Key Insights

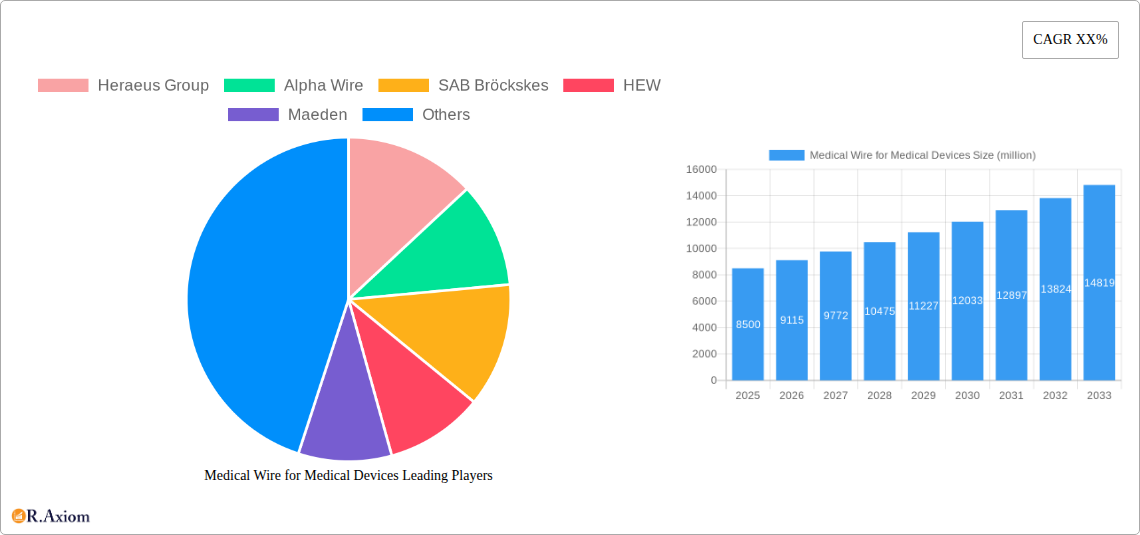

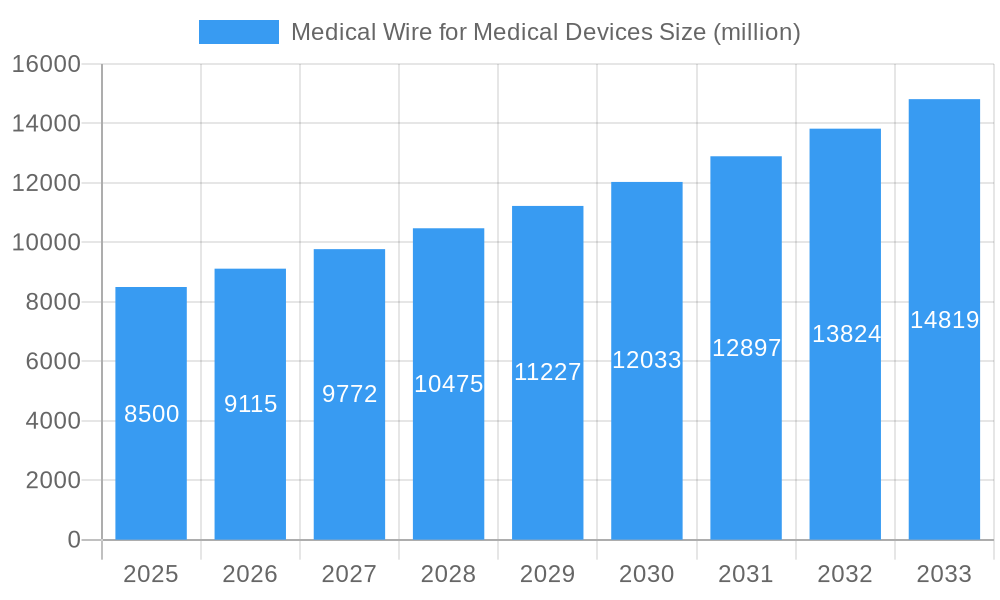

The global market for Medical Wires for Medical Devices is poised for robust expansion, estimated to reach approximately $8,500 million in 2025. This growth trajectory is fueled by an anticipated Compound Annual Growth Rate (CAGR) of around 7.2% throughout the forecast period extending to 2033. This expansion is primarily driven by the escalating demand for minimally invasive surgical procedures, which heavily rely on sophisticated medical wires for applications such as ultrasound imaging systems, intracardiac ablation catheters, and endoscopic therapeutic devices. The increasing prevalence of chronic diseases, coupled with advancements in medical technology leading to more complex and intricate device designs, further bolsters market growth. Moreover, the growing adoption of advanced materials like Nitinol and specialized alloys, offering superior biocompatibility, flexibility, and strength, contributes significantly to market value. The focus on developing smaller, more precise, and highly functional medical devices is a key catalyst, pushing manufacturers to invest in high-performance medical wire solutions.

Medical Wire for Medical Devices Market Size (In Billion)

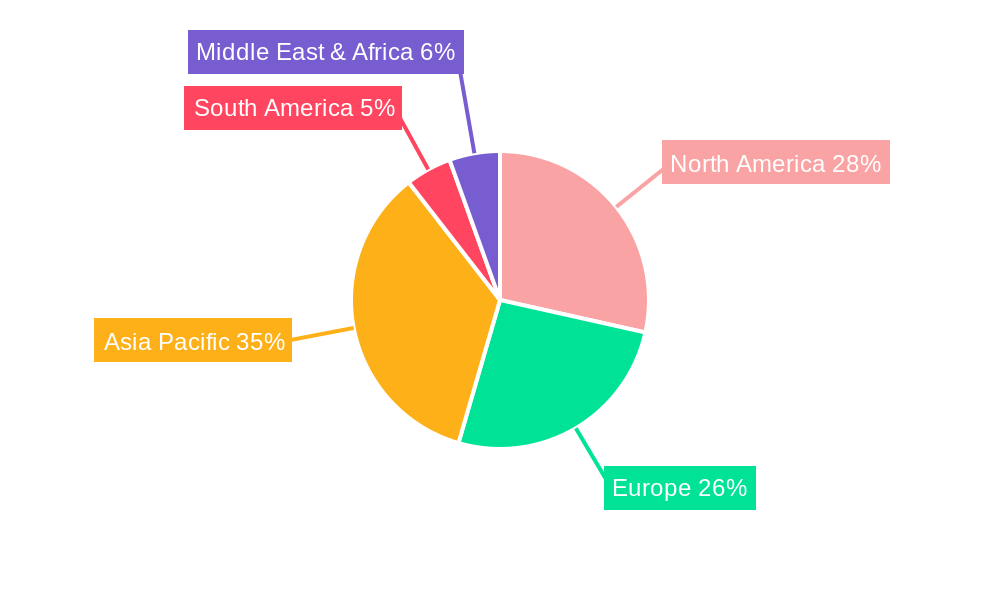

The market is characterized by several key trends that will shape its future landscape. A significant trend is the increasing integration of smart technologies into medical devices, demanding wires with enhanced conductivity and data transmission capabilities. Furthermore, the growing emphasis on personalized medicine and targeted therapies necessitates the development of highly specialized and customized medical wires. While the market presents substantial opportunities, certain restraints may influence its pace. These include the stringent regulatory landscape governing medical devices, which can prolong product development and approval cycles, and the high cost associated with raw materials for specialized alloys. Geographically, Asia Pacific is expected to emerge as a dominant region, driven by rapid industrialization, a growing healthcare infrastructure, and a large patient population, alongside North America and Europe, which are established hubs for medical device innovation and adoption.

Medical Wire for Medical Devices Company Market Share

Medical Wire for Medical Devices Market: Comprehensive Growth Analysis and Strategic Outlook (2019–2033)

This in-depth report provides a definitive analysis of the global Medical Wire for Medical Devices market, covering historical trends, current dynamics, and future projections. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this report offers actionable insights for industry stakeholders. It meticulously examines key segments, dominant players, technological advancements, and market drivers, equipping businesses with the knowledge to navigate this rapidly evolving landscape and capitalize on emerging opportunities.

Medical Wire for Medical Devices Market Concentration & Innovation

The Medical Wire for Medical Devices market exhibits a moderate level of concentration, characterized by a blend of established global manufacturers and specialized regional players. Innovation is primarily driven by the relentless demand for miniaturization, enhanced biocompatibility, and superior mechanical properties in medical devices. Regulatory frameworks, such as those set by the FDA and EMA, play a crucial role in shaping product development and market entry. Product substitutes exist, particularly in advanced polymer-based materials for certain less critical applications, but high-performance metallic wires remain indispensable for critical medical interventions. End-user trends are heavily influenced by the increasing prevalence of chronic diseases, an aging global population, and the growing adoption of minimally invasive surgical procedures, all of which fuel the demand for sophisticated medical devices employing advanced wires. Merger and acquisition (M&A) activities are strategic, focusing on acquiring niche technologies, expanding geographical reach, or consolidating market share. For instance, recent M&A deals within the broader medical device component sector have seen values in the range of 200 million to 500 million, signaling consolidation efforts. Key market share leaders are anticipated to hold positions ranging from 8% to 15% in specific niche segments, indicating fragmented yet competitive dynamics.

Medical Wire for Medical Devices Industry Trends & Insights

The global Medical Wire for Medical Devices market is poised for robust expansion, driven by a confluence of escalating healthcare expenditures, the burgeoning demand for advanced diagnostic and therapeutic tools, and relentless technological innovation. The compound annual growth rate (CAGR) is projected to be a healthy 7.5% from 2025 to 2033, with the market size expected to reach over 8,000 million by the end of the forecast period. Key growth drivers include the increasing prevalence of cardiovascular diseases and neurological disorders, necessitating the use of sophisticated wires in devices like pacemakers, stents, and neurostimulation systems. The growing adoption of minimally invasive surgery techniques worldwide further fuels demand for flexible, biocompatible, and highly conductive medical wires used in catheters, endoscopes, and surgical instruments. Technological disruptions, such as advancements in material science enabling the development of superelastic nitinol wires and ultra-fine tungsten wires, are expanding the application spectrum and improving device performance. Consumer preferences are leaning towards safer, more reliable, and less invasive medical procedures, directly impacting the demand for high-quality medical wires. The competitive dynamics are characterized by intense R&D efforts, strategic partnerships between wire manufacturers and medical device companies, and a focus on regulatory compliance and quality assurance. Market penetration for specialized medical wires is projected to increase significantly as new applications emerge and as healthcare infrastructure expands in developing economies, estimated at around 65% by 2033, up from 45% in 2024. The overall market value in 2025 is estimated at 5,500 million.

Dominant Markets & Segments in Medical Wire for Medical Devices

The Medical Wire for Medical Devices market is segmented by application and type, with specific regions and countries demonstrating significant dominance.

Application Segment Dominance:

- Medical Ultrasound Imaging Systems: This segment is a major contributor to market growth, driven by the increasing demand for diagnostic imaging globally. Factors like the rising incidence of fetal abnormalities, cardiac conditions, and abdominal diseases, coupled with the widespread adoption of portable ultrasound devices, are key drivers. Economic policies supporting healthcare infrastructure development and increased government spending on medical diagnostics in emerging economies are further bolstering this segment. The market size for this segment alone is projected to exceed 2,500 million by 2033.

- Intracardiac Ablation Catheters: The growing burden of atrial fibrillation and other cardiac arrhythmias is a significant catalyst for this segment. Advancements in catheter technology, enabling more precise and less invasive ablation procedures, directly translate to increased demand for specialized medical wires. Favorable reimbursement policies for electrophysiology procedures and an aging population prone to cardiac issues are critical economic factors. The market penetration in this segment is estimated at 75% in developed nations.

- Endoscopic Therapeutic Devices: With the increasing focus on minimally invasive procedures for gastrointestinal, pulmonary, and urological conditions, this segment is experiencing substantial growth. The development of sophisticated endoscopic instruments for diagnosis and treatment, such as guidewires and retrieval devices, is directly linked to the demand for high-performance medical wires. Investment in healthcare infrastructure and a growing awareness of the benefits of endoscopic procedures are key drivers. The market share for this segment is anticipated to reach 18% by 2033.

- Other Applications: This broad category includes wires used in neurostimulation, orthopedic implants, wound closure devices, and various other specialized medical instruments. The diversity of applications within this segment ensures steady growth, driven by ongoing innovation in each sub-sector.

Type Segment Dominance:

- Nitinol Wire: Nitinol wire stands out due to its unique superelasticity and shape memory properties, making it indispensable for applications requiring flexibility and resilience, such as guidewires, stents, and orthodontic archwires. The increasing demand for minimally invasive cardiac and peripheral vascular interventions is a primary growth driver. Technological advancements in manufacturing processes are improving its cost-effectiveness and accessibility, further enhancing its market dominance. The market share for Nitinol wire is estimated to reach 35% by 2033.

- Stainless Steel Wire: Stainless steel wires remain a foundational material in the medical device industry due to their excellent biocompatibility, corrosion resistance, and mechanical strength. They are widely used in surgical instruments, guidewires, and certain orthopedic applications. The consistent demand from established medical device manufacturers and its relatively lower cost compared to exotic alloys contribute to its sustained market presence.

- Platinum Wire: Platinum wire is crucial for applications requiring high conductivity, radiopacity, and biocompatibility, particularly in pacemakers, neurostimulators, and certain electrophysiological catheters. Its inert nature and excellent electrical properties make it a preferred choice for critical implantable devices. The growing market for implantable electronic devices is a key driver for this segment.

- Tungsten Wire: Known for its high tensile strength and density, tungsten wire finds applications in X-ray tubes, electrosurgical electrodes, and specialized surgical tools where precision and durability are paramount. The advancement of imaging technologies and surgical techniques is contributing to its demand.

Regional Dominance:

North America and Europe are currently the dominant regions, owing to established healthcare systems, high disposable incomes, and a strong presence of leading medical device manufacturers. However, the Asia-Pacific region is emerging as a high-growth market, driven by increasing healthcare investments, a large patient pool, and the expansion of manufacturing capabilities.

Medical Wire for Medical Devices Regional Market Share

Medical Wire for Medical Devices Product Developments

Recent product developments in medical wire for medical devices are characterized by a strong emphasis on enhanced performance and novel applications. Innovations include the development of ultra-fine stainless steel wires with improved tensile strength for delicate surgical procedures, advanced Nitinol alloys offering superior fatigue resistance and kink resistance for complex catheter designs, and biocompatible platinum alloys with optimized conductivity for next-generation implantable electronic devices. These developments are driven by the need for greater precision, improved patient outcomes, and the expansion of minimally invasive treatments. The competitive advantage lies in proprietary manufacturing techniques and material science breakthroughs that enable wires to withstand harsher physiological environments and meet stringent regulatory requirements.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Medical Wire for Medical Devices market, segmented by Application and Type.

- Application Segments: The report details the market size, growth projections, and competitive dynamics for Medical Ultrasound Imaging Systems, Intracardiac Ablation Catheters, Endoscopic Therapeutic Devices, and Other applications. For Medical Ultrasound Imaging Systems, a market size of 1,800 million is projected for 2025, with a CAGR of 8.2% from 2025-2033. Intracardiac Ablation Catheters are estimated at 1,500 million in 2025, with a CAGR of 7.8%. Endoscopic Therapeutic Devices are projected at 1,200 million in 2025, with a CAGR of 7.0%. The 'Other' segment is expected to reach 1,000 million in 2025, with a CAGR of 6.5%.

- Type Segments: Analysis includes Stainless Steel Wire, Nitinol Wire, Platinum Wire, Tungsten Wire, and Other types. Stainless Steel Wire is estimated at 2,000 million in 2025, with a CAGR of 6.8%. Nitinol Wire is projected at 1,600 million in 2025, with a CAGR of 9.5%. Platinum Wire is estimated at 800 million in 2025, with a CAGR of 7.2%. Tungsten Wire is projected at 500 million in 2025, with a CAGR of 6.0%. The 'Other' types segment is estimated at 600 million in 2025, with a CAGR of 5.5%.

Key Drivers of Medical Wire for Medical Devices Growth

The Medical Wire for Medical Devices market growth is primarily propelled by the rising global healthcare expenditure, which is projected to reach 12,000,000 million by 2033, indicating increased investment in medical technologies. The escalating prevalence of chronic diseases, particularly cardiovascular and neurological conditions, directly drives the demand for sophisticated implantable and interventional devices utilizing advanced medical wires. Furthermore, the continuous technological advancements in material science and manufacturing processes are enabling the development of wires with superior biocompatibility, miniaturization capabilities, and enhanced mechanical properties, thereby expanding their application scope. The growing preference for minimally invasive surgical procedures, coupled with favorable reimbursement policies for such interventions, is another significant growth catalyst.

Challenges in the Medical Wire for Medical Devices Sector

The Medical Wire for Medical Devices sector faces several significant challenges that can impede growth. Stringent regulatory approval processes for new medical devices and materials can lead to extended product development cycles and increased costs, estimated to add 15%-20% to R&D budgets. Supply chain complexities and the reliance on specific raw materials, such as rare earth elements for certain alloys, can result in price volatility and potential shortages, impacting production timelines and costs, with potential cost increases of up to 10% in raw material sourcing. Intense competition from both established players and emerging manufacturers can lead to pricing pressures. Moreover, the need for continuous investment in advanced manufacturing technologies and skilled labor to meet evolving industry standards presents a substantial financial and operational hurdle for many companies.

Emerging Opportunities in Medical Wire for Medical Devices

Emerging opportunities within the Medical Wire for Medical Devices market are abundant, driven by innovation and evolving healthcare needs. The growing demand for personalized medicine and advanced diagnostics presents a significant avenue for specialized, high-performance wires used in next-generation medical devices. The expanding applications of wearable health monitoring devices and smart implants will necessitate the development of highly flexible, biocompatible, and wirelessly connected micro-wires, creating a new market segment projected to grow by 25% annually. Furthermore, the increasing focus on sustainable manufacturing practices and the development of recyclable or biodegradable medical materials offer opportunities for companies that can innovate in this space. The expanding healthcare infrastructure and rising disposable incomes in emerging economies represent a vast untapped market for a wide range of medical wires.

Leading Players in the Medical Wire for Medical Devices Market

- Heraeus Group

- Alpha Wire

- SAB Bröckskes

- HEW

- Maeden

- LS Cable & System

- ZHAOLONG

- Proterial

- Plansee

- Nippon Steel SG Wire

- Ulbrich

- Haynes International

- Fort Wayne Metals Research Products

- ETCO

- Alleima

Key Developments in Medical Wire for Medical Devices Industry

- 2023 October: Alpha Wire launches a new line of ultra-high purity medical grade stainless steel wires, offering enhanced biocompatibility and corrosion resistance for demanding cardiovascular applications.

- 2023 September: Heraeus Group announces a significant investment in expanding its Nitinol wire production capacity to meet the growing global demand for advanced cardiovascular and orthopedic devices.

- 2023 July: SAB Bröckskes introduces a novel braided Nitinol wire composite for enhanced flexibility and kink resistance in complex neurovascular catheters.

- 2023 March: HEW receives FDA clearance for a new generation of platinum-iridium alloy wires designed for high-performance implantable pulse generators.

- 2022 November: LS Cable & System expands its medical wire portfolio with the introduction of micro-diameter tungsten wires for advanced endoscopic surgical instruments.

Strategic Outlook for Medical Wire for Medical Devices Market

The strategic outlook for the Medical Wire for Medical Devices market is overwhelmingly positive, fueled by sustained innovation and increasing global healthcare demands. Key growth catalysts include the continued advancement in material science, leading to the development of wires with superior performance characteristics such as increased flexibility, higher tensile strength, and enhanced biocompatibility. The ongoing shift towards minimally invasive surgical procedures and the rising adoption of implantable electronic devices will continue to drive demand. Companies that invest in R&D, focus on regulatory compliance, and build strong partnerships with medical device manufacturers are well-positioned for success. Furthermore, the expanding healthcare sector in emerging economies presents significant opportunities for market penetration and growth in the coming years.

Medical Wire for Medical Devices Segmentation

-

1. Application

- 1.1. Medical Ultrasound Imaging Systems

- 1.2. Intracardiac Ablation Catheters

- 1.3. Endoscopic Therapeutic Devices

- 1.4. Other

-

2. Types

- 2.1. Stainless Steel Wire

- 2.2. Nitinol Wire

- 2.3. Platinum Wire

- 2.4. Tungsten Wire

- 2.5. Other

Medical Wire for Medical Devices Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Wire for Medical Devices Regional Market Share

Geographic Coverage of Medical Wire for Medical Devices

Medical Wire for Medical Devices REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Medical Ultrasound Imaging Systems

- 5.1.2. Intracardiac Ablation Catheters

- 5.1.3. Endoscopic Therapeutic Devices

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Stainless Steel Wire

- 5.2.2. Nitinol Wire

- 5.2.3. Platinum Wire

- 5.2.4. Tungsten Wire

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Medical Wire for Medical Devices Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Medical Ultrasound Imaging Systems

- 6.1.2. Intracardiac Ablation Catheters

- 6.1.3. Endoscopic Therapeutic Devices

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Stainless Steel Wire

- 6.2.2. Nitinol Wire

- 6.2.3. Platinum Wire

- 6.2.4. Tungsten Wire

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Medical Wire for Medical Devices Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Medical Ultrasound Imaging Systems

- 7.1.2. Intracardiac Ablation Catheters

- 7.1.3. Endoscopic Therapeutic Devices

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Stainless Steel Wire

- 7.2.2. Nitinol Wire

- 7.2.3. Platinum Wire

- 7.2.4. Tungsten Wire

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Medical Wire for Medical Devices Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Medical Ultrasound Imaging Systems

- 8.1.2. Intracardiac Ablation Catheters

- 8.1.3. Endoscopic Therapeutic Devices

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Stainless Steel Wire

- 8.2.2. Nitinol Wire

- 8.2.3. Platinum Wire

- 8.2.4. Tungsten Wire

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Medical Wire for Medical Devices Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Medical Ultrasound Imaging Systems

- 9.1.2. Intracardiac Ablation Catheters

- 9.1.3. Endoscopic Therapeutic Devices

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Stainless Steel Wire

- 9.2.2. Nitinol Wire

- 9.2.3. Platinum Wire

- 9.2.4. Tungsten Wire

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Medical Wire for Medical Devices Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Medical Ultrasound Imaging Systems

- 10.1.2. Intracardiac Ablation Catheters

- 10.1.3. Endoscopic Therapeutic Devices

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Stainless Steel Wire

- 10.2.2. Nitinol Wire

- 10.2.3. Platinum Wire

- 10.2.4. Tungsten Wire

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Medical Wire for Medical Devices Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Medical Ultrasound Imaging Systems

- 11.1.2. Intracardiac Ablation Catheters

- 11.1.3. Endoscopic Therapeutic Devices

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Stainless Steel Wire

- 11.2.2. Nitinol Wire

- 11.2.3. Platinum Wire

- 11.2.4. Tungsten Wire

- 11.2.5. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Heraeus Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Alpha Wire

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SAB Bröckskes

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 HEW

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Maeden

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 LS Cable & System

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ZHAOLONG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Proterial

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Plansee

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nippon Steel SG Wire

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ulbrich

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Haynes International

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Fort Wayne Metals Research Products

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 ETCO

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Alleima

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Heraeus Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Medical Wire for Medical Devices Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Medical Wire for Medical Devices Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Medical Wire for Medical Devices Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Medical Wire for Medical Devices Volume (K), by Application 2025 & 2033

- Figure 5: North America Medical Wire for Medical Devices Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Medical Wire for Medical Devices Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Medical Wire for Medical Devices Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Medical Wire for Medical Devices Volume (K), by Types 2025 & 2033

- Figure 9: North America Medical Wire for Medical Devices Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Medical Wire for Medical Devices Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Medical Wire for Medical Devices Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Medical Wire for Medical Devices Volume (K), by Country 2025 & 2033

- Figure 13: North America Medical Wire for Medical Devices Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Medical Wire for Medical Devices Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Medical Wire for Medical Devices Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Medical Wire for Medical Devices Volume (K), by Application 2025 & 2033

- Figure 17: South America Medical Wire for Medical Devices Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Medical Wire for Medical Devices Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Medical Wire for Medical Devices Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Medical Wire for Medical Devices Volume (K), by Types 2025 & 2033

- Figure 21: South America Medical Wire for Medical Devices Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Medical Wire for Medical Devices Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Medical Wire for Medical Devices Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Medical Wire for Medical Devices Volume (K), by Country 2025 & 2033

- Figure 25: South America Medical Wire for Medical Devices Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Medical Wire for Medical Devices Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Medical Wire for Medical Devices Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Medical Wire for Medical Devices Volume (K), by Application 2025 & 2033

- Figure 29: Europe Medical Wire for Medical Devices Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Medical Wire for Medical Devices Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Medical Wire for Medical Devices Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Medical Wire for Medical Devices Volume (K), by Types 2025 & 2033

- Figure 33: Europe Medical Wire for Medical Devices Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Medical Wire for Medical Devices Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Medical Wire for Medical Devices Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Medical Wire for Medical Devices Volume (K), by Country 2025 & 2033

- Figure 37: Europe Medical Wire for Medical Devices Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Medical Wire for Medical Devices Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Medical Wire for Medical Devices Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Medical Wire for Medical Devices Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Medical Wire for Medical Devices Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Medical Wire for Medical Devices Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Medical Wire for Medical Devices Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Medical Wire for Medical Devices Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Medical Wire for Medical Devices Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Medical Wire for Medical Devices Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Medical Wire for Medical Devices Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Medical Wire for Medical Devices Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Medical Wire for Medical Devices Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Medical Wire for Medical Devices Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Medical Wire for Medical Devices Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Medical Wire for Medical Devices Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Medical Wire for Medical Devices Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Medical Wire for Medical Devices Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Medical Wire for Medical Devices Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Medical Wire for Medical Devices Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Medical Wire for Medical Devices Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Medical Wire for Medical Devices Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Medical Wire for Medical Devices Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Medical Wire for Medical Devices Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Medical Wire for Medical Devices Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Medical Wire for Medical Devices Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Wire for Medical Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Medical Wire for Medical Devices Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Medical Wire for Medical Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Medical Wire for Medical Devices Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Medical Wire for Medical Devices Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Medical Wire for Medical Devices Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Medical Wire for Medical Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Medical Wire for Medical Devices Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Medical Wire for Medical Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Medical Wire for Medical Devices Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Medical Wire for Medical Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Medical Wire for Medical Devices Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Medical Wire for Medical Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Medical Wire for Medical Devices Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Medical Wire for Medical Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Medical Wire for Medical Devices Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Medical Wire for Medical Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Medical Wire for Medical Devices Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Medical Wire for Medical Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Medical Wire for Medical Devices Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Medical Wire for Medical Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Medical Wire for Medical Devices Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Medical Wire for Medical Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Medical Wire for Medical Devices Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Medical Wire for Medical Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Medical Wire for Medical Devices Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Medical Wire for Medical Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Medical Wire for Medical Devices Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Medical Wire for Medical Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Medical Wire for Medical Devices Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Medical Wire for Medical Devices Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Medical Wire for Medical Devices Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Medical Wire for Medical Devices Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Medical Wire for Medical Devices Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Medical Wire for Medical Devices Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Medical Wire for Medical Devices Volume K Forecast, by Country 2020 & 2033

- Table 79: China Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Medical Wire for Medical Devices Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Medical Wire for Medical Devices Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Wire for Medical Devices?

The projected CAGR is approximately 6.4%.

2. Which companies are prominent players in the Medical Wire for Medical Devices?

Key companies in the market include Heraeus Group, Alpha Wire, SAB Bröckskes, HEW, Maeden, LS Cable & System, ZHAOLONG, Proterial, Plansee, Nippon Steel SG Wire, Ulbrich, Haynes International, Fort Wayne Metals Research Products, ETCO, Alleima.

3. What are the main segments of the Medical Wire for Medical Devices?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Wire for Medical Devices," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Wire for Medical Devices report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Wire for Medical Devices?

To stay informed about further developments, trends, and reports in the Medical Wire for Medical Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence