Key Insights

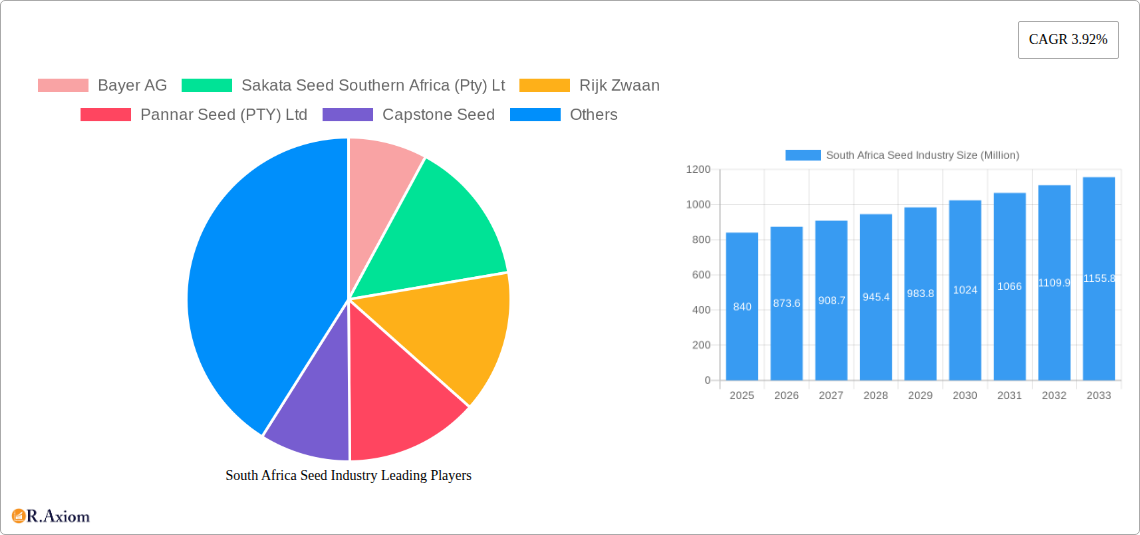

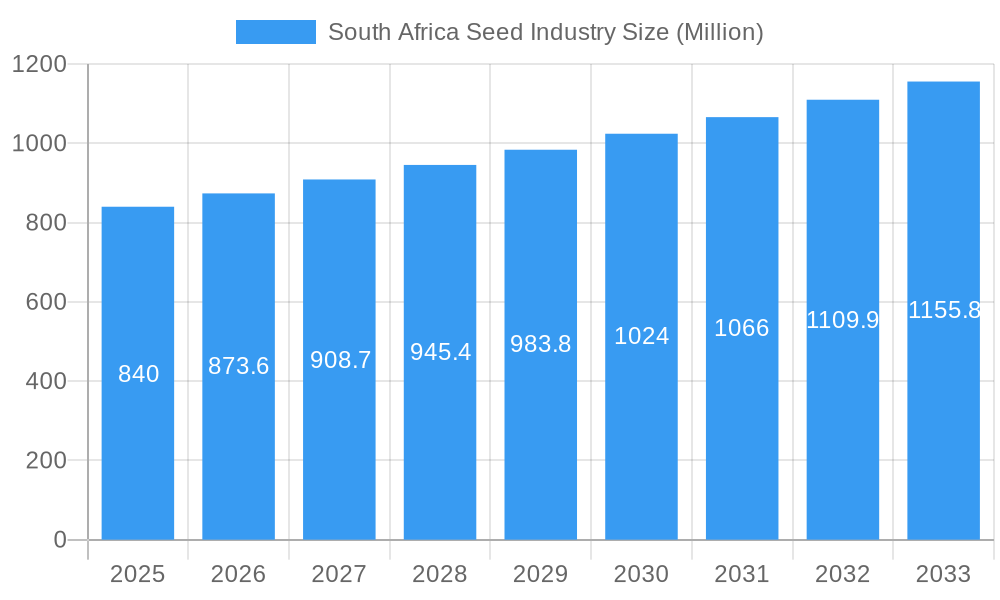

The South African seed industry, valued at approximately $840 million in 2025, is projected to experience robust growth, driven by increasing demand for food security and rising agricultural productivity. A Compound Annual Growth Rate (CAGR) of 3.92% from 2025 to 2033 indicates a promising trajectory. Key drivers include government initiatives promoting agricultural modernization, advancements in seed technology (particularly hybrid and GM seeds tailored to local conditions), and the expanding cultivation of high-value crops like vegetables and oilseeds. The market is segmented by seed type (conventional, hybrid, genetically modified) and crop type (grain & cereal, pulses, vegetables, oilseeds), offering diverse investment opportunities. While challenges remain, such as climate change impacting crop yields and the need for improved infrastructure, the overall market outlook remains positive. Leading players like Bayer AG, Syngenta, and Sakata Seed are well-positioned to capitalize on this growth, focusing on research and development to enhance seed quality and resilience. The strong regional focus on South Africa, with expansion into other African countries like Sudan, Uganda, and Kenya creating further growth opportunities, points towards a significant market expansion in the coming decade.

South Africa Seed Industry Market Size (In Million)

The South African seed market's growth is significantly influenced by the adoption of modern agricultural practices. The increasing preference for high-yielding hybrid and GM seeds reflects a shift towards enhanced agricultural efficiency. However, the market faces challenges including price volatility related to input costs and the need for greater farmer awareness regarding the benefits of advanced seed technologies. Government support and investment in research & development will play a crucial role in mitigating these challenges and fostering sustainable growth within the South African seed industry. The ongoing expansion into neighboring African nations signifies a broader continental impact, highlighting South Africa's position as a pivotal player in the African agricultural landscape. Successful market players will need to address logistical complexities in distribution across diverse geographical regions and tailor their offerings to the specific needs of each region's agricultural sector.

South Africa Seed Industry Company Market Share

South Africa Seed Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the South Africa seed industry, encompassing market size, growth forecasts, segment analysis, competitive landscape, and future trends. The study period covers 2019-2033, with 2025 serving as both the base and estimated year. The forecast period is 2025-2033, and the historical period is 2019-2024. This report is essential for industry stakeholders, investors, and strategic decision-makers seeking to understand and capitalize on opportunities within this dynamic market. The total market size in 2025 is estimated at xx Million, projected to reach xx Million by 2033.

South Africa Seed Industry Market Concentration & Innovation

The South African seed industry exhibits a moderately concentrated market structure, with a few multinational corporations and established local players dominating the landscape. Key players such as Bayer AG, Bayer AG, Sakata Seed Southern Africa (Pty) Ltd, Rijk Zwaan, Pannar Seed (PTY) Ltd, Capstone Seed, Seed Co Limited, Syngenta Seed SA (Pty) Ltd, Limagrai, and Corteva Agriscience collectively hold a significant market share, estimated at approximately 70% in 2025. Market share fluctuates based on crop performance and specific product introductions. Innovation is driven by the need for higher yields, disease resistance, and improved crop quality, leading to significant investments in R&D. The regulatory framework, while generally supportive of innovation, faces ongoing challenges in adapting to the rapid pace of technological advancements in genetic modification. The industry witnesses increasing M&A activity, with deal values reaching xx Million in the past five years. Key drivers behind these activities include market consolidation, access to new technologies, and expansion into diverse crop segments.

- Market Concentration: Top 10 players account for approximately 70% market share (2025).

- Innovation Drivers: Higher yields, disease resistance, improved quality, and GMO technologies.

- M&A Activity: Deal values totaled approximately xx Million in the past five years.

- Regulatory Framework: Undergoes continuous evolution to accommodate GMO and biotechnology advancements.

South Africa Seed Industry Industry Trends & Insights

The South African seed industry is experiencing dynamic evolution, underpinned by a growing agricultural sector, escalating demand for superior-yielding and resilient crop varieties, and robust government programs aimed at modernizing agricultural practices. Projections indicate a Compound Annual Growth Rate (CAGR) of [Insert Projected CAGR Here]% for the period 2025-2033, signaling sustained market expansion. Technological advancements, particularly in precision agriculture, digital farming solutions, and sophisticated data analytics, are revolutionizing crop management and optimizing seed selection processes. Concurrently, evolving consumer preferences are steering the market towards seeds that offer enhanced nutritional profiles, improved environmental sustainability, and superior disease resistance. The competitive landscape is characterized by vigorous competition among both established multinational corporations and agile local enterprises, fostering strategic collaborations, vital partnerships, and a continuous drive for product innovation and diversification. The adoption rate of hybrid seeds and genetically modified (GM) varieties is on a consistent upward trajectory, reflecting a growing farmer embrace of advanced agricultural technologies.

Dominant Markets & Segments in South Africa Seed Industry

The South African seed industry displays diverse market segments, with grain and cereal seeds holding the largest share, followed by oilseeds and vegetables. The dominant geographic regions are those with favorable agricultural conditions and robust agricultural infrastructure.

- Leading Segment: Grain and Cereal (market share xx% in 2025). Key drivers include government support for staple crop production and consistent demand.

- Growth Segments: Oilseed and Vegetable seeds are experiencing significant growth fueled by increasing demand for healthier oils and vegetable consumption.

- Types of Seeds: Hybrid seeds are gaining market share over conventional seeds due to higher yields and improved traits. GM seeds, while facing some regulatory and consumer resistance, also show increasing adoption.

- Regional Dominance: Regions with developed agricultural infrastructure and access to irrigation systems.

South Africa Seed Industry Product Developments

Recent product innovations focus on developing drought-tolerant, disease-resistant, and high-yielding varieties adapted to local climatic conditions. This includes advances in hybrid and GM seeds to meet specific market demands. Competitive advantages are often achieved through proprietary technologies, strong distribution networks, and effective marketing strategies. Technological trends are driving the development of seeds with enhanced nutritional properties and resilience to climate change.

Report Scope & Segmentation Analysis

This report segments the South African seed industry based on seed type (Conventional, Hybrid, GM) and crop type (Grain & Cereal, Pulse, Vegetables, Oilseed). Each segment is analyzed considering market size, growth projections, and competitive dynamics. The market size for each segment is estimated separately for the forecast period. Detailed growth projections for each segment are also provided.

- Conventional Seeds: Market size xx Million in 2025, projected growth at xx% CAGR. Competitive dynamics include price competition and brand loyalty.

- Hybrid Seeds: Market size xx Million in 2025, projected growth at xx% CAGR. Key competitive factors include yield performance and trait packages.

- GM Seeds: Market size xx Million in 2025, projected growth at xx% CAGR. Growth is influenced by regulatory approvals and consumer acceptance.

- Grain & Cereal: Market size xx Million in 2025, projected growth at xx% CAGR. Competition is fierce, focused on yield and disease resistance.

- Pulse: Market size xx Million in 2025, projected growth at xx% CAGR. Growth is driven by health-conscious consumer preferences.

- Vegetables: Market size xx Million in 2025, projected growth at xx% CAGR. Competition centers around specific varieties and quality.

- Oilseed: Market size xx Million in 2025, projected growth at xx% CAGR. Growth is linked to biofuel demand and health trends.

Key Drivers of South Africa Seed Industry Growth

The expansion of the South African seed industry is significantly fueled by several interconnected factors. Proactive government initiatives focused on modernizing agriculture and substantial investments in agricultural infrastructure are pivotal. Concurrently, cutting-edge advancements in seed breeding techniques and genetic modification technologies are making substantial contributions. The escalating consumer demand for food products that are not only high in quality but also rich in nutrients serves as a strong impetus for market growth. Furthermore, a growing economy coupled with rising disposable incomes is enhancing purchasing power, thereby supporting a broader adoption of improved seed technologies by farmers.

Challenges in the South Africa Seed Industry Sector

Despite its growth, the South African seed industry navigates several considerable challenges. Unpredictable weather patterns continue to pose a risk to crop yields, and escalating input costs place pressure on farmer profitability. Regulatory complexities surrounding GM seeds, alongside stringent quality control mandates, can introduce operational impediments. Inefficiencies within the supply chain and persistent competition from informal seed markets further complicate the operating environment. These obstacles, while varying in intensity across different market segments, can collectively influence profitability and temper the pace of market expansion.

Emerging Opportunities in South Africa Seed Industry

The burgeoning demand for climate-resilient seed varieties, particularly those engineered for water efficiency and drought tolerance, presents a significant avenue for growth. The development of seeds enriched with essential nutrients to bolster food security is another critical area ripe for innovation. The widespread adoption of precision farming methodologies and associated technologies offers substantial opportunities to boost operational efficiency and achieve higher crop yields. Moreover, the potential to expand into international markets by exporting specific high-value seed varieties represents an attractive prospect for market growth.

Leading Players in the South Africa Seed Industry Market

- Bayer AG

- Sakata Seed Southern Africa (Pty) Lt

- Rijk Zwaan

- Pannar Seed (PTY) Ltd

- Capstone Seed

- Seed Co Limited

- Syngenta Seed SA (Pty) Ltd

- Limagrai

- Corteva Agriscience

Key Developments in South Africa Seed Industry Industry

- 2022: Introduction of new drought-resistant maize hybrid by Pannar Seed.

- 2021: Acquisition of a local seed company by a multinational player.

- 2020: Launch of a new range of vegetable seeds by Sakata Seed Southern Africa.

- 2019: Implementation of new regulations impacting GMO seed approvals. (Specific details on these regulations and their impacts should be included in the full report.)

Strategic Outlook for South Africa Seed Industry Market

The South African seed industry is strategically positioned for sustained and robust growth, propelled by continuous technological innovation, an ever-increasing demand for advanced seed solutions, and supportive government policies. Future growth avenues are strongly linked to the development of climate-smart seeds, the effective leveraging of precision agriculture techniques, and the strategic expansion into new domestic and international markets. Addressing the pressing challenges posed by climate change and ensuring national food security will be paramount for achieving enduring and sustainable growth. The market is also likely to witness continued consolidation, with potential for increased mergers and acquisitions shaping the competitive landscape.

South Africa Seed Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

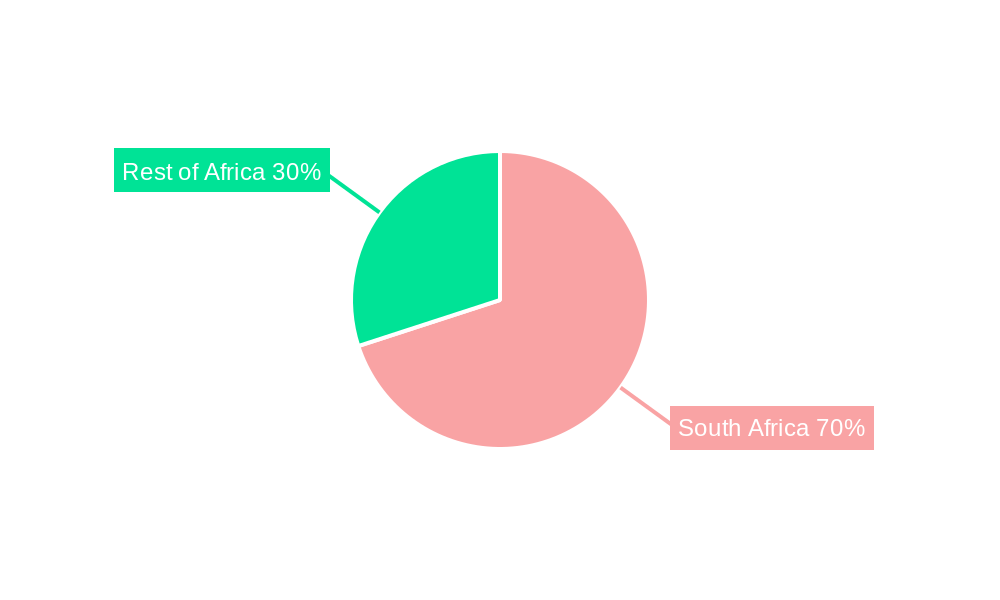

South Africa Seed Industry Segmentation By Geography

- 1. South Africa

South Africa Seed Industry Regional Market Share

Geographic Coverage of South Africa Seed Industry

South Africa Seed Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.92% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. South Africa

- 6. South Africa Seed Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bayer AG

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sakata Seed Southern Africa (Pty) Lt

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Rijk Zwaan

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Pannar Seed (PTY) Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Capstone Seed

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Seed Co Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Syngenta Seed SA (Pty) Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Limagrai

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Corteva Agriscience

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Bayer AG

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Africa Seed Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South Africa Seed Industry Share (%) by Company 2025

List of Tables

- Table 1: South Africa Seed Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: South Africa Seed Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: South Africa Seed Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: South Africa Seed Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: South Africa Seed Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: South Africa Seed Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: South Africa Seed Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: South Africa Seed Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: South Africa Seed Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: South Africa Seed Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: South Africa Seed Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: South Africa Seed Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Africa Seed Industry?

The projected CAGR is approximately 3.92%.

2. Which companies are prominent players in the South Africa Seed Industry?

Key companies in the market include Bayer AG, Sakata Seed Southern Africa (Pty) Lt, Rijk Zwaan, Pannar Seed (PTY) Ltd, Capstone Seed, Seed Co Limited, Syngenta Seed SA (Pty) Ltd, Limagrai, Corteva Agriscience.

3. What are the main segments of the South Africa Seed Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.84 Million as of 2022.

5. What are some drivers contributing to market growth?

Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns.

6. What are the notable trends driving market growth?

Demand for Quality Seeds.

7. Are there any restraints impacting market growth?

High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Africa Seed Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Africa Seed Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Africa Seed Industry?

To stay informed about further developments, trends, and reports in the South Africa Seed Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence