Key Insights

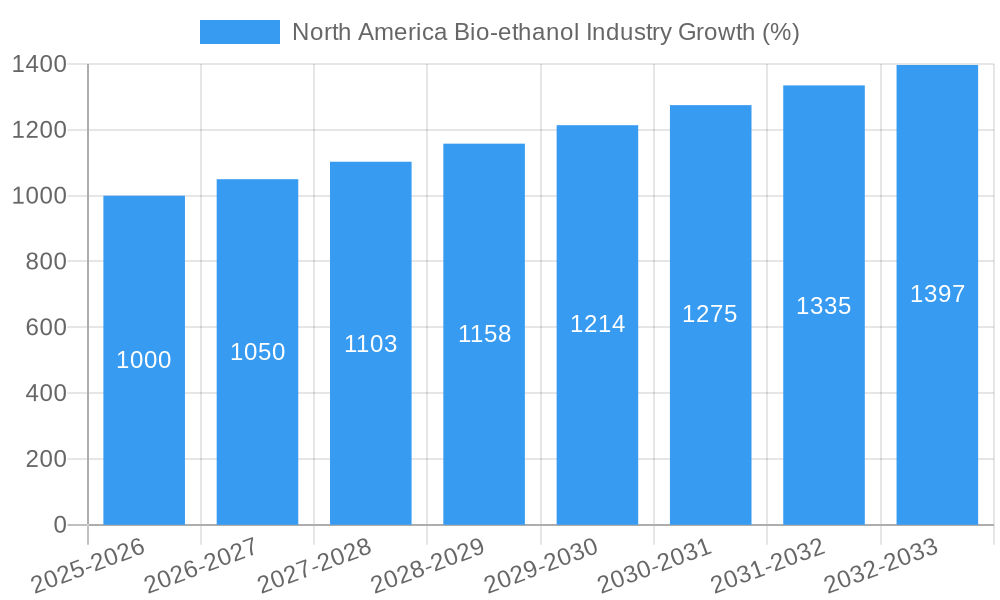

The North American bioethanol industry, currently valued at approximately $XX million (assuming a reasonable value based on global market size and North America's share), is projected to experience robust growth, exceeding a 5% Compound Annual Growth Rate (CAGR) from 2025 to 2033. This expansion is driven by several key factors. Firstly, increasing government regulations aimed at reducing greenhouse gas emissions and promoting renewable energy sources are incentivizing bioethanol production and adoption. Secondly, the burgeoning automotive and transportation sector, with its increasing demand for cleaner fuels, acts as a significant driver. The food and beverage industry's ongoing demand for bioethanol as a solvent and ingredient also contributes to market growth. Furthermore, expanding applications in pharmaceuticals and cosmetics further diversify the market. While feedstock availability and price fluctuations pose challenges, technological advancements in efficient ethanol production from diverse feedstocks like sugarcane, corn, and wheat are mitigating these restraints. The competitive landscape features a mix of established players like ADM and Valero, alongside emerging companies, signifying a dynamic and innovative sector. Regional variations exist, with the United States likely dominating the North American market due to its established infrastructure and government support. Canada and Mexico, while smaller contributors, are expected to show growth aligned with regional sustainability initiatives.

The forecast period (2025-2033) anticipates consistent growth for the North American bioethanol market, propelled by continued advancements in biofuel technology, growing consumer awareness of environmental sustainability, and the ongoing need for renewable fuel options. Strategic partnerships between established companies and technology developers are expected to further boost production efficiency and expand the market reach. However, future growth will hinge upon addressing challenges such as fluctuating feedstock prices, the need for improved infrastructure to handle increased production and distribution, and ensuring the sustainability and environmental friendliness of the entire production process. Diversification of feedstocks beyond corn, through the exploration of cellulosic biomass, will likely play a critical role in securing the long-term viability and sustainability of the North American bioethanol industry.

This in-depth report provides a comprehensive analysis of the North America bio-ethanol industry, covering market trends, competitive landscape, and future growth prospects from 2019 to 2033. The study period spans 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033 and the historical period is 2019-2024. This report is essential for industry stakeholders, investors, and businesses seeking to understand and capitalize on opportunities within this dynamic sector.

North America Bio-ethanol Industry Market Concentration & Innovation

The North American bio-ethanol market exhibits a moderately concentrated structure, with key players such as ADM, Green Plains Inc, and Valero holding significant market share. However, the presence of numerous smaller players and emerging companies fosters a competitive environment. Innovation is driven by factors such as stringent environmental regulations promoting sustainable fuels, advancements in feedstock technology (including cellulosic ethanol), and the increasing demand for renewable energy sources. Mergers and acquisitions (M&A) activity has played a significant role in shaping the market landscape. For instance, ADM's sale of its Peoria ethanol plant in October 2021, valued at xx Million, exemplifies the strategic shifts within the industry. The average M&A deal value in the period 2019-2024 was approximately xx Million, indicating considerable investment and consolidation.

- Market Concentration: High concentration in the top 5 players, holding approximately xx% of the market share.

- Innovation Drivers: Stringent environmental regulations, technological advancements (cellulosic ethanol), and rising renewable energy demand.

- Regulatory Frameworks: Government subsidies and mandates significantly impact market dynamics.

- Product Substitutes: Competition from other biofuels and fossil fuels influences market share.

- End-User Trends: Increasing demand from the automotive and transportation sector drives market growth.

- M&A Activity: Significant consolidation through mergers and acquisitions, impacting market share and competitiveness.

North America Bio-ethanol Industry Industry Trends & Insights

The North American bio-ethanol industry is experiencing robust growth, fueled by government policies supporting renewable fuels, increasing environmental concerns, and the expanding transportation sector. The Compound Annual Growth Rate (CAGR) during the historical period (2019-2024) was approximately xx%, with the market size reaching xx Million in 2024. Technological advancements, particularly in cellulosic ethanol production, are transforming the industry, allowing for a more efficient and sustainable production process. Consumer preferences are shifting towards eco-friendly products, which further boosts the demand for bio-ethanol. However, competitive pressures from other renewable fuels and fluctuating feedstock prices remain challenges. Market penetration of bio-ethanol in the automotive fuel market is steadily increasing, projected to reach xx% by 2033. The industry is also witnessing significant investment in research and development, focusing on improving yield, reducing costs, and expanding applications beyond transportation.

Dominant Markets & Segments in North America Bio-ethanol Industry

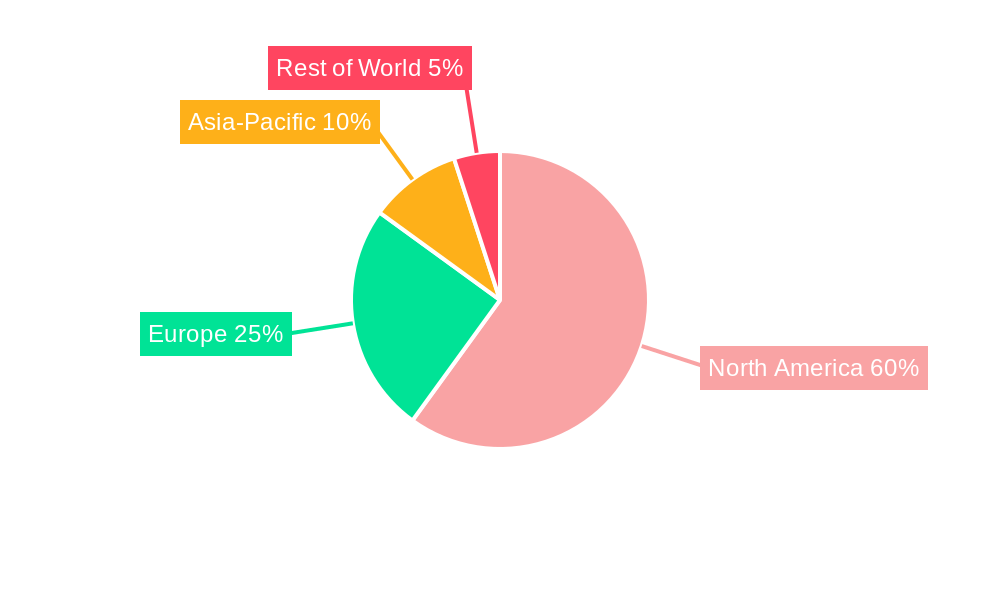

The United States dominates the North American bio-ethanol market, owing to its vast corn production and established infrastructure. Corn remains the predominant feedstock, accounting for approximately xx% of the market.

Dominant Feedstock Type:

- Corn: Largest market share due to readily available resources and established infrastructure. Key drivers include government support programs and economies of scale.

- Sugarcane: Significant presence in specific regions (e.g., parts of the US), with growth prospects tied to expansion of cultivation and policy changes.

- Wheat: Smaller market share compared to corn; its usage depends on price competitiveness and regional availability.

- Other Feedstocks: Emerging feedstocks, such as cellulosic biomass, are gaining traction, driven by sustainability concerns and technological advancements.

Dominant Application:

- Automotive and Transportation: This is the largest application segment, driven by government mandates and environmental regulations.

- Food and Beverage: Bio-ethanol finds applications in food and beverage production as a solvent and processing aid.

- Pharmaceutical, Cosmetics and Personal Care: Smaller but growing niche applications, offering opportunities for specialized bio-ethanol products.

- Other Applications: Includes diverse applications like industrial solvents and cleaning agents.

North America Bio-ethanol Industry Product Developments

Recent product innovations include advancements in cellulosic ethanol production, enabling the utilization of non-food sources for biofuel production. This aligns with the growing demand for sustainable and environmentally friendly fuels, providing a competitive advantage for companies investing in this technology. Furthermore, the development of bio-ethanol with enhanced properties, such as improved blending characteristics or reduced emissions, is attracting significant attention. These innovations are shaping the market by creating new applications and improving market fit.

Report Scope & Segmentation Analysis

This report segments the North American bio-ethanol market by feedstock type (corn, sugarcane, wheat, other feedstocks) and application (automotive and transportation, food and beverage, pharmaceutical, cosmetics and personal care, other applications). Each segment’s market size, growth projections, and competitive dynamics are analyzed. For example, the corn-based ethanol segment is expected to maintain a dominant market share due to its established infrastructure and economies of scale. However, the "other feedstocks" segment exhibits the highest projected growth rate, driven by technological innovations in cellulosic ethanol.

Key Drivers of North America Bio-ethanol Industry Growth

The growth of the North American bio-ethanol industry is primarily driven by:

- Government Policies: Subsidies, tax incentives, and renewable fuel standards (RFS) incentivize bio-ethanol production and consumption.

- Environmental Concerns: Growing awareness of climate change and the need to reduce greenhouse gas emissions fuels demand for renewable fuels.

- Technological Advancements: Innovations in feedstock utilization and production efficiency increase the competitiveness of bio-ethanol.

- Transportation Sector Demand: The expanding automotive sector, coupled with stringent emission regulations, significantly boosts bio-ethanol demand.

Challenges in the North America Bio-ethanol Industry Sector

The industry faces challenges such as:

- Feedstock Price Volatility: Fluctuations in the prices of corn and other feedstocks impact production costs and profitability.

- Competition from other Biofuels: Competition from other renewable fuels, such as biodiesel, limits market share growth.

- Land Use Concerns: Concerns about land use change and deforestation associated with biofuel production present a challenge.

- Infrastructure Limitations: In some regions, inadequate infrastructure for bio-ethanol distribution and storage remains a hurdle.

Emerging Opportunities in North America Bio-ethanol Industry

Emerging opportunities include:

- Cellulosic Ethanol: Technological advancements are making cellulosic ethanol production increasingly viable and cost-effective.

- Bio-based Products: Expanding applications of bio-ethanol in various industries beyond fuel, such as chemicals and plastics.

- Carbon Capture and Storage: Integration of carbon capture and storage technologies to further reduce greenhouse gas emissions from bio-ethanol production.

- Advanced Biofuels: Research and development into next-generation biofuels with improved sustainability and energy density.

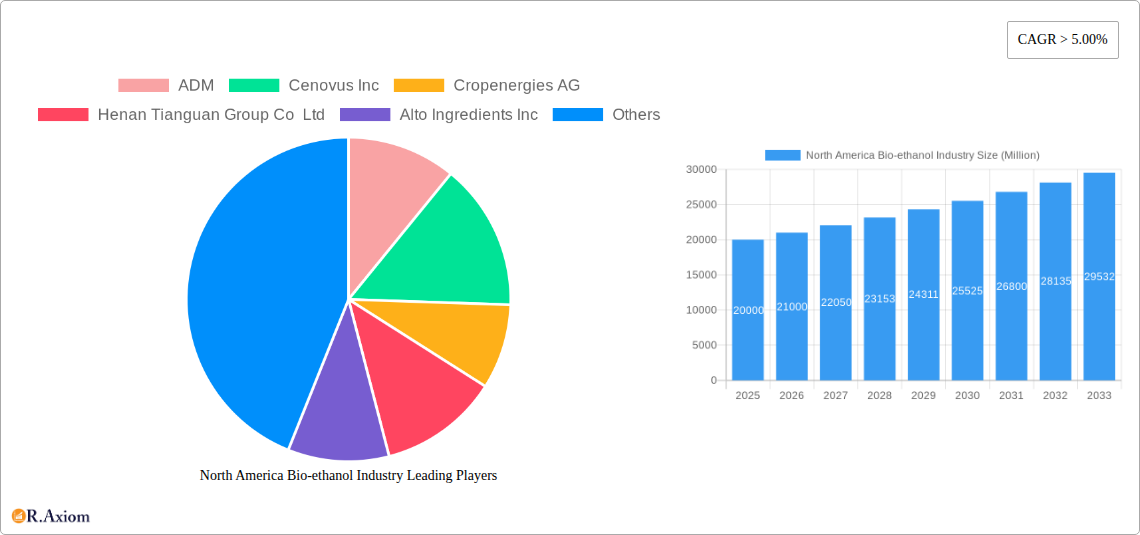

Leading Players in the North America Bio-ethanol Industry Market

- ADM

- Cenovus Inc

- Cropenergies AG

- Henan Tianguan Group Co Ltd

- Alto Ingredients Inc

- Green Plains Inc

- Suncor Energy Inc

- Valero

- Ethanol Technologies

- Verbio Vereinigte Bioenergie AG

- Abengoa

- Granbio Investimentos SA

- Sekab

- Blue Bio Fuels Inc

- Lantmannen

- Cristalco

- Poet LLC

- Jilin Fuel Ethanol Co Ltd

- Raizen

- KWST

Key Developments in North America Bio-ethanol Industry Industry

- May 2022: VERBIO AG opened the first cellulosic RNG plant in the U.S., achieving full-scale production of 7 Million EGE of RNG annually. This project is expected to produce 60 Million gallons of corn-based ethanol annually starting in 2023, marking a significant step towards sustainable biofuel production.

- October 2021: ADM sold its ethanol manufacturing plant in Peoria, Illinois, to BioUrja Group, reflecting strategic adjustments within the industry.

Strategic Outlook for North America Bio-ethanol Industry Market

The North American bio-ethanol market is poised for continued growth, driven by supportive government policies, increasing environmental awareness, and technological advancements. The focus on sustainable and efficient production methods, coupled with diversification into new applications, will shape the future market landscape. Investments in cellulosic ethanol and advanced biofuels will be key to achieving further growth and reducing reliance on fossil fuels. The market's future success hinges on addressing challenges related to feedstock price volatility, competition, and environmental sustainability.

North America Bio-ethanol Industry Segmentation

-

1. Feedstock Type

- 1.1. Sugarcane

- 1.2. Corn

- 1.3. Wheat

- 1.4. Other Feedstocks

-

2. Application

- 2.1. Automotive and Transportation

- 2.2. Food and Beverage

- 2.3. Pharmaceutical

- 2.4. Cosmetics and Personal Care

- 2.5. Other Applications

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Bio-ethanol Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Bio-ethanol Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Favorable Initiatives and Blending Mandates by Regulatory Bodies; Rising Environmental Concerns by the Use of Fossil Fuels and Need for the Bio-fuels

- 3.3. Market Restrains

- 3.3.1. Phasing out of Fuel-based Vehicles Due to Rising Demand for Electric Vehicles; Shifting Focus to Bio-butanol

- 3.4. Market Trends

- 3.4.1. Automotive and Transportation Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 5.1.1. Sugarcane

- 5.1.2. Corn

- 5.1.3. Wheat

- 5.1.4. Other Feedstocks

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Automotive and Transportation

- 5.2.2. Food and Beverage

- 5.2.3. Pharmaceutical

- 5.2.4. Cosmetics and Personal Care

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 6. United States North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 6.1.1. Sugarcane

- 6.1.2. Corn

- 6.1.3. Wheat

- 6.1.4. Other Feedstocks

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Automotive and Transportation

- 6.2.2. Food and Beverage

- 6.2.3. Pharmaceutical

- 6.2.4. Cosmetics and Personal Care

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 7. Canada North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 7.1.1. Sugarcane

- 7.1.2. Corn

- 7.1.3. Wheat

- 7.1.4. Other Feedstocks

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Automotive and Transportation

- 7.2.2. Food and Beverage

- 7.2.3. Pharmaceutical

- 7.2.4. Cosmetics and Personal Care

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 8. Mexico North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 8.1.1. Sugarcane

- 8.1.2. Corn

- 8.1.3. Wheat

- 8.1.4. Other Feedstocks

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Automotive and Transportation

- 8.2.2. Food and Beverage

- 8.2.3. Pharmaceutical

- 8.2.4. Cosmetics and Personal Care

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 9. United States North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 ADM

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Cenovus Inc

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Cropenergies AG

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Henan Tianguan Group Co Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Alto Ingredients Inc

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Green Plains Inc

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Suncor Energy Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Valero

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Ethanol Technologies

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Verbio Vereinigte Bioenergie AG*List Not Exhaustive

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Abengoa

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Granbio Investimentos SA

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 Sekab

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 Blue Bio Fuels Inc

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 Lantmannen

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.16 Cristalco

- 13.2.16.1. Overview

- 13.2.16.2. Products

- 13.2.16.3. SWOT Analysis

- 13.2.16.4. Recent Developments

- 13.2.16.5. Financials (Based on Availability)

- 13.2.17 Poet LLC

- 13.2.17.1. Overview

- 13.2.17.2. Products

- 13.2.17.3. SWOT Analysis

- 13.2.17.4. Recent Developments

- 13.2.17.5. Financials (Based on Availability)

- 13.2.18 Jilin Fuel Ethanol Co Ltd

- 13.2.18.1. Overview

- 13.2.18.2. Products

- 13.2.18.3. SWOT Analysis

- 13.2.18.4. Recent Developments

- 13.2.18.5. Financials (Based on Availability)

- 13.2.19 Raizen

- 13.2.19.1. Overview

- 13.2.19.2. Products

- 13.2.19.3. SWOT Analysis

- 13.2.19.4. Recent Developments

- 13.2.19.5. Financials (Based on Availability)

- 13.2.20 KWST

- 13.2.20.1. Overview

- 13.2.20.2. Products

- 13.2.20.3. SWOT Analysis

- 13.2.20.4. Recent Developments

- 13.2.20.5. Financials (Based on Availability)

- 13.2.1 ADM

List of Figures

- Figure 1: North America Bio-ethanol Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Bio-ethanol Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Bio-ethanol Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 3: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Bio-ethanol Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 12: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 13: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 16: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 20: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 21: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 22: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Bio-ethanol Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the North America Bio-ethanol Industry?

Key companies in the market include ADM, Cenovus Inc, Cropenergies AG, Henan Tianguan Group Co Ltd, Alto Ingredients Inc, Green Plains Inc, Suncor Energy Inc, Valero, Ethanol Technologies, Verbio Vereinigte Bioenergie AG*List Not Exhaustive, Abengoa, Granbio Investimentos SA, Sekab, Blue Bio Fuels Inc, Lantmannen, Cristalco, Poet LLC, Jilin Fuel Ethanol Co Ltd, Raizen, KWST.

3. What are the main segments of the North America Bio-ethanol Industry?

The market segments include Feedstock Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Favorable Initiatives and Blending Mandates by Regulatory Bodies; Rising Environmental Concerns by the Use of Fossil Fuels and Need for the Bio-fuels.

6. What are the notable trends driving market growth?

Automotive and Transportation Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Phasing out of Fuel-based Vehicles Due to Rising Demand for Electric Vehicles; Shifting Focus to Bio-butanol.

8. Can you provide examples of recent developments in the market?

May 2022: VERBIO AG opened the first cellulosic RNG plant in the United States, achieving full-scale production of 7 million ethanol gallons equivalent (EGE) of RNG annually by mid-summer 2022. In 2023, this project is expected to start functioning as a biorefinery, producing 60 million gallons of corn-based ethanol annually.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Bio-ethanol Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Bio-ethanol Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Bio-ethanol Industry?

To stay informed about further developments, trends, and reports in the North America Bio-ethanol Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence