Key Insights

The North American satellite manufacturing market is experiencing robust growth, driven by increasing demand for satellite-based services across various sectors. The market, valued at approximately $XX million in 2025 (assuming a logical estimation based on the provided CAGR of 4.96% and the unspecified market size), is projected to expand significantly over the forecast period (2025-2033). Key growth drivers include the burgeoning need for advanced communication technologies, enhanced earth observation capabilities for environmental monitoring and resource management, and the expanding military and government applications for surveillance and reconnaissance. The rising adoption of miniaturized satellites (below 100kg), coupled with advancements in propulsion technologies like electric propulsion, is further fueling market expansion. Specific segments like LEO (Low Earth Orbit) satellites for communication and Earth observation are showing particularly strong growth, attracting substantial investment from both established players like Lockheed Martin and Maxar Technologies, and innovative startups like Swarm Technologies and Planet Labs. While potential restraints such as high manufacturing costs and regulatory complexities exist, the overall market outlook remains optimistic, fueled by technological advancements, supportive government policies, and the increasing reliance on space-based infrastructure.

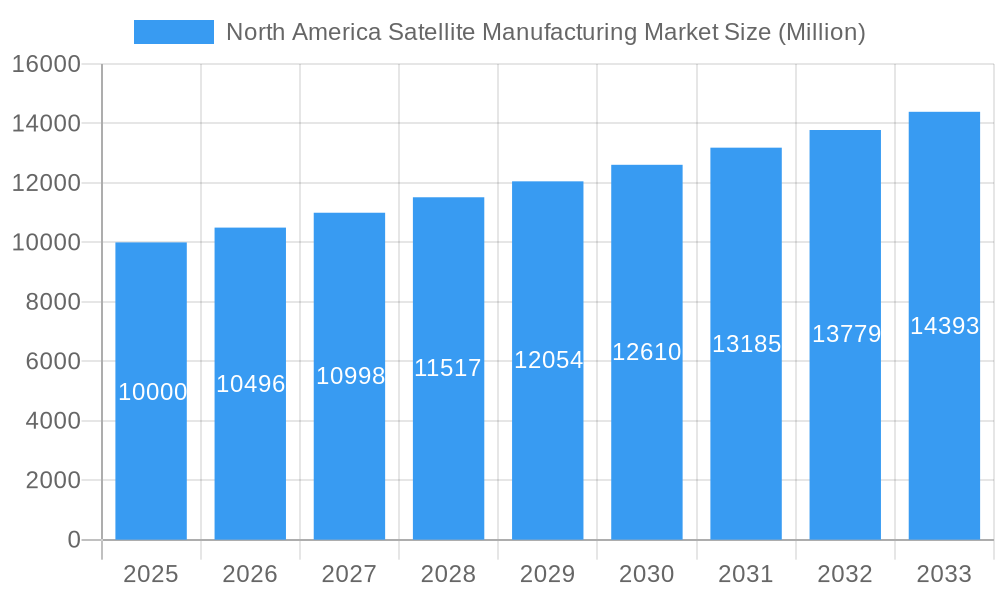

North America Satellite Manufacturing Market Market Size (In Billion)

The segmentation within the North American market reveals significant opportunities. The commercial sector dominates, fueled by the expansion of private satellite constellations for broadband internet access and other services. However, the military and government segments are also exhibiting strong growth, driven by national security and defense initiatives. In terms of satellite subsystems, propulsion hardware and propellant, satellite bus & subsystems, and solar array & power hardware are experiencing the most significant demand. The United States remains the dominant market within North America, accounting for the largest share of revenue, due to its mature space industry and extensive R&D investments. However, Canada's growing space sector also presents a promising sub-market. The forecast period, therefore, anticipates a continued surge in satellite manufacturing activity in North America, propelled by diverse technological advancements and a widening array of applications across various industries.

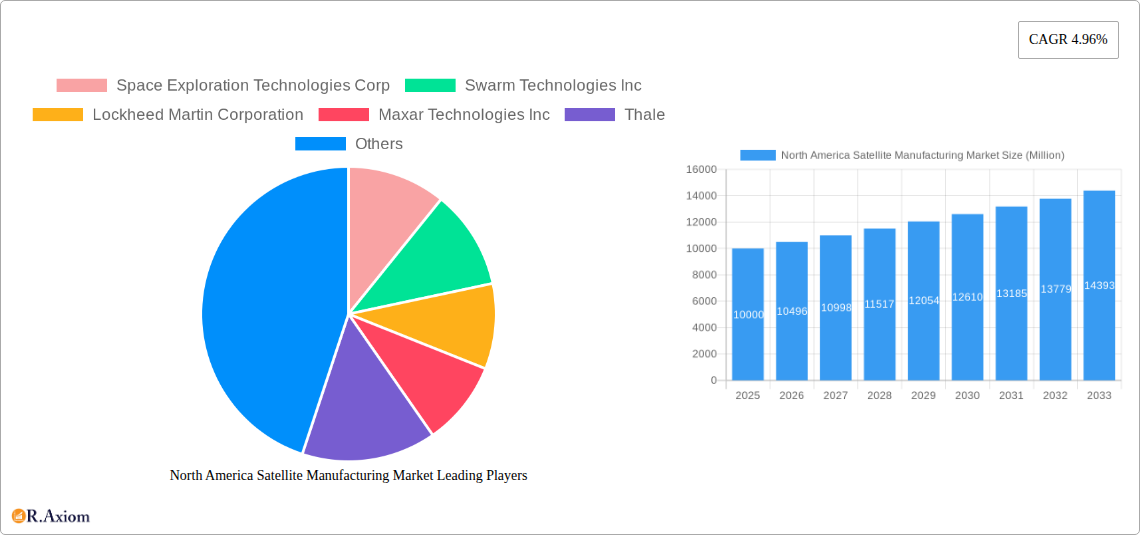

North America Satellite Manufacturing Market Company Market Share

This detailed report provides a comprehensive analysis of the North America satellite manufacturing market, covering the period 2019-2033. It offers actionable insights for industry stakeholders, investors, and businesses involved in this dynamic sector. The report incorporates detailed segmentation, competitive landscape analysis, and future growth projections, leveraging extensive data and market intelligence. The base year for this report is 2025, with estimations for 2025 and a forecast period spanning 2025-2033. The historical period covered is 2019-2024. The market is valued in Millions.

North America Satellite Manufacturing Market Market Concentration & Innovation

The North American satellite manufacturing market exhibits a moderately concentrated landscape, dominated by a few major players like SpaceX, Lockheed Martin, and Maxar Technologies, who collectively hold approximately xx% of the market share in 2025. However, the emergence of numerous smaller companies specializing in niche segments, particularly in nanosatellite technology, is increasing competition and fostering innovation. The market is driven by continuous technological advancements, including miniaturization, improved propulsion systems, and advanced sensor technologies. Regulatory frameworks, such as those set by the Federal Communications Commission (FCC) in the United States, play a significant role in shaping market dynamics. Product substitutes, such as terrestrial communication networks and alternative data acquisition methods, pose a certain level of competitive pressure. End-user trends, particularly the growing demand for high-resolution Earth observation data from both commercial and government sectors, are key market drivers. Mergers and acquisitions (M&A) activity has been significant, with deal values exceeding xx Million in the last five years. Notable M&A activities include:

- [Example M&A deal 1, with value if available]

- [Example M&A deal 2, with value if available]

The innovative landscape is shaped by intense R&D efforts focused on:

- Improving satellite lifespan and reliability.

- Developing cost-effective manufacturing processes for smaller satellites.

- Enhancing data processing and analytics capabilities.

North America Satellite Manufacturing Market Industry Trends & Insights

The North American satellite manufacturing market is experiencing robust growth, with a projected CAGR of xx% during the forecast period (2025-2033). This growth is propelled by several key factors: increasing demand for satellite-based communication services, growing adoption of satellite imagery for various applications (Earth observation, environmental monitoring, precision agriculture), and the expansion of government-led space exploration initiatives. Technological disruptions, such as the rise of constellations of small satellites and advancements in electric propulsion systems, are reshaping the industry landscape. Consumer preferences are shifting towards more affordable, readily available, and higher-resolution data services, influencing market demand. Competitive dynamics are characterized by a mix of established players and new entrants, leading to continuous innovation and price competition. Market penetration of smallsat constellations is increasing rapidly, driven by cost-effectiveness and faster deployment capabilities. The commercial sector dominates the end-user segment, accounting for approximately xx% of the market in 2025, followed by the military & government sector.

Dominant Markets & Segments in North America Satellite Manufacturing Market

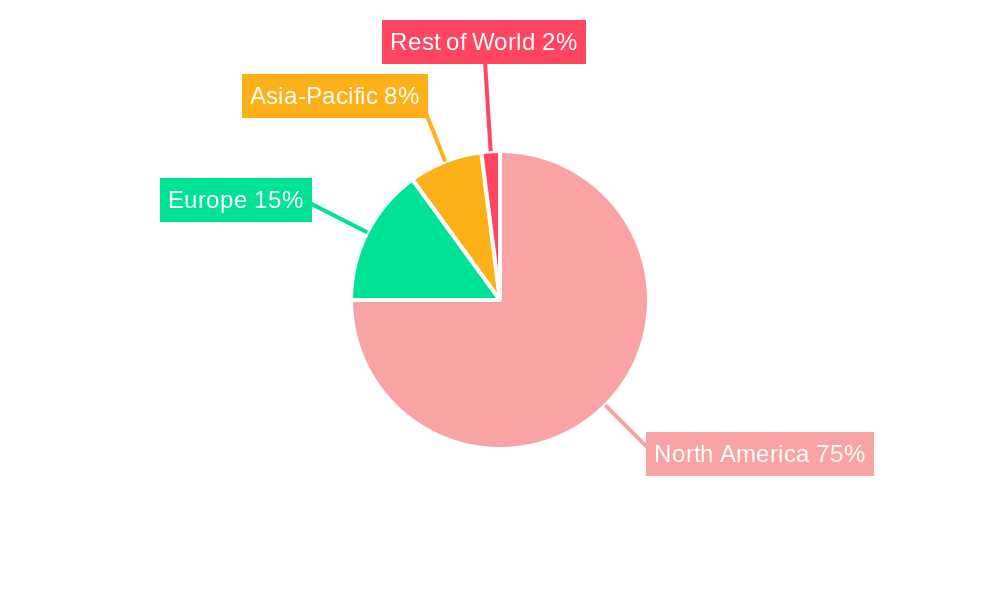

The United States constitutes the dominant market within North America, accounting for approximately xx% of the total market revenue in 2025. This dominance stems from a robust aerospace industry, a strong presence of major satellite manufacturers, and substantial government funding for space-related programs. Canada contributes significantly to the market, specializing in certain satellite sub-systems and components.

Key Drivers for US Dominance:

- Strong government support for aerospace research and development.

- Presence of established satellite manufacturers with extensive experience.

- Well-developed infrastructure for satellite launch and operations.

- High demand for satellite-based services across various sectors.

Segment Dominance:

- Orbit Class: LEO (Low Earth Orbit) satellites dominate due to their advantages in data acquisition and cost-effectiveness.

- End User: The commercial sector is the largest end-user segment, driven by increasing demand for satellite imagery, communication services, and navigation data.

- Satellite Subsystem: Satellite Bus & Subsystems is the largest segment due to their integral role in satellite functionality.

- Propulsion Tech: Electric propulsion is gaining traction due to its efficiency and extended lifespan compared to traditional gas-based systems.

- Application: Earth Observation applications dominate, driven by high demand for satellite imagery across various commercial and government applications.

- Satellite Mass: The 10-100kg segment is rapidly growing, mainly due to the rising popularity of CubeSats and nanosatellites.

North America Satellite Manufacturing Market Product Developments

Recent years have witnessed significant advancements in satellite technology, including the development of smaller, more cost-effective satellites, improved propulsion systems, and more sophisticated sensor technologies. This has enabled the emergence of megaconstellations, offering ubiquitous global coverage for communication and Earth observation applications. These innovations cater to increasing demand for higher-resolution imagery, faster data transmission, and more affordable access to satellite data. Miniaturization and increased automation in manufacturing processes are also key trends enhancing competitiveness.

Report Scope & Segmentation Analysis

This report comprehensively segments the North America satellite manufacturing market based on:

Orbit Class: LEO, MEO, GEO, Elliptical. Each orbit class exhibits unique characteristics impacting its market size and growth projections. LEO is projected to dominate due to its cost-effectiveness.

End User: Commercial, Military & Government, Other. The commercial segment is the largest, demonstrating robust growth and diverse applications.

Satellite Subsystem: Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms. Each subsystem segment contributes significantly to the overall market value, with Bus & Subsystems holding the largest share.

Propulsion Technology: Electric, Gas based, Liquid Fuel. Electric propulsion is gaining market share due to its efficiency.

Country: United States, Canada. The United States accounts for a large proportion of the total market.

Application: Communication, Earth Observation, Navigation, Space Observation, Others. Earth observation is a leading application driving market growth.

Satellite Mass: Below 10 Kg, 10-100kg, 100-500kg, 500-1000kg, above 1000kg. The smaller satellite mass segments are expanding rapidly.

Key Drivers of North America Satellite Manufacturing Market Growth

Several factors contribute to the market's growth: increasing demand for high-bandwidth communication, the rising need for advanced Earth observation capabilities across diverse industries (e.g., agriculture, environmental monitoring, disaster management), and government investments in space exploration and national security programs. Technological advancements, such as miniaturization of satellites and the development of electric propulsion systems, further fuel market expansion. Favorable regulatory environments and supportive government policies in both the US and Canada also contribute to market growth.

Challenges in the North America Satellite Manufacturing Market Sector

The industry faces challenges such as high manufacturing costs, lengthy development cycles, and the complexities involved in obtaining regulatory approvals for satellite launches and operations. Supply chain disruptions, particularly regarding specialized components and materials, can significantly impact production timelines and costs. Intense competition, especially from emerging players and international companies, also puts pressure on profitability margins. The market also faces challenges related to space debris and the sustainability of space operations.

Emerging Opportunities in North America Satellite Manufacturing Market

Emerging opportunities include the growth of smallsat constellations providing global broadband internet access, the increasing adoption of IoT (Internet of Things) devices relying on satellite communication, and the expanding use of AI and machine learning for satellite data analysis and interpretation. New markets are opening up in areas like precision agriculture, environmental monitoring, and maritime surveillance. The development of more robust and resilient satellite systems, capable of withstanding harsh environmental conditions, presents significant opportunities.

Leading Players in the North America Satellite Manufacturing Market Market

- Space Exploration Technologies Corp

- Swarm Technologies Inc

- Lockheed Martin Corporation

- Maxar Technologies Inc

- Thales Alenia Space (Website link unavailable)

- Planet Labs Inc

- Northrop Grumman Corporation

- Spire Global Inc

- Capella Space Corp (Website link unavailable)

Key Developments in North America Satellite Manufacturing Industry

- July 2023: Planet Labs launched 48 Dove satellites from the Baikonur Cosmodrome, expanding its Earth observation constellation.

- November 2023: Thales Alenia Space secured a contract with Inmarsat for the Inmarsat-5 satellite, demonstrating continued growth in large satellite projects.

- December 2023: Planet Labs deployed 12 Dove nanosatellites from the Vostochny Cosmodrome, highlighting the ongoing trend of nanosatellite deployments.

Strategic Outlook for North America Satellite Manufacturing Market Market

The North American satellite manufacturing market is poised for sustained growth, driven by technological advancements, increasing demand for satellite-based services, and continued government investment. The focus on miniaturization, cost reduction, and enhanced data capabilities will shape future market dynamics. The emergence of new applications and market segments will create further opportunities for growth and innovation. The industry will need to address challenges related to sustainability and space debris mitigation to ensure the long-term health of the sector.

North America Satellite Manufacturing Market Segmentation

-

1. Application

- 1.1. Communication

- 1.2. Earth Observation

- 1.3. Navigation

- 1.4. Space Observation

- 1.5. Others

-

2. Satellite Mass

- 2.1. 10-100kg

- 2.2. 100-500kg

- 2.3. 500-1000kg

- 2.4. Below 10 Kg

- 2.5. above 1000kg

-

3. Orbit Class

- 3.1. Eliptical

- 3.2. GEO

- 3.3. LEO

- 3.4. MEO

-

4. End User

- 4.1. Commercial

- 4.2. Military & Government

- 4.3. Other

-

5. Satellite Subsystem

- 5.1. Propulsion Hardware and Propellant

- 5.2. Satellite Bus & Subsystems

- 5.3. Solar Array & Power Hardware

- 5.4. Structures, Harness & Mechanisms

-

6. Propulsion Tech

- 6.1. Electric

- 6.2. Gas based

- 6.3. Liquid Fuel

North America Satellite Manufacturing Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Satellite Manufacturing Market Regional Market Share

Geographic Coverage of North America Satellite Manufacturing Market

North America Satellite Manufacturing Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication

- 5.1.2. Earth Observation

- 5.1.3. Navigation

- 5.1.4. Space Observation

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Satellite Mass

- 5.2.1. 10-100kg

- 5.2.2. 100-500kg

- 5.2.3. 500-1000kg

- 5.2.4. Below 10 Kg

- 5.2.5. above 1000kg

- 5.3. Market Analysis, Insights and Forecast - by Orbit Class

- 5.3.1. Eliptical

- 5.3.2. GEO

- 5.3.3. LEO

- 5.3.4. MEO

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Commercial

- 5.4.2. Military & Government

- 5.4.3. Other

- 5.5. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 5.5.1. Propulsion Hardware and Propellant

- 5.5.2. Satellite Bus & Subsystems

- 5.5.3. Solar Array & Power Hardware

- 5.5.4. Structures, Harness & Mechanisms

- 5.6. Market Analysis, Insights and Forecast - by Propulsion Tech

- 5.6.1. Electric

- 5.6.2. Gas based

- 5.6.3. Liquid Fuel

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Satellite Manufacturing Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Communication

- 6.1.2. Earth Observation

- 6.1.3. Navigation

- 6.1.4. Space Observation

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Satellite Mass

- 6.2.1. 10-100kg

- 6.2.2. 100-500kg

- 6.2.3. 500-1000kg

- 6.2.4. Below 10 Kg

- 6.2.5. above 1000kg

- 6.3. Market Analysis, Insights and Forecast - by Orbit Class

- 6.3.1. Eliptical

- 6.3.2. GEO

- 6.3.3. LEO

- 6.3.4. MEO

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Commercial

- 6.4.2. Military & Government

- 6.4.3. Other

- 6.5. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 6.5.1. Propulsion Hardware and Propellant

- 6.5.2. Satellite Bus & Subsystems

- 6.5.3. Solar Array & Power Hardware

- 6.5.4. Structures, Harness & Mechanisms

- 6.6. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6.6.1. Electric

- 6.6.2. Gas based

- 6.6.3. Liquid Fuel

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Space Exploration Technologies Corp

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Swarm Technologies Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Lockheed Martin Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Maxar Technologies Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Thale

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Planet Labs Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Northrop Grumman Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Spire Global Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Capella Space Corp

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Space Exploration Technologies Corp

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Satellite Manufacturing Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America Satellite Manufacturing Market Share (%) by Company 2025

List of Tables

- Table 1: North America Satellite Manufacturing Market Revenue million Forecast, by Application 2020 & 2033

- Table 2: North America Satellite Manufacturing Market Revenue million Forecast, by Satellite Mass 2020 & 2033

- Table 3: North America Satellite Manufacturing Market Revenue million Forecast, by Orbit Class 2020 & 2033

- Table 4: North America Satellite Manufacturing Market Revenue million Forecast, by End User 2020 & 2033

- Table 5: North America Satellite Manufacturing Market Revenue million Forecast, by Satellite Subsystem 2020 & 2033

- Table 6: North America Satellite Manufacturing Market Revenue million Forecast, by Propulsion Tech 2020 & 2033

- Table 7: North America Satellite Manufacturing Market Revenue million Forecast, by Region 2020 & 2033

- Table 8: North America Satellite Manufacturing Market Revenue million Forecast, by Application 2020 & 2033

- Table 9: North America Satellite Manufacturing Market Revenue million Forecast, by Satellite Mass 2020 & 2033

- Table 10: North America Satellite Manufacturing Market Revenue million Forecast, by Orbit Class 2020 & 2033

- Table 11: North America Satellite Manufacturing Market Revenue million Forecast, by End User 2020 & 2033

- Table 12: North America Satellite Manufacturing Market Revenue million Forecast, by Satellite Subsystem 2020 & 2033

- Table 13: North America Satellite Manufacturing Market Revenue million Forecast, by Propulsion Tech 2020 & 2033

- Table 14: North America Satellite Manufacturing Market Revenue million Forecast, by Country 2020 & 2033

- Table 15: United States North America Satellite Manufacturing Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada North America Satellite Manufacturing Market Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Mexico North America Satellite Manufacturing Market Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Satellite Manufacturing Market?

The projected CAGR is approximately 14.4%.

2. Which companies are prominent players in the North America Satellite Manufacturing Market?

Key companies in the market include Space Exploration Technologies Corp, Swarm Technologies Inc, Lockheed Martin Corporation, Maxar Technologies Inc, Thale, Planet Labs Inc, Northrop Grumman Corporation, Spire Global Inc, Capella Space Corp.

3. What are the main segments of the North America Satellite Manufacturing Market?

The market segments include Application, Satellite Mass, Orbit Class, End User, Satellite Subsystem, Propulsion Tech.

4. Can you provide details about the market size?

The market size is estimated to be USD 12031.2 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

December 2023: Planet Labs has built 12 Dove nanosatellites for Planet. These satellites are launched from Vostochny Cosmodrome.November 2023: Thales Alenia Space signed a contract with Inmarsat for the construction of Inmarsat-5 satellite. The satellite was launched aboard Ariane-5ECAJuly 2023: Planet Labs has built 48 Dove satellites. These satellites are launched from Baikonur Cosmodrome.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Satellite Manufacturing Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Satellite Manufacturing Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Satellite Manufacturing Market?

To stay informed about further developments, trends, and reports in the North America Satellite Manufacturing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence