Key Insights

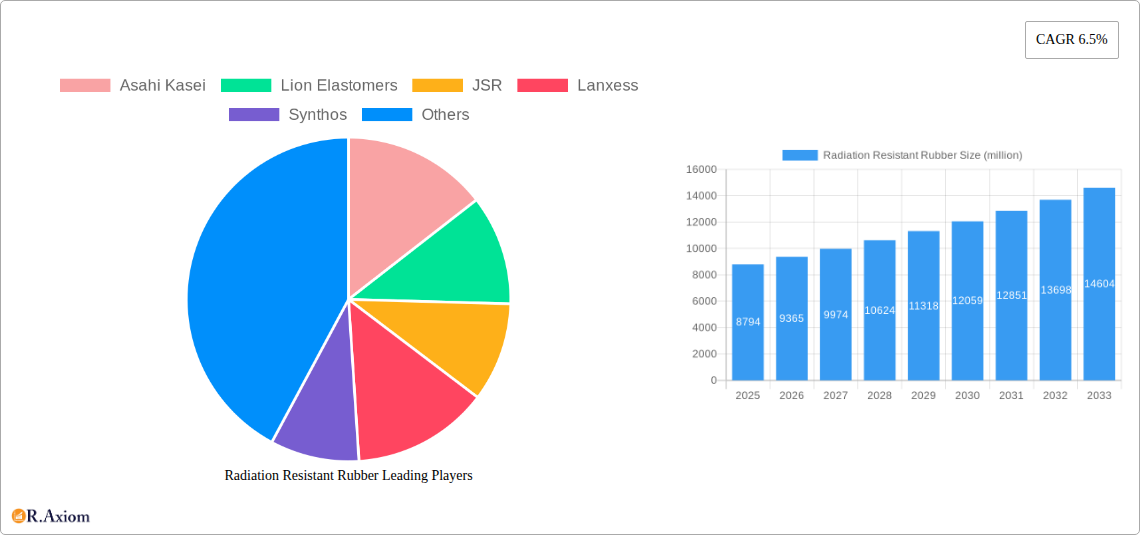

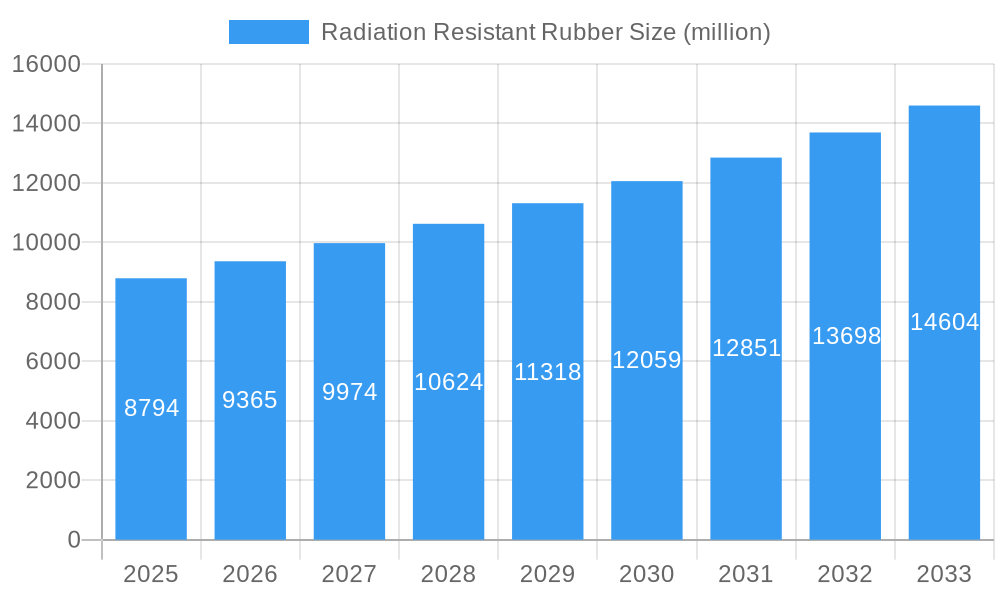

The global Radiation Resistant Rubber market is poised for robust expansion, projected to reach a significant valuation by 2033. Currently valued at approximately $8,794 million in 2025, the market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% throughout the forecast period. This growth is primarily fueled by the increasing demand from critical sectors that require materials capable of withstanding intense radiation environments. The aerospace industry, with its stringent safety regulations and the need for durable components in space exploration and aircraft manufacturing, stands as a major driver. Similarly, the nuclear industry's continuous need for specialized seals, gaskets, and protective coatings that can endure high levels of ionizing radiation is a significant growth catalyst. Furthermore, the medical sector's reliance on radiation-resistant materials for equipment used in radiotherapy and imaging is contributing to the market's upward trajectory. Emerging applications in advanced scientific research and industrial processes involving radioactive materials are also expected to bolster demand.

Radiation Resistant Rubber Market Size (In Billion)

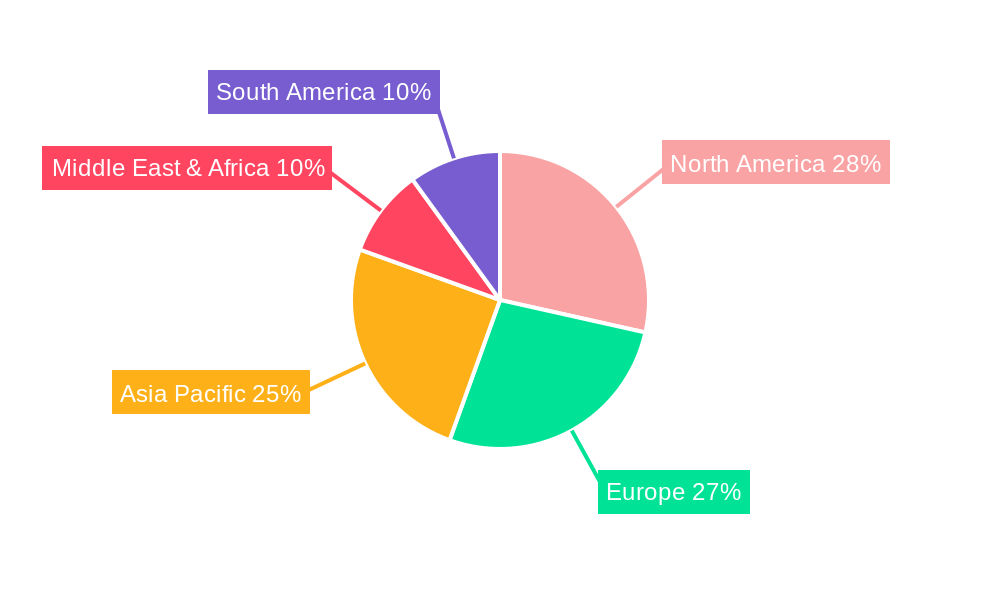

The market's segmentation highlights diverse application and material preferences. In terms of application, the strong performance of the aerospace, medical, and nuclear industries is evident. On the material front, Nitrile Rubber, Fluororubber, and Silicone Rubber are anticipated to dominate, owing to their inherent properties such as chemical resistance, thermal stability, and, crucially, their effectiveness in mitigating radiation damage. EPDM rubber and other specialized elastomers also play a vital role in niche applications. Geographically, North America and Europe currently hold significant market share, driven by their established industrial bases and extensive research and development activities. However, the Asia Pacific region is projected to exhibit the fastest growth, propelled by rapid industrialization, expanding nuclear power programs, and increasing investments in the aerospace and healthcare sectors in countries like China and India. The market's trajectory suggests a strong and sustained demand for advanced radiation-resistant rubber solutions across a wide spectrum of critical industries.

Radiation Resistant Rubber Company Market Share

This in-depth report provides a detailed analysis of the global Radiation Resistant Rubber market, covering the historical period from 2019 to 2024, the base year of 2025, and a forecast period extending to 2033. We explore market dynamics, key players, emerging trends, and growth opportunities within this critical sector. The report utilizes high-traffic keywords such as "radiation shielding materials," "high-performance elastomers," "nuclear safety components," "aerospace seals," and "medical device materials" to ensure maximum search engine visibility and engagement for industry stakeholders.

Radiation Resistant Rubber Market Concentration & Innovation

The Radiation Resistant Rubber market exhibits a moderate to high concentration, with a significant portion of market share held by a few key global players. The innovation landscape is driven by the relentless demand for enhanced radiation protection across diverse high-stakes applications. Key innovation drivers include the development of novel polymer formulations with superior resistance to gamma, neutron, and electron radiation, improved thermal stability, and extended operational lifespans in extreme environments. Regulatory frameworks, particularly in the nuclear and aerospace sectors, are stringent, mandating extensive testing and certification, thereby influencing product development and market entry. Product substitutes, such as lead shielding and specialized plastics, exist but often fall short in terms of flexibility, weight, or cost-effectiveness for specific applications. End-user trends are increasingly focused on miniaturization of components, lightweight materials, and enhanced safety protocols. Mergers and acquisitions (M&A) activity has been observed as companies seek to expand their product portfolios and geographical reach. For instance, a recent M&A deal in the specialty chemicals sector, valued at approximately $500 million, aimed to consolidate expertise in high-performance elastomer development.

- Market Share: Leading players collectively hold an estimated 70% of the global market share.

- M&A Deal Value: Average M&A deal values are estimated to be between $50 million and $750 million.

- Innovation Focus: Development of advanced cross-linking technologies, nanoparticle integration for enhanced shielding, and eco-friendly manufacturing processes.

- Regulatory Impact: Strict adherence to standards like ASTM D4099 and ISO 19200 is crucial for market access.

Radiation Resistant Rubber Industry Trends & Insights

The Radiation Resistant Rubber industry is poised for significant growth, projected at a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period. This expansion is fueled by a confluence of technological advancements, increasing global energy demands, and the growing adoption of radiation-emitting technologies in various sectors. The escalating need for robust radiation shielding in nuclear power plants, research facilities, and medical imaging equipment represents a primary market driver. Furthermore, the aerospace industry's continuous pursuit of lighter yet highly durable materials for spacecraft and aircraft components exposed to cosmic radiation is creating substantial demand. Technological disruptions, such as advancements in polymer synthesis and compounding techniques, are enabling the creation of radiation-resistant rubbers with tailored properties, including improved mechanical strength, chemical resistance, and sealing capabilities at elevated temperatures. Consumer preferences are leaning towards enhanced safety, reliability, and longer product lifecycles, pushing manufacturers to develop high-performance materials that meet these stringent requirements. Competitive dynamics are characterized by a blend of established global manufacturers and niche players specializing in custom formulations. Market penetration is deepening in emerging economies as their infrastructure development and technological adoption accelerate.

- CAGR: Estimated at 6.5% for the forecast period 2025–2033.

- Market Penetration: Growing in regions with developing nuclear power programs and advanced medical infrastructure.

- Technological Advancements: Focus on fluorinated polymers, silicone elastomers, and nitrile rubber compounds for enhanced radiation degradation resistance.

- Economic Factors: Global investment in nuclear energy and space exploration programs are key economic catalysts.

Dominant Markets & Segments in Radiation Resistant Rubber

The global Radiation Resistant Rubber market is segmented by application and type, with specific regions and segments demonstrating pronounced dominance. Geographically, North America and Europe currently dominate the market, driven by their well-established nuclear industries, advanced aerospace sectors, and sophisticated healthcare systems. Asia-Pacific is emerging as a rapidly growing region, propelled by substantial investments in nuclear power expansion and increasing adoption of advanced medical technologies in countries like China and India.

Within applications, the Nuclear Industry is the largest and most dominant segment, accounting for an estimated 45% of the market revenue. This is attributed to the critical need for reliable sealing, gasketing, and protective components in reactors, spent fuel storage, and waste management facilities. Radiation-resistant rubbers are essential for maintaining containment integrity and ensuring the safety of personnel and the environment.

The Aerospace segment, holding approximately 30% of the market share, is another significant driver. Components such as O-rings, seals, and coatings for spacecraft, satellites, and high-altitude aircraft require materials that can withstand prolonged exposure to cosmic and solar radiation, as well as extreme temperature fluctuations.

The Medical segment, representing about 25% of the market, is experiencing robust growth due to the increasing use of radiation in diagnostics and therapeutics. Radiation-resistant rubbers are crucial for manufacturing components of X-ray machines, CT scanners, linear accelerators, and implantable medical devices, where material integrity and safety are paramount.

In terms of rubber types, Fluororubber (FKM) dominates due to its exceptional resistance to high temperatures, chemicals, and various forms of radiation, making it ideal for demanding applications in the nuclear and aerospace industries. Nitrile Rubber (NBR), often enhanced with specific additives, is widely used for its good mechanical properties and cost-effectiveness in less extreme radiation environments. Silicone Rubber offers excellent flexibility across a wide temperature range and good radiation resistance, finding applications in medical devices and specialized sealing. EPDM Rubber is utilized for its weatherability and ozone resistance, with specific grades offering improved radiation resilience for outdoor nuclear infrastructure.

- Dominant Region: North America and Europe, with Asia-Pacific showing rapid growth.

- Dominant Application: Nuclear Industry (estimated 45% market share).

- Key Drivers in Nuclear Industry: Reactor safety regulations, spent fuel management, and fusion research initiatives.

- Key Drivers in Aerospace: Increased satellite launches, manned space missions, and development of new aircraft technologies.

- Key Drivers in Medical: Advancements in radiotherapy, diagnostic imaging, and the need for biocompatible radiation shielding.

- Dominant Type: Fluororubber (FKM).

- Emerging Type: Advanced composites incorporating radiation-resistant elastomers.

Radiation Resistant Rubber Product Developments

Recent product developments in the Radiation Resistant Rubber market focus on enhancing performance characteristics and expanding application suitability. Innovations include the formulation of advanced fluoropolymers and silicone elastomers with superior resistance to ionizing radiation, achieving extended service life in high-dose environments. Companies are also developing novel additive packages, such as specialized nanoparticles and ceramic fillers, to boost the radiation attenuation properties of existing rubber compounds. These developments are critical for meeting the increasing safety standards in nuclear power, enabling longer-duration space missions, and ensuring the reliability of sophisticated medical equipment. Competitive advantages are being gained through materials that offer improved mechanical strength, thermal stability, and chemical inertness alongside their radiation resistance.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Radiation Resistant Rubber market across key segmentations, providing detailed insights into each category.

Application Segmentation:

- Aerospace: This segment encompasses seals, gaskets, and protective components for satellites, spacecraft, and aircraft. Projected market size is estimated to reach $1.5 billion by 2033, with a CAGR of 6.0%. Competitive dynamics involve high-performance material providers like DuPont and 3M.

- Medical: Includes materials for diagnostic and therapeutic equipment, as well as implantable devices. The market size is estimated at $1.2 billion by 2033, with a CAGR of 7.0%. Key players include JSR and LG Chem, focusing on biocompatibility and precise radiation shielding.

- Nuclear Industry: This segment covers components for nuclear power plants, research reactors, and waste management. It is the largest segment, projected at $2.2 billion by 2033, with a CAGR of 6.2%. Companies like Asahi Kasei and Solvay are major contributors, emphasizing extreme durability and safety.

Type Segmentation:

- Nitrile Rubber: Known for its oil and fuel resistance, modified grades offer moderate radiation resistance. Market size estimated at $0.8 billion by 2033, CAGR of 5.5%.

- Fluororubber: Offers excellent resistance to heat, chemicals, and radiation. Market size estimated at $1.8 billion by 2033, CAGR of 6.8%.

- Silicone Rubber: Provides flexibility and high-temperature resistance with good radiation resilience. Market size estimated at $1.0 billion by 2033, CAGR of 6.5%.

- EPDM Rubber: Known for its weatherability, specific grades are developed for radiation resistance. Market size estimated at $0.5 billion by 2033, CAGR of 5.8%.

- Others: Includes specialized elastomers and composite materials tailored for specific radiation environments. Market size estimated at $0.3 billion by 2033, CAGR of 7.2%.

Key Drivers of Radiation Resistant Rubber Growth

The growth of the Radiation Resistant Rubber market is primarily propelled by several interconnected factors. The escalating global demand for clean energy, with a continued reliance on nuclear power, necessitates robust safety components and shielding materials. Advancements in medical imaging and radiotherapy technologies, requiring more precise and reliable radiation management, also contribute significantly. The burgeoning aerospace sector, with an increasing number of satellite launches and ambitious space exploration initiatives, demands materials that can withstand extreme radiation environments. Furthermore, stringent safety regulations across these industries are mandating the use of high-performance radiation-resistant materials, driving innovation and market expansion. Technological progress in polymer science is enabling the development of more effective and cost-efficient radiation shielding solutions.

Challenges in the Radiation Resistant Rubber Sector

Despite the promising growth trajectory, the Radiation Resistant Rubber sector faces several challenges. The stringent regulatory landscape for nuclear and aerospace applications can lead to lengthy approval processes and high compliance costs, acting as a barrier to market entry for new players. Supply chain complexities for specialized raw materials, particularly for high-performance polymers like fluororubbers, can lead to price volatility and availability issues. The high cost of R&D and specialized manufacturing processes for radiation-resistant elastomers can also impact market affordability for certain applications. Moreover, the development of more efficient and cost-effective radiation shielding alternatives, such as advanced composites or specialized shielding metals, presents a competitive pressure. Ensuring consistent product quality and long-term performance in highly demanding radiation environments remains a critical technical challenge.

Emerging Opportunities in Radiation Resistant Rubber

Emerging opportunities in the Radiation Resistant Rubber market are diverse and promising. The development of new nuclear reactor designs, including advanced small modular reactors (SMRs) and fusion reactors, will create demand for novel radiation-resistant materials with enhanced performance characteristics. The growing space economy, with private sector involvement in satellite constellations and lunar missions, presents a significant opportunity for lightweight and highly durable radiation shielding. In the medical field, the increasing sophistication of proton therapy and other advanced radiation treatments will require specialized elastomers for precision delivery systems. Furthermore, the development of radiation-resistant rubbers for industrial applications, such as in particle accelerators for research and industrial processing, and for protecting sensitive electronic components in high-radiation environments, offers substantial untapped potential. Sustainability initiatives are also driving opportunities for eco-friendly radiation-resistant rubber formulations.

Leading Players in the Radiation Resistant Rubber Market

- Asahi Kasei

- Lion Elastomers

- JSR

- Lanxess

- Synthos

- Goodyear

- Michelin

- LG Chem

- DuPont

- 3M

- Solvay

- ExxonMobil

- SK Chemical

- Sumitomo

- James Walker

- Borflex

- Hayakawa Rubber

- TRP Polymer Solutions

- REONTECH

- Hutchinson

- Xi'an Sunward Aeromat Co.,Ltd

- SEEFAR

Key Developments in Radiation Resistant Rubber Industry

- 2023: Launch of a new generation of fluororubber compounds with enhanced neutron shielding capabilities for next-generation nuclear reactors.

- 2022: Significant investment by a major aerospace materials supplier in R&D for radiation-resistant silicone elastomers for satellite applications.

- 2021: A leading medical device manufacturer partnered with a specialty chemical company to develop custom radiation-resistant seals for advanced radiotherapy equipment.

- 2020: Introduction of novel EPDM rubber formulations with improved UV and radiation resistance for outdoor nuclear infrastructure.

- 2019: Acquisition of a niche radiation shielding materials company by a global chemical conglomerate to expand its specialty elastomer portfolio.

Strategic Outlook for Radiation Resistant Rubber Market

The strategic outlook for the Radiation Resistant Rubber market is overwhelmingly positive, driven by persistent demand from critical sectors such as nuclear energy, aerospace, and healthcare. Future growth will be shaped by continuous innovation in material science, focusing on enhanced radiation attenuation properties, improved thermal and chemical resistance, and extended operational lifespans. Strategic collaborations between material manufacturers and end-users will be crucial for developing tailored solutions that meet evolving industry requirements and stringent regulatory standards. The market's expansion into emerging economies, coupled with the increasing adoption of advanced technologies, presents significant untapped potential. Companies that can offer cost-effective, high-performance, and sustainable radiation-resistant rubber solutions are well-positioned for sustained success in this vital and growing industry.

Radiation Resistant Rubber Segmentation

-

1. Application

- 1.1. Aerospace

- 1.2. Medical

- 1.3. Nuclear Industry

-

2. Type

- 2.1. Nitrile Rubber

- 2.2. Fluororubber

- 2.3. Silicone Rubber

- 2.4. EPDM Rubber

- 2.5. Others

Radiation Resistant Rubber Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Radiation Resistant Rubber Regional Market Share

Geographic Coverage of Radiation Resistant Rubber

Radiation Resistant Rubber REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aerospace

- 5.1.2. Medical

- 5.1.3. Nuclear Industry

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Nitrile Rubber

- 5.2.2. Fluororubber

- 5.2.3. Silicone Rubber

- 5.2.4. EPDM Rubber

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Radiation Resistant Rubber Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aerospace

- 6.1.2. Medical

- 6.1.3. Nuclear Industry

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Nitrile Rubber

- 6.2.2. Fluororubber

- 6.2.3. Silicone Rubber

- 6.2.4. EPDM Rubber

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Radiation Resistant Rubber Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aerospace

- 7.1.2. Medical

- 7.1.3. Nuclear Industry

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Nitrile Rubber

- 7.2.2. Fluororubber

- 7.2.3. Silicone Rubber

- 7.2.4. EPDM Rubber

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Radiation Resistant Rubber Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aerospace

- 8.1.2. Medical

- 8.1.3. Nuclear Industry

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Nitrile Rubber

- 8.2.2. Fluororubber

- 8.2.3. Silicone Rubber

- 8.2.4. EPDM Rubber

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Radiation Resistant Rubber Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aerospace

- 9.1.2. Medical

- 9.1.3. Nuclear Industry

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Nitrile Rubber

- 9.2.2. Fluororubber

- 9.2.3. Silicone Rubber

- 9.2.4. EPDM Rubber

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Radiation Resistant Rubber Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aerospace

- 10.1.2. Medical

- 10.1.3. Nuclear Industry

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Nitrile Rubber

- 10.2.2. Fluororubber

- 10.2.3. Silicone Rubber

- 10.2.4. EPDM Rubber

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Radiation Resistant Rubber Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Aerospace

- 11.1.2. Medical

- 11.1.3. Nuclear Industry

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Nitrile Rubber

- 11.2.2. Fluororubber

- 11.2.3. Silicone Rubber

- 11.2.4. EPDM Rubber

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Asahi Kasei

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Lion Elastomers

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 JSR

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lanxess

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Synthos

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Goodyear

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Michelin

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 LG Chem

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DuPont

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 3M

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Solvay

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 ExxonMobil

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 SK Chemical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Sumitomo

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 James Walker

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Borflex

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Hayakawa Rubber

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 TRP Polymer Solutions

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 REONTECH

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Hutchinson

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Xi'an Sunward Aeromat Co.Ltd

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 SEEFAR

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.1 Asahi Kasei

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Radiation Resistant Rubber Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Radiation Resistant Rubber Revenue (million), by Application 2025 & 2033

- Figure 3: North America Radiation Resistant Rubber Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Radiation Resistant Rubber Revenue (million), by Type 2025 & 2033

- Figure 5: North America Radiation Resistant Rubber Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Radiation Resistant Rubber Revenue (million), by Country 2025 & 2033

- Figure 7: North America Radiation Resistant Rubber Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Radiation Resistant Rubber Revenue (million), by Application 2025 & 2033

- Figure 9: South America Radiation Resistant Rubber Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Radiation Resistant Rubber Revenue (million), by Type 2025 & 2033

- Figure 11: South America Radiation Resistant Rubber Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Radiation Resistant Rubber Revenue (million), by Country 2025 & 2033

- Figure 13: South America Radiation Resistant Rubber Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Radiation Resistant Rubber Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Radiation Resistant Rubber Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Radiation Resistant Rubber Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Radiation Resistant Rubber Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Radiation Resistant Rubber Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Radiation Resistant Rubber Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Radiation Resistant Rubber Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Radiation Resistant Rubber Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Radiation Resistant Rubber Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Radiation Resistant Rubber Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Radiation Resistant Rubber Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Radiation Resistant Rubber Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Radiation Resistant Rubber Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Radiation Resistant Rubber Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Radiation Resistant Rubber Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Radiation Resistant Rubber Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Radiation Resistant Rubber Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Radiation Resistant Rubber Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Radiation Resistant Rubber Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Radiation Resistant Rubber Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Radiation Resistant Rubber Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Radiation Resistant Rubber Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Radiation Resistant Rubber Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Radiation Resistant Rubber Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Radiation Resistant Rubber Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Radiation Resistant Rubber Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Radiation Resistant Rubber Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Radiation Resistant Rubber Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Radiation Resistant Rubber Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Radiation Resistant Rubber Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Radiation Resistant Rubber Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Radiation Resistant Rubber Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Radiation Resistant Rubber Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Radiation Resistant Rubber Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Radiation Resistant Rubber Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Radiation Resistant Rubber Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Radiation Resistant Rubber Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Radiation Resistant Rubber?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Radiation Resistant Rubber?

Key companies in the market include Asahi Kasei, Lion Elastomers, JSR, Lanxess, Synthos, Goodyear, Michelin, LG Chem, DuPont, 3M, Solvay, ExxonMobil, SK Chemical, Sumitomo, James Walker, Borflex, Hayakawa Rubber, TRP Polymer Solutions, REONTECH, Hutchinson, Xi'an Sunward Aeromat Co.,Ltd, SEEFAR.

3. What are the main segments of the Radiation Resistant Rubber?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8794 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Radiation Resistant Rubber," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Radiation Resistant Rubber report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Radiation Resistant Rubber?

To stay informed about further developments, trends, and reports in the Radiation Resistant Rubber, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence