Key Insights

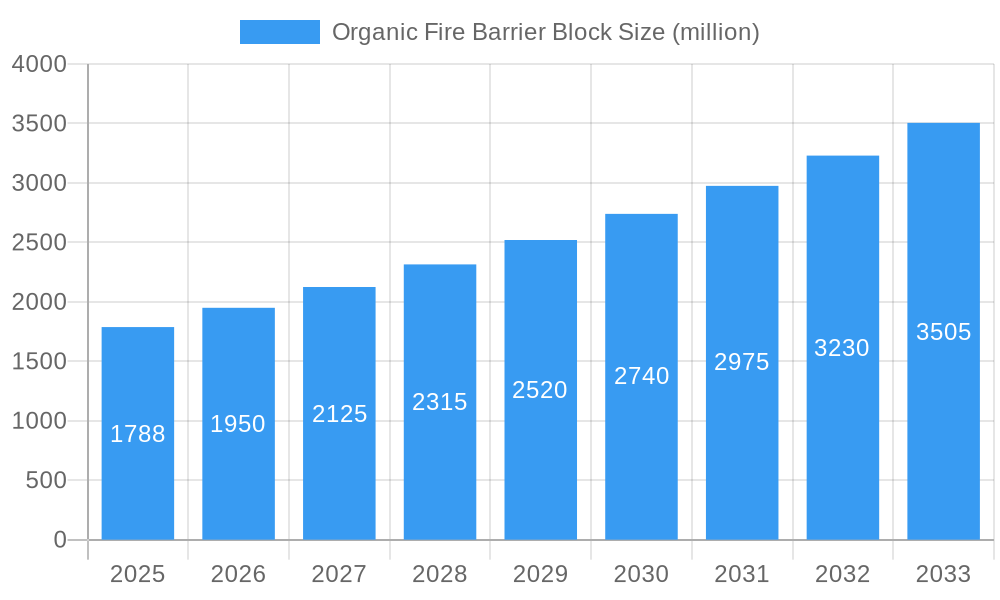

The Organic Fire Barrier Block market is poised for significant expansion, projected to reach $1788 million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 9.1% from 2019 to 2033. This impressive growth trajectory is fueled by escalating global concerns for fire safety regulations across residential, commercial, and industrial sectors. The increasing adoption of stringent building codes worldwide mandates the implementation of effective fire containment solutions, directly boosting the demand for organic fire barrier blocks. Furthermore, advancements in material science are leading to the development of more efficient and sustainable fire-retardant materials, enhancing the performance and appeal of these products. The expanding construction industry, particularly in emerging economies, coupled with the renovation of older structures to meet modern safety standards, represents a substantial market opportunity. The emphasis on lightweight, easy-to-install, and environmentally friendly fireproofing solutions further positions organic fire barrier blocks as a preferred choice.

Organic Fire Barrier Block Market Size (In Billion)

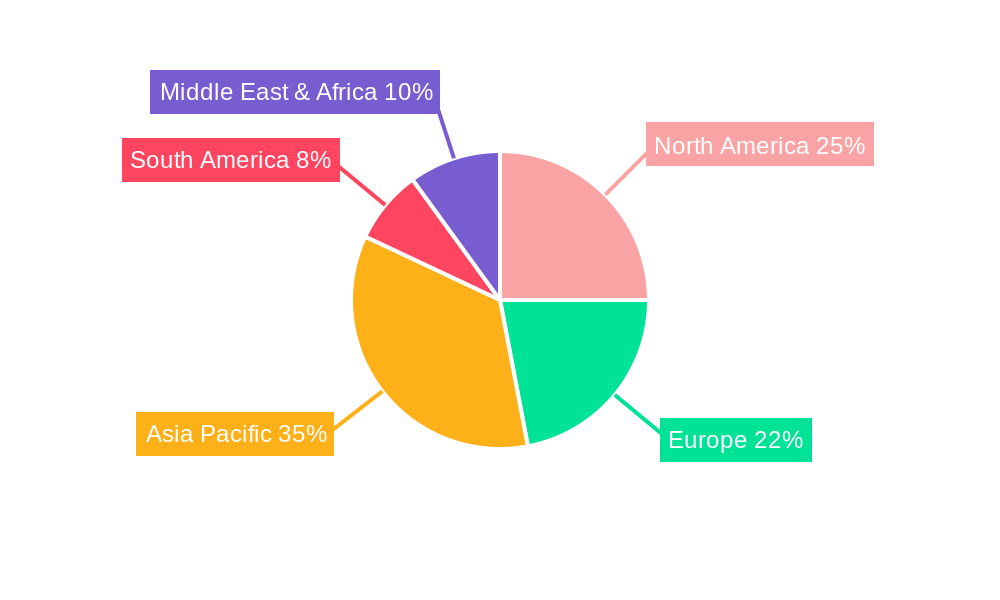

The market is segmented by application into Pipes, Cables, Walls, and Other, with Pipes and Cables likely dominating due to their critical role in preventing fire spread through service penetrations. By type, EVA Made, Foam Made, and PU Made blocks represent key product categories, each offering distinct properties to cater to diverse fire safety requirements. Geographically, the Asia Pacific region, led by China and India, is expected to exhibit the highest growth rates owing to rapid urbanization, significant infrastructure development, and increasing awareness of fire safety. North America and Europe, with their mature markets and well-established regulatory frameworks, will continue to be substantial contributors, driven by ongoing retrofitting projects and new construction demanding high-performance fire barriers. Restrains such as the availability of alternative fireproofing materials and the initial cost of implementation in certain applications are present, but the overarching trend of prioritizing life safety and asset protection is expected to outweigh these limitations, ensuring sustained market expansion.

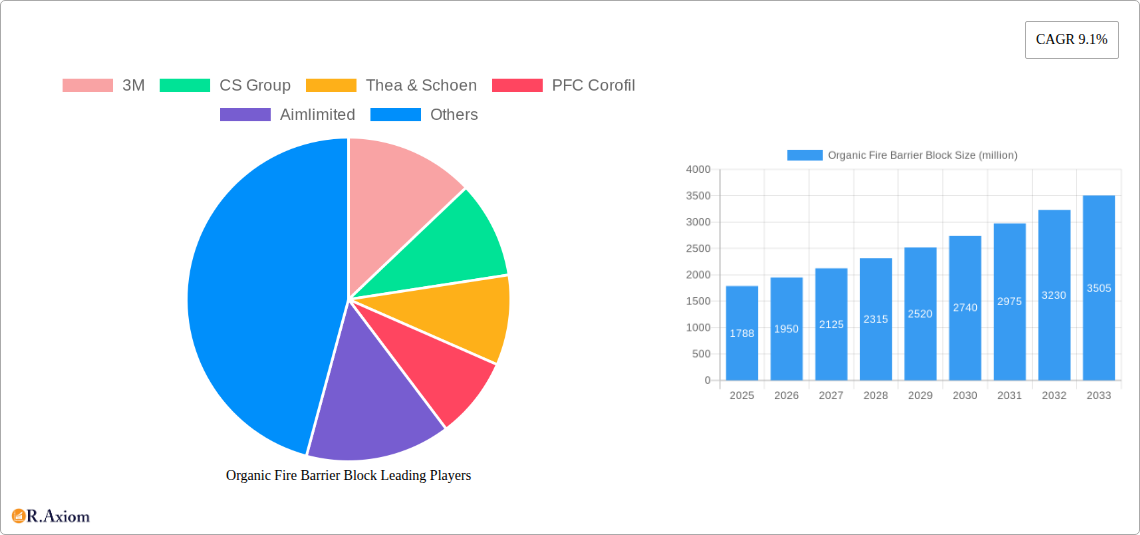

Organic Fire Barrier Block Company Market Share

The organic fire barrier block market exhibits a moderate to high concentration, driven by key players investing heavily in research and development. Innovation is primarily focused on enhancing fire resistance ratings, improving ease of installation, and developing sustainable, eco-friendly materials. Regulatory frameworks, such as stringent building codes and fire safety standards globally, act as significant innovation drivers and market entry barriers. The market is also influenced by the increasing demand for passive fire protection solutions across various sectors. Product substitutes, including intumescent coatings and fire-rated sealants, present a competitive landscape, necessitating continuous product improvement and differentiation. End-user trends favor lightweight, durable, and cost-effective solutions with extended lifecycles. Mergers and Acquisitions (M&A) activities are observed as companies aim to consolidate market share, acquire advanced technologies, and expand their geographical reach. For instance, recent M&A deals in the passive fire protection sector have seen valuations in the hundreds of millions, indicating strategic interest in acquiring innovative product portfolios and established customer bases. The market share of leading companies is estimated to range from 10% to 25%, highlighting a competitive yet consolidated structure.

Organic Fire Barrier Block Industry Trends & Insights

The global organic fire barrier block market is poised for robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of XX% between 2025 and 2033. This expansion is fueled by a confluence of escalating construction activities worldwide, a heightened awareness of fire safety regulations, and the increasing adoption of advanced fire protection systems in both commercial and residential infrastructure. The market penetration of organic fire barrier blocks is steadily increasing as building owners and contractors recognize their efficacy in preventing the spread of fire and smoke through penetrations in fire-rated walls and floors. Technological disruptions are playing a pivotal role, with manufacturers continuously innovating to produce blocks that offer superior thermal insulation, enhanced acoustic properties, and greater resistance to moisture and chemical degradation. The development of novel organic materials, such as advanced EVA (Ethylene Vinyl Acetate) and PU (Polyurethane) composites, is enabling the creation of lighter, more flexible, and easier-to-install fire barrier solutions. Consumer preferences are shifting towards sustainable and non-toxic fireproofing materials, driving demand for organic options that align with green building initiatives. This trend is particularly evident in regions with strong environmental regulations and a growing eco-conscious consumer base. The competitive dynamics within the industry are characterized by a blend of established global players and emerging regional manufacturers, all vying for market share through product differentiation, strategic partnerships, and aggressive marketing campaigns. The increasing complexity of building designs and the growing emphasis on life safety are creating sustained demand for high-performance fire barrier solutions, positioning the organic fire barrier block market for significant long-term growth. The market size is expected to reach XX million by 2033, from an estimated XX million in 2025.

Dominant Markets & Segments in Organic Fire Barrier Block

The organic fire barrier block market is significantly influenced by regional economic policies and infrastructure development, with Asia Pacific emerging as a dominant region. The escalating pace of urbanization and significant investments in infrastructure projects across countries like China, India, and Southeast Asian nations are creating substantial demand for advanced fire safety solutions, including organic fire barrier blocks. Economic policies that promote safe construction practices and enforce stringent building codes further bolster this dominance.

Application: Cables

The Cables segment is a key driver of market growth. The increasing density of electrical and telecommunications cabling in modern buildings, data centers, and industrial facilities necessitates robust fire stopping solutions to prevent fire and smoke propagation along cable pathways. The ease of installation and re-enterability of organic fire barrier blocks make them an ideal choice for managing complex cable penetrations.

- Key Drivers: Growing adoption of smart buildings, expansion of data centers, and increased telecommunication network infrastructure.

- Dominance Analysis: The demand for effective cable fire stopping solutions is particularly high in densely populated urban areas and rapidly developing industrial zones within emerging economies.

Application: Pipes

The Pipes segment also holds significant market share, driven by the widespread use of various piping systems in HVAC, plumbing, and industrial processes. Fire barrier blocks are crucial for sealing penetrations made by pipes through fire-rated walls and floors, ensuring compartmentalization and preventing the spread of fire and smoke.

- Key Drivers: Robust construction of residential, commercial, and industrial facilities; stringent regulations on fire safety for utility penetrations.

- Dominance Analysis: Regions with extensive industrial complexes, large-scale manufacturing, and high-density residential developments exhibit the strongest demand.

Type: EVA Made

EVA Made organic fire barrier blocks are gaining traction due to their excellent flexibility, durability, and ease of use. EVA's inherent properties allow for effective sealing around irregular shapes and provide good resistance to environmental factors, making them a preferred choice for various applications.

- Key Drivers: Demand for lightweight and flexible fire stopping solutions, increasing preference for materials with good thermal and acoustic insulation properties.

- Dominance Analysis: This type of block is favored in applications requiring ease of installation and where movement or vibration might be a concern.

Type: Foam Made

Foam Made organic fire barrier blocks offer excellent void-filling capabilities and superior thermal and acoustic insulation. Their lightweight nature and ability to expand and conform to complex shapes make them highly effective in sealing large or irregularly shaped penetrations.

- Key Drivers: Need for superior insulation properties, ease of application in large or complex openings.

- Dominance Analysis: Widely adopted in industrial settings, commercial buildings, and infrastructure projects where comprehensive fire and smoke containment is paramount.

The dominance of Asia Pacific is further amplified by government initiatives promoting construction safety and smart city development, creating a sustained demand for these essential fire protection products.

Organic Fire Barrier Block Product Developments

Recent product developments in the organic fire barrier block market focus on enhanced fire resistance ratings, improved ease of installation, and greater environmental sustainability. Innovations include advanced EVA and PU formulations offering superior thermal insulation and acoustic damping. Companies are developing blocks with self-adhesive properties for quicker application and re-enterable designs for future cable or pipe additions. These developments aim to provide competitive advantages through reduced installation time, lower labor costs, and compliance with evolving fire safety standards, catering to the growing demand for high-performance and eco-friendly passive fire protection solutions.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the organic fire barrier block market, encompassing segmentation by Application and Type.

Application: Pipes

The Pipes segment is projected to reach XX million by 2033, driven by ongoing construction and renovation projects requiring effective sealing of pipe penetrations. Competitive dynamics are influenced by material performance and ease of installation.

Application: Cables

The Cables segment is expected to expand to XX million by 2033, fueled by the increasing complexity of cable infrastructure in modern buildings and data centers. Manufacturers are focusing on solutions offering high fire ratings and re-enterability.

Application: Walls

The Walls segment is anticipated to grow to XX million by 2033, driven by the demand for fire-rated compartmentation in all types of construction. The ease of integration with wall systems is a key factor.

Application: Other

The Other segment, encompassing applications like ductwork and HVAC systems, is projected to reach XX million by 2033. This segment benefits from the versatility of organic fire barrier blocks.

Type: EVA Made

The EVA Made segment is forecast to reach XX million by 2033, owing to its flexibility and durability. Its growing adoption in various applications is a significant growth driver.

Type: Foam Made

The Foam Made segment is expected to grow to XX million by 2033, driven by its superior insulation properties and void-filling capabilities. Its use in industrial and commercial applications is prominent.

Type: PU Made

The PU Made segment is projected to reach XX million by 2033, leveraging its robust fire performance and chemical resistance.

Type: Other

The Other type segment is anticipated to expand to XX million by 2033, reflecting the development of niche and specialized organic fire barrier block solutions.

Key Drivers of Organic Fire Barrier Block Growth

The growth of the organic fire barrier block market is propelled by several key factors. Stringent global fire safety regulations and building codes mandate the use of effective passive fire protection systems, creating a consistent demand. The increasing construction of high-rise buildings, commercial complexes, data centers, and industrial facilities, particularly in developing economies, requires advanced fire stopping solutions. Technological advancements leading to improved product performance, such as higher fire resistance ratings, enhanced durability, and ease of installation, further stimulate market expansion. A growing awareness among end-users regarding the importance of life safety and property protection in the event of a fire also plays a crucial role in driving market adoption.

Challenges in the Organic Fire Barrier Block Sector

Despite positive growth prospects, the organic fire barrier block sector faces several challenges. Regulatory hurdles and the need for continuous compliance with evolving international and regional fire safety standards can be complex and costly. Supply chain disruptions, particularly for raw materials, can impact production costs and availability, leading to price volatility. Competition from alternative passive fire protection solutions, such as intumescent coatings and mineral wool, poses a constant challenge, requiring manufacturers to innovate and demonstrate superior performance. Additionally, cost sensitivity in certain construction projects can lead to the selection of less expensive but potentially less effective alternatives.

Emerging Opportunities in Organic Fire Barrier Block

The organic fire barrier block market is ripe with emerging opportunities. The increasing focus on sustainable construction and green building certifications presents an opportunity for manufacturers to develop and market eco-friendly and low-VOC (Volatile Organic Compound) fire barrier blocks. The burgeoning smart building technology sector creates demand for fire stopping solutions that can accommodate complex wiring and data cables while maintaining fire integrity. Furthermore, the growing trend of retrofitting older buildings with enhanced fire safety features offers a significant market expansion potential. Geographically, the underserved markets in developing nations represent substantial growth opportunities as their infrastructure development accelerates.

Leading Players in the Organic Fire Barrier Block Market

- 3M

- CS Group

- Thea & Schoen

- PFC Corofil

- Aimlimited

- Rogers Corporation

- Ultrablock

- STI Firestop

- AiM Limited

- Block & Company

- W. W. Grainger

- Balco, Inc

- Sweets

Key Developments in Organic Fire Barrier Block Industry

- 2023/04: Launch of a new generation of lightweight, high-performance EVA-based fire barrier blocks offering enhanced fire resistance and acoustic insulation.

- 2023/09: Strategic partnership formed between a leading fire protection manufacturer and a raw material supplier to ensure stable supply of specialized polymers.

- 2024/01: Company A acquires Company B, a specialist in PU-based fire stopping solutions, to expand its product portfolio and market reach.

- 2024/05: Introduction of a new range of sustainable organic fire barrier blocks made from recycled materials, targeting the growing green building market.

- 2024/10: Major product certification achieved for a new series of fire barrier blocks, enabling wider adoption in stringent building codes.

Strategic Outlook for Organic Fire Barrier Block Market

The strategic outlook for the organic fire barrier block market remains exceptionally positive, driven by an unwavering commitment to fire safety and the continuous evolution of construction practices. Growth catalysts include the global push for enhanced building safety standards, significant investments in infrastructure across both developed and emerging economies, and a heightened consumer demand for reliable and sustainable passive fire protection solutions. The market will benefit from ongoing innovation in material science, leading to products with improved performance characteristics and application efficiencies. Companies that focus on developing specialized solutions for high-demand segments like data centers and renewable energy infrastructure, while also emphasizing environmental responsibility, are well-positioned for sustained success. The ongoing consolidation within the industry, through strategic mergers and acquisitions, is expected to further refine the competitive landscape, fostering greater innovation and market penetration.

Organic Fire Barrier Block Segmentation

-

1. Application

- 1.1. Pipes

- 1.2. Cables

- 1.3. Walls

- 1.4. Other

-

2. Type

- 2.1. EVA Made

- 2.2. Foam Made

- 2.3. PU Made

- 2.4. Other

Organic Fire Barrier Block Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Organic Fire Barrier Block Regional Market Share

Geographic Coverage of Organic Fire Barrier Block

Organic Fire Barrier Block REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pipes

- 5.1.2. Cables

- 5.1.3. Walls

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. EVA Made

- 5.2.2. Foam Made

- 5.2.3. PU Made

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Organic Fire Barrier Block Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pipes

- 6.1.2. Cables

- 6.1.3. Walls

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. EVA Made

- 6.2.2. Foam Made

- 6.2.3. PU Made

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Organic Fire Barrier Block Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pipes

- 7.1.2. Cables

- 7.1.3. Walls

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. EVA Made

- 7.2.2. Foam Made

- 7.2.3. PU Made

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Organic Fire Barrier Block Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pipes

- 8.1.2. Cables

- 8.1.3. Walls

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. EVA Made

- 8.2.2. Foam Made

- 8.2.3. PU Made

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Organic Fire Barrier Block Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pipes

- 9.1.2. Cables

- 9.1.3. Walls

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. EVA Made

- 9.2.2. Foam Made

- 9.2.3. PU Made

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Organic Fire Barrier Block Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pipes

- 10.1.2. Cables

- 10.1.3. Walls

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. EVA Made

- 10.2.2. Foam Made

- 10.2.3. PU Made

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Organic Fire Barrier Block Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Pipes

- 11.1.2. Cables

- 11.1.3. Walls

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. EVA Made

- 11.2.2. Foam Made

- 11.2.3. PU Made

- 11.2.4. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 3M

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 CS Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Thea & Schoen

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 PFC Corofil

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Aimlimited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rogers Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Ultrablock

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 STI Firestop

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AiM Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Block & Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 W. W. Grainger

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Balco Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sweets

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 3M

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Organic Fire Barrier Block Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Organic Fire Barrier Block Revenue (million), by Application 2025 & 2033

- Figure 3: North America Organic Fire Barrier Block Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Organic Fire Barrier Block Revenue (million), by Type 2025 & 2033

- Figure 5: North America Organic Fire Barrier Block Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Organic Fire Barrier Block Revenue (million), by Country 2025 & 2033

- Figure 7: North America Organic Fire Barrier Block Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Organic Fire Barrier Block Revenue (million), by Application 2025 & 2033

- Figure 9: South America Organic Fire Barrier Block Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Organic Fire Barrier Block Revenue (million), by Type 2025 & 2033

- Figure 11: South America Organic Fire Barrier Block Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Organic Fire Barrier Block Revenue (million), by Country 2025 & 2033

- Figure 13: South America Organic Fire Barrier Block Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Organic Fire Barrier Block Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Organic Fire Barrier Block Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Organic Fire Barrier Block Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Organic Fire Barrier Block Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Organic Fire Barrier Block Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Organic Fire Barrier Block Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Organic Fire Barrier Block Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Organic Fire Barrier Block Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Organic Fire Barrier Block Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Organic Fire Barrier Block Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Organic Fire Barrier Block Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Organic Fire Barrier Block Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Organic Fire Barrier Block Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Organic Fire Barrier Block Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Organic Fire Barrier Block Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Organic Fire Barrier Block Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Organic Fire Barrier Block Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Organic Fire Barrier Block Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Organic Fire Barrier Block Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Organic Fire Barrier Block Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Organic Fire Barrier Block Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Organic Fire Barrier Block Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Organic Fire Barrier Block Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Organic Fire Barrier Block Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Organic Fire Barrier Block Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Organic Fire Barrier Block Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Organic Fire Barrier Block Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Organic Fire Barrier Block Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Organic Fire Barrier Block Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Organic Fire Barrier Block Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Organic Fire Barrier Block Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Organic Fire Barrier Block Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Organic Fire Barrier Block Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Organic Fire Barrier Block Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Organic Fire Barrier Block Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Organic Fire Barrier Block Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Organic Fire Barrier Block Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Organic Fire Barrier Block?

The projected CAGR is approximately 9.1%.

2. Which companies are prominent players in the Organic Fire Barrier Block?

Key companies in the market include 3M, CS Group, Thea & Schoen, PFC Corofil, Aimlimited, Rogers Corporation, Ultrablock, STI Firestop, AiM Limited, Block & Company, W. W. Grainger, Balco, Inc, Sweets.

3. What are the main segments of the Organic Fire Barrier Block?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1788 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Organic Fire Barrier Block," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Organic Fire Barrier Block report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Organic Fire Barrier Block?

To stay informed about further developments, trends, and reports in the Organic Fire Barrier Block, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence