Key Insights

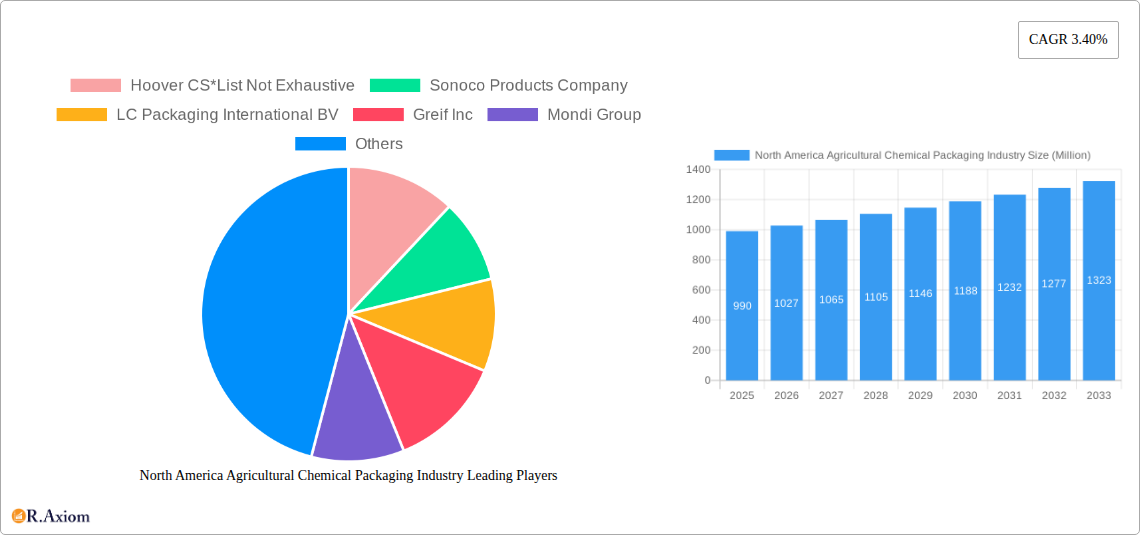

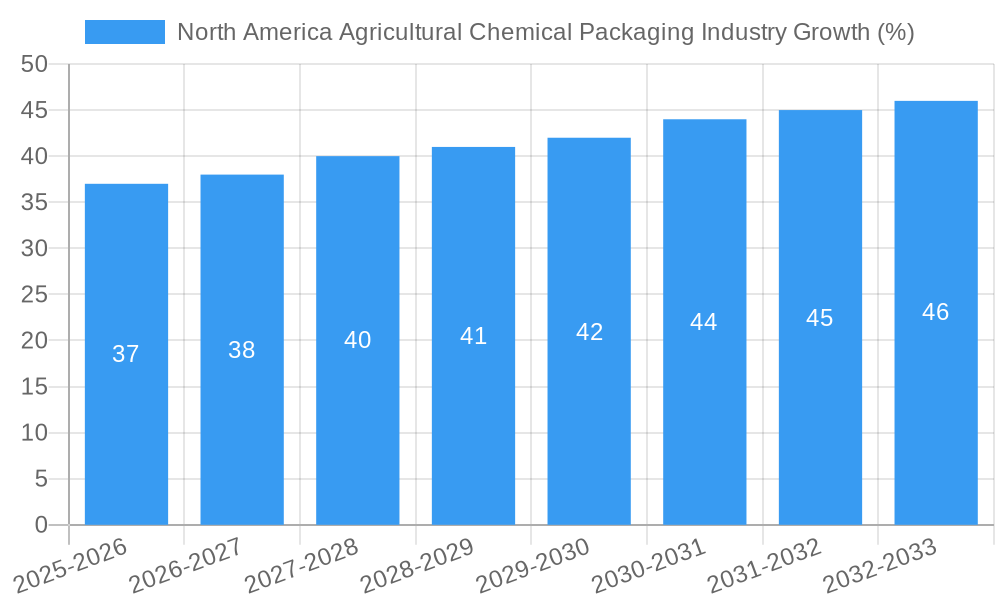

The North America agricultural chemical packaging market, valued at $0.99 billion in 2025, is projected to experience steady growth, driven by the increasing demand for agricultural products and the rising adoption of advanced packaging solutions to ensure product safety and efficacy. The market's Compound Annual Growth Rate (CAGR) of 3.40% from 2025 to 2033 reflects a consistent expansion, albeit at a moderate pace. Key drivers include the growing global population, necessitating increased agricultural output, and stringent government regulations promoting sustainable packaging materials. Trends such as the increasing adoption of flexible packaging (bags and pouches) for cost-effectiveness and ease of handling, along with the shift toward eco-friendly options like biodegradable plastics and recycled paperboard, are shaping the market landscape. While the market faces restraints such as fluctuating raw material prices and the potential for environmental concerns related to certain packaging types, these challenges are being addressed through innovations in sustainable and cost-effective materials and packaging designs. The market segmentation reveals a strong demand across various product types, including bags and pouches, containers and cans, and IBCs, with plastic remaining a dominant material type. Major players like Sonoco Products Company, Greif Inc., and Mondi Group are strategically investing in research and development to offer innovative and sustainable solutions, fostering competition and driving market growth. The North American region, encompassing the United States, Canada, and Mexico, holds a significant market share, boosted by intensive agricultural activities and robust regulatory frameworks.

The forecast period (2025-2033) suggests a continued expansion of the North American agricultural chemical packaging market, particularly fueled by advancements in sustainable packaging materials and the adoption of efficient supply chain management practices. The market's segmentation by application type (fertilizers, pesticides, herbicides) reveals a diverse demand pattern across various agricultural chemicals. While plastic continues to dominate due to its versatility and cost-effectiveness, the rising awareness of environmental concerns is expected to propel the adoption of eco-friendly alternatives. Companies are responding to these trends by investing in research and development of biodegradable and compostable materials, driving the adoption of more sustainable packaging solutions. Furthermore, the increasing demand for tamper-evident and specialized packaging solutions for enhanced product security is further driving market growth. The competitive landscape is marked by the presence of both large multinational corporations and specialized packaging companies, with continuous innovation and strategic partnerships shaping market dynamics.

This comprehensive report provides an in-depth analysis of the North America agricultural chemical packaging industry, covering market size, segmentation, growth drivers, challenges, and key players. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report offers actionable insights for industry stakeholders, investors, and businesses seeking to navigate this dynamic market.

North America Agricultural Chemical Packaging Industry Market Concentration & Innovation

The North American agricultural chemical packaging market exhibits a moderately consolidated structure, with several major players holding significant market share. Hoover CS, Sonoco Products Company, LC Packaging International BV, Greif Inc., Mondi Group, Tri Rinse, ProAmpac LLC, Mauser Packaging Solutions, and Silgan Holdings are some of the key participants. However, the presence of numerous smaller players and regional specialists contributes to a competitive landscape. Market concentration is further influenced by factors such as M&A activity. For instance, Greif Inc.'s divestiture of its Flexible Packaging joint venture (FPS) for USD 123 Million in April 2022 significantly impacted market dynamics, altering market share distribution and debt structures within the industry. The value of other M&A deals during the study period is estimated at xx Million. Innovation within the sector is driven by the need for sustainable and efficient packaging solutions, stringent environmental regulations, and advancements in material science. Key innovation areas include lightweighting, recyclable materials (such as biodegradable plastics and recycled paperboard), improved barrier properties, and smart packaging technologies. The regulatory framework, focused on reducing environmental impact, further pushes innovation towards eco-friendly alternatives. The increasing preference for sustainable packaging among agricultural chemical producers and consumers also acts as a significant driver for innovation. Substitutes for traditional packaging materials are emerging, including bio-based polymers and compostable materials, but their market penetration remains limited as of 2025.

North America Agricultural Chemical Packaging Industry Industry Trends & Insights

The North American agricultural chemical packaging market is experiencing robust growth, driven by the increasing demand for agricultural chemicals globally and the rising awareness of sustainable packaging solutions. The industry's CAGR during the forecast period (2025-2033) is projected to be xx%. This growth is fueled by several factors: rising agricultural output, increasing adoption of advanced farming techniques, technological advancements in packaging materials, and a growing focus on supply chain optimization. Technological disruptions, such as the rise of automation in packaging processes and the use of advanced materials, are transforming the industry. Consumer preferences are shifting towards sustainable and eco-friendly packaging, pushing companies to adopt recycled and renewable materials. Competitive dynamics are intense, with companies focusing on product differentiation, cost optimization, and strategic partnerships to maintain their market position. Market penetration of sustainable packaging options is slowly increasing, reaching an estimated xx% in 2025.

Dominant Markets & Segments in North America Agricultural Chemical Packaging Industry

Dominant Segments:

- By Product Type: Bags and pouches hold the largest market share, driven by their versatility and cost-effectiveness. Containers and cans are also significant, particularly for liquid and semi-liquid products. IBCs are crucial for bulk transportation, and 'Other Product Types' represent specialized packaging solutions.

- By Material Type: Plastic remains the dominant material, offering durability and cost-effectiveness. However, the growing emphasis on sustainability is driving the adoption of paper and paperboard alternatives. Metal packaging retains its niche in specific applications. 'Other Materials' include bioplastics and other innovative materials with increasing but still limited market share in 2025.

- By Application Type: Fertilizers represent the largest application segment, followed by pesticides and herbicides. 'Other Application Types' represent niche applications within the agricultural chemical sector.

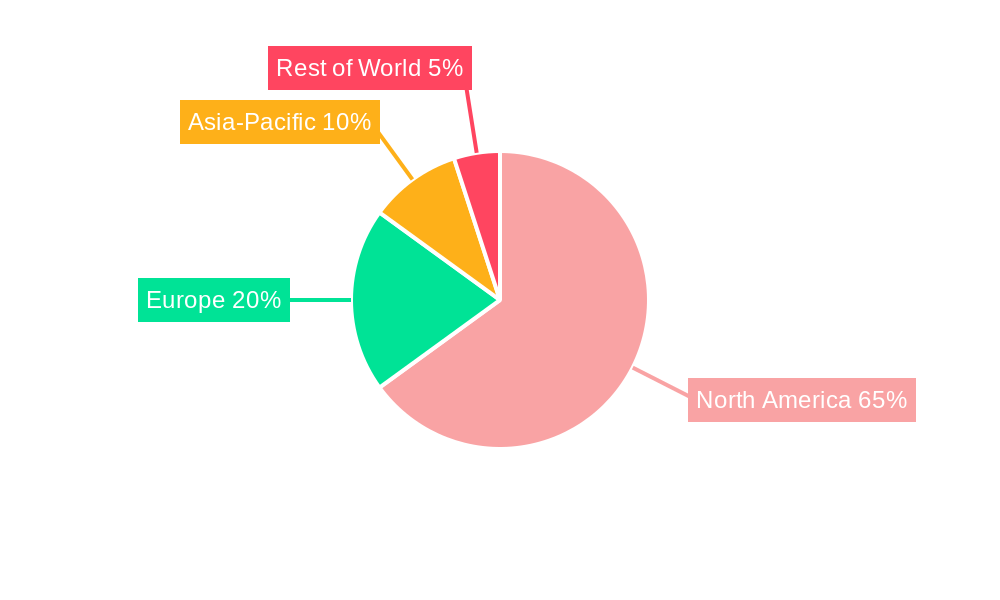

Regional Dominance: The US currently holds the largest market share in North America, driven by its extensive agricultural sector and robust demand for agricultural chemicals. Key factors for this dominance include favorable economic policies, well-developed infrastructure, and a substantial agricultural production base. Canada and Mexico contribute to the overall market but at a lower scale than the US.

North America Agricultural Chemical Packaging Industry Product Developments

Recent product innovations focus on enhancing barrier properties to ensure product safety and extend shelf life, improving recyclability through the use of mono-materials and recyclable designs, and integrating smart packaging features for tracking and traceability. These developments cater to the increasing demand for sustainable, secure, and efficient packaging solutions, creating a competitive advantage for companies that can successfully integrate these features into their product offerings. Technological trends such as lightweighting and the adoption of bio-based materials are significantly impacting product development. These innovations aim to align with market trends prioritizing sustainability and regulatory compliance.

Report Scope & Segmentation Analysis

This report segments the North American agricultural chemical packaging market based on product type (bags and pouches, containers and cans, IBCs, other), material type (plastic, paper and paperboard, metal, other), and application type (fertilizers, pesticides, herbicides, other). Growth projections for each segment are provided, along with insights into market size and competitive dynamics. For instance, the plastic segment is expected to witness significant growth, driven by the cost-effectiveness of plastic materials. However, environmental concerns are pushing the market towards increased adoption of sustainable alternatives. The paper and paperboard segment, though smaller currently, demonstrates the highest projected growth rate. The fertilizer application segment is the largest, with a high demand for robust and reliable packaging solutions. Each segment displays unique competitive dynamics and growth trajectories. All data provided in this report reflects projections for 2025 and beyond.

Key Drivers of North America Agricultural Chemical Packaging Industry Growth

The growth of the North American agricultural chemical packaging industry is driven by several factors: increasing demand for agricultural chemicals due to global population growth and the need for increased food production; stricter regulations regarding product safety and environmental protection, driving the demand for compliant packaging; and technological advancements in packaging materials, offering enhanced functionality and sustainability. The ongoing development of innovative, sustainable packaging solutions significantly contributes to market growth, while economic factors, such as increasing disposable incomes and investments in agricultural infrastructure, further contribute to overall demand.

Challenges in the North America Agricultural Chemical Packaging Industry Sector

Significant challenges include fluctuating raw material prices, impacting production costs; stringent environmental regulations requiring costly compliance measures; and intense competition among established and emerging players, leading to pricing pressures. Supply chain disruptions, particularly those witnessed in recent years, have also presented a challenge, impacting the timely delivery of raw materials and finished products. These factors significantly impact profitability and sustainability within the sector. The estimated impact of these challenges on market growth is estimated at xx% during the study period.

Emerging Opportunities in North America Agricultural Chemical Packaging Industry

Emerging opportunities lie in the development of sustainable and eco-friendly packaging solutions, such as biodegradable and compostable materials; the integration of smart packaging technologies for improved product traceability and supply chain management; and the expansion into niche agricultural markets and emerging regions. The growing demand for customized packaging solutions presents a lucrative opportunity for players who can offer tailor-made products to meet specific requirements.

Leading Players in the North America Agricultural Chemical Packaging Market

- Hoover CS*List Not Exhaustive

- Sonoco Products Company

- LC Packaging International BV

- Greif Inc

- Mondi Group

- Tri Rinse

- ProAmpac LLC

- Mauser Packaging Solutions

- Silgan Holdings

Key Developments in North America Agricultural Chemical Packaging Industry Industry

- April 2022: Greif Inc. announced the divestiture of its Flexible Packaging joint venture (FPS) for USD 123 Million, impacting market share and debt structures.

- April 2022: LC Packaging collaborated with M.B. Nieuwenhuijse B.V. and Plastic Bank to promote ocean cleanup and sustainable material sourcing, demonstrating a commitment to environmental responsibility and innovation in raw material acquisition.

Strategic Outlook for North America Agricultural Chemical Packaging Market

The North American agricultural chemical packaging market presents significant growth potential driven by a combination of factors. Continued demand for agricultural chemicals, a growing emphasis on sustainability, and the adoption of advanced packaging technologies will shape the industry's future. Companies that successfully adapt to evolving consumer preferences, regulatory landscapes, and technological advancements are poised to capture significant market share and contribute to the sector's sustained growth in the coming years. Focus on eco-friendly packaging and supply chain resilience will be pivotal for sustained success.

North America Agricultural Chemical Packaging Industry Segmentation

-

1. Product Type

- 1.1. Bags and Pouches

- 1.2. Containers and Cans

- 1.3. Intermediate Bulk Containers (IBCs)

- 1.4. Other Product Types

-

2. Material Type

- 2.1. Plastic

- 2.2. Paper and Paperboard

- 2.3. Metal

- 2.4. Other Materials

-

3. Application Type

- 3.1. Fertilizers

- 3.2. Pesticides

- 3.3. Herbicides

- 3.4. Other Application Types

North America Agricultural Chemical Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Agricultural Chemical Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging

- 3.3. Market Restrains

- 3.3.1. ; High Inventory Costs and Premium Pricing

- 3.4. Market Trends

- 3.4.1. Fertilizers to Hold Major Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Bags and Pouches

- 5.1.2. Containers and Cans

- 5.1.3. Intermediate Bulk Containers (IBCs)

- 5.1.4. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Material Type

- 5.2.1. Plastic

- 5.2.2. Paper and Paperboard

- 5.2.3. Metal

- 5.2.4. Other Materials

- 5.3. Market Analysis, Insights and Forecast - by Application Type

- 5.3.1. Fertilizers

- 5.3.2. Pesticides

- 5.3.3. Herbicides

- 5.3.4. Other Application Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United States North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Agricultural Chemical Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Hoover CS*List Not Exhaustive

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Sonoco Products Company

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 LC Packaging International BV

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Greif Inc

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Mondi Group

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Tri Rinse

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 ProAmpac LLC

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Mauser Packaging Solutions

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Silgan Holdings

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.1 Hoover CS*List Not Exhaustive

List of Figures

- Figure 1: North America Agricultural Chemical Packaging Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Agricultural Chemical Packaging Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 4: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 5: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 12: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 13: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Application Type 2019 & 2032

- Table 14: North America Agricultural Chemical Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Agricultural Chemical Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Agricultural Chemical Packaging Industry?

The projected CAGR is approximately 3.40%.

2. Which companies are prominent players in the North America Agricultural Chemical Packaging Industry?

Key companies in the market include Hoover CS*List Not Exhaustive, Sonoco Products Company, LC Packaging International BV, Greif Inc, Mondi Group, Tri Rinse, ProAmpac LLC, Mauser Packaging Solutions, Silgan Holdings.

3. What are the main segments of the North America Agricultural Chemical Packaging Industry?

The market segments include Product Type, Material Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.99 Million as of 2022.

5. What are some drivers contributing to market growth?

Material-based Innovations to Enhance Shelf Life of Products and Ongoing Theme of Sustainability in Packaging.

6. What are the notable trends driving market growth?

Fertilizers to Hold Major Market Share.

7. Are there any restraints impacting market growth?

; High Inventory Costs and Premium Pricing.

8. Can you provide examples of recent developments in the market?

April 2022 - Greif Inc. announced the divestiture of the Flexible Packaging joint venture or 'FPS' for USD 123 million. The company will use the sale of FPS to clear the debt payments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Agricultural Chemical Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Agricultural Chemical Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Agricultural Chemical Packaging Industry?

To stay informed about further developments, trends, and reports in the North America Agricultural Chemical Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence