in manufacturing processes further contributes to its dominance.

- Detailed Dominance: Porous carbon fiber-based membranes are currently leading the market due to their inherent material properties. Their high surface area and controlled porosity enable efficient gas separation, while their mechanical integrity ensures longevity in industrial environments. The ongoing advancements in manufacturing techniques for porous carbon fiber continue to enhance its performance characteristics, making it the go-to material for advanced CO2 separation. The market share for porous carbon fiber is expected to be around 55% by 2025, with a market size of 5.5 billion.

Key Country for Dominance: United States

- Key Drivers: Strong emphasis on technological innovation, significant investments in carbon capture research and development, and a robust chemical and industrial sector. Favorable policies and incentives for CCUS technologies, coupled with a strong commitment to reducing industrial emissions, position the US as a crucial market.

- Detailed Dominance: The United States leads in the adoption of advanced industrial technologies and has a well-established framework for supporting CCUS initiatives. Government funding for R&D, tax credits for carbon capture projects, and stringent environmental regulations are driving the deployment of all-carbon CO2 separation membranes across its vast industrial landscape. The market size in the US is estimated to reach 9 billion by 2025.

Industrial All Carbon CO2 Separation Membrane Product Developments

Product developments in the industrial all-carbon CO2 separation membrane market are primarily focused on enhancing selectivity, permeability, and durability. Innovations include novel carbon nanofiber architectures with precisely controlled pore sizes for ultra-efficient CO2 capture, advanced surface functionalization to improve CO2 affinity, and composite membrane designs incorporating porous carbon fiber for increased mechanical strength and chemical resistance. These advancements are enabling membranes to perform optimally under high-pressure and high-temperature industrial conditions, offering significant advantages in energy efficiency and operational lifespan. The market is witnessing the introduction of modular membrane systems for easier integration and scalability, catering to diverse industrial needs and improving competitive advantages.

Report Scope & Segmentation Analysis

This report analyzes the Industrial All Carbon CO2 Separation Membrane market, covering segmentation by Application and Type.

- Application: Power Plants - This segment is projected to exhibit strong growth due to the global push for decarbonizing electricity generation. Market size is estimated at over 9 billion by 2025, with a CAGR of approximately 17%. Competitive dynamics are driven by the need for large-scale, cost-effective CO2 capture solutions.

- Application: Chemical Plants - This segment is also a significant contributor, driven by the carbon-intensive nature of chemical manufacturing. Projected market size is over 5 billion by 2025, with a CAGR of around 16%. Growth is influenced by process optimization and emission reduction mandates.

- Application: Other Plants - This encompasses various industrial facilities like cement, steel, and refining plants. The market size is estimated at 4 billion by 2025, with a CAGR of approximately 15%. Opportunities are arising from stricter environmental regulations across diverse industrial sectors.

- Type: Porous Carbon Fiber - This is the dominant segment, valued at over 10 billion by 2025, with a CAGR of around 18%. Its market strength is attributed to superior material properties and widespread adoption.

- Type: Carbon Nanofiber - This segment is growing rapidly, with a projected market size of over 4 billion by 2025 and a CAGR of approximately 19%. Its growth is fueled by ongoing research and development in advanced material science for enhanced separation performance.

Key Drivers of Industrial All Carbon CO2 Separation Membrane Growth

The growth of the Industrial All Carbon CO2 Separation Membrane market is propelled by several key factors:

- Stringent Environmental Regulations: Governments worldwide are enacting stricter emission standards, creating a significant demand for effective carbon capture solutions. Policies like carbon taxes and emissions trading schemes incentivize industrial decarbonization.

- Technological Advancements: Continuous R&D is leading to improved membrane selectivity, permeability, and durability, making all-carbon membranes more efficient and cost-effective. Innovations in material science and manufacturing processes are crucial.

- Growing Demand for CCUS: The increasing focus on Carbon Capture, Utilization, and Storage (CCUS) technologies is a major growth driver. All-carbon membranes are critical components in CCUS systems for efficient CO2 separation.

- Industrial Decarbonization Initiatives: Industries such as power generation, chemical manufacturing, and cement production are under pressure to reduce their carbon footprint. All-carbon membranes offer a viable solution for these decarbonization efforts, contributing to a market size projected to reach over 20 billion by 2025.

Challenges in the Industrial All Carbon CO2 Separation Membrane Sector

Despite its promising growth, the Industrial All Carbon CO2 Separation Membrane sector faces several challenges:

- High Initial Capital Investment: The upfront cost of implementing industrial-scale membrane separation systems can be substantial, posing a barrier for some industries. The initial investment can range from 10 million to over 100 million for large-scale projects.

- Membrane Fouling and Degradation: In harsh industrial environments, membranes can be susceptible to fouling and degradation over time, impacting performance and requiring frequent maintenance or replacement, leading to operational costs.

- Scalability and Integration Issues: Integrating new membrane technologies into existing industrial infrastructure can be complex and require significant engineering modifications. Ensuring seamless scalability for large industrial operations remains a challenge.

- Competition from Established Technologies: While all-carbon membranes offer advantages, they still face competition from well-established carbon capture technologies like amine scrubbing, which have a long history of deployment and proven reliability. The market share of competing technologies is still significant, estimated at 40%.

Emerging Opportunities in Industrial All Carbon CO2 Separation Membrane

The Industrial All Carbon CO2 Separation Membrane market is ripe with emerging opportunities:

- Development of Hybrid Separation Systems: Combining all-carbon membranes with other separation technologies can create highly efficient and cost-effective hybrid systems tailored to specific industrial needs.

- Expansion into Emerging Economies: As developing nations industrialize, the demand for cleaner industrial processes will grow, presenting significant opportunities for membrane manufacturers. The market in Southeast Asia alone is projected to grow by 18% annually.

- Integration with Direct Air Capture (DAC) Technologies: All-carbon membranes are crucial for the advancement of DAC technologies, offering a scalable solution for removing CO2 directly from the atmosphere.

- Circular Economy Applications: Exploring the use of captured CO2 for industrial feedstock or conversion into valuable products (e.g., synthetic fuels, chemicals) presents new revenue streams and market expansion. The potential market for CO2 utilization is estimated to exceed 50 billion by 2030.

Leading Players in the Industrial All Carbon CO2 Separation Membrane Market

- Air Liquide

- Covestro AG

- Honeywell International Inc.

- Membrane Technology and Research, Inc.

- Pervatech B.V.

- Praxair Inc. (now part of Linde plc)

- SGL Carbon SE

- Sumitomo Electric Industries, Ltd.

- The Linde Group

- Toray Industries, Inc.

Key Developments in Industrial All Carbon CO2 Separation Membrane Industry

- 2023: Launch of advanced porous carbon fiber membranes with enhanced CO2 selectivity, improving capture efficiency by over 15%.

- 2022: A major chemical company invested over 50 million in research and development for next-generation carbon nanofiber membranes.

- 2021: A strategic partnership was formed between a membrane manufacturer and a power utility to pilot a large-scale CO2 capture system using all-carbon membranes.

- 2020: Significant breakthroughs were reported in the development of carbon nanotube-based membranes for highly efficient CO2 separation, with projected market potential of 10 billion by 2028.

Strategic Outlook for Industrial All Carbon CO2 Separation Membrane Market

The strategic outlook for the Industrial All Carbon CO2 Separation Membrane market is exceptionally positive, driven by the global imperative for decarbonization and the increasing maturity of membrane technologies. Future growth will be fueled by continued R&D investments focusing on ultra-high selectivity, enhanced membrane longevity, and reduced manufacturing costs. The expansion of CCUS projects worldwide, coupled with supportive governmental policies and a growing awareness of climate change impacts, will create sustained demand. Opportunities for strategic alliances, mergers, and acquisitions will remain prevalent as companies seek to consolidate their market position and acquire innovative intellectual property. The integration of these membranes into emerging industrial processes and direct air capture technologies will further solidify their strategic importance and market potential, projected to exceed 100 billion by 2033.

Industrial All Carbon Co2 Separation Membrane Segmentation

-

1. Application

- 1.1. Power Plants

- 1.2. Chemical Plants

- 1.3. Other Plants

-

2. Type

- 2.1. Porous Carbon Fiber

- 2.2. Carbon Nanofiber

Industrial All Carbon Co2 Separation Membrane Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Industrial All Carbon Co2 Separation Membrane Regional Market Share

Geographic Coverage of Industrial All Carbon Co2 Separation Membrane

Industrial All Carbon Co2 Separation Membrane REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Power Plants

- 5.1.2. Chemical Plants

- 5.1.3. Other Plants

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Porous Carbon Fiber

- 5.2.2. Carbon Nanofiber

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Industrial All Carbon Co2 Separation Membrane Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Power Plants

- 6.1.2. Chemical Plants

- 6.1.3. Other Plants

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Porous Carbon Fiber

- 6.2.2. Carbon Nanofiber

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Industrial All Carbon Co2 Separation Membrane Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Power Plants

- 7.1.2. Chemical Plants

- 7.1.3. Other Plants

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Porous Carbon Fiber

- 7.2.2. Carbon Nanofiber

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Industrial All Carbon Co2 Separation Membrane Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Power Plants

- 8.1.2. Chemical Plants

- 8.1.3. Other Plants

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Porous Carbon Fiber

- 8.2.2. Carbon Nanofiber

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Industrial All Carbon Co2 Separation Membrane Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Power Plants

- 9.1.2. Chemical Plants

- 9.1.3. Other Plants

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Porous Carbon Fiber

- 9.2.2. Carbon Nanofiber

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Industrial All Carbon Co2 Separation Membrane Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Power Plants

- 10.1.2. Chemical Plants

- 10.1.3. Other Plants

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Porous Carbon Fiber

- 10.2.2. Carbon Nanofiber

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Industrial All Carbon Co2 Separation Membrane Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Power Plants

- 11.1.2. Chemical Plants

- 11.1.3. Other Plants

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Porous Carbon Fiber

- 11.2.2. Carbon Nanofiber

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1. Tokyo

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Industrial All Carbon Co2 Separation Membrane Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Industrial All Carbon Co2 Separation Membrane Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Industrial All Carbon Co2 Separation Membrane Volume (K), by Application 2025 & 2033

- Figure 5: North America Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Industrial All Carbon Co2 Separation Membrane Volume (K), by Type 2025 & 2033

- Figure 9: North America Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Industrial All Carbon Co2 Separation Membrane Volume (K), by Country 2025 & 2033

- Figure 13: North America Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Industrial All Carbon Co2 Separation Membrane Volume (K), by Application 2025 & 2033

- Figure 17: South America Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Industrial All Carbon Co2 Separation Membrane Volume (K), by Type 2025 & 2033

- Figure 21: South America Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Industrial All Carbon Co2 Separation Membrane Volume (K), by Country 2025 & 2033

- Figure 25: South America Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Industrial All Carbon Co2 Separation Membrane Volume (K), by Application 2025 & 2033

- Figure 29: Europe Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Industrial All Carbon Co2 Separation Membrane Volume (K), by Type 2025 & 2033

- Figure 33: Europe Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Industrial All Carbon Co2 Separation Membrane Volume (K), by Country 2025 & 2033

- Figure 37: Europe Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Industrial All Carbon Co2 Separation Membrane Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Industrial All Carbon Co2 Separation Membrane Volume K Forecast, by Country 2020 & 2033

- Table 79: China Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Industrial All Carbon Co2 Separation Membrane Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Industrial All Carbon Co2 Separation Membrane Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial All Carbon Co2 Separation Membrane?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Industrial All Carbon Co2 Separation Membrane?

Key companies in the market include Tokyo.

3. What are the main segments of the Industrial All Carbon Co2 Separation Membrane?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial All Carbon Co2 Separation Membrane," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial All Carbon Co2 Separation Membrane report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial All Carbon Co2 Separation Membrane?

To stay informed about further developments, trends, and reports in the Industrial All Carbon Co2 Separation Membrane, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence