Key Insights

The North American baby food packaging market, valued at approximately $X billion in 2025, is experiencing robust growth, projected to reach $Y billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 7.92%. This expansion is driven by several key factors. The rising preference for convenient and safe baby food products fuels demand for innovative packaging solutions, such as pouches and ready-to-feed bottles, offering improved shelf life and portability. Furthermore, increasing health consciousness among parents is driving the adoption of eco-friendly packaging materials like recyclable paperboard and sustainable plastics, aligning with the growing environmental sustainability concerns. Stringent regulatory frameworks regarding food safety and labeling also influence packaging choices, prompting manufacturers to invest in advanced technologies to ensure product integrity and consumer trust. The market segmentation reveals significant contributions from various material types, with plastic and paperboard dominating, while product types like bottles and pouches show high demand. Leading players like AptarGroup, RPC Group, and Amcor Ltd. are driving innovation and competition, expanding their product portfolios to cater to evolving consumer needs and preferences. The North American market, characterized by high disposable incomes and a significant baby boomer population, serves as a lucrative market for baby food packaging manufacturers.

However, market growth faces certain challenges. Fluctuating raw material prices, particularly for plastics and metals, can impact production costs and profitability. The increasing demand for sustainable packaging solutions requires continuous investment in research and development of eco-friendly alternatives. Furthermore, maintaining a balance between cost-effectiveness and high-quality packaging is crucial for manufacturers to remain competitive. Despite these restraints, the overall market outlook remains positive, driven by continuous innovation, growing demand, and the industry's responsiveness to evolving consumer and regulatory demands. Future growth will likely be shaped by advancements in packaging technology, such as smart packaging with improved traceability and tamper-evidence features, alongside the further adoption of sustainable materials and solutions.

North America Baby Food Packaging Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the North America baby food packaging industry, covering market size, segmentation, trends, competitive landscape, and future outlook. The study period spans 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033, and the historical period encompasses 2019-2024. This report is invaluable for industry stakeholders, investors, and businesses seeking to understand and capitalize on opportunities within this dynamic market.

North America Baby Food Packaging Industry Market Concentration & Innovation

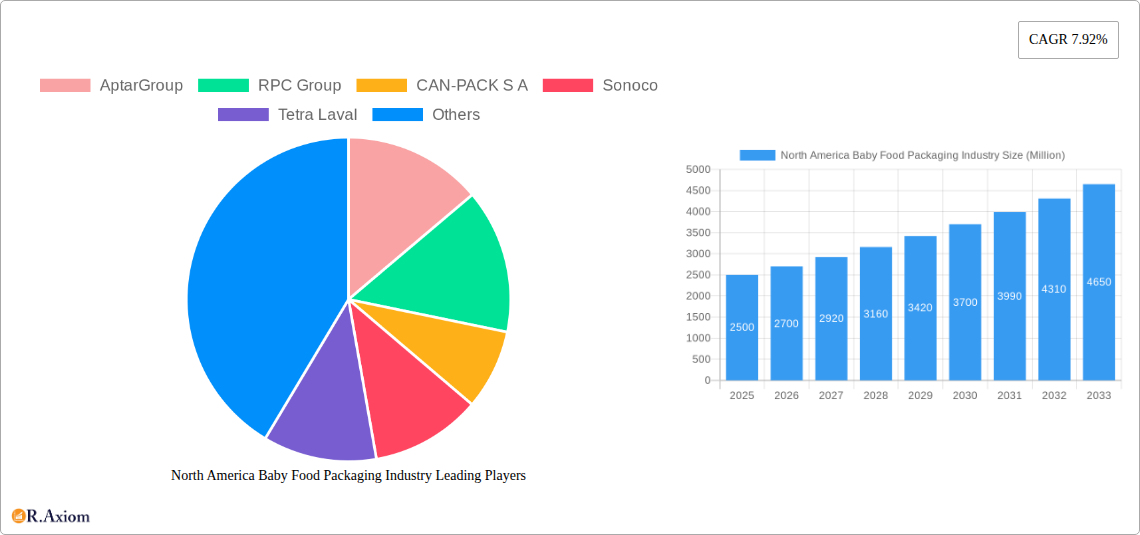

The North America baby food packaging market exhibits moderate concentration, with several key players holding significant market share. The top ten companies, including AptarGroup, RPC Group, CAN-PACK S A, Sonoco, Tetra Laval, Bemis Company Inc, Mondi Group, Winpak Ltd, DS Smith Plc, and Prolamina Packaging (list not exhaustive), Silgan Holdings Inc, Rexam PLC, and Amcor Ltd, collectively account for an estimated xx% of the market in 2025. However, the market also features numerous smaller players, particularly in niche segments. Innovation is driven by increasing consumer demand for sustainable and convenient packaging solutions. This includes the rise of pouches and recyclable materials like paperboard and bioplastics. Regulatory frameworks, such as those related to food safety and environmental sustainability, significantly influence packaging choices. The industry witnesses ongoing M&A activity, with deal values totaling an estimated $xx Million in the past five years. Recent examples include the Hero Group's acquisition of Baby Gourmet in 2021. This consolidation trend reflects companies' strategies to expand their product portfolios and market reach. Product substitutes, such as bulk packaging options, pose a challenge to established players. Furthermore, evolving end-user preferences, including increasing preference for eco-friendly packaging, are reshaping industry dynamics.

- Market Share: Top 10 companies hold approximately xx% of the market (2025).

- M&A Deal Value (2019-2024): Approximately $xx Million.

- Key Innovation Drivers: Sustainability, Convenience, Regulatory Compliance.

North America Baby Food Packaging Industry Industry Trends & Insights

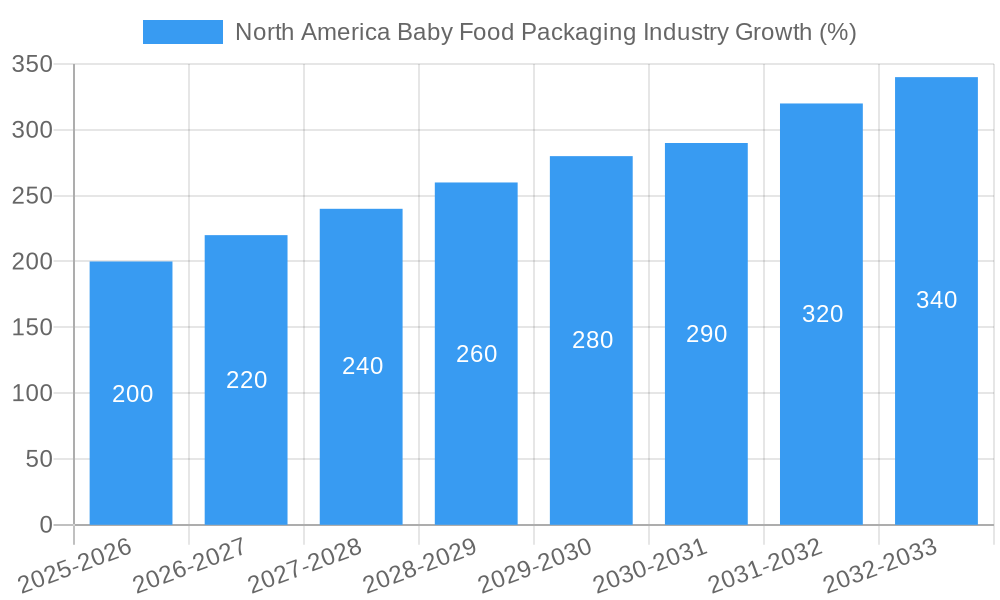

The North America baby food packaging market is experiencing robust growth, driven by factors such as rising disposable incomes, increasing birth rates (albeit fluctuating regionally), and growing awareness of the importance of infant nutrition. The market is projected to achieve a CAGR of xx% during the forecast period (2025-2033), reaching a market value of $xx Million by 2033. Technological disruptions, including the adoption of advanced printing technologies and smart packaging, are transforming the industry. Consumer preferences are shifting toward sustainable and convenient packaging options, with pouches and recyclable materials gaining traction. The competitive dynamics are intense, with companies focusing on product differentiation, innovation, and strategic partnerships to gain a competitive edge. Market penetration of eco-friendly packaging is growing steadily, but traditional materials like plastic remain dominant due to their cost-effectiveness and functionality.

Dominant Markets & Segments in North America Baby Food Packaging Industry

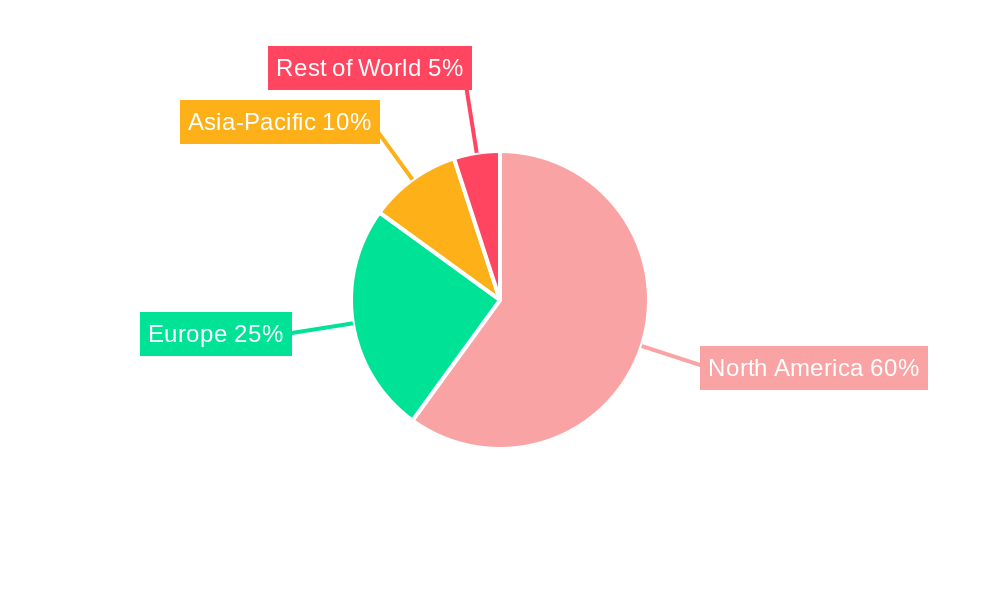

The United States remains the dominant market in North America, accounting for approximately xx% of the total market value in 2025. This dominance is attributable to factors including:

- Large consumer base: High birth rates and strong consumer spending power.

- Established supply chain: Well-developed infrastructure supporting packaging manufacturing and distribution.

- Favorable regulatory environment: Supportive policies for the food and beverage industry.

Dominant Segments:

- Primary Material: Plastic currently holds the largest market share due to its cost-effectiveness and versatility. However, paperboard is witnessing significant growth driven by its eco-friendly profile.

- Product Type: Pouches are experiencing rapid adoption due to their convenience and suitability for various baby food products. Bottles and jars remain dominant segments due to their established presence and consumer preference.

- Food Products: Prepared baby food dominates, followed by liquid and powdered milk formula.

North America Baby Food Packaging Industry Product Developments

Recent product innovations focus on enhancing convenience, sustainability, and food safety. This includes the introduction of retort pouches for extended shelf life, recyclable and compostable packaging materials, and innovative closures that improve product preservation. Companies are leveraging advanced printing techniques for eye-catching designs and clear labeling. These developments aim to appeal to health-conscious parents and meet stringent regulatory requirements. The market fit is strong for sustainable and convenient options, creating a positive outlook for innovation in this sector.

Report Scope & Segmentation Analysis

This report segments the North America baby food packaging market based on primary material (Plastic, Paperboard, Metal, Glass, Others), product type (Bottles, Metal Cans, Cartons, Jars, Pouches, Others), and food products (Liquid Milk Formula, Dried Baby Food, Powder Milk Formula, Prepared Baby Food, Other). Each segment is analyzed in detail, providing growth projections, market size estimates for 2025 and beyond, and a competitive landscape analysis. For instance, the plastic segment is projected to grow at xx% CAGR, while the pouch segment is expected to see faster growth due to its convenience and sustainability features. The competitive landscape varies across segments; some are dominated by a few large players while others exhibit greater fragmentation.

Key Drivers of North America Baby Food Packaging Growth

The growth of the North America baby food packaging industry is fueled by several key factors:

- Rising birth rates: Although fluctuating, birth rates remain a significant driver of demand for baby food and related packaging.

- Increased disposable incomes: Growing purchasing power enables parents to afford higher-quality and more convenient baby food options.

- Shifting consumer preferences: Demand for sustainable and convenient packaging is driving innovation in the industry.

Challenges in the North America Baby Food Packaging Industry Sector

The industry faces several challenges, including:

- Fluctuations in raw material prices: This impacts the cost of production and profitability.

- Stringent regulatory requirements: Compliance with food safety and environmental regulations poses significant challenges.

- Competition: Intense competition among established players and new entrants. This pressure on pricing and requires constant innovation to maintain market share.

Emerging Opportunities in North America Baby Food Packaging Industry

Emerging opportunities include:

- Growth in organic and specialized baby food: This fuels demand for packaging solutions that maintain product integrity and quality.

- Increasing adoption of sustainable packaging: Opportunities abound in developing and adopting bioplastics, recycled content, and compostable materials.

- Expansion into e-commerce: Growing online sales channels create demand for convenient packaging suitable for shipping and delivery.

Leading Players in the North America Baby Food Packaging Industry Market

- AptarGroup

- RPC Group

- CAN-PACK S A

- Sonoco

- Tetra Laval

- Bemis Company Inc

- Mondi Group

- Winpak Ltd

- DS Smith Plc

- Prolamina Packaging

- Silgan Holdings Inc

- Rexam PLC

- Amcor Ltd

Key Developments in North America Baby Food Packaging Industry

- January 2021: The Hero Group acquired Baby Gourmet, expanding its presence in the organic baby food market.

- June 2021: Nestlé's Gerber partnered with TerraCycle to launch a recycling program for baby food packaging in Canada, addressing sustainability concerns.

Strategic Outlook for North America Baby Food Packaging Industry Market

The North America baby food packaging market is poised for continued growth, driven by rising consumer demand for convenient, sustainable, and safe packaging solutions. Companies that prioritize innovation, sustainability, and efficient supply chain management are well-positioned to succeed. The focus on eco-friendly packaging materials, innovative designs, and enhanced food safety features will shape the industry's future trajectory. The market offers significant opportunities for both established players and new entrants to capitalize on evolving consumer preferences and technological advancements.

North America Baby Food Packaging Industry Segmentation

-

1. Primary Material

- 1.1. Plastic

- 1.2. Paperboard

- 1.3. Metal

- 1.4. Glass

- 1.5. Others

-

2. Product type

- 2.1. Bottles

- 2.2. Metal Cans

- 2.3. Cartons

- 2.4. Jars

- 2.5. Pouches

- 2.6. Others

-

3. Food Products

- 3.1. Liquid Milk Formula

- 3.2. Dried Baby Food

- 3.3. Powder Milk Formula

- 3.4. Prepared Baby Food

- 3.5. Other

North America Baby Food Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Baby Food Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.92% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand of Packaged Baby Food and Infant Formula; Increasing Working Women in Urban Areas residing Population

- 3.3. Market Restrains

- 3.3.1. Stringent Government Regulations over Single-Use Plastic-based Packaging

- 3.4. Market Trends

- 3.4.1. Plastic is Expected to Hold the Largest Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Baby Food Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Primary Material

- 5.1.1. Plastic

- 5.1.2. Paperboard

- 5.1.3. Metal

- 5.1.4. Glass

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Product type

- 5.2.1. Bottles

- 5.2.2. Metal Cans

- 5.2.3. Cartons

- 5.2.4. Jars

- 5.2.5. Pouches

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Food Products

- 5.3.1. Liquid Milk Formula

- 5.3.2. Dried Baby Food

- 5.3.3. Powder Milk Formula

- 5.3.4. Prepared Baby Food

- 5.3.5. Other

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Primary Material

- 6. United States North America Baby Food Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Baby Food Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Baby Food Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Baby Food Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 AptarGroup

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 RPC Group

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 CAN-PACK S A

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Sonoco

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Tetra Laval

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Bemis Company Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Mondi Group

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Winpak Ltd

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 DS Smith Plc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Prolamina Packaging*List Not Exhaustive

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Silgan Holdings Inc

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Rexam PLC

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 Amcor Ltd

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.1 AptarGroup

List of Figures

- Figure 1: North America Baby Food Packaging Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Baby Food Packaging Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Baby Food Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Baby Food Packaging Industry Revenue Million Forecast, by Primary Material 2019 & 2032

- Table 3: North America Baby Food Packaging Industry Revenue Million Forecast, by Product type 2019 & 2032

- Table 4: North America Baby Food Packaging Industry Revenue Million Forecast, by Food Products 2019 & 2032

- Table 5: North America Baby Food Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Baby Food Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Baby Food Packaging Industry Revenue Million Forecast, by Primary Material 2019 & 2032

- Table 12: North America Baby Food Packaging Industry Revenue Million Forecast, by Product type 2019 & 2032

- Table 13: North America Baby Food Packaging Industry Revenue Million Forecast, by Food Products 2019 & 2032

- Table 14: North America Baby Food Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Baby Food Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Baby Food Packaging Industry?

The projected CAGR is approximately 7.92%.

2. Which companies are prominent players in the North America Baby Food Packaging Industry?

Key companies in the market include AptarGroup, RPC Group, CAN-PACK S A, Sonoco, Tetra Laval, Bemis Company Inc, Mondi Group, Winpak Ltd, DS Smith Plc, Prolamina Packaging*List Not Exhaustive, Silgan Holdings Inc, Rexam PLC, Amcor Ltd.

3. What are the main segments of the North America Baby Food Packaging Industry?

The market segments include Primary Material, Product type, Food Products.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand of Packaged Baby Food and Infant Formula; Increasing Working Women in Urban Areas residing Population.

6. What are the notable trends driving market growth?

Plastic is Expected to Hold the Largest Market Share.

7. Are there any restraints impacting market growth?

Stringent Government Regulations over Single-Use Plastic-based Packaging.

8. Can you provide examples of recent developments in the market?

January 2021 - The Hero Group has acquired Baby Gourmet, a Canadian organic meal and snack brand for babies and toddlers. The acquisition includes Slammers Snacks, a Baby Gourmet-owned organic US children's snack brand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Baby Food Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Baby Food Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Baby Food Packaging Industry?

To stay informed about further developments, trends, and reports in the North America Baby Food Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence