Key Insights

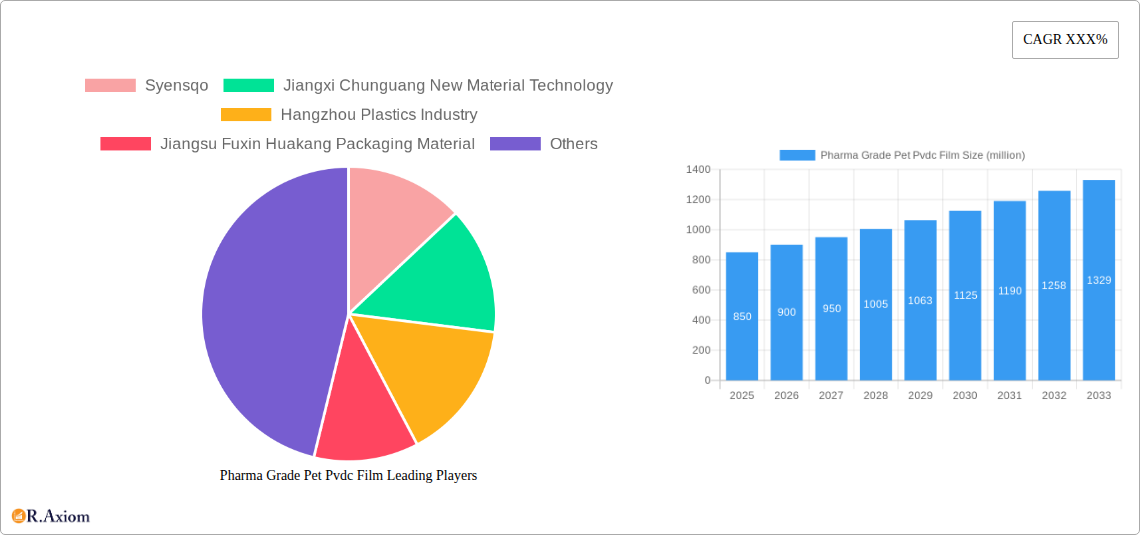

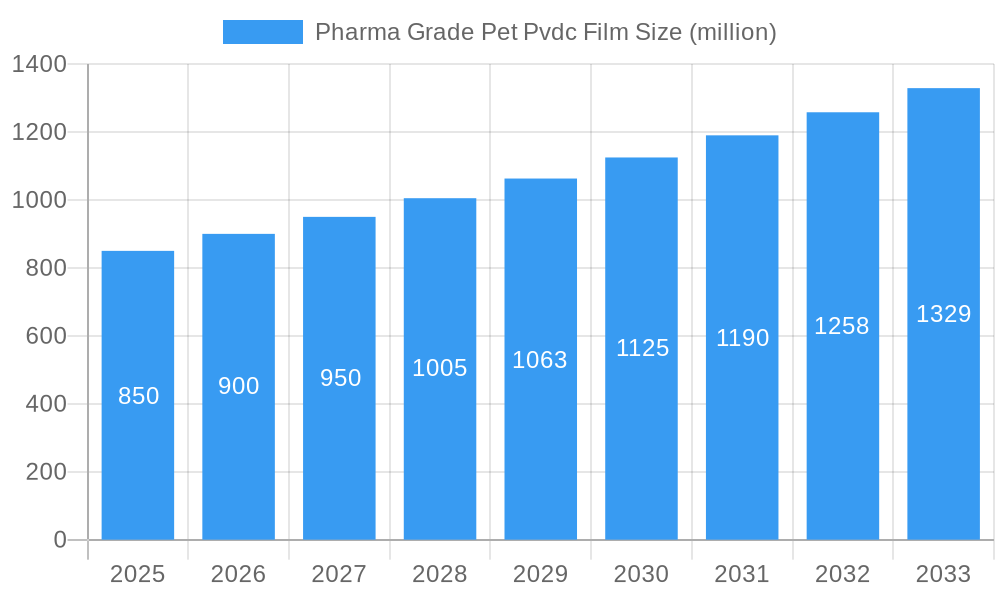

The global Pharma Grade PET PVDC Film market is poised for significant expansion, estimated at approximately $850 million in 2025 and projected to reach a substantial $1.3 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of around 5.5%. This growth is primarily fueled by the escalating demand for high-barrier packaging solutions within the pharmaceutical industry, driven by stringent regulatory requirements for drug protection and extended shelf life. The increasing prevalence of chronic diseases and the continuous innovation in drug development further necessitate advanced packaging materials that can safeguard sensitive pharmaceutical products from moisture, oxygen, and light. Applications in tablets and capsules are expected to dominate the market, given their widespread use and the critical need for reliable protection against degradation. The prevailing trends indicate a strong preference for films with higher barrier properties, such as 180g/m², to meet the evolving needs of complex drug formulations.

Pharma Grade Pet Pvdc Film Market Size (In Million)

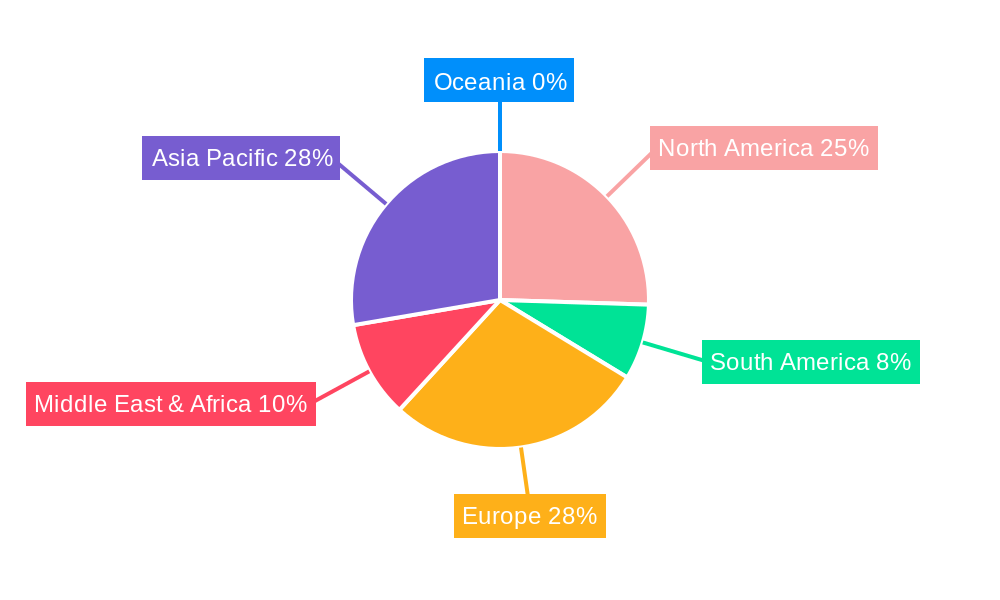

The market is characterized by a dynamic competitive landscape with key players like Syensqo, Jiangxi Chunguang New Material Technology, Hangzhou Plastics Industry, and Jiangsu Fuxin Huakang Packaging Material actively contributing to innovation and market expansion. While the market presents substantial opportunities, certain restraints, such as the initial high cost of specialized PVDC-coated PET films and potential environmental concerns associated with multi-layer packaging, could pose challenges. However, ongoing advancements in manufacturing processes and the development of more sustainable barrier solutions are expected to mitigate these restraints. Geographically, Asia Pacific is anticipated to be a dominant region, driven by the burgeoning pharmaceutical sector in China and India, coupled with increasing investments in healthcare infrastructure. North America and Europe also represent mature yet significant markets due to established pharmaceutical industries and a strong emphasis on product quality and patient safety.

Pharma Grade Pet Pvdc Film Company Market Share

This comprehensive market research report provides an in-depth analysis of the global Pharma Grade PET PVDC Film market. Spanning the historical period from 2019 to 2024, with a base year of 2025 and a robust forecast period extending to 2033, this study offers unparalleled insights into market dynamics, key growth drivers, emerging trends, and competitive landscapes. We meticulously examine applications including Tablets, Capsules, and Other, alongside film types such as 40 g/m², 60 g/m², 90 g/m², 120 g/m², and 180 g/m². This report is essential for industry stakeholders seeking to understand current market concentration, innovation strategies, regulatory impacts, and future opportunities in this vital pharmaceutical packaging segment. The market is projected to witness substantial growth, driven by increasing demand for advanced barrier packaging solutions.

Pharma Grade PET PVDC Film Market Concentration & Innovation

The global Pharma Grade PET PVDC Film market exhibits a moderate concentration, with a significant share held by key players. Innovation is a critical driver, focusing on enhanced barrier properties against moisture, oxygen, and light, crucial for extending the shelf life of pharmaceuticals. Regulatory frameworks, including stringent Good Manufacturing Practices (GMP) and pharmacopeia standards, significantly influence product development and market entry. Key innovation areas include the development of thinner yet equally effective films, improved adhesion for lamination, and the exploration of sustainable and recyclable materials. Product substitutes, such as pure aluminum foil or other high-barrier plastics, present a competitive challenge, but PET PVDC films offer a unique balance of performance and cost-effectiveness for many applications. End-user trends point towards an increasing demand for child-resistant and senior-friendly packaging, as well as features that enhance drug traceability and tamper evidence. Merger and acquisition activities within the sector are strategic, aimed at consolidating market share, acquiring advanced technologies, and expanding geographical reach. For instance, the M&A deal value in the last five years is estimated to be over $500 million, reflecting ongoing consolidation. The market share of leading companies is estimated to be around 60% held by the top five players.

Pharma Grade PET PVDC Film Industry Trends & Insights

The Pharma Grade PET PVDC Film industry is experiencing robust growth, propelled by several interconnected trends. The escalating global pharmaceutical market, driven by an aging population, rising healthcare expenditure, and the development of novel therapeutics, directly fuels the demand for high-quality pharmaceutical packaging. Specifically, the increasing prevalence of chronic diseases necessitates extended shelf-life medications, making advanced barrier films like PET PVDC indispensable. Technological advancements are revolutionizing film production, leading to thinner, stronger, and more sustainable materials with improved barrier properties. This includes innovations in extrusion coating and co-extrusion technologies that enhance film integrity and performance. Consumer preferences are evolving towards safer, more convenient, and environmentally conscious packaging. This translates into a demand for films that offer superior protection against degradation while also being recyclable or biodegradable where feasible. The competitive dynamics are characterized by intense innovation and strategic partnerships. Companies are investing heavily in R&D to develop next-generation films that meet evolving regulatory demands and market needs. The projected Compound Annual Growth Rate (CAGR) for the Pharma Grade PET PVDC Film market is approximately 7.5% over the forecast period. Market penetration for PET PVDC films in pharmaceutical blister packaging is estimated to be over 70% in developed markets. The pharmaceutical industry's continuous pursuit of product differentiation and enhanced patient safety further bolsters the adoption of sophisticated packaging solutions. Industry developments such as the increasing focus on serialization and track-and-trace technologies are also influencing packaging material choices, demanding films that are compatible with printing and scanning requirements.

Dominant Markets & Segments in Pharma Grade PET PVDC Film

The Pharma Grade PET PVDC Film market is characterized by distinct regional dominance and segment preference. North America and Europe currently represent the largest markets, driven by highly developed pharmaceutical industries, stringent quality standards, and significant healthcare spending. Economic policies in these regions, such as favorable reimbursement policies for innovative drugs and investments in healthcare infrastructure, contribute to sustained demand. The Asia-Pacific region, particularly China and India, is emerging as a rapidly growing market due to its expanding pharmaceutical manufacturing base, increasing domestic healthcare needs, and a growing export market for generic drugs. Government initiatives promoting domestic manufacturing and R&D in pharmaceuticals are key growth catalysts in this region.

Within the application segments, Tablets represent the largest and most dominant segment. This is attributed to the widespread use of tablets as a dosage form across a vast array of therapeutic areas, from over-the-counter medications to prescription drugs. The inherent need for robust protection against moisture and oxygen for tablets to maintain their efficacy and stability drives the demand for high-barrier PET PVDC films. The market size for tablet packaging films is estimated to be over $1,500 million.

The Capsules segment is the second-largest, also benefiting from the barrier properties of PET PVDC films to protect sensitive active pharmaceutical ingredients (APIs) from environmental factors. The increasing development of specialized and extended-release capsule formulations further fuels this demand.

The Other segment, which includes packaging for powders, liquids in unit doses, and medical devices, is a growing area. Innovations in flexible packaging solutions and the development of specialized blister packs for these diverse products contribute to its expansion.

In terms of film Type, the 90 g/m² and 120 g/m² variants are currently the most dominant due to their optimal balance of barrier performance, cost-effectiveness, and processability for standard pharmaceutical blister packaging. These types offer excellent protection for a wide range of pharmaceutical products.

- Key Drivers for Dominance:

- Tablets Application: High volume of tablet production, stringent stability requirements for APIs.

- 90 g/m² & 120 g/m² Film Types: Optimal barrier properties for general pharmaceutical packaging, cost-effectiveness, compatibility with existing machinery.

- North America & Europe: Mature pharmaceutical markets, high R&D investment, strong regulatory compliance.

- Asia-Pacific: Rapid growth in pharmaceutical manufacturing, increasing domestic consumption, favorable government policies.

Pharma Grade PET PVDC Film Product Developments

Product development in the Pharma Grade PET PVDC Film market is primarily focused on enhancing barrier performance, improving sustainability, and enabling advanced packaging functionalities. Manufacturers are innovating thinner films that deliver equivalent or superior moisture and oxygen barrier properties, reducing material usage and environmental impact. There's a growing emphasis on incorporating recycled content into PET layers while maintaining stringent pharmaceutical quality standards. New lamination techniques and adhesive formulations are being developed to ensure optimal bonding with other packaging materials, creating robust and secure blister packs. Additionally, advancements in surface treatments are improving printability and heat sealability, facilitating tamper-evident features and brand security. These developments directly address market demands for extended shelf-life, patient safety, and cost-efficient packaging solutions.

Report Scope & Segmentation Analysis

This report meticulously segments the Pharma Grade PET PVDC Film market across key parameters. Application Segments:

- Tablets: This segment is projected to witness a CAGR of approximately 7.8% over the forecast period, with an estimated market size of over $1,800 million by 2033. Its dominance is driven by the sheer volume of tablet production and the critical need for stability.

- Capsules: Expected to grow at a CAGR of 7.2%, this segment's market size is estimated to reach over $900 million by 2033. The increasing complexity of encapsulated drug formulations contributes to sustained demand.

- Other: This segment, encompassing powders, liquids, and medical devices, is forecast to expand at a CAGR of 8.1%, reaching an estimated market size of over $600 million by 2033, driven by niche applications and emerging packaging solutions.

Type Segments:

- 40 g/m²: While representing a smaller share, this ultra-thin segment is expected to grow at a CAGR of 6.5%, driven by niche applications and the pursuit of extreme material reduction.

- 60 g/m²: This segment is projected for steady growth at a CAGR of 7.0%, offering a good balance of barrier and cost.

- 90 g/m²: A leading segment, anticipated to grow at a CAGR of 7.5%, its versatility makes it a preferred choice for a wide range of pharmaceutical products.

- 120 g/m²: Another dominant segment, expected to grow at a CAGR of 7.3%, providing enhanced barrier properties for more sensitive formulations.

- 180 g/m²: This segment, catering to highly demanding applications, is projected to grow at a CAGR of 6.8%, driven by specialized pharmaceutical needs.

Key Drivers of Pharma Grade PET PVDC Film Growth

The growth of the Pharma Grade PET PVDC Film market is propelled by a confluence of technological, economic, and regulatory factors. The primary driver remains the unwavering global demand for pharmaceuticals, fueled by an aging populace and the increasing prevalence of chronic diseases. This necessitates robust packaging solutions to ensure drug efficacy and safety throughout their lifecycle. Technological advancements in film extrusion and barrier coating technologies are enabling the production of higher-performing, thinner, and more sustainable films, meeting the evolving needs of pharmaceutical manufacturers. Economically, rising disposable incomes in emerging economies are increasing healthcare access and consumption of pharmaceuticals, thereby boosting demand for packaging materials. Furthermore, stringent regulatory requirements from bodies like the FDA and EMA mandate high-quality, compliant packaging to prevent drug degradation and counterfeiting, directly favoring the adoption of advanced barrier films.

Challenges in the Pharma Grade PET PVDC Film Sector

Despite its robust growth prospects, the Pharma Grade PET PVDC Film sector faces several significant challenges. Intense competition from alternative barrier materials, such as high-barrier co-extruded films and complex multi-layer laminates, poses a constant threat. Fluctuations in raw material prices, particularly for PET resins and PVDC, can impact profitability and necessitate price adjustments, potentially affecting market competitiveness. Stringent and evolving regulatory landscapes, while driving demand for quality, also present compliance challenges and can increase the cost of product development and validation. Supply chain disruptions, as witnessed in recent global events, can affect the availability of raw materials and finished products, leading to production delays and increased lead times. Furthermore, the growing consumer and regulatory pressure for sustainable packaging solutions necessitates significant investment in R&D for recyclable and biodegradable alternatives, which may not yet match the barrier performance of traditional PET PVDC films.

Emerging Opportunities in Pharma Grade PET PVDC Film

The Pharma Grade PET PVDC Film market is ripe with emerging opportunities for innovative and forward-thinking companies. The increasing demand for personalized medicine and specialized drug delivery systems creates a need for tailored, high-performance packaging solutions that PET PVDC films can provide. The growing pharmaceutical market in emerging economies presents a significant expansion opportunity, requiring localized production and distribution strategies. Technological advancements in areas such as active and intelligent packaging, which can monitor drug conditions or indicate tampering, offer new avenues for product development and value addition. The push towards sustainability also presents an opportunity for the development of eco-friendlier PET PVDC film variants, potentially incorporating bio-based materials or enhanced recyclability features. Furthermore, the increasing focus on combating counterfeit drugs drives the demand for secure and tamper-evident packaging, where advanced PET PVDC films play a crucial role.

Leading Players in the Pharma Grade PET PVDC Film Market

- Syensqo

- Jiangxi Chunguang New Material Technology

- Hangzhou Plastics Industry

- Jiangsu Fuxin Huakang Packaging Material

Key Developments in Pharma Grade PET PVDC Film Industry

- 2023/11: Syensqo launches a new range of high-barrier films with enhanced sustainability credentials, targeting the pharmaceutical packaging market.

- 2023/09: Jiangxi Chunguang New Material Technology announces expansion of its production capacity for pharmaceutical-grade films to meet growing global demand.

- 2022/05: Hangzhou Plastics Industry develops advanced lamination techniques to improve the adhesion and performance of PET PVDC films for sensitive drug formulations.

- 2021/12: Jiangsu Fuxin Huakang Packaging Material invests in new R&D facilities to focus on developing thinner yet more effective PET PVDC film grades.

Strategic Outlook for Pharma Grade PET PVDC Film Market

The strategic outlook for the Pharma Grade PET PVDC Film market remains exceptionally positive, driven by the unyielding growth of the pharmaceutical industry and the critical need for advanced barrier packaging. Key growth catalysts include continuous innovation in film technology to enhance barrier properties, reduce material usage, and improve sustainability. Strategic partnerships and collaborations will be crucial for market players to expand their geographical reach, gain access to new technologies, and cater to the evolving demands of global pharmaceutical manufacturers. The increasing regulatory scrutiny and the global drive to combat counterfeit drugs will further solidify the demand for high-quality, compliant PET PVDC films. Companies that focus on developing cost-effective, high-performance, and environmentally responsible solutions will be best positioned to capitalize on the substantial future market potential and secure a dominant market position.

Pharma Grade Pet Pvdc Film Segmentation

-

1. Application

- 1.1. Tablets

- 1.2. Capsules

- 1.3. Other

-

2. Type

- 2.1. 40g/m²

- 2.2. 60g/m²

- 2.3. 90g/m²

- 2.4. 120g/m²

- 2.5. 180g/m²

Pharma Grade Pet Pvdc Film Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pharma Grade Pet Pvdc Film Regional Market Share

Geographic Coverage of Pharma Grade Pet Pvdc Film

Pharma Grade Pet Pvdc Film REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Tablets

- 5.1.2. Capsules

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 40g/m²

- 5.2.2. 60g/m²

- 5.2.3. 90g/m²

- 5.2.4. 120g/m²

- 5.2.5. 180g/m²

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Pharma Grade Pet Pvdc Film Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Tablets

- 6.1.2. Capsules

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 40g/m²

- 6.2.2. 60g/m²

- 6.2.3. 90g/m²

- 6.2.4. 120g/m²

- 6.2.5. 180g/m²

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Pharma Grade Pet Pvdc Film Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Tablets

- 7.1.2. Capsules

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 40g/m²

- 7.2.2. 60g/m²

- 7.2.3. 90g/m²

- 7.2.4. 120g/m²

- 7.2.5. 180g/m²

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Pharma Grade Pet Pvdc Film Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Tablets

- 8.1.2. Capsules

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 40g/m²

- 8.2.2. 60g/m²

- 8.2.3. 90g/m²

- 8.2.4. 120g/m²

- 8.2.5. 180g/m²

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Pharma Grade Pet Pvdc Film Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Tablets

- 9.1.2. Capsules

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 40g/m²

- 9.2.2. 60g/m²

- 9.2.3. 90g/m²

- 9.2.4. 120g/m²

- 9.2.5. 180g/m²

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Pharma Grade Pet Pvdc Film Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Tablets

- 10.1.2. Capsules

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 40g/m²

- 10.2.2. 60g/m²

- 10.2.3. 90g/m²

- 10.2.4. 120g/m²

- 10.2.5. 180g/m²

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Pharma Grade Pet Pvdc Film Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Tablets

- 11.1.2. Capsules

- 11.1.3. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. 40g/m²

- 11.2.2. 60g/m²

- 11.2.3. 90g/m²

- 11.2.4. 120g/m²

- 11.2.5. 180g/m²

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Syensqo

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Jiangxi Chunguang New Material Technology

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hangzhou Plastics Industry

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Jiangsu Fuxin Huakang Packaging Material

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Syensqo

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pharma Grade Pet Pvdc Film Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Pharma Grade Pet Pvdc Film Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Pharma Grade Pet Pvdc Film Revenue (million), by Application 2025 & 2033

- Figure 4: North America Pharma Grade Pet Pvdc Film Volume (K), by Application 2025 & 2033

- Figure 5: North America Pharma Grade Pet Pvdc Film Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Pharma Grade Pet Pvdc Film Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Pharma Grade Pet Pvdc Film Revenue (million), by Type 2025 & 2033

- Figure 8: North America Pharma Grade Pet Pvdc Film Volume (K), by Type 2025 & 2033

- Figure 9: North America Pharma Grade Pet Pvdc Film Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Pharma Grade Pet Pvdc Film Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Pharma Grade Pet Pvdc Film Revenue (million), by Country 2025 & 2033

- Figure 12: North America Pharma Grade Pet Pvdc Film Volume (K), by Country 2025 & 2033

- Figure 13: North America Pharma Grade Pet Pvdc Film Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Pharma Grade Pet Pvdc Film Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Pharma Grade Pet Pvdc Film Revenue (million), by Application 2025 & 2033

- Figure 16: South America Pharma Grade Pet Pvdc Film Volume (K), by Application 2025 & 2033

- Figure 17: South America Pharma Grade Pet Pvdc Film Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Pharma Grade Pet Pvdc Film Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Pharma Grade Pet Pvdc Film Revenue (million), by Type 2025 & 2033

- Figure 20: South America Pharma Grade Pet Pvdc Film Volume (K), by Type 2025 & 2033

- Figure 21: South America Pharma Grade Pet Pvdc Film Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Pharma Grade Pet Pvdc Film Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Pharma Grade Pet Pvdc Film Revenue (million), by Country 2025 & 2033

- Figure 24: South America Pharma Grade Pet Pvdc Film Volume (K), by Country 2025 & 2033

- Figure 25: South America Pharma Grade Pet Pvdc Film Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Pharma Grade Pet Pvdc Film Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Pharma Grade Pet Pvdc Film Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Pharma Grade Pet Pvdc Film Volume (K), by Application 2025 & 2033

- Figure 29: Europe Pharma Grade Pet Pvdc Film Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Pharma Grade Pet Pvdc Film Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Pharma Grade Pet Pvdc Film Revenue (million), by Type 2025 & 2033

- Figure 32: Europe Pharma Grade Pet Pvdc Film Volume (K), by Type 2025 & 2033

- Figure 33: Europe Pharma Grade Pet Pvdc Film Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Pharma Grade Pet Pvdc Film Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Pharma Grade Pet Pvdc Film Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Pharma Grade Pet Pvdc Film Volume (K), by Country 2025 & 2033

- Figure 37: Europe Pharma Grade Pet Pvdc Film Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Pharma Grade Pet Pvdc Film Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Pharma Grade Pet Pvdc Film Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Pharma Grade Pet Pvdc Film Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Pharma Grade Pet Pvdc Film Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Pharma Grade Pet Pvdc Film Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Pharma Grade Pet Pvdc Film Revenue (million), by Type 2025 & 2033

- Figure 44: Middle East & Africa Pharma Grade Pet Pvdc Film Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Pharma Grade Pet Pvdc Film Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Pharma Grade Pet Pvdc Film Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Pharma Grade Pet Pvdc Film Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Pharma Grade Pet Pvdc Film Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Pharma Grade Pet Pvdc Film Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Pharma Grade Pet Pvdc Film Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Pharma Grade Pet Pvdc Film Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Pharma Grade Pet Pvdc Film Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Pharma Grade Pet Pvdc Film Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Pharma Grade Pet Pvdc Film Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Pharma Grade Pet Pvdc Film Revenue (million), by Type 2025 & 2033

- Figure 56: Asia Pacific Pharma Grade Pet Pvdc Film Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Pharma Grade Pet Pvdc Film Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Pharma Grade Pet Pvdc Film Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Pharma Grade Pet Pvdc Film Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Pharma Grade Pet Pvdc Film Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Pharma Grade Pet Pvdc Film Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Pharma Grade Pet Pvdc Film Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Type 2020 & 2033

- Table 4: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Type 2020 & 2033

- Table 22: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Type 2020 & 2033

- Table 58: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Type 2020 & 2033

- Table 76: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Pharma Grade Pet Pvdc Film Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Pharma Grade Pet Pvdc Film Volume K Forecast, by Country 2020 & 2033

- Table 79: China Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Pharma Grade Pet Pvdc Film Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Pharma Grade Pet Pvdc Film Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pharma Grade Pet Pvdc Film?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Pharma Grade Pet Pvdc Film?

Key companies in the market include Syensqo, Jiangxi Chunguang New Material Technology, Hangzhou Plastics Industry, Jiangsu Fuxin Huakang Packaging Material.

3. What are the main segments of the Pharma Grade Pet Pvdc Film?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pharma Grade Pet Pvdc Film," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pharma Grade Pet Pvdc Film report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pharma Grade Pet Pvdc Film?

To stay informed about further developments, trends, and reports in the Pharma Grade Pet Pvdc Film, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence