Key Insights

The North American sugar substitutes market, valued at approximately $X billion in 2025, is projected to experience steady growth, driven by increasing health consciousness and the prevalence of chronic diseases like diabetes. The market's Compound Annual Growth Rate (CAGR) of 3.99% from 2019-2033 indicates a consistent demand for healthier alternatives to traditional sugar. Key segments driving this growth include the food and beverage industry, which utilizes sugar substitutes extensively in low-calorie and diet products, and the dietary supplement sector, where sugar substitutes are used in products promoting weight management. The natural segment, particularly stevia, is gaining traction due to consumer preference for natural ingredients, while artificial sweeteners like sucralose and aspartame maintain a strong presence owing to their widespread use and established market share. However, concerns regarding the long-term health effects of some artificial sweeteners pose a restraint to the market’s growth, encouraging research and development efforts focusing on safer and more natural alternatives. Major players like Cargill, DuPont, and ADM are actively involved in innovation, product diversification, and strategic acquisitions to maintain market competitiveness. Geographic analysis reveals strong market presence in the United States, Canada, and Mexico, with the US holding the largest share due to its significant food and beverage industry. The market is further segmented by type (Acesulfame K, Aspartame, Saccharin, Sucralose, Neotame, Stevia, Others), origin (Natural, Artificial/Synthetic), and application (Food & Beverage, Dietary Supplements, Pharmaceuticals, Others).

Looking forward, the North American sugar substitutes market is expected to witness a further expansion, propelled by the rising demand for low-calorie and zero-calorie food and beverages. The growing prevalence of obesity and diabetes will continue to push consumers toward sugar alternatives. Furthermore, increased awareness of the health risks associated with excessive sugar consumption is expected to further boost the market. However, fluctuating raw material prices and stringent regulations regarding the use and labeling of artificial sweeteners could present challenges. The market will likely see increasing investment in research and development of novel sugar substitutes with improved taste profiles and safety profiles, catering to the evolving consumer preferences and stringent regulatory environments. The competitive landscape is expected to remain dynamic, with companies focusing on product innovation, brand building, and expansion into new markets to capture a larger market share.

North America Sugar Substitutes Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America sugar substitutes industry, covering market size, segmentation, growth drivers, challenges, and future outlook. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report offers invaluable insights for industry stakeholders, investors, and businesses seeking to understand and capitalize on the evolving dynamics of this significant market.

North America Sugar Substitutes Industry Market Concentration & Innovation

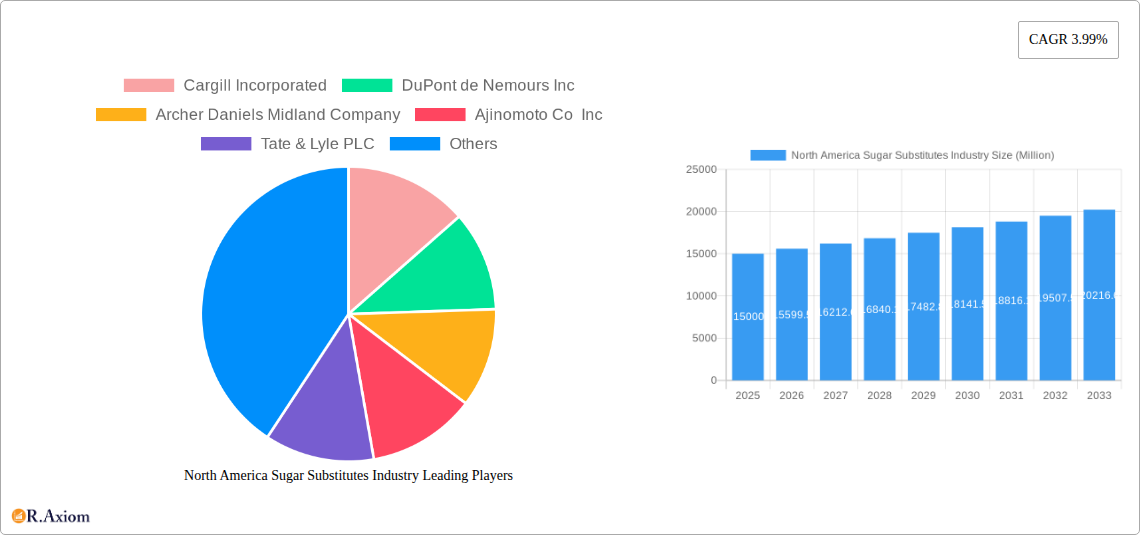

The North America sugar substitutes market exhibits a moderately concentrated structure, with key players like Cargill Incorporated, DuPont de Nemours Inc, Archer Daniels Midland Company, Ajinomoto Co Inc, Tate & Lyle PLC, Roquette Freres, PureCircle Ltd, and Ingredion Incorporated holding significant market share. The exact market share distribution for 2025 is estimated at xx%, reflecting a dynamic competitive landscape. Innovation is a crucial driver, fueled by the increasing demand for healthier alternatives to sugar and advancements in sweetener technology.

Regulatory frameworks, particularly those concerning labeling and health claims, significantly influence market dynamics. The emergence of novel sugar substitutes and the ongoing research into their long-term health effects further shape the competitive environment. Mergers and acquisitions (M&A) activity has been moderate in recent years, with deal values totaling approximately $xx Million in the period 2019-2024. Future M&A activity is anticipated to increase as companies seek to expand their product portfolios and market reach. Consumer trends towards natural and low-calorie options continue to influence product development and market growth.

- Market Concentration: Moderately concentrated, with top players holding xx% market share (2025 estimate).

- Innovation Drivers: Health concerns, technological advancements, consumer preferences.

- Regulatory Framework: Stringent labeling and health claim regulations impact market dynamics.

- M&A Activity: Total deal value of approximately $xx Million (2019-2024).

North America Sugar Substitutes Industry Industry Trends & Insights

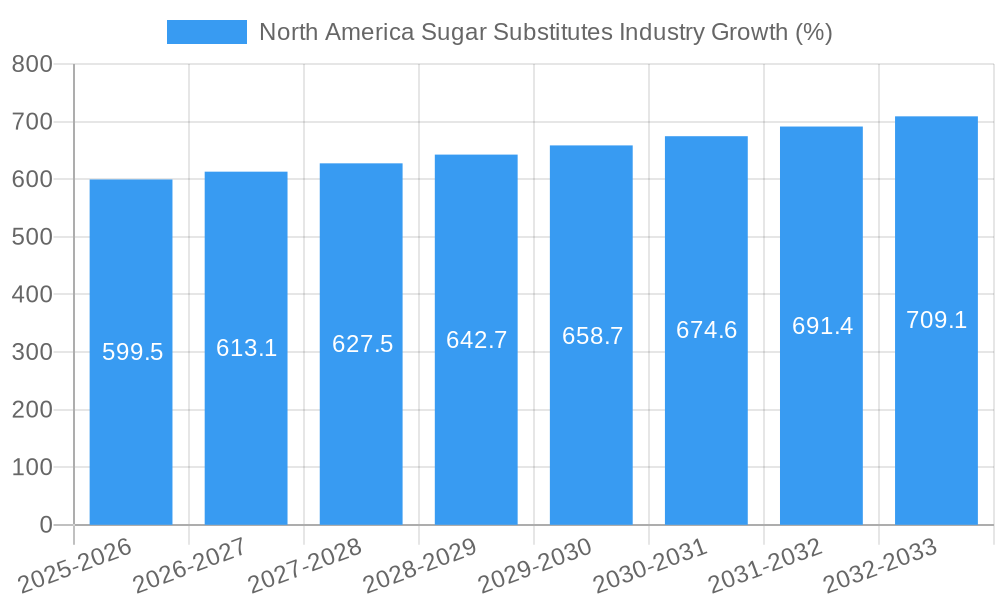

The North America sugar substitutes market is experiencing robust growth, driven by increasing health consciousness among consumers, rising prevalence of diabetes and obesity, and the growing demand for low-calorie and sugar-free food and beverage products. The market is projected to register a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), reaching a market size of $xx Million by 2033. Technological advancements in sweetener production, particularly in the area of natural sweeteners, are creating new opportunities and driving market expansion.

Consumer preferences are shifting towards natural and plant-based sweeteners, creating a significant opportunity for companies offering stevia, monk fruit, and other natural alternatives. The market is also witnessing increased adoption of sugar substitutes in various applications beyond food and beverages, including dietary supplements and pharmaceuticals. Competitive dynamics are shaped by product innovation, branding, pricing strategies, and distribution networks. Market penetration of natural sweeteners is steadily increasing, reaching an estimated xx% in 2025.

Dominant Markets & Segments in North America Sugar Substitutes Industry

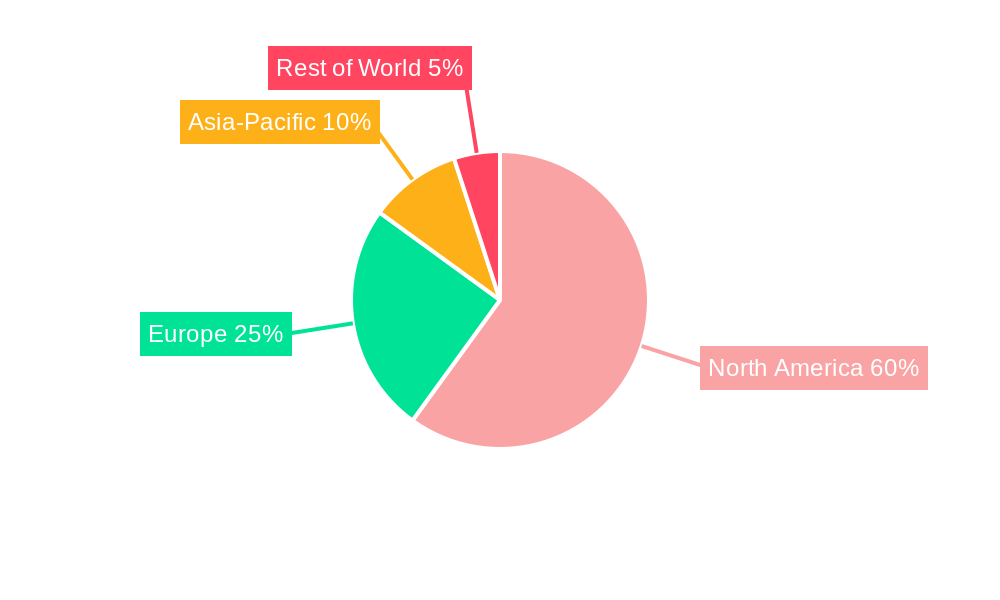

The Food and Beverage segment remains the dominant application area for sugar substitutes in North America, accounting for approximately xx% of the total market in 2025. This dominance is driven by the extensive use of sugar substitutes in processed foods, beverages, and confectionery products. The United States is the largest market within North America, driven by high consumer demand and established distribution channels.

- By Application:

- Food and Beverage: Largest segment, driven by high demand for low-calorie and sugar-free options. xx% market share (2025).

- Dietary Supplements & Pharmaceuticals: Growing segment, driven by health benefits and functional food trends. xx% market share (2025)

- By Origin:

- Natural Sweeteners: Fastest-growing segment, driven by consumer preference for natural products. xx% market share (2025).

- Artificial/Synthetic Sweeteners: Maintains significant market share due to cost-effectiveness. xx% market share (2025).

- By Type:

- Sucralose, Stevia: Dominant types due to consumer acceptance and widespread application. xx% and xx% market share (2025), respectively.

- Acesulfame K, Aspartame, Saccharin: Maintain significant market share due to long-standing presence and wide use. xx%, xx%, and xx% market share (2025), respectively.

Key drivers for this dominance include favorable economic conditions, well-developed infrastructure, and a strong regulatory framework.

North America Sugar Substitutes Industry Product Developments

Recent product innovations include the development of new sweetener blends offering improved taste profiles and functionalities. Advances in extraction and processing technologies are leading to more sustainable and cost-effective production of natural sweeteners. Companies are focusing on creating sugar substitutes with minimal aftertaste and better integration into various food and beverage applications. These innovations are enhancing the market fit and competitiveness of sugar substitutes.

Report Scope & Segmentation Analysis

This report comprehensively segments the North American sugar substitutes market by application (food and beverage, dietary supplements, pharmaceuticals), origin (natural, artificial/synthetic), and type (acesulfame K, aspartame, saccharin, sucralose, neotame, stevia, other types). Each segment's growth projections, market size (in Millions), and competitive dynamics are analyzed, offering a granular understanding of the market landscape. For example, the natural sweeteners segment is projected to experience the highest growth rate due to increasing consumer demand for healthier alternatives. The artificial sweeteners segment will remain significant due to their cost-effectiveness and wide acceptance, albeit facing increasing competition from the natural segment. Individual sweetener types such as sucralose and stevia will show differing growth trajectories based on consumer preferences and regulatory considerations.

Key Drivers of North America Sugar Substitutes Industry Growth

The growth of the North America sugar substitutes industry is primarily propelled by increasing health concerns, particularly regarding obesity and diabetes. This is coupled with rising consumer awareness of the health risks associated with high sugar intake. Government regulations promoting healthier food options and the development of innovative, better-tasting sugar substitutes further accelerate market growth. Technological advancements leading to the cost-effective production of natural sweeteners also contribute to the expansion of the market.

Challenges in the North America Sugar Substitutes Industry Sector

The North America sugar substitutes industry faces several challenges, including evolving consumer perceptions of certain artificial sweeteners, fluctuating raw material prices, and stringent regulatory requirements. Supply chain disruptions and concerns regarding the long-term health effects of some sugar substitutes present additional obstacles. These challenges can lead to increased production costs and price volatility, potentially impacting market growth.

Emerging Opportunities in North America Sugar Substitutes Industry

Emerging opportunities lie in the development of novel, naturally derived sweeteners, expansion into niche applications (e.g., functional foods, specialized beverages), and personalized nutrition strategies. Technological advancements in sweetener production and the growing demand for sustainable and ethically sourced ingredients present significant potential for market expansion. Moreover, increasing awareness of the link between diet and overall health continues to propel the market forward.

Leading Players in the North America Sugar Substitutes Industry Market

- Cargill Incorporated

- DuPont de Nemours Inc

- Archer Daniels Midland Company

- Ajinomoto Co Inc

- Tate & Lyle PLC

- Roquette Freres

- PureCircle Ltd

- Ingredion Incorporated

Key Developments in North America Sugar Substitutes Industry Industry

- 2022 Q3: Ingredion Incorporated launches a new stevia-based sweetener.

- 2023 Q1: Cargill Incorporated announces a strategic partnership to expand its natural sweetener portfolio.

- 2024 Q2: New regulations regarding sugar substitute labeling go into effect in several states. (Further details on specific developments would be added in the full report)

Strategic Outlook for North America Sugar Substitutes Industry Market

The North America sugar substitutes market is poised for continued growth, driven by increasing health awareness, evolving consumer preferences, and ongoing innovation in sweetener technologies. The focus on natural and sustainable sweeteners, coupled with strategic partnerships and acquisitions, will shape the future market landscape. Opportunities exist for companies to expand their product portfolios, penetrate new market segments, and address unmet consumer needs. The market's growth trajectory is projected to remain strong throughout the forecast period.

North America Sugar Substitutes Industry Segmentation

-

1. Origin

- 1.1. Natural

- 1.2. Artificial/Synthetic

-

2. Type

- 2.1. Acesulfame K

- 2.2. Aspartame

- 2.3. Saccharin

- 2.4. Sucralose

- 2.5. Neotame

- 2.6. Stevia

- 2.7. Other Types

-

3. Application

-

3.1. Food and Beverage

- 3.1.1. Bakery

- 3.1.2. Confectionery

- 3.1.3. Dairy Products

- 3.1.4. Beverages

- 3.1.5. Meat and Seafood

- 3.1.6. Others

- 3.2. Dietary Supplements

- 3.3. Pharmaceuticals

-

3.1. Food and Beverage

-

4. Geography

-

4.1. North America

- 4.1.1. United States

- 4.1.2. Canada

- 4.1.3. Mexixo

- 4.1.4. Rest of North America

-

4.1. North America

North America Sugar Substitutes Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexixo

- 1.4. Rest of North America

North America Sugar Substitutes Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.99% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Health Benefits Promoting Apple Cider Vinegar Demand; Unfiltered Apple Cider Vinegar Being Popular

- 3.3. Market Restrains

- 3.3.1. Rising Demand for Other Vinegar Types

- 3.4. Market Trends

- 3.4.1. Rising Popularity of Stevia

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Sugar Substitutes Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Origin

- 5.1.1. Natural

- 5.1.2. Artificial/Synthetic

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Acesulfame K

- 5.2.2. Aspartame

- 5.2.3. Saccharin

- 5.2.4. Sucralose

- 5.2.5. Neotame

- 5.2.6. Stevia

- 5.2.7. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Food and Beverage

- 5.3.1.1. Bakery

- 5.3.1.2. Confectionery

- 5.3.1.3. Dairy Products

- 5.3.1.4. Beverages

- 5.3.1.5. Meat and Seafood

- 5.3.1.6. Others

- 5.3.2. Dietary Supplements

- 5.3.3. Pharmaceuticals

- 5.3.1. Food and Beverage

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. North America

- 5.4.1.1. United States

- 5.4.1.2. Canada

- 5.4.1.3. Mexixo

- 5.4.1.4. Rest of North America

- 5.4.1. North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Origin

- 6. United States North America Sugar Substitutes Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Sugar Substitutes Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Sugar Substitutes Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Sugar Substitutes Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Cargill Incorporated

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 DuPont de Nemours Inc

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Archer Daniels Midland Company

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Ajinomoto Co Inc

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Tate & Lyle PLC

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Roquette Freres*List Not Exhaustive

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 PureCircle Ltd

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Ingredion Incorporated

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.1 Cargill Incorporated

List of Figures

- Figure 1: North America Sugar Substitutes Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Sugar Substitutes Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Sugar Substitutes Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Sugar Substitutes Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 3: North America Sugar Substitutes Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: North America Sugar Substitutes Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: North America Sugar Substitutes Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 6: North America Sugar Substitutes Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: North America Sugar Substitutes Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Mexico North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Rest of North America North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: North America Sugar Substitutes Industry Revenue Million Forecast, by Origin 2019 & 2032

- Table 13: North America Sugar Substitutes Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: North America Sugar Substitutes Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 15: North America Sugar Substitutes Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 16: North America Sugar Substitutes Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: United States North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Canada North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Mexixo North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of North America North America Sugar Substitutes Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Sugar Substitutes Industry?

The projected CAGR is approximately 3.99%.

2. Which companies are prominent players in the North America Sugar Substitutes Industry?

Key companies in the market include Cargill Incorporated, DuPont de Nemours Inc, Archer Daniels Midland Company, Ajinomoto Co Inc, Tate & Lyle PLC, Roquette Freres*List Not Exhaustive, PureCircle Ltd, Ingredion Incorporated.

3. What are the main segments of the North America Sugar Substitutes Industry?

The market segments include Origin, Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Health Benefits Promoting Apple Cider Vinegar Demand; Unfiltered Apple Cider Vinegar Being Popular.

6. What are the notable trends driving market growth?

Rising Popularity of Stevia.

7. Are there any restraints impacting market growth?

Rising Demand for Other Vinegar Types.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Sugar Substitutes Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Sugar Substitutes Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Sugar Substitutes Industry?

To stay informed about further developments, trends, and reports in the North America Sugar Substitutes Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence