Key Insights

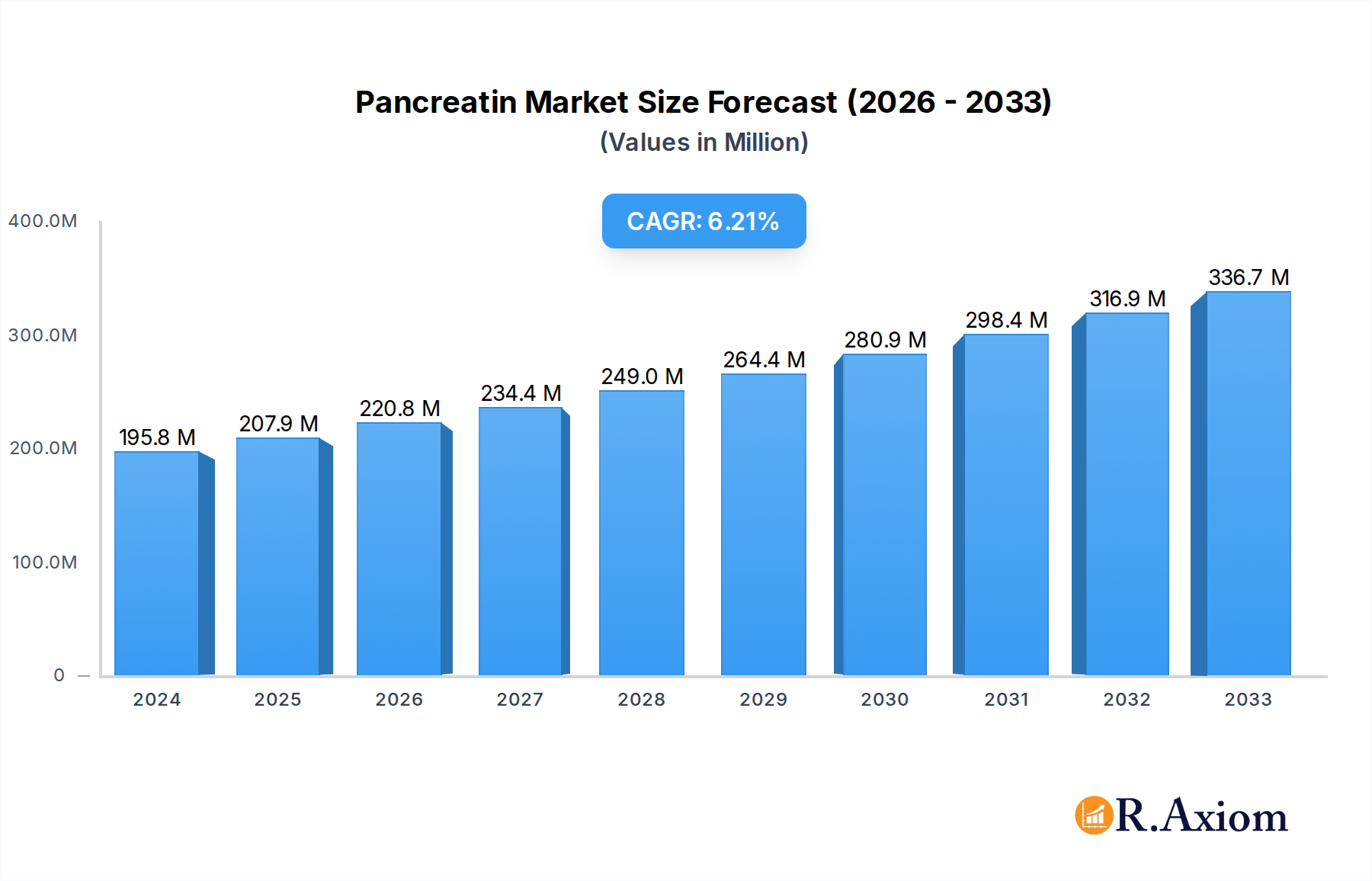

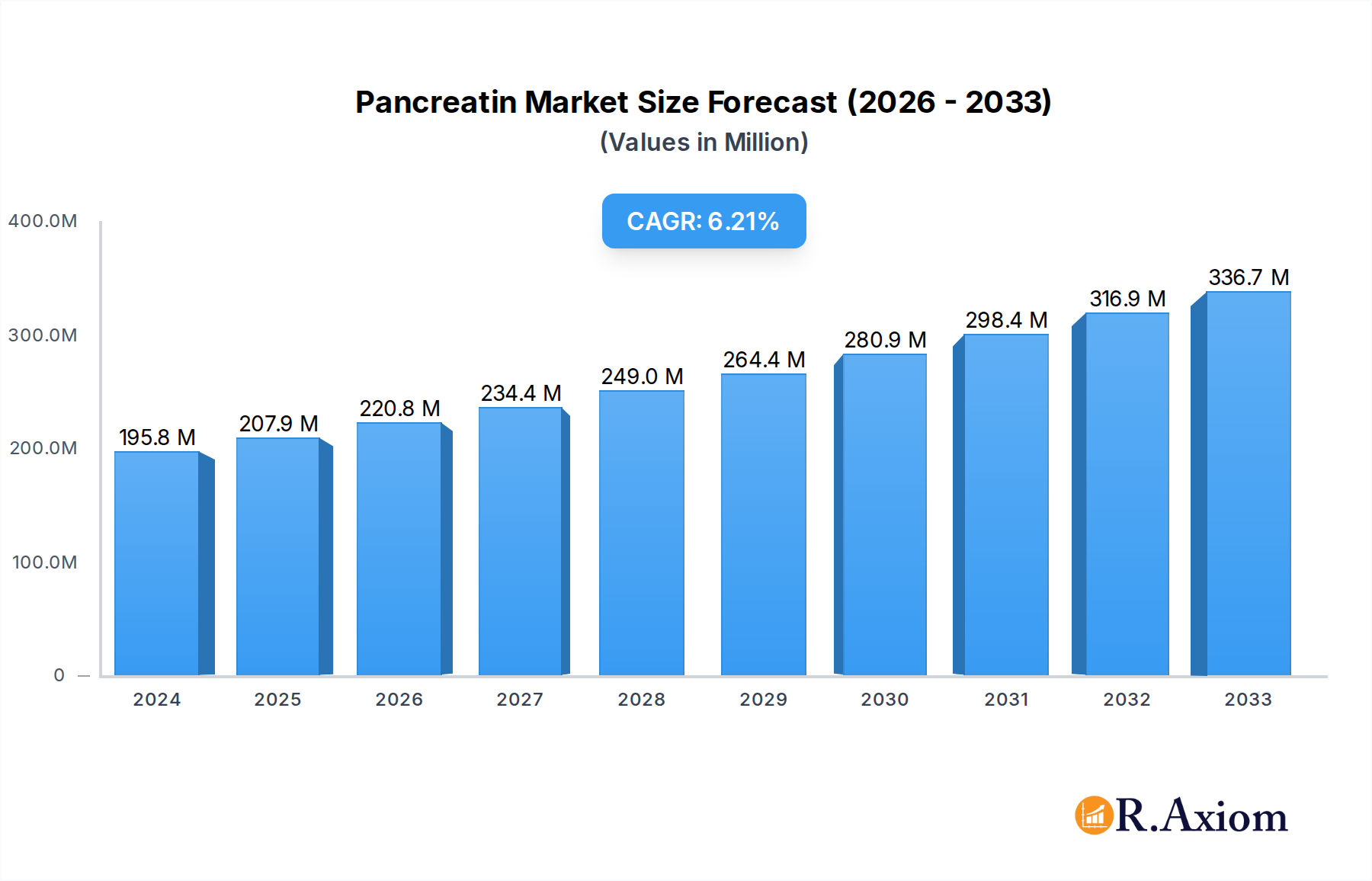

The global pancreatin market is poised for robust expansion, projected to reach an estimated $207.89 million by 2025, growing at a compound annual growth rate (CAGR) of 6.2% through 2033. This growth is primarily fueled by the increasing demand for digestive enzyme supplements and therapeutic applications in the pharmaceutical and food processing industries. The rising prevalence of digestive disorders worldwide, coupled with a growing awareness among consumers about the benefits of enzyme supplementation for improved digestion and nutrient absorption, acts as a significant market driver. Furthermore, advancements in extraction and purification technologies are enhancing the quality and efficacy of pancreatin-based products, thereby broadening their application scope. The food processing sector is leveraging pancreatin for its enzymatic properties in tenderizing meat, modifying starches, and improving dough consistency, while the pharmaceutical industry utilizes it for treating pancreatic insufficiency and other gastrointestinal ailments.

Pancreatin Market Size (In Million)

The market's trajectory is further shaped by emerging trends such as the development of novel drug delivery systems for pancreatin, aiming for enhanced bioavailability and patient compliance. A growing preference for natural and plant-derived enzymes, though currently a niche, also presents an area for potential innovation and diversification within the broader enzyme market, indirectly influencing pancreatin's market dynamics. However, challenges such as stringent regulatory frameworks for pharmaceutical-grade pancreatin and the fluctuating costs of raw materials (animal pancreases) could present hurdles to consistent market growth. Despite these restraints, the expanding application spectrum across both health and industrial sectors, coupled with continuous research and development efforts by key players like Shenzhen Hepalink, Nordmark, and Sichuan Deebio, positions the pancreatin market for sustained and healthy growth over the forecast period. The market's segmentation, with distinct applications in Food Processing and the Pharma Industry, and types like Porcine and Bovine Pancreatin, highlights the diverse opportunities available.

Pancreatin Company Market Share

Here is an SEO-optimized, detailed report description for Pancreatin, incorporating high-traffic keywords and adhering to all specified requirements.

Pancreatin Market Concentration & Innovation

The global Pancreatin market exhibits moderate concentration, with key players including Shenzhen Hepalink, Nordmark, Sichuan Deebio, Sichuan Biosyn, Chongqing Aoli, ALI, Geyuan Tianrun, BIOZYM, and Spectrum Chemicals vying for significant market share. Innovation remains a critical differentiator, driven by advancements in enzyme extraction and purification technologies. The pharmaceutical industry, a primary end-user, demands high purity and specific enzymatic activities, spurring continuous R&D investment. Regulatory frameworks, particularly stringent in North America and Europe, influence product development and market entry, emphasizing safety and efficacy. While direct product substitutes are limited due to pancreatin's unique enzymatic profile, advancements in synthetic digestive aids and alternative therapeutic approaches pose potential long-term threats. End-user trends point towards a growing demand for specialized pancreatin formulations catering to specific digestive disorders and applications in food processing for enhanced texture and digestibility. Mergers and acquisitions (M&A) activities are anticipated to shape the market landscape, with estimated deal values potentially reaching hundreds of millions of dollars, as larger entities seek to consolidate their market position and expand their product portfolios. The total market share of the top five players is projected to be around 70 million.

Pancreatin Industry Trends & Insights

The Pancreatin industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2019 to 2033, with an estimated market size of over 1,500 million in the base year of 2025. This expansion is primarily fueled by the increasing prevalence of pancreatic insufficiency disorders, such as cystic fibrosis and chronic pancreatitis, which necessitate exogenous enzyme replacement therapy. The pharmaceutical sector represents a significant market penetration for pancreatin, driven by its critical role in treating malabsorption syndromes. Technological disruptions are emerging in enzyme immobilization techniques and controlled-release formulations, aiming to improve therapeutic efficacy and patient compliance. Consumer preferences are evolving towards more bioavailable and targeted enzyme supplements, particularly within the burgeoning nutraceutical segment. Competitive dynamics are characterized by intense R&D efforts to enhance enzyme potency, stability, and reduce manufacturing costs. The global market is expected to reach over 2,500 million by the end of the forecast period in 2033. Market penetration within the pharmaceutical sector is estimated to be over 80 million.

Dominant Markets & Segments in Pancreatin

The pharmaceutical industry is the dominant application segment within the global Pancreatin market, driven by the critical need for enzyme replacement therapy in patients suffering from pancreatic exocrine insufficiency. Within this segment, Porcine Pancreatin accounts for the largest market share due to its established efficacy and availability, estimated to be over 900 million in the base year of 2025. The United States and European countries are the leading geographical markets, owing to advanced healthcare infrastructure, high disease prevalence, and favorable reimbursement policies for pancreatic enzyme supplements. Economic policies supporting healthcare accessibility and research funding further bolster these regions. Key drivers for dominance in the pharmaceutical sector include stringent regulatory approvals that favor well-established products like porcine pancreatin, alongside ongoing clinical research validating its therapeutic benefits. The food processing sector, though smaller, is also experiencing significant growth, driven by the demand for natural enzymes in baking, brewing, and meat tenderization, contributing an estimated 300 million to the market. Bovine Pancreatin holds a smaller, yet significant, share, with its adoption influenced by religious or dietary restrictions in certain populations, estimated at over 150 million. The "Others" segment, encompassing research and diagnostic applications, contributes an estimated 50 million, with potential for niche growth.

Pancreatin Product Developments

Product developments in the Pancreatin market are focused on enhancing enzymatic activity, stability, and targeted delivery. Innovations include microencapsulation technologies for improved gastrointestinal transit and delayed release of enzymes, optimizing their therapeutic effect in the small intestine. The development of highly purified pancreatin formulations with specific ratios of amylase, lipase, and protease caters to precise therapeutic needs, offering competitive advantages over generalized enzyme supplements. Advancements in extraction and purification methods are also reducing impurities and increasing the potency of the final product, aligning with market demands for efficacy and safety. These technological trends are crucial for achieving market fit in both the pharmaceutical and specialized food processing applications.

Report Scope & Segmentation Analysis

The global Pancreatin market is meticulously segmented to provide comprehensive insights. The Application segmentation includes Food Processing (estimated market size of over 300 million in 2025, with a projected CAGR of 5.8%), the Pharma Industry (estimated market size of over 900 million in 2025, with a projected CAGR of 6.8%), and Others (estimated market size of over 50 million in 2025, with a projected CAGR of 4.5%). The Type segmentation comprises Porcine Pancreatin (dominant segment, estimated market size over 900 million in 2025, with a projected CAGR of 6.5%), Bovine Pancreatin (estimated market size over 150 million in 2025, with a projected CAGR of 5.5%), and Others (estimated market size over 100 million in 2025, with a projected CAGR of 5.0%). Growth projections for each segment are based on current market trends and anticipated demand shifts.

Key Drivers of Pancreatin Growth

Several key drivers are propelling the growth of the Pancreatin market. The escalating global incidence of pancreatic diseases, including chronic pancreatitis and cystic fibrosis, significantly boosts demand for enzyme replacement therapies. Technological advancements in enzyme purification and formulation technologies, such as microencapsulation, are enhancing product efficacy and patient compliance, leading to market expansion. Growing awareness among healthcare professionals and patients regarding the benefits of pancreatic enzyme supplementation for digestive health is another crucial factor. Furthermore, the expanding applications of pancreatin in the food processing industry, for improving digestibility and texture in various food products, contribute to overall market growth. Favorable regulatory environments in key markets, supporting the approval and adoption of pancreatin-based products, also play a vital role.

Challenges in the Pancreatin Sector

The Pancreatin sector faces several challenges that could impede its growth trajectory. Stringent regulatory requirements for pharmaceutical-grade pancreatin, demanding extensive clinical trials and quality control measures, can significantly increase development costs and time-to-market. Supply chain disruptions, particularly concerning the sourcing of raw animal pancreata, can lead to price volatility and potential shortages, impacting market stability. Intense competition among established players and the threat of emerging alternative digestive aids pose constant pressure on market share. Additionally, consumer perception and potential ethical concerns surrounding the use of animal-derived enzymes in certain markets necessitate careful marketing and communication strategies.

Emerging Opportunities in Pancreatin

Emerging opportunities within the Pancreatin market are ripe for exploitation. The growing nutraceutical and dietary supplement market presents a significant avenue for expansion, with increasing consumer interest in digestive health solutions. Advancements in biotechnology and genetic engineering could lead to the development of recombinant or plant-based pancreatic enzymes, potentially addressing supply limitations and consumer preferences for non-animal-derived products. Expansion into emerging economies with increasing healthcare access and rising disposable incomes offers substantial untapped potential. Furthermore, the exploration of novel therapeutic applications for pancreatin beyond traditional enzyme replacement therapy, such as in wound healing or anti-inflammatory treatments, could unlock new market segments.

Leading Players in the Pancreatin Market

- Shenzhen Hepalink

- Nordmark

- Sichuan Deebio

- Sichuan Biosyn

- Chongqing Aoli

- ALI

- Geyuan Tianrun

- BIOZYM

- Spectrum Chemicals

Key Developments in Pancreatin Industry

- 2024: Launch of advanced microencapsulated porcine pancreatin formulations by Nordmark, enhancing targeted delivery and patient compliance.

- 2023: Sichuan Deebio announced a strategic partnership with a leading European distributor to expand its market reach for pharmaceutical-grade pancreatin.

- 2022: Shenzhen Hepalink invested heavily in R&D for novel extraction techniques to improve the purity and yield of pancreatin.

- 2021: Chongqing Aoli received expanded regulatory approval for its pancreatin product in several Asian markets.

- 2020: BIOZYM introduced a new line of food-grade pancreatin enzymes for improved baking applications.

Strategic Outlook for Pancreatin Market

The strategic outlook for the Pancreatin market remains optimistic, driven by a confluence of factors including an aging global population, increasing prevalence of digestive disorders, and advancements in biotechnology. Focus on product innovation, particularly in areas like targeted delivery systems and enhanced enzyme potency, will be crucial for maintaining competitive advantage. Strategic collaborations and market penetration into emerging economies present significant growth catalysts. The industry's ability to navigate evolving regulatory landscapes and address potential supply chain vulnerabilities will determine the pace of future expansion. The growing demand for high-quality, effective enzyme therapies and supplements positions the pancreatin market for sustained growth in the coming years.

Pancreatin Segmentation

-

1. Application

- 1.1. Food Processing

- 1.2. Pharma Industry

- 1.3. Others

-

2. Type

- 2.1. Porcine Pancreatin

- 2.2. Bovine Pancreatin

- 2.3. Others

Pancreatin Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

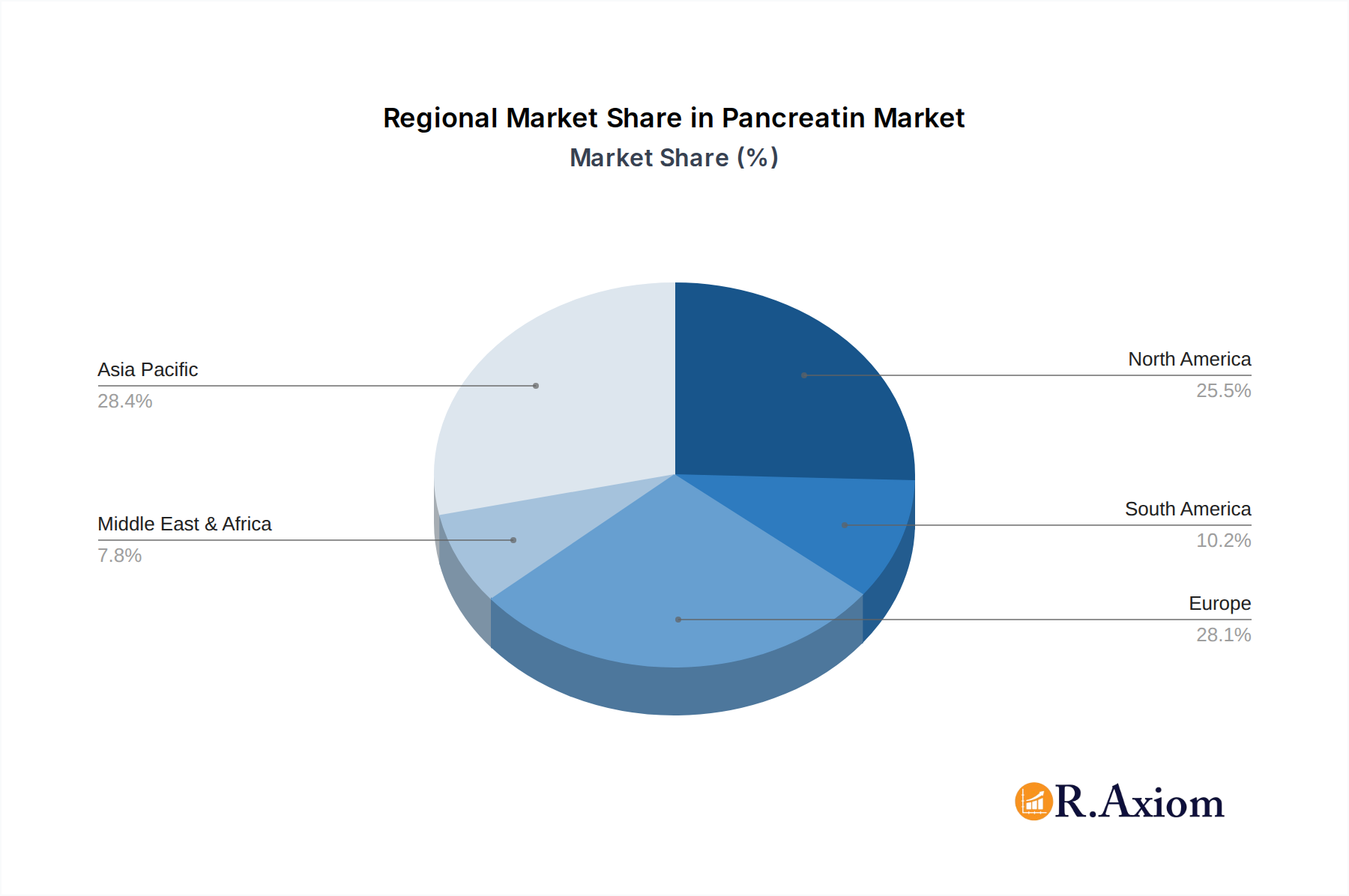

Pancreatin Regional Market Share

Geographic Coverage of Pancreatin

Pancreatin REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food Processing

- 5.1.2. Pharma Industry

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Porcine Pancreatin

- 5.2.2. Bovine Pancreatin

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Pancreatin Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food Processing

- 6.1.2. Pharma Industry

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Porcine Pancreatin

- 6.2.2. Bovine Pancreatin

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Pancreatin Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food Processing

- 7.1.2. Pharma Industry

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Porcine Pancreatin

- 7.2.2. Bovine Pancreatin

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Pancreatin Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food Processing

- 8.1.2. Pharma Industry

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Porcine Pancreatin

- 8.2.2. Bovine Pancreatin

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Pancreatin Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food Processing

- 9.1.2. Pharma Industry

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Porcine Pancreatin

- 9.2.2. Bovine Pancreatin

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Pancreatin Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food Processing

- 10.1.2. Pharma Industry

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Porcine Pancreatin

- 10.2.2. Bovine Pancreatin

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Pancreatin Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food Processing

- 11.1.2. Pharma Industry

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Porcine Pancreatin

- 11.2.2. Bovine Pancreatin

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Shenzhen Hepalink

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Nordmark

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sichuan Deebio

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sichuan Biosyn

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Chongqing Aoli

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 ALI

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Geyuan Tianrun

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 BIOZYM

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Spectrum Chemicals

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Shenzhen Hepalink

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pancreatin Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Pancreatin Revenue (million), by Application 2025 & 2033

- Figure 3: North America Pancreatin Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Pancreatin Revenue (million), by Type 2025 & 2033

- Figure 5: North America Pancreatin Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Pancreatin Revenue (million), by Country 2025 & 2033

- Figure 7: North America Pancreatin Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Pancreatin Revenue (million), by Application 2025 & 2033

- Figure 9: South America Pancreatin Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Pancreatin Revenue (million), by Type 2025 & 2033

- Figure 11: South America Pancreatin Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Pancreatin Revenue (million), by Country 2025 & 2033

- Figure 13: South America Pancreatin Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Pancreatin Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Pancreatin Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Pancreatin Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Pancreatin Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Pancreatin Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Pancreatin Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Pancreatin Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Pancreatin Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Pancreatin Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Pancreatin Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Pancreatin Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Pancreatin Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Pancreatin Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Pancreatin Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Pancreatin Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Pancreatin Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Pancreatin Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Pancreatin Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pancreatin Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Pancreatin Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Pancreatin Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Pancreatin Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Pancreatin Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Pancreatin Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Pancreatin Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Pancreatin Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Pancreatin Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Pancreatin Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Pancreatin Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Pancreatin Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Pancreatin Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Pancreatin Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Pancreatin Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Pancreatin Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Pancreatin Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Pancreatin Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Pancreatin Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pancreatin?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Pancreatin?

Key companies in the market include Shenzhen Hepalink, Nordmark, Sichuan Deebio, Sichuan Biosyn, Chongqing Aoli, ALI, Geyuan Tianrun, BIOZYM, Spectrum Chemicals.

3. What are the main segments of the Pancreatin?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 168 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pancreatin," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pancreatin report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pancreatin?

To stay informed about further developments, trends, and reports in the Pancreatin, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence