Key Insights

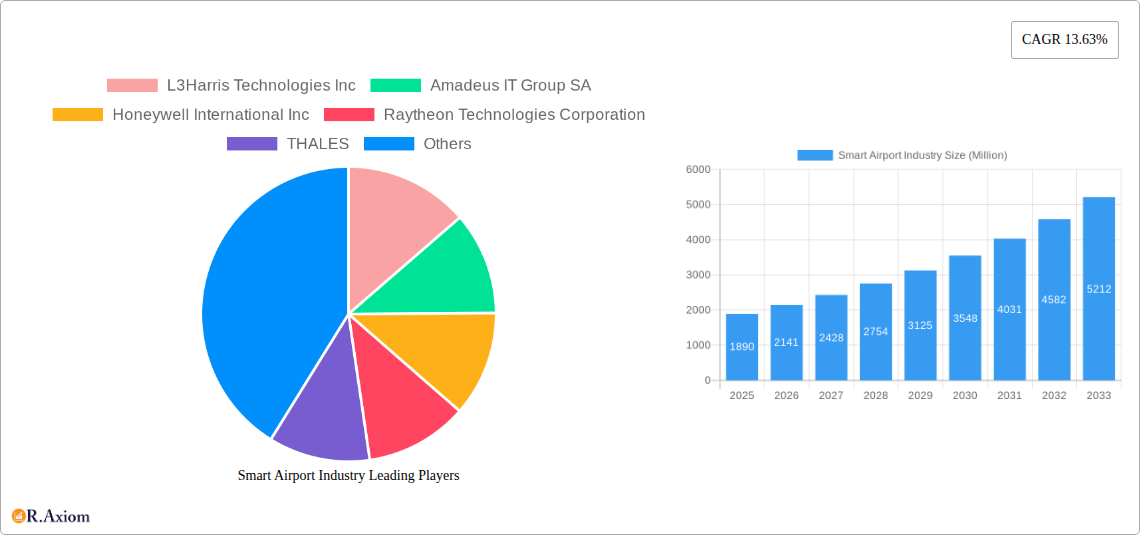

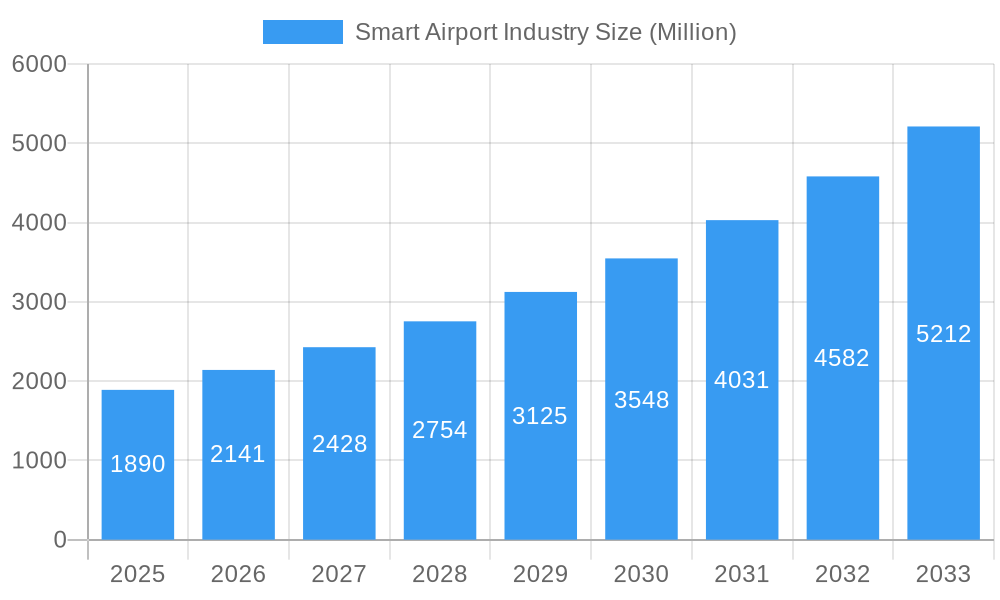

The smart airport industry is experiencing robust growth, projected to reach a market size of $1.89 billion in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) of 13.63% from 2025 to 2033. This expansion is driven by several key factors. Increasing passenger traffic globally necessitates efficient airport operations, leading to significant investments in advanced technologies such as automated baggage handling systems, improved security checkpoints, and real-time passenger information systems. Furthermore, the rising demand for enhanced passenger experience, including personalized services and seamless connectivity, fuels the adoption of smart technologies. The integration of Artificial Intelligence (AI) and the Internet of Things (IoT) in various airport functions is streamlining operations, improving safety, and reducing operational costs. The growth is further fueled by government initiatives promoting smart city infrastructure, including smart airports, and the increasing adoption of cloud-based solutions for data management and analytics.

Smart Airport Industry Market Size (In Billion)

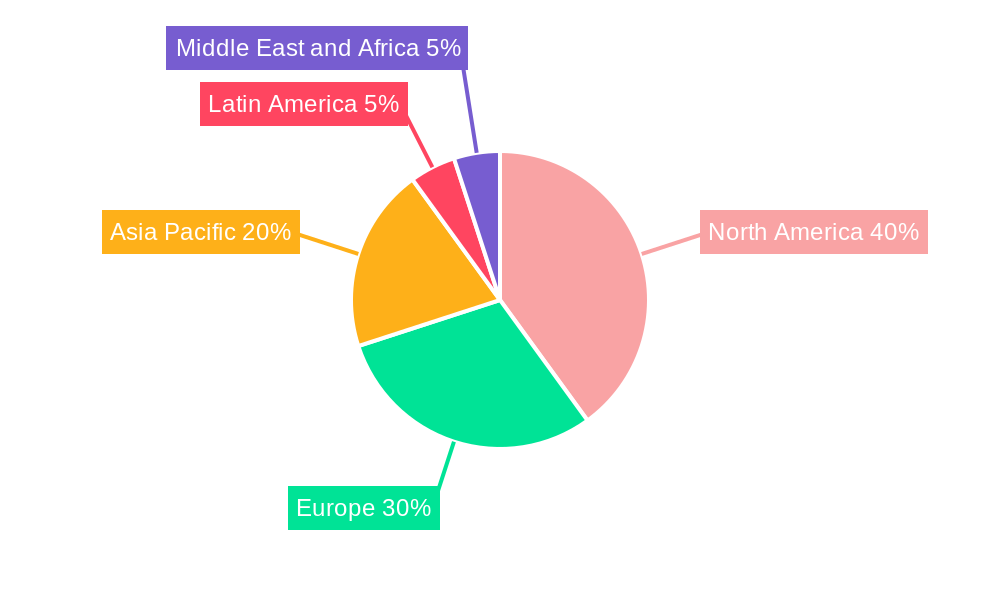

Segmentation within the smart airport market reveals significant opportunities across various technologies (security systems, communication systems, air and ground traffic control, passenger, cargo & baggage ground handling) and operational areas (landside, airside, terminal side). North America currently holds a substantial market share due to early adoption and advanced technological infrastructure, but the Asia-Pacific region is projected to witness the fastest growth over the forecast period, driven by rapid infrastructure development and rising air travel demand in countries like China and India. Competitive landscape analysis reveals key players including L3Harris Technologies, Amadeus IT Group, Honeywell, Raytheon, Thales, Sabre, IBM, Cisco, Siemens, NATS, SITA, and T-Systems are actively developing and deploying innovative smart airport solutions, fueling further market expansion and competition. However, high initial investment costs for implementing smart technologies and concerns related to data security and cybersecurity could pose challenges to market growth.

Smart Airport Industry Company Market Share

This comprehensive report provides a detailed analysis of the Smart Airport Industry, offering invaluable insights for stakeholders seeking to understand market dynamics, growth opportunities, and competitive landscapes. The study period covers 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, and the historical period encompasses 2019-2024. The report's findings are supported by rigorous research and data analysis, encompassing key players such as L3Harris Technologies Inc, Amadeus IT Group SA, Honeywell International Inc, Raytheon Technologies Corporation, THALES, Sabre GLBL Inc, IBM Corporation, Cisco Systems Inc, Siemens AG, NATS Holdings Limited, SITA, and T-Systems International GmbH. The market is segmented by technology (Security Systems, Communication Systems, Air and Ground Traffic Control, Passenger, Cargo & Baggage Ground Handling) and airport operation (Landside, Airside, Terminal Side). The global market size is predicted to reach xx Million by 2033.

Smart Airport Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the smart airport industry, exploring market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and mergers & acquisitions (M&A) activities.

The smart airport market demonstrates a moderately concentrated structure, with a few major players holding significant market share. For example, Amadeus IT Group SA and SITA hold substantial shares in the passenger processing and communication systems segments, while companies like Honeywell and Thales are major players in the security and air traffic control systems segments. However, the market also accommodates several smaller, specialized players, leading to healthy competition and innovation.

Market Share: Amadeus IT Group SA and SITA are estimated to hold a combined market share of approximately xx% in 2025. Honeywell International Inc. and Thales are estimated to hold approximately xx% combined in the security and air traffic control segments.

Innovation Drivers: The primary drivers of innovation are the rising demand for enhanced passenger experience, increasing security concerns, and the need for efficient airport operations. Technological advancements in areas like AI, IoT, and cloud computing are significantly accelerating innovation in smart airport technologies.

Regulatory Frameworks: Stringent aviation safety regulations and data privacy regulations influence the adoption of new technologies and impact the market growth. International standards like ICAO regulations play a crucial role in shaping industry practices.

M&A Activities: The industry has witnessed significant M&A activity in recent years. Deal values have fluctuated, with larger deals exceeding xx Million USD. This activity is primarily driven by the need to expand market reach, gain access to new technologies, and improve service offerings. Examples include (but are not limited to): strategic partnerships between software providers and airport operators to integrate smart solutions.

Product Substitutes: While the core functions provided by smart airport solutions are unique, certain aspects might see substitutions with more cost-effective or specialized alternatives. For example, improved manual processes could partially substitute some automated systems in certain smaller airports.

Smart Airport Industry Industry Trends & Insights

The smart airport industry is experiencing robust growth, fueled by several key factors. The Compound Annual Growth Rate (CAGR) is projected to be xx% during the forecast period (2025-2033). This growth reflects an increasing focus on optimizing operational efficiency, enhancing passenger experience, and improving security.

Technological disruptions, such as the integration of artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT) are revolutionizing airport operations. The market penetration of AI-powered solutions for passenger screening, baggage handling, and predictive maintenance is steadily increasing. Consumer preferences are shifting towards seamless and personalized airport experiences, driving the demand for smart solutions that improve passenger flow, minimize waiting times, and provide personalized services.

The competitive dynamics are characterized by both collaboration and competition. Strategic partnerships are common between technology providers and airport operators, facilitating the deployment of integrated smart airport systems. However, competition is also intense, with established players and new entrants vying for market share by offering innovative solutions.

Dominant Markets & Segments in Smart Airport Industry

North America and Europe currently dominate the smart airport market, driven by advanced technological infrastructure and higher spending on airport modernization projects. However, the Asia-Pacific region is experiencing rapid growth, projected to show the highest CAGR over the forecast period, driven by increasing air travel demand and government initiatives to modernize airports.

Key Drivers:

- North America: Strong government support, advanced technological infrastructure, and the presence of major technology providers.

- Europe: High air passenger traffic, focus on sustainable airport operations, and stringent security regulations.

- Asia-Pacific: Rapid growth in air travel demand, increasing investments in airport infrastructure, and government support for smart city initiatives.

Dominant Segments:

By Technology: Security systems currently represent the largest segment, driven by increasing security concerns and regulatory mandates. The Communication systems segment exhibits high growth potential driven by increasing data needs within airports. Air and ground traffic control technology is mature but continues to evolve with automation and AI integration. Passenger, Cargo & Baggage Ground Handling segments are exhibiting strong growth due to technology advancements in automating these processes and reducing operational costs.

By Airport Operation: The airside segment is witnessing significant growth as it plays a crucial role in improving overall airport efficiency and safety. Investments in advanced technologies for aircraft operations and ground handling contribute to its growth. Landside and Terminal Side are experiencing improvements and enhancements through automation, improved passenger flow management and technological advancements.

Smart Airport Industry Product Developments

The smart airport industry is experiencing a dynamic phase of innovation, with recent product developments primarily centered on **elevating security protocols, revolutionizing the passenger journey, and streamlining airport operations.** Key advancements include the deployment of sophisticated AI-powered passenger screening systems that enhance threat detection with greater accuracy and speed. Travelers benefit from the convenience and efficiency of self-service bag drop kiosks, reducing wait times and improving overall flow. Airport infrastructure is becoming more resilient through predictive maintenance solutions, which leverage data analytics to anticipate and address potential issues before they impact operations. Furthermore, the integration of advanced communication systems is playing a crucial role in optimizing air traffic management, ensuring smoother and safer air travel. These innovations collectively contribute to heightened efficiency, robust security, and an enriched passenger experience, providing significant competitive advantages for pioneering vendors in the market.

Report Scope & Segmentation Analysis

By Technology: The smart airport market is meticulously segmented by key technology verticals, including security systems, communication systems, air and ground traffic control, passenger services, and cargo & baggage handling. For each segment, the report provides in-depth analysis of growth projections, current market sizes, and evolving competitive dynamics. The Security Systems segment is anticipated to experience robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately XX% between 2025 and 2033, driven by increasing global security concerns. Similarly, the Communication Systems segment is expected to witness a strong CAGR of around XX% over the same period, fueled by the need for seamless data exchange and advanced connectivity. The growth trajectory of the Air and Ground Traffic Control market will be significantly influenced by evolving regulatory frameworks and the successful integration of new technologies. The Passenger Services segment is projected to exhibit a high CAGR, directly correlating with escalating consumer demand for seamless, personalized, and efficient travel experiences. Lastly, the Cargo and Baggage Handling segment is forecasted to achieve steady growth, propelled by the ongoing adoption of automation and a continuous drive for operational efficiency improvements.

By Airport Operation: The market is further dissected based on critical airport operational domains: landside, airside, and terminal-side operations. Each of these segments is subjected to detailed analysis, outlining market size, future growth trajectories, and the competitive landscape. Growth rates within these segments are expected to vary, influenced by regional investment priorities and the specific operational aspects that airports choose to emphasize in their modernization efforts.

Key Drivers of Smart Airport Industry Growth

The key drivers of growth in the smart airport industry include:

- Technological advancements: AI, IoT, and cloud computing are transforming airport operations.

- Increased passenger traffic: The continuous increase in air travel fuels demand for efficient and secure airport services.

- Stringent security regulations: Security concerns drive investment in advanced security systems.

- Government initiatives: Government support for airport modernization projects fosters growth.

Challenges in the Smart Airport Industry Sector

The industry faces challenges such as:

- High initial investment costs: Implementing smart airport technologies involves substantial investments.

- Cybersecurity risks: Connected systems are vulnerable to cyberattacks.

- Integration complexities: Integrating different technologies across various airport systems can be challenging.

- Data privacy concerns: Collecting and using passenger data raises privacy concerns. These factors affect the overall adoption of smart solutions and may lead to slower-than-expected growth in certain segments.

Emerging Opportunities in Smart Airport Industry

The smart airport industry is ripe with emerging opportunities, poised to redefine airport functionality and passenger interaction:

- Biometric Technologies: The integration of biometric-based passenger processing is rapidly gaining traction, offering enhanced security and a frictionless travel experience from check-in to boarding.

- Robotic Process Automation (RPA): The deployment of robots is on the rise, automating a wide array of airport tasks, from cleaning and maintenance to baggage handling and passenger assistance, thereby improving efficiency and reducing labor costs.

- Predictive Analytics: Leveraging advanced predictive analytics allows airports to forecast passenger flow, anticipate demand fluctuations, and optimize resource allocation, leading to more efficient operations and improved passenger satisfaction.

- Sustainable Solutions: There is a growing and significant demand for environmentally friendly airport solutions, encompassing energy efficiency, waste reduction, and sustainable infrastructure development, aligning with global climate initiatives.

Leading Players in the Smart Airport Industry Market

- L3Harris Technologies Inc

- Amadeus IT Group SA

- Honeywell International Inc

- Raytheon Technologies Corporation

- THALES

- Sabre GLBL Inc

- IBM Corporation

- Cisco Systems Inc

- Siemens AG

- NATS Holdings Limited

- SITA

- T-Systems International GmbH

Key Developments in Smart Airport Industry Industry

February 2023: Smiths Detection secured a significant contract to equip five major international airports in New Zealand with their cutting-edge checkpoint security technology, underscoring the escalating global demand for advanced security screening solutions.

June 2022: Fiumicino Airport in Italy unveiled plans and advancements for a 100% baggage X-ray control system, showcasing a substantial leap forward in the sophistication and thoroughness of baggage handling technology.

June 2022: SITA, in collaboration with Alstef Group, launched Swift Drop, an innovative self-bag drop solution designed to enhance passenger experience and boost operational efficiency. Mexico City's Felipe Ángeles International Airport was the pioneering adopter, installing 20 units of this advanced system.

Strategic Outlook for Smart Airport Industry Market

The smart airport market is on an impressive trajectory, poised for substantial growth in the coming decade. This expansion will be primarily fueled by the accelerated adoption of advanced technologies across all airport functions, the ever-increasing demand for superior passenger experiences, and a relentless focus on optimizing operational efficiency. Airlines and airport operators that can deliver innovative, interconnected solutions capable of addressing critical security concerns, significantly improving operational workflows, and enhancing passenger journeys will be strategically positioned to capture a substantial share of future market growth. Furthermore, the growing emphasis on sustainability and comprehensive digital transformation initiatives will continue to shape and define the industry's future direction and competitive landscape.

Smart Airport Industry Segmentation

-

1. Technology

- 1.1. Security Systems

- 1.2. Communication Systems

- 1.3. Air and Ground Traffic Control

- 1.4. Passenger, Cargo, and Baggage Ground Handling

-

2. Airport Operation

- 2.1. Landside

- 2.2. Airside

- 2.3. Terminal Side

Smart Airport Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Rest of Latin America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Smart Airport Industry Regional Market Share

Geographic Coverage of Smart Airport Industry

Smart Airport Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Security Systems

- 5.1.2. Communication Systems

- 5.1.3. Air and Ground Traffic Control

- 5.1.4. Passenger, Cargo, and Baggage Ground Handling

- 5.2. Market Analysis, Insights and Forecast - by Airport Operation

- 5.2.1. Landside

- 5.2.2. Airside

- 5.2.3. Terminal Side

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Smart Airport Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Security Systems

- 6.1.2. Communication Systems

- 6.1.3. Air and Ground Traffic Control

- 6.1.4. Passenger, Cargo, and Baggage Ground Handling

- 6.2. Market Analysis, Insights and Forecast - by Airport Operation

- 6.2.1. Landside

- 6.2.2. Airside

- 6.2.3. Terminal Side

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Smart Airport Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Security Systems

- 7.1.2. Communication Systems

- 7.1.3. Air and Ground Traffic Control

- 7.1.4. Passenger, Cargo, and Baggage Ground Handling

- 7.2. Market Analysis, Insights and Forecast - by Airport Operation

- 7.2.1. Landside

- 7.2.2. Airside

- 7.2.3. Terminal Side

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Europe Smart Airport Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Security Systems

- 8.1.2. Communication Systems

- 8.1.3. Air and Ground Traffic Control

- 8.1.4. Passenger, Cargo, and Baggage Ground Handling

- 8.2. Market Analysis, Insights and Forecast - by Airport Operation

- 8.2.1. Landside

- 8.2.2. Airside

- 8.2.3. Terminal Side

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Asia Pacific Smart Airport Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Security Systems

- 9.1.2. Communication Systems

- 9.1.3. Air and Ground Traffic Control

- 9.1.4. Passenger, Cargo, and Baggage Ground Handling

- 9.2. Market Analysis, Insights and Forecast - by Airport Operation

- 9.2.1. Landside

- 9.2.2. Airside

- 9.2.3. Terminal Side

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Latin America Smart Airport Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Security Systems

- 10.1.2. Communication Systems

- 10.1.3. Air and Ground Traffic Control

- 10.1.4. Passenger, Cargo, and Baggage Ground Handling

- 10.2. Market Analysis, Insights and Forecast - by Airport Operation

- 10.2.1. Landside

- 10.2.2. Airside

- 10.2.3. Terminal Side

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Middle East and Africa Smart Airport Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Security Systems

- 11.1.2. Communication Systems

- 11.1.3. Air and Ground Traffic Control

- 11.1.4. Passenger, Cargo, and Baggage Ground Handling

- 11.2. Market Analysis, Insights and Forecast - by Airport Operation

- 11.2.1. Landside

- 11.2.2. Airside

- 11.2.3. Terminal Side

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 L3Harris Technologies Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amadeus IT Group SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Honeywell International Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Raytheon Technologies Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 THALES

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sabre GLBL Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 IBM Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Cisco Systems Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Siemens AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 NATS Holdings Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 SITA

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 T-Systems International GmbH

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 L3Harris Technologies Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Smart Airport Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Smart Airport Industry Revenue (Million), by Technology 2025 & 2033

- Figure 3: North America Smart Airport Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Smart Airport Industry Revenue (Million), by Airport Operation 2025 & 2033

- Figure 5: North America Smart Airport Industry Revenue Share (%), by Airport Operation 2025 & 2033

- Figure 6: North America Smart Airport Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Smart Airport Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Smart Airport Industry Revenue (Million), by Technology 2025 & 2033

- Figure 9: Europe Smart Airport Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Europe Smart Airport Industry Revenue (Million), by Airport Operation 2025 & 2033

- Figure 11: Europe Smart Airport Industry Revenue Share (%), by Airport Operation 2025 & 2033

- Figure 12: Europe Smart Airport Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Smart Airport Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Smart Airport Industry Revenue (Million), by Technology 2025 & 2033

- Figure 15: Asia Pacific Smart Airport Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Asia Pacific Smart Airport Industry Revenue (Million), by Airport Operation 2025 & 2033

- Figure 17: Asia Pacific Smart Airport Industry Revenue Share (%), by Airport Operation 2025 & 2033

- Figure 18: Asia Pacific Smart Airport Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Smart Airport Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Smart Airport Industry Revenue (Million), by Technology 2025 & 2033

- Figure 21: Latin America Smart Airport Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Latin America Smart Airport Industry Revenue (Million), by Airport Operation 2025 & 2033

- Figure 23: Latin America Smart Airport Industry Revenue Share (%), by Airport Operation 2025 & 2033

- Figure 24: Latin America Smart Airport Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Smart Airport Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Smart Airport Industry Revenue (Million), by Technology 2025 & 2033

- Figure 27: Middle East and Africa Smart Airport Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Middle East and Africa Smart Airport Industry Revenue (Million), by Airport Operation 2025 & 2033

- Figure 29: Middle East and Africa Smart Airport Industry Revenue Share (%), by Airport Operation 2025 & 2033

- Figure 30: Middle East and Africa Smart Airport Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Smart Airport Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Airport Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 2: Global Smart Airport Industry Revenue Million Forecast, by Airport Operation 2020 & 2033

- Table 3: Global Smart Airport Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Smart Airport Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 5: Global Smart Airport Industry Revenue Million Forecast, by Airport Operation 2020 & 2033

- Table 6: Global Smart Airport Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Smart Airport Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 10: Global Smart Airport Industry Revenue Million Forecast, by Airport Operation 2020 & 2033

- Table 11: Global Smart Airport Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: France Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Germany Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Italy Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Smart Airport Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 18: Global Smart Airport Industry Revenue Million Forecast, by Airport Operation 2020 & 2033

- Table 19: Global Smart Airport Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: China Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: India Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: South Korea Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Rest of Asia Pacific Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Global Smart Airport Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 26: Global Smart Airport Industry Revenue Million Forecast, by Airport Operation 2020 & 2033

- Table 27: Global Smart Airport Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: Brazil Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Latin America Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Smart Airport Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 31: Global Smart Airport Industry Revenue Million Forecast, by Airport Operation 2020 & 2033

- Table 32: Global Smart Airport Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 33: Saudi Arabia Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Arab Emirates Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Rest of Middle East and Africa Smart Airport Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Airport Industry?

The projected CAGR is approximately 13.63%.

2. Which companies are prominent players in the Smart Airport Industry?

Key companies in the market include L3Harris Technologies Inc, Amadeus IT Group SA, Honeywell International Inc, Raytheon Technologies Corporation, THALES, Sabre GLBL Inc, IBM Corporation, Cisco Systems Inc, Siemens AG, NATS Holdings Limited, SITA, T-Systems International GmbH.

3. What are the main segments of the Smart Airport Industry?

The market segments include Technology, Airport Operation.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.89 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The Passenger. Cargo & Baggage Ground Handling Segment to Dominate the Market During the Forecasted Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In February 2023, the Aviation Security Service (AvSec) of New Zealand awarded a contract to Smiths Detection, a leader in threat detection and security inspection technologies, to provide cutting-edge checkpoint security technology for its five main international airports: Auckland, Christchurch, Dunedin, Queenstown, and Wellington.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Airport Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Airport Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Airport Industry?

To stay informed about further developments, trends, and reports in the Smart Airport Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence