Key Insights

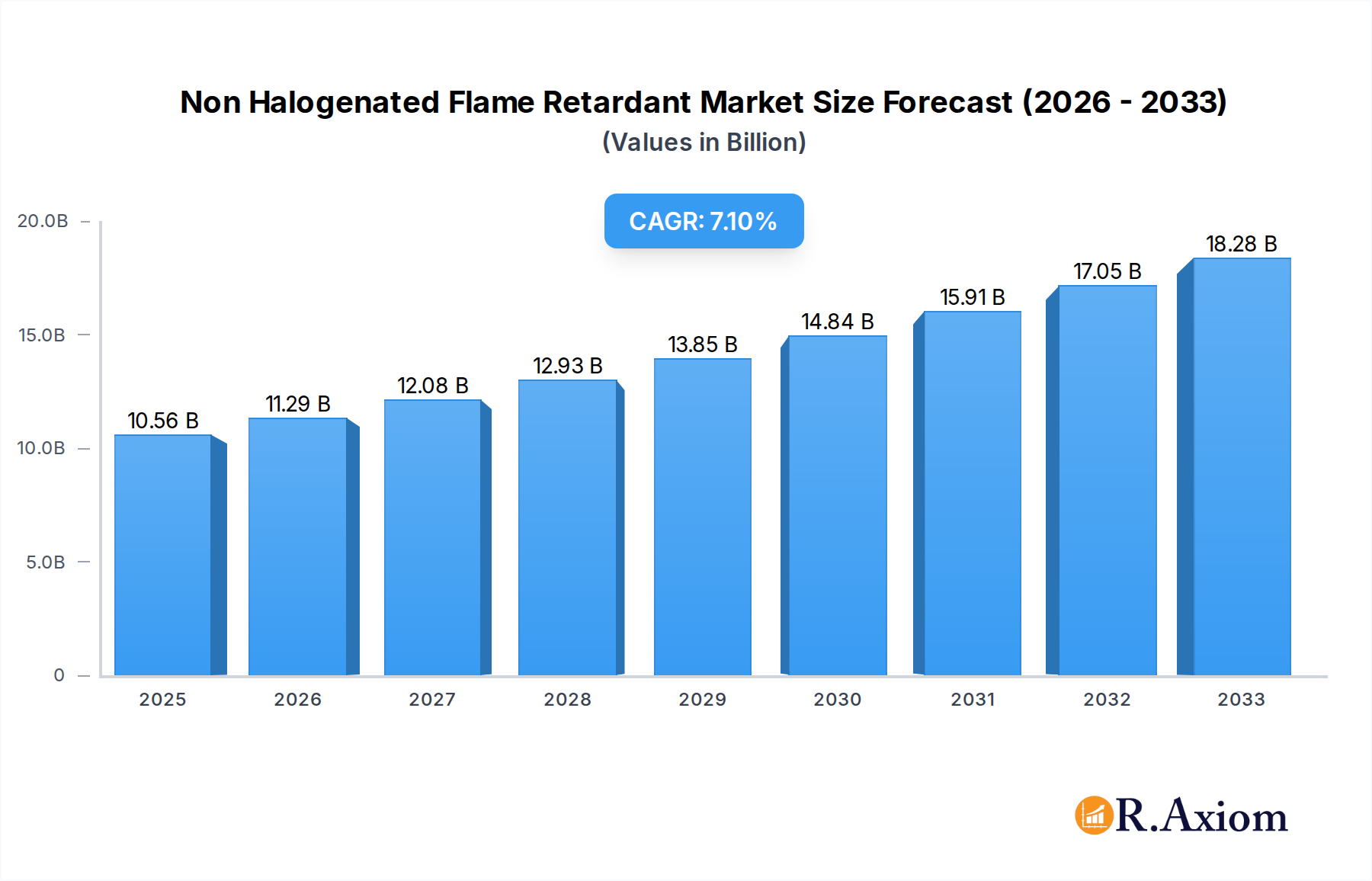

The global Non-Halogenated Flame Retardant market is poised for significant expansion, projected to reach an impressive $10,559.2 million in 2025. This growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 6.9% expected over the forecast period. A primary driver for this market's ascent is the increasing stringency of fire safety regulations across various industries, particularly in construction, electronics, and automotive sectors. The growing consumer demand for safer products, coupled with a heightened awareness of the environmental and health concerns associated with traditional halogenated flame retardants, is further propelling the adoption of their non-halogenated counterparts. Innovations in material science are yielding advanced non-halogenated flame retardant solutions with improved performance characteristics, reduced environmental impact, and cost-effectiveness, thereby widening their applicability and market penetration.

Non Halogenated Flame Retardant Market Size (In Billion)

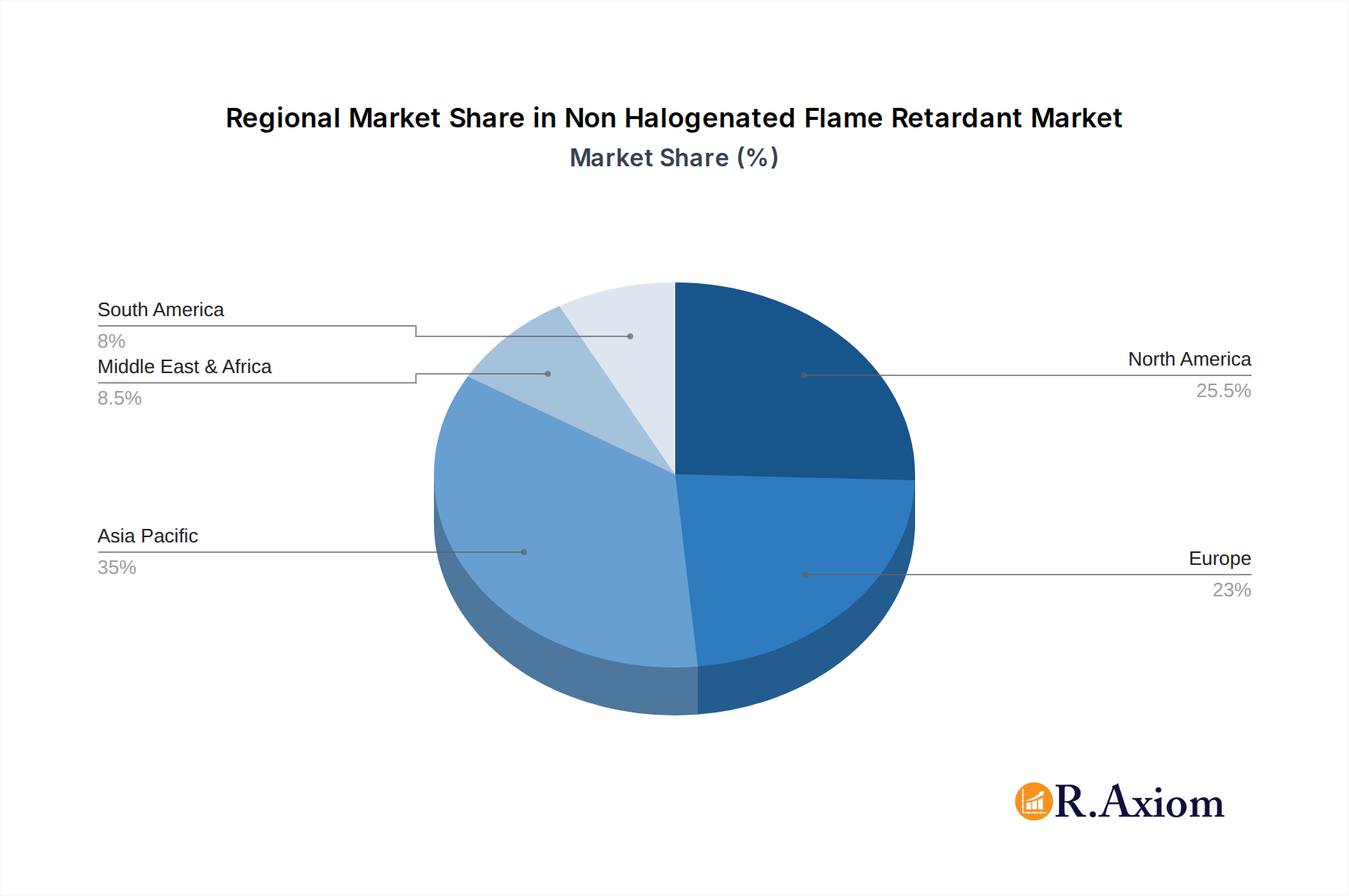

Key application segments driving this market include Polyolefins, Epoxy Resins, and Unsaturated Polyesters (UPE), which are extensively used in diverse end-use industries. The increasing adoption of flame retardant materials in automotive components, electrical and electronic devices, and building insulation materials are major growth catalysts. Geographically, the Asia Pacific region, led by China and India, is expected to witness the fastest growth due to rapid industrialization, burgeoning manufacturing activities, and substantial investments in infrastructure development. North America and Europe, while mature markets, continue to exhibit steady demand driven by regulatory mandates and the ongoing transition towards sustainable and safer chemical alternatives. The market is characterized by a competitive landscape with key players focusing on product innovation, strategic collaborations, and expanding their manufacturing capacities to cater to the growing global demand for non-halogenated flame retardants.

Non Halogenated Flame Retardant Company Market Share

SEO-Optimized, Detailed Report Description: Non-Halogenated Flame Retardant Market Analysis (2019-2033)

This comprehensive report offers an in-depth analysis of the global Non-Halogenated Flame Retardant market, a rapidly expanding sector driven by increasing safety regulations and a growing demand for environmentally friendly alternatives. Covering the historical period from 2019 to 2024, the base year of 2025, and a robust forecast period from 2025 to 2033, this study provides critical insights into market dynamics, key players, technological advancements, and future growth trajectories. With a focus on high-traffic keywords such as "eco-friendly flame retardants," "sustainable materials," "halogen-free solutions," and "advanced polymer additives," this report is an essential resource for industry stakeholders seeking to navigate this evolving landscape.

Non-Halogenated Flame Retardant Market Concentration & Innovation

The Non-Halogenated Flame Retardant market exhibits moderate concentration, with key players like Clariant International Ltd., Lanxess AG, Israel Chemicals Limited (ICL), Albemarle Corporation, Nabaltech AG., Chemtura Corporation Limited, BASF SE, Akzo Nobel, Huber Engineered Materials, Italmatch Chemicals, Mitsui Chemicals, Inc., DuPont de Nemours, Inc., and Evonik Industries AG holding significant market shares. Innovation is a primary driver, fueled by stringent environmental regulations pushing for the elimination of halogenated compounds due to their persistent organic pollutant (POP) characteristics. The development of novel, high-performance non-halogenated flame retardants with improved thermal stability, processing ease, and cost-effectiveness is paramount. Regulatory frameworks worldwide, particularly in Europe (REACH) and North America, continue to tighten restrictions on hazardous substances, directly benefiting the non-halogenated segment. While direct product substitutes are limited, ongoing research into synergistic flame retardant systems and bio-based alternatives presents a potential challenge and opportunity. End-user trends lean towards sustainable and safe materials across various applications, including electronics, construction, automotive, and textiles. Mergers and acquisitions (M&A) activity, valued in the hundreds of millions, is expected to continue as larger entities seek to consolidate their positions and acquire innovative technologies. For instance, recent M&A deals have focused on expanding production capacities and broadening product portfolios in specialty chemical segments.

Non-Halogenated Flame Retardant Industry Trends & Insights

The global Non-Halogenated Flame Retardant market is poised for significant expansion, driven by a confluence of robust growth drivers, technological disruptions, evolving consumer preferences, and dynamic competitive landscapes. The projected Compound Annual Growth Rate (CAGR) for the Non-Halogenated Flame Retardant market is estimated at approximately 7.5% over the forecast period from 2025 to 2033. This impressive growth trajectory is largely attributable to the escalating global demand for safer materials, particularly in sectors with high fire risk and stringent regulatory oversight. The increasing awareness and concern surrounding the environmental and health impacts of traditional halogenated flame retardants have created a substantial market penetration opportunity for their non-halogenated counterparts. Consumers and manufacturers alike are actively seeking sustainable and eco-friendly alternatives, pushing material suppliers to adopt greener chemistries. Technological advancements in the synthesis and application of non-halogenated flame retardants are continuously improving their performance characteristics, such as thermal stability, mechanical properties, and ease of processing, making them increasingly viable substitutes for halogenated options across a wider range of polymers. The development of novel inorganic flame retardants like advanced aluminum hydroxides and magnesium hydroxides, alongside sophisticated organophosphorus compounds and intumescent systems, is at the forefront of this innovation. These advancements enable enhanced fire safety without compromising the desired properties of the end products, whether in plastics for electronics, construction materials, automotive components, or textiles. The competitive landscape is characterized by intense R&D efforts, strategic partnerships, and a focus on product differentiation. Key players are investing heavily in expanding their production capacities and geographical reach to meet the burgeoning demand. Furthermore, the growing emphasis on circular economy principles and the demand for recyclable materials are influencing the development of non-halogenated flame retardants that are compatible with recycling processes. This trend is expected to further accelerate market growth as industries strive to meet sustainability targets and regulatory mandates. The market penetration of non-halogenated flame retardants is steadily increasing, replacing traditional halogenated alternatives in applications such as polyolefins, epoxy resins, unsaturated polyesters (UPE), poly-vinyl chloride (PVC), engineering thermoplastics (ETP), rubber, and styrenics. This shift is not merely regulatory driven; it is also influenced by the desire for enhanced product performance and brand reputation associated with sustainable practices. The future of the non-halogenated flame retardant market is bright, with continued innovation and a strong commitment to environmental responsibility shaping its growth for years to come.

Dominant Markets & Segments in Non-Halogenated Flame Retardant

The global Non-Halogenated Flame Retardant market demonstrates varied dominance across different regions and application segments, driven by specific economic policies, infrastructure development, and regulatory pressures.

Leading Region and Country Dominance

- Asia Pacific: This region is currently the largest and fastest-growing market for non-halogenated flame retardants.

- Key Drivers: Rapid industrialization, expanding manufacturing bases in countries like China and India, increasing domestic demand for electronics and automotive products, and a growing emphasis on environmental compliance in line with global standards. Government initiatives promoting green manufacturing and stricter fire safety regulations are also significant contributors.

- Dominance Analysis: China, in particular, leads due to its massive manufacturing output across various sectors that utilize flame retardants. The country’s evolving environmental policies are pushing manufacturers to adopt safer alternatives, creating a substantial demand for non-halogenated solutions. The extensive infrastructure development and construction projects also contribute to the demand for flame-retardant materials in building and construction applications.

Dominant Application Segments

- Polyolefins (e.g., Polypropylene, Polyethylene): This segment holds a significant market share, driven by its widespread use in automotive interiors, consumer electronics casings, packaging, and construction materials.

- Key Drivers: Cost-effectiveness, good processability, and the increasing demand for lightweight and safe materials in automotive applications to meet fuel efficiency standards and safety regulations. The stringent fire safety requirements in electronics further propel the adoption of non-halogenated flame retardants in polyolefin-based components.

- Engineering Thermoplastic (ETP) (e.g., Polyamides, Polycarbonates): ETPs are crucial for high-performance applications, and the demand for non-halogenated flame retardants here is driven by the need for superior fire resistance without compromising mechanical integrity.

- Key Drivers: Applications in electrical and electronic components, automotive under-the-hood parts, and industrial equipment. The growing trend towards miniaturization in electronics and the increasing complexity of automotive systems necessitate advanced flame retardant solutions.

- Epoxy Resins: This segment is vital for the electronics industry, particularly in printed circuit boards (PCBs) and encapsulation materials.

- Key Drivers: The stringent flammability standards for electronic devices and the need for high dielectric strength and thermal stability in epoxy-based materials. The phase-out of brominated flame retardants in this sector has led to a substantial shift towards non-halogenated alternatives.

- Poly-vinyl Chloride (PVC): While PVC inherently has flame-retardant properties, the demand for enhanced performance and specific certifications drives the use of non-halogenated additives.

- Key Drivers: Applications in construction (cables, flooring, window profiles), automotive interiors, and medical devices where fire safety is critical. The focus on reducing smoke and toxic gas emissions during combustion is a key factor.

Dominant Type Segments

- Aluminum Hydroxide: This inorganic compound is one of the most widely used and cost-effective non-halogenated flame retardants.

- Key Drivers: Its high loading capacity, good thermal stability, and excellent smoke suppression properties make it suitable for a broad range of polymers. Its environmental benignity and abundance contribute to its widespread adoption.

- Organo-phosphorus Chemicals: This category includes various phosphorus-based compounds that offer excellent flame retardancy, often with synergistic effects.

- Key Drivers: Their ability to form char layers, which insulate the underlying material from heat and oxygen, makes them highly effective. They are particularly favored in applications requiring good mechanical properties and electrical insulation, such as ETPs and epoxy resins.

Non-Halogenated Flame Retardant Product Developments

Recent product developments in the non-halogenated flame retardant market focus on enhancing efficacy, sustainability, and processability. Innovations include advanced aluminum and magnesium hydroxides with tailored particle sizes and surface treatments for improved dispersion in polymer matrices, leading to enhanced mechanical properties. The development of novel organophosphorus compounds, such as reactive flame retardants that chemically bond with polymers, offers superior durability and performance. Intumescent systems, designed to swell and form a protective char layer upon heating, are also seeing advancements, particularly for polyolefins and unsaturated polyesters. These developments aim to achieve higher levels of fire safety compliance while minimizing impact on the material's aesthetics and physical characteristics, providing a competitive edge in applications like electronics, automotive, and construction.

Report Scope & Segmentation Analysis

This report meticulously segments the Non-Halogenated Flame Retardant market across various dimensions to provide a granular understanding of its dynamics.

Application Segmentation:

- Polyolefins: This segment is projected to witness substantial growth, driven by increasing demand from the automotive and packaging industries. Expected market size in the billions with a CAGR of approximately 7.8%.

- Epoxy Resins: Crucial for the electronics sector, this segment is anticipated to grow steadily. Projected market size in the hundreds of millions with a CAGR of around 7.2%.

- Unsaturated Polyesters (UPE): Demand is strong from construction and marine applications. Expected market size in the hundreds of millions with a CAGR of approximately 6.9%.

- Poly-vinyl Chloride (PVC): A mature segment with consistent demand from construction and infrastructure. Projected market size in the billions with a CAGR of around 6.5%.

- Engineering Thermoplastic (ETP): This high-growth segment benefits from demand in automotive and electrical/electronic applications. Expected market size in the billions with a CAGR of approximately 8.1%.

- Rubber: Applications in tires and industrial rubber goods contribute to this segment's steady growth. Projected market size in the hundreds of millions with a CAGR of around 6.8%.

- Styrenics: Driven by applications in consumer goods and appliances. Expected market size in the hundreds of millions with a CAGR of approximately 7.0%.

Type Segmentation:

- Aluminum Hydroxide: Dominant type, offering cost-effectiveness and broad applicability. Expected market share in the billions.

- Organo-phosphorus Chemicals: High-performance type, particularly for demanding applications. Expected market share in the billions.

- Others: This category includes inorganic compounds like magnesium hydroxide and other specialty flame retardants. Expected market share in the hundreds of millions.

Key Drivers of Non-Halogenated Flame Retardant Growth

The growth of the Non-Halogenated Flame Retardant market is underpinned by several critical factors. Stringent global regulations, such as REACH and RoHS, that restrict the use of hazardous halogenated compounds, are a primary catalyst. The increasing consumer and industry demand for sustainable and eco-friendly materials, driven by corporate social responsibility initiatives and environmental consciousness, further bolsters adoption. Technological advancements in developing highly effective and cost-competitive non-halogenated alternatives are expanding their applicability across a wider range of polymers and end-use industries, including automotive, electronics, and construction. The rising awareness of health risks associated with halogenated flame retardants is also a significant driver pushing manufacturers towards safer alternatives, ensuring product safety and compliance.

Challenges in the Non-Halogenated Flame Retardant Sector

Despite robust growth, the Non-Halogenated Flame Retardant sector faces several challenges. Higher initial costs compared to some traditional halogenated flame retardants can be a barrier, especially in price-sensitive markets. Achieving equivalent performance levels, particularly in terms of thermal stability and processing characteristics, can sometimes require higher loading levels of non-halogenated additives, potentially impacting material properties and cost-effectiveness. Supply chain complexities and the need for specialized manufacturing processes for certain advanced non-halogenated compounds can also pose challenges. Furthermore, ongoing research into the long-term environmental impact and potential end-of-life issues for some newer chemistries requires continuous evaluation and innovation to ensure full sustainability.

Emerging Opportunities in Non-Halogenated Flame Retardant

Emerging opportunities in the Non-Halogenated Flame Retardant market are abundant and diverse. The development of bio-based and renewable flame retardants presents a significant avenue for growth, aligning with the circular economy and sustainability trends. Expansion into new and emerging applications, such as renewable energy infrastructure (solar panels, wind turbines), advanced textiles, and electric vehicle battery components, offers substantial market potential. Technological advancements in nanotechnology for flame retardant applications, enabling superior performance at lower concentrations, also represent a promising frontier. Furthermore, the growing demand for low-smoke and low-toxicity flame retardants in confined spaces like tunnels and public transportation systems creates niche opportunities for specialized non-halogenated solutions.

Leading Players in the Non-Halogenated Flame Retardant Market

- Clariant International Ltd.

- Lanxess AG

- Israel Chemicals Limited (ICL)

- Albemarle Corporation

- Nabaltech AG.

- Chemtura Corporation Limited

- BASF SE

- Akzo Nobel

- Huber Engineered Materials

- Italmatch Chemicals

- Mitsui Chemicals, Inc.

- DuPont de Nemours, Inc.

- Evonik Industries AG

Key Developments in Non-Halogenated Flame Retardant Industry

- 2023: Increased investment in R&D for novel organophosphorus flame retardants with improved thermal stability.

- 2023: Several key players announced capacity expansions for aluminum hydroxide production to meet rising demand.

- 2022: Launch of new intumescent flame retardant systems tailored for polyolefins in automotive applications.

- 2022: Strategic collaborations between chemical manufacturers and polymer producers to develop integrated flame retardant solutions.

- 2021: Growing trend towards acquisition of smaller, innovative flame retardant additive companies by larger corporations.

- 2021: Increased focus on bio-based flame retardants and their market viability.

Strategic Outlook for Non-Halogenated Flame Retardant Market

The strategic outlook for the Non-Halogenated Flame Retardant market remains exceptionally strong, driven by persistent regulatory pressures and a global shift towards sustainable manufacturing. Key growth catalysts include ongoing innovation in developing multifunctional flame retardants that offer enhanced performance, improved processability, and reduced environmental footprint. Strategic partnerships and mergers & acquisitions will continue to shape the competitive landscape, enabling companies to expand their technological capabilities and market reach. The increasing adoption of non-halogenated solutions in high-growth sectors like electric vehicles, advanced electronics, and sustainable construction materials will provide significant avenues for market expansion. Companies that prioritize research and development in eco-friendly chemistries and focus on providing tailored solutions for specific application needs will be well-positioned to capitalize on the expanding opportunities in this dynamic market.

Non Halogenated Flame Retardant Segmentation

-

1. Application

- 1.1. Polyolefins

- 1.2. Epoxy Resins

- 1.3. Unsaturated Polyesters (UPE)

- 1.4. Poly-vinyl Chloride (PVC)

- 1.5. Engineering Thermoplastic (ETP)

- 1.6. Rubber

- 1.7. Styrenics

-

2. Type

- 2.1. Aluminum Hydroxide

- 2.2. Organo-phosphorus Chemicals

- 2.3. Others

Non Halogenated Flame Retardant Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Non Halogenated Flame Retardant Regional Market Share

Geographic Coverage of Non Halogenated Flame Retardant

Non Halogenated Flame Retardant REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Polyolefins

- 5.1.2. Epoxy Resins

- 5.1.3. Unsaturated Polyesters (UPE)

- 5.1.4. Poly-vinyl Chloride (PVC)

- 5.1.5. Engineering Thermoplastic (ETP)

- 5.1.6. Rubber

- 5.1.7. Styrenics

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Aluminum Hydroxide

- 5.2.2. Organo-phosphorus Chemicals

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Non Halogenated Flame Retardant Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Polyolefins

- 6.1.2. Epoxy Resins

- 6.1.3. Unsaturated Polyesters (UPE)

- 6.1.4. Poly-vinyl Chloride (PVC)

- 6.1.5. Engineering Thermoplastic (ETP)

- 6.1.6. Rubber

- 6.1.7. Styrenics

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Aluminum Hydroxide

- 6.2.2. Organo-phosphorus Chemicals

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Non Halogenated Flame Retardant Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Polyolefins

- 7.1.2. Epoxy Resins

- 7.1.3. Unsaturated Polyesters (UPE)

- 7.1.4. Poly-vinyl Chloride (PVC)

- 7.1.5. Engineering Thermoplastic (ETP)

- 7.1.6. Rubber

- 7.1.7. Styrenics

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Aluminum Hydroxide

- 7.2.2. Organo-phosphorus Chemicals

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Non Halogenated Flame Retardant Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Polyolefins

- 8.1.2. Epoxy Resins

- 8.1.3. Unsaturated Polyesters (UPE)

- 8.1.4. Poly-vinyl Chloride (PVC)

- 8.1.5. Engineering Thermoplastic (ETP)

- 8.1.6. Rubber

- 8.1.7. Styrenics

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Aluminum Hydroxide

- 8.2.2. Organo-phosphorus Chemicals

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Non Halogenated Flame Retardant Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Polyolefins

- 9.1.2. Epoxy Resins

- 9.1.3. Unsaturated Polyesters (UPE)

- 9.1.4. Poly-vinyl Chloride (PVC)

- 9.1.5. Engineering Thermoplastic (ETP)

- 9.1.6. Rubber

- 9.1.7. Styrenics

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Aluminum Hydroxide

- 9.2.2. Organo-phosphorus Chemicals

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Non Halogenated Flame Retardant Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Polyolefins

- 10.1.2. Epoxy Resins

- 10.1.3. Unsaturated Polyesters (UPE)

- 10.1.4. Poly-vinyl Chloride (PVC)

- 10.1.5. Engineering Thermoplastic (ETP)

- 10.1.6. Rubber

- 10.1.7. Styrenics

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Aluminum Hydroxide

- 10.2.2. Organo-phosphorus Chemicals

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Non Halogenated Flame Retardant Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Polyolefins

- 11.1.2. Epoxy Resins

- 11.1.3. Unsaturated Polyesters (UPE)

- 11.1.4. Poly-vinyl Chloride (PVC)

- 11.1.5. Engineering Thermoplastic (ETP)

- 11.1.6. Rubber

- 11.1.7. Styrenics

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Aluminum Hydroxide

- 11.2.2. Organo-phosphorus Chemicals

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Clariant International Ltd.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Lanxess AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Israel Chemicals Limited (ICL)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Albemarle Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Nabaltech AG.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Chemtura Corporation Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BASF SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Akzo Nobel

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Huber Engineered Materials

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Italmatch Chemicals

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Mitsui Chemicals Inc.

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 DuPont de Nemours Inc.

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Evonik Industries AG

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Clariant International Ltd.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Non Halogenated Flame Retardant Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Non Halogenated Flame Retardant Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Non Halogenated Flame Retardant Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Non Halogenated Flame Retardant Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Non Halogenated Flame Retardant Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Non Halogenated Flame Retardant Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Non Halogenated Flame Retardant Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Non Halogenated Flame Retardant Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Non Halogenated Flame Retardant Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Non Halogenated Flame Retardant Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Non Halogenated Flame Retardant Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Non Halogenated Flame Retardant Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Non Halogenated Flame Retardant Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Non Halogenated Flame Retardant Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Non Halogenated Flame Retardant Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Non Halogenated Flame Retardant Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Non Halogenated Flame Retardant Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Non Halogenated Flame Retardant Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Non Halogenated Flame Retardant Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Non Halogenated Flame Retardant Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Non Halogenated Flame Retardant Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Non Halogenated Flame Retardant Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Non Halogenated Flame Retardant Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Non Halogenated Flame Retardant Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Non Halogenated Flame Retardant Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Non Halogenated Flame Retardant Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Non Halogenated Flame Retardant Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Non Halogenated Flame Retardant Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Non Halogenated Flame Retardant Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Non Halogenated Flame Retardant Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Non Halogenated Flame Retardant Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Non Halogenated Flame Retardant Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Non Halogenated Flame Retardant Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Non Halogenated Flame Retardant?

The projected CAGR is approximately 6.9%.

2. Which companies are prominent players in the Non Halogenated Flame Retardant?

Key companies in the market include Clariant International Ltd., Lanxess AG, Israel Chemicals Limited (ICL), Albemarle Corporation, Nabaltech AG., Chemtura Corporation Limited, BASF SE, Akzo Nobel, Huber Engineered Materials, Italmatch Chemicals, Mitsui Chemicals, Inc., DuPont de Nemours, Inc., Evonik Industries AG.

3. What are the main segments of the Non Halogenated Flame Retardant?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Non Halogenated Flame Retardant," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Non Halogenated Flame Retardant report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Non Halogenated Flame Retardant?

To stay informed about further developments, trends, and reports in the Non Halogenated Flame Retardant, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence