Key Insights

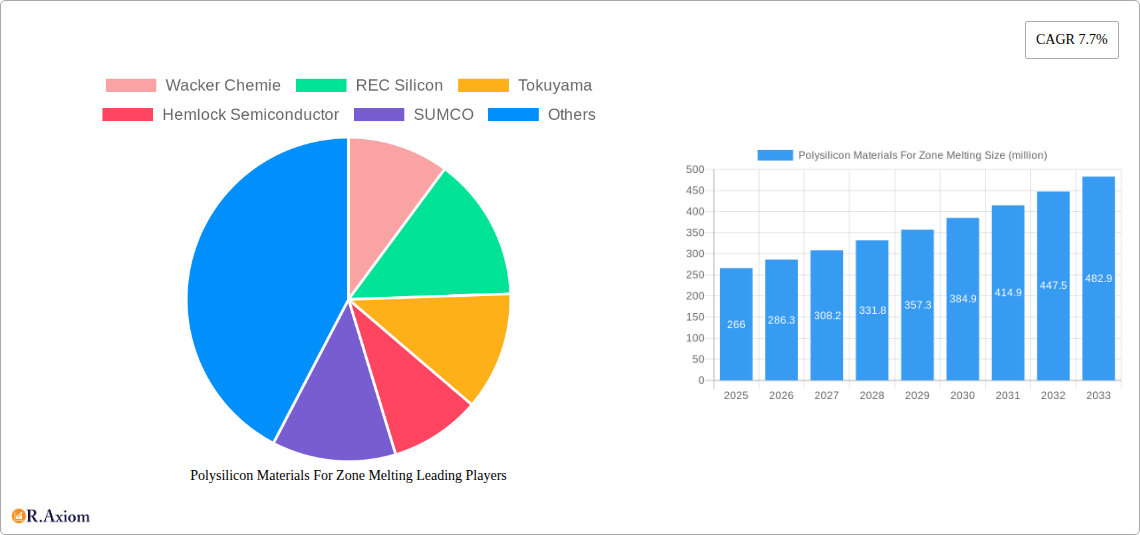

The global market for Polysilicon Materials for Zone Melting is poised for significant expansion, projected to reach approximately \$266 million in 2025 with a robust Compound Annual Growth Rate (CAGR) of 7.7% through 2033. This impressive growth trajectory is primarily fueled by the escalating demand across critical sectors, most notably in the production of high-purity polysilicon essential for advanced power semiconductors and cutting-edge communications and RF applications. The increasing sophistication of electronic devices, coupled with the global push towards renewable energy solutions that rely heavily on efficient solar cells, underscores the foundational role of zone-melted polysilicon. Furthermore, the stringent purity requirements of the aerospace industry for specialized components will continue to be a substantial market driver. Emerging economies and technological advancements in semiconductor manufacturing processes are expected to further accelerate market penetration and adoption of these high-grade materials.

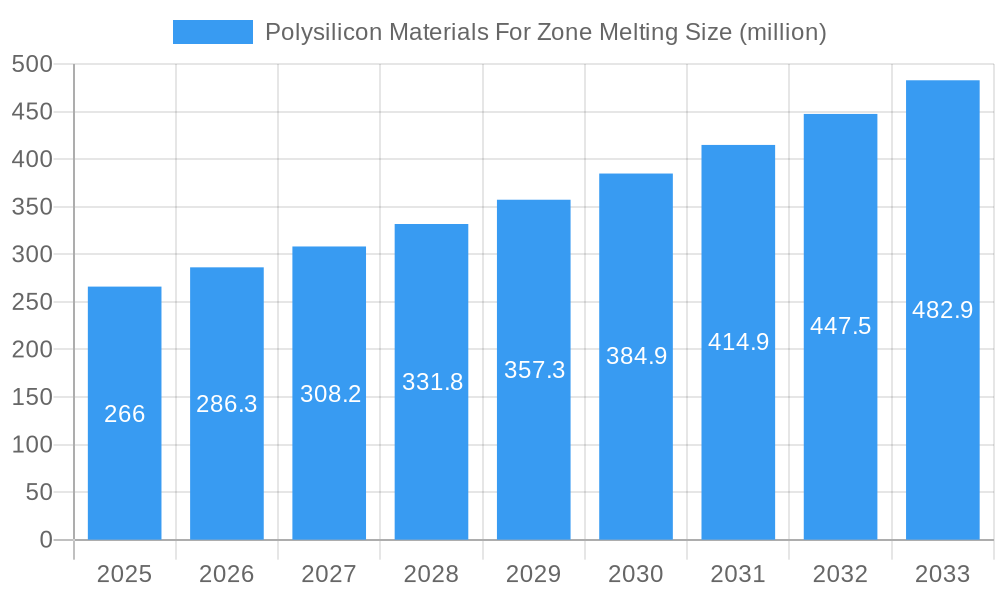

Polysilicon Materials For Zone Melting Market Size (In Million)

Despite the favorable growth outlook, the market faces certain headwinds. The primary restraint stems from the energy-intensive nature of the zone melting process, which contributes to higher production costs and environmental concerns, potentially impacting price competitiveness and sustainability initiatives. Fluctuations in raw material prices and the availability of essential feedstocks can also introduce volatility. However, ongoing research and development into more energy-efficient purification techniques and the exploration of alternative production methods are actively being pursued by key industry players. The market segmentation, with a focus on types like 11N, 12N, and 13N polysilicon, highlights a clear trend towards higher purity grades driven by performance demands in specialized applications. Geographically, the Asia Pacific region, particularly China and Japan, is expected to dominate both production and consumption due to its strong presence in semiconductor manufacturing and its leading role in solar energy deployment.

Polysilicon Materials For Zone Melting Company Market Share

This in-depth market research report provides a detailed analysis of the Polysilicon Materials for Zone Melting sector, covering historical performance, current trends, and future projections from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this report offers crucial insights for industry stakeholders seeking to navigate the evolving landscape of high-purity polysilicon production. We delve into market concentration, innovation drivers, regulatory influences, dominant segments, product developments, and strategic outlooks, equipping businesses with actionable intelligence to capitalize on growth opportunities and mitigate potential challenges in this critical materials market.

Polysilicon Materials For Zone Melting Market Concentration & Innovation

The Polysilicon Materials for Zone Melting market exhibits a moderate concentration, with key players such as Wacker Chemie, REC Silicon, Tokuyama, Hemlock Semiconductor, SUMCO, and OCI holding significant market share. In 2025, the estimated market share for these leading entities is projected to be over 70%. Innovation in this sector is primarily driven by the relentless demand for higher purity polysilicon, crucial for advanced semiconductor manufacturing, particularly for power semiconductors and the burgeoning communications and RF sectors. Advancements in the zone melting process itself, aiming for increased efficiency and reduced energy consumption, are also key innovation drivers. Regulatory frameworks, particularly those pertaining to environmental impact and material sourcing, are increasingly influencing production methods and market entry barriers. Product substitutes, while limited for ultra-high purity requirements, are being explored in emerging technologies. End-user trends are strongly influenced by the growth in electric vehicles, renewable energy infrastructure (solar panels), and high-speed telecommunications, all demanding superior silicon material properties. Mergers and acquisition (M&A) activities, while not as frequent as in some other industries, are strategically focused on consolidating production capabilities and securing supply chains. For instance, estimated M&A deal values in the semiconductor materials sector have reached several hundred million dollars in recent years, signaling consolidation efforts. The report further explores the interplay of these factors in shaping the market's competitive dynamics.

Polysilicon Materials For Zone Melting Industry Trends & Insights

The Polysilicon Materials for Zone Melting industry is poised for significant expansion driven by a confluence of powerful trends and technological advancements. The projected Compound Annual Growth Rate (CAGR) for the forecast period 2025–2033 is estimated to be between 6% and 8%, reflecting the escalating demand from diverse high-tech applications. A primary growth driver is the insatiable appetite for polysilicon of exceptional purity, exceeding 11N, 12N, and even reaching 13N levels, necessary for the production of advanced power semiconductors that are critical for the electrification of transportation, industrial automation, and the integration of renewable energy sources into the grid. These advanced semiconductors enable higher efficiency, faster switching speeds, and improved thermal management in electronic devices.

Technological disruptions are continuously reshaping production methodologies. While the Siemens process remains a cornerstone for producing metallurgical-grade silicon, zone melting is the proprietary technique for achieving the ultra-high purity required for semiconductor wafers. Ongoing research focuses on enhancing the efficiency of the zone melting process, reducing energy consumption, and minimizing waste byproducts. Innovations in crucible materials and furnace designs are also contributing to improved material quality and cost-effectiveness.

Consumer preferences, indirectly influencing this B2B market, are increasingly leaning towards energy-efficient devices, electric vehicles, and advanced communication technologies. This translates into a higher demand for the high-performance components that rely on zone-melted polysilicon. For example, the widespread adoption of electric vehicles is directly fueling the demand for efficient power semiconductor modules, which in turn necessitates the use of high-purity polysilicon.

Competitive dynamics are characterized by intense R&D investments and a focus on securing reliable and cost-competitive production. Companies are investing heavily in expanding their production capacities to meet the anticipated surge in demand. Market penetration is steadily increasing across key application segments. The global market for polysilicon materials for zone melting, estimated at approximately 200 million dollars in 2025, is projected to grow substantially. The report also delves into the evolving geopolitical landscape and its impact on supply chain resilience, as well as the growing importance of sustainable manufacturing practices in the silicon industry.

Dominant Markets & Segments in Polysilicon Materials For Zone Melting

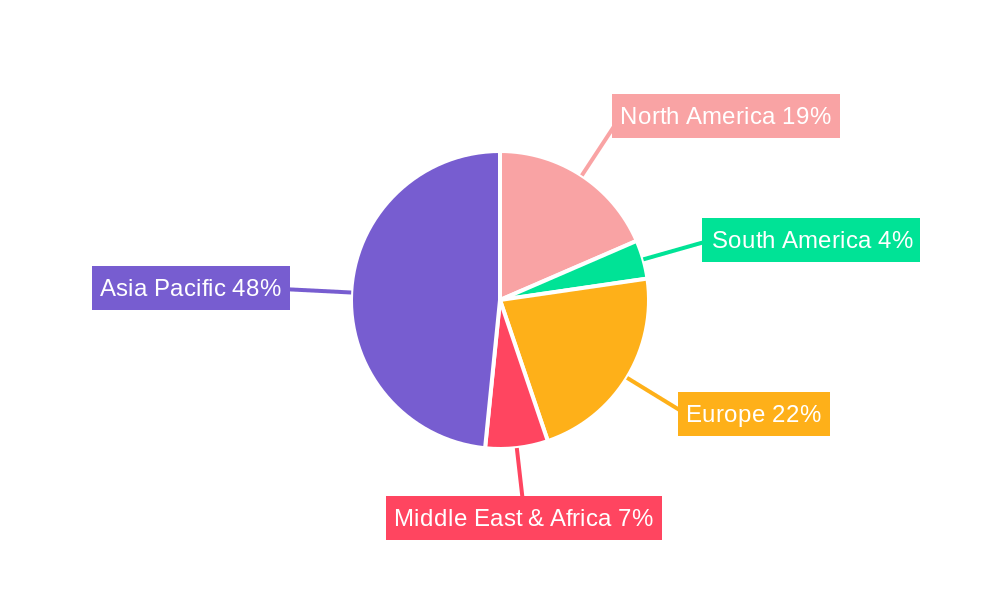

The Polysilicon Materials for Zone Melting market is experiencing robust growth across various applications and purity types. The leading region for consumption and production is Asia-Pacific, driven by the significant presence of semiconductor manufacturing hubs in countries like China, South Korea, Taiwan, and Japan.

Leading Region: Asia-Pacific

- Key Drivers: The dominance of Asia-Pacific is attributed to several factors, including:

- Robust Semiconductor Manufacturing Ecosystem: The region hosts the majority of the world's wafer fabrication plants and semiconductor assembly facilities.

- Government Support and Investments: Numerous governments in Asia-Pacific are actively promoting the semiconductor industry through favorable policies, subsidies, and R&D initiatives, leading to substantial investments in silicon material production and consumption.

- Growing Demand for Consumer Electronics and EVs: The region is a massive consumer of electronic devices and a rapidly growing market for electric vehicles, both of which are major end-users of polysilicon-based semiconductors.

- Infrastructure Development: Significant investments in renewable energy infrastructure, such as solar power plants, also contribute to the demand for polysilicon, although this report focuses on zone-melted polysilicon for higher-tier applications.

Dominant Application Segment: Power Semiconductors

- Market Drivers: The Power Semiconductors segment is the primary driver of demand for zone-melted polysilicon due to its critical role in:

- Electric Vehicles (EVs): The burgeoning EV market requires high-performance power modules (IGBTs, MOSFETs) for inverters, converters, and battery management systems. These components demand polysilicon with purity levels of 12N and above for optimal efficiency and reliability.

- Renewable Energy Systems: Efficient power conversion and grid management in solar inverters and wind turbine systems rely heavily on advanced power semiconductors made from high-purity polysilicon.

- Industrial Automation and Power Management: The increasing demand for energy efficiency in industrial processes and the proliferation of smart grids further elevate the need for high-quality power semiconductor devices.

- Consumer Electronics: While not the largest driver for zone-melted polysilicon compared to other segments, the demand for energy-efficient power supplies in high-end consumer electronics still contributes.

Dominant Purity Type: 12N and 13N Polysilicon

- Market Drivers: The trend towards higher purity polysilicon is a direct consequence of advancements in semiconductor technology:

- Shrinking Transistor Sizes: As semiconductor devices become smaller and more complex, even minute impurities can significantly degrade performance and reliability. Purity levels of 12N and 13N are essential for fabricating next-generation microchips.

- High-Frequency and High-Power Applications: Communications and RF applications, as well as advanced power devices, demand materials with exceptionally low defect densities and precise electrical characteristics, achievable only with ultra-high purity polysilicon.

- Reduced Leakage Currents and Improved Yield: Higher purity polysilicon minimizes leakage currents and improves wafer yield during the complex fabrication process, leading to more cost-effective and reliable end products. The market for 11N polysilicon remains substantial for less demanding applications, but the growth in 12N and 13N segments is projected to outpace it significantly.

Other Significant Segments

- Communications and RF: This segment is a growing contributor, fueled by the deployment of 5G networks, advanced wireless communication devices, and high-frequency integrated circuits. The need for low-loss, high-performance components in these applications necessitates the use of 12N and 13N purity polysilicon.

- Aerospace: While a niche market, the aerospace industry's stringent requirements for reliability and performance in critical systems (e.g., satellite electronics, avionics) also contribute to the demand for ultra-high purity polysilicon.

Polysilicon Materials For Zone Melting Product Developments

Recent product developments in polysilicon materials for zone melting are characterized by an aggressive push towards achieving and sustaining purity levels of 12N and 13N. Companies are focusing on enhancing the efficiency and yield of the zone melting process, leading to more cost-effective ultra-high purity silicon. Innovations in crucible materials and furnace designs aim to minimize contamination and improve crystal quality. These advancements directly benefit the power semiconductor and communications and RF sectors by enabling the production of more efficient, reliable, and high-performance electronic components. The competitive advantage lies in the ability to consistently deliver these higher purity grades at competitive price points, meeting the stringent demands of advanced semiconductor fabrication.

Report Scope & Segmentation Analysis

This report meticulously segments the Polysilicon Materials for Zone Melting market across key application areas and purity types. The Application segmentation includes:

- Power Semiconductors: This segment is projected to witness the highest growth, driven by electric vehicles and renewable energy. Estimated market size in 2025 is around 100 million dollars, with a forecast CAGR of approximately 9%.

- Communications and RF: Experiencing robust expansion due to 5G deployment, this segment is estimated at 40 million dollars in 2025, with a projected CAGR of 7%.

- Aerospace: A smaller but critical segment, this is estimated at 10 million dollars in 2025, with a steady CAGR of 5%.

- Other: Encompassing miscellaneous applications, this segment is estimated at 50 million dollars in 2025, with a CAGR of 6%.

The Type segmentation analyzes demand based on purity levels:

- 11N Polysilicon: While foundational, its growth is expected to be slower compared to higher grades, with an estimated market size of 60 million dollars in 2025 and a CAGR of 5%.

- 12N Polysilicon: A significant growth driver, estimated at 90 million dollars in 2025, with a projected CAGR of 8%.

- 13N Polysilicon: The fastest-growing segment, driven by cutting-edge applications, estimated at 50 million dollars in 2025, with a CAGR of 10%.

Key Drivers of Polysilicon Materials For Zone Melting Growth

The growth of the Polysilicon Materials for Zone Melting market is underpinned by several pivotal factors. Technologically, the relentless miniaturization and performance enhancement demands in the semiconductor industry are driving the need for higher purity silicon. Economically, the exponential growth in electric vehicles, renewable energy installations, and advanced communication infrastructure creates a substantial and expanding market for polysilicon-based components. Regulatory drivers include government initiatives supporting domestic semiconductor manufacturing and the push for energy efficiency standards, which indirectly boost demand for high-performance silicon. For instance, government incentives for EV adoption in major economies directly translate to increased demand for silicon carbide (SiC) and advanced power semiconductor components, thus driving polysilicon demand.

Challenges in the Polysilicon Materials For Zone Melting Sector

Despite its promising growth trajectory, the Polysilicon Materials for Zone Melting sector faces significant challenges. Regulatory hurdles, particularly those related to stringent environmental compliance and waste disposal in high-purity silicon production, can increase operational costs and slow down expansion. Supply chain vulnerabilities, exacerbated by geopolitical tensions and the concentration of raw material sources, pose a risk to consistent production. Competitive pressures from established players and the high capital expenditure required for setting up and maintaining ultra-high purity polysilicon production facilities act as barriers to entry for new competitors. Furthermore, the energy-intensive nature of the zone melting process presents challenges related to rising energy costs and the need for sustainable energy solutions, estimated to contribute to operational cost increases of up to 15% in regions with volatile energy prices.

Emerging Opportunities in Polysilicon Materials For Zone Melting

Emerging opportunities in the Polysilicon Materials for Zone Melting sector are abundant and diverse. The accelerating adoption of electric vehicles presents a colossal opportunity for polysilicon suppliers, as advanced power semiconductors are essential for their operation. The ongoing build-out of 5G infrastructure globally is creating a sustained demand for high-performance communication chips that rely on ultra-high purity silicon. Furthermore, the increasing focus on energy efficiency and sustainability is driving innovation in power management solutions, opening new avenues for polysilicon applications. The development of novel semiconductor devices and advanced packaging technologies also presents opportunities for customized ultra-high purity silicon materials. The growing demand for silicon in emerging markets like India and Southeast Asia, as they ramp up their domestic semiconductor manufacturing capabilities, is another significant emerging opportunity, projected to add an additional 100 million dollars in market value by 2030.

Leading Players in the Polysilicon Materials For Zone Melting Market

- Wacker Chemie

- REC Silicon

- Tokuyama

- Hemlock Semiconductor

- SUMCO

- OCI

- Henan Silane Technology Development

- Shaanxi Non-Ferrous Tian Hong REC Silicon Materials

- Sinosico

- GCL-Poly Energy

- Huanghe Hydropower Development

- Jiangsu Xinhua Semiconductor Materials Technology

Key Developments in Polysilicon Materials For Zone Melting Industry

- 2023/Ongoing: Increased investment in expanding polysilicon production capacity globally, particularly by Chinese manufacturers, to meet surging demand.

- 2023/Q4: Advancements in energy-efficient zone melting technologies reported by leading R&D institutions, aiming to reduce operational costs.

- 2022/Q3: Strategic partnerships formed between polysilicon producers and semiconductor manufacturers to secure long-term supply agreements for 12N and 13N purity silicon.

- 2021/Q2: Announcement of new plant constructions focused on ultra-high purity polysilicon production by several key players to cater to the growing EV market demand.

- 2020/Q1: Increased M&A activity and joint ventures aimed at consolidating market share and acquiring advanced production technologies.

Strategic Outlook for Polysilicon Materials For Zone Melting Market

The strategic outlook for the Polysilicon Materials for Zone Melting market remains exceptionally positive, characterized by sustained high growth driven by fundamental technological shifts and escalating demand across critical sectors. The ongoing electrification of transportation, the global rollout of 5G networks, and the continuous drive for energy efficiency in industrial and consumer applications are foundational catalysts that will propel market expansion. Companies that can effectively navigate supply chain complexities, invest in cutting-edge R&D for even higher purity levels (e.g., 14N), and optimize their production processes for cost-effectiveness and sustainability will be best positioned for success. The strategic imperative will be to ensure a reliable and scalable supply of ultra-high purity polysilicon to meet the burgeoning needs of the advanced semiconductor industry, offering significant growth potential in the coming decade.

Polysilicon Materials For Zone Melting Segmentation

-

1. Application

- 1.1. Power Semiconductors

- 1.2. Communications and RF

- 1.3. Aerospace

- 1.4. Other

-

2. Type

- 2.1. 11N

- 2.2. 12N

- 2.3. 13N

Polysilicon Materials For Zone Melting Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Polysilicon Materials For Zone Melting Regional Market Share

Geographic Coverage of Polysilicon Materials For Zone Melting

Polysilicon Materials For Zone Melting REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Power Semiconductors

- 5.1.2. Communications and RF

- 5.1.3. Aerospace

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 11N

- 5.2.2. 12N

- 5.2.3. 13N

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Polysilicon Materials For Zone Melting Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Power Semiconductors

- 6.1.2. Communications and RF

- 6.1.3. Aerospace

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 11N

- 6.2.2. 12N

- 6.2.3. 13N

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Polysilicon Materials For Zone Melting Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Power Semiconductors

- 7.1.2. Communications and RF

- 7.1.3. Aerospace

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 11N

- 7.2.2. 12N

- 7.2.3. 13N

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Polysilicon Materials For Zone Melting Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Power Semiconductors

- 8.1.2. Communications and RF

- 8.1.3. Aerospace

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 11N

- 8.2.2. 12N

- 8.2.3. 13N

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Polysilicon Materials For Zone Melting Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Power Semiconductors

- 9.1.2. Communications and RF

- 9.1.3. Aerospace

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 11N

- 9.2.2. 12N

- 9.2.3. 13N

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Polysilicon Materials For Zone Melting Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Power Semiconductors

- 10.1.2. Communications and RF

- 10.1.3. Aerospace

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 11N

- 10.2.2. 12N

- 10.2.3. 13N

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Polysilicon Materials For Zone Melting Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Power Semiconductors

- 11.1.2. Communications and RF

- 11.1.3. Aerospace

- 11.1.4. Other

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. 11N

- 11.2.2. 12N

- 11.2.3. 13N

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Wacker Chemie

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 REC Silicon

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tokuyama

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hemlock Semiconductor

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SUMCO

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 OCI

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Henan Silane Technology Development

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Shaanxi Non-Ferrous Tian Hong REC Silicon Materials

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sinosico

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 GCL-Poly Energy

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Huanghe Hydropower Development

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Jiangsu Xinhua Semiconductor Materials Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Wacker Chemie

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Polysilicon Materials For Zone Melting Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Polysilicon Materials For Zone Melting Revenue (million), by Application 2025 & 2033

- Figure 3: North America Polysilicon Materials For Zone Melting Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Polysilicon Materials For Zone Melting Revenue (million), by Type 2025 & 2033

- Figure 5: North America Polysilicon Materials For Zone Melting Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Polysilicon Materials For Zone Melting Revenue (million), by Country 2025 & 2033

- Figure 7: North America Polysilicon Materials For Zone Melting Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Polysilicon Materials For Zone Melting Revenue (million), by Application 2025 & 2033

- Figure 9: South America Polysilicon Materials For Zone Melting Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Polysilicon Materials For Zone Melting Revenue (million), by Type 2025 & 2033

- Figure 11: South America Polysilicon Materials For Zone Melting Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Polysilicon Materials For Zone Melting Revenue (million), by Country 2025 & 2033

- Figure 13: South America Polysilicon Materials For Zone Melting Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Polysilicon Materials For Zone Melting Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Polysilicon Materials For Zone Melting Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Polysilicon Materials For Zone Melting Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Polysilicon Materials For Zone Melting Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Polysilicon Materials For Zone Melting Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Polysilicon Materials For Zone Melting Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Polysilicon Materials For Zone Melting Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Polysilicon Materials For Zone Melting Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Polysilicon Materials For Zone Melting Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Polysilicon Materials For Zone Melting Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Polysilicon Materials For Zone Melting Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Polysilicon Materials For Zone Melting Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Polysilicon Materials For Zone Melting Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Polysilicon Materials For Zone Melting Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Polysilicon Materials For Zone Melting Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Polysilicon Materials For Zone Melting Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Polysilicon Materials For Zone Melting Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Polysilicon Materials For Zone Melting Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Polysilicon Materials For Zone Melting Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Polysilicon Materials For Zone Melting Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polysilicon Materials For Zone Melting?

The projected CAGR is approximately 7.7%.

2. Which companies are prominent players in the Polysilicon Materials For Zone Melting?

Key companies in the market include Wacker Chemie, REC Silicon, Tokuyama, Hemlock Semiconductor, SUMCO, OCI, Henan Silane Technology Development, Shaanxi Non-Ferrous Tian Hong REC Silicon Materials, Sinosico, GCL-Poly Energy, Huanghe Hydropower Development, Jiangsu Xinhua Semiconductor Materials Technology.

3. What are the main segments of the Polysilicon Materials For Zone Melting?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 266 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Polysilicon Materials For Zone Melting," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Polysilicon Materials For Zone Melting report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Polysilicon Materials For Zone Melting?

To stay informed about further developments, trends, and reports in the Polysilicon Materials For Zone Melting, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence