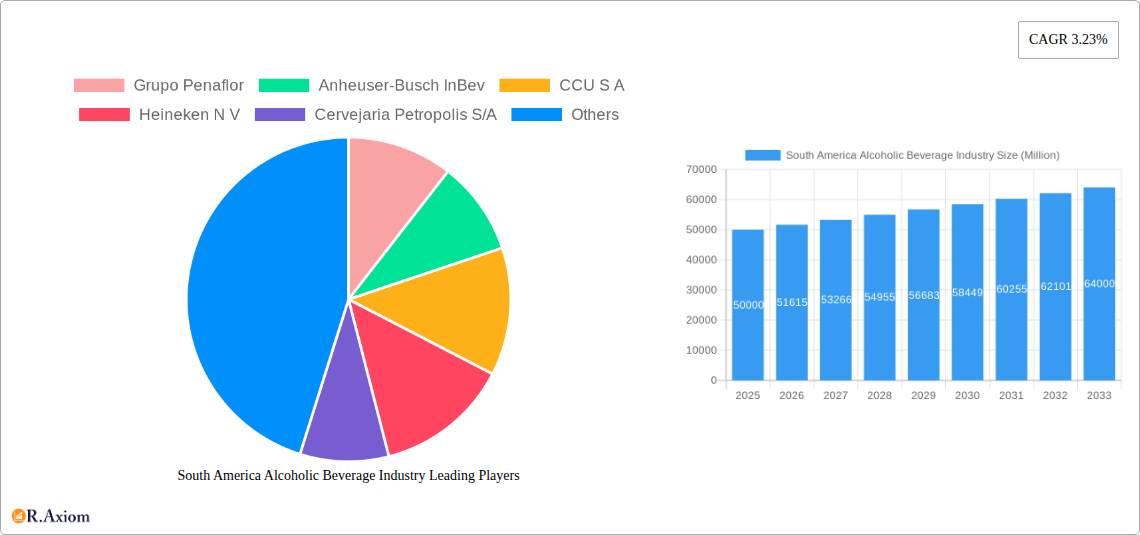

Key Insights

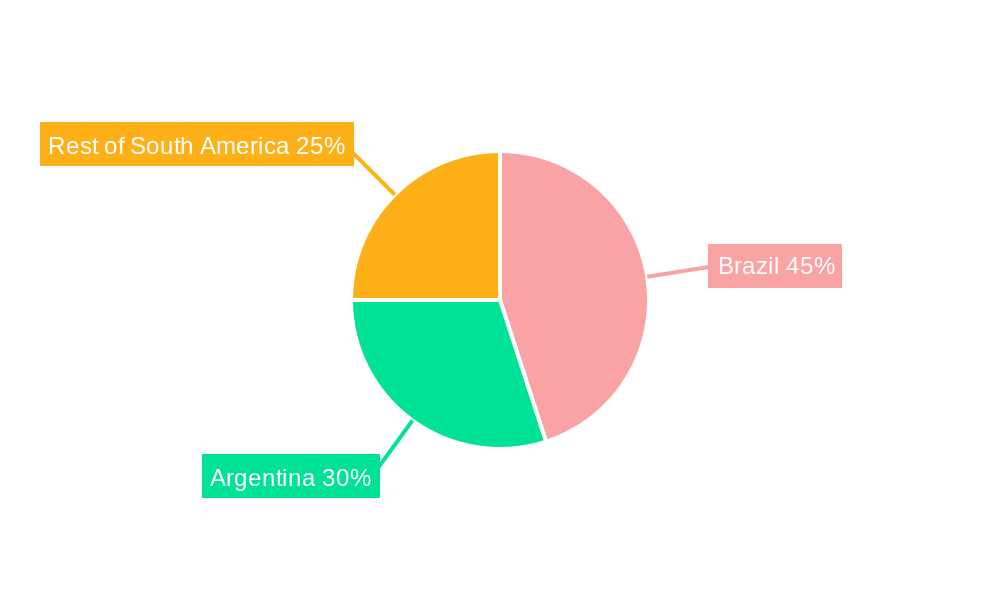

The South American alcoholic beverage market, valued at approximately $XX million in 2025, is projected to experience steady growth, exhibiting a compound annual growth rate (CAGR) of 3.23% from 2025 to 2033. This growth is fueled by several key factors. Rising disposable incomes, particularly within the burgeoning middle class of countries like Brazil and Argentina, are driving increased consumer spending on premium alcoholic beverages. Furthermore, evolving consumer preferences towards craft beers, premium wines, and innovative spirit offerings are reshaping the market landscape. The increasing popularity of online alcohol delivery services and the expansion of modern trade channels are also contributing to market expansion. However, regulatory restrictions on alcohol advertising and consumption, along with health concerns related to excessive alcohol intake, pose significant restraints to market growth. Competition remains intense among both multinational giants and local players, leading to strategic initiatives such as mergers and acquisitions, product diversification, and brand building. The market is segmented by product type (beer, wine, spirits) and distribution channel (on-trade, off-trade), with beer currently dominating the market share. Brazil and Argentina constitute the largest regional markets, owing to their higher population density and robust economies. Growth in the Rest of South America segment is expected to lag slightly behind the major markets but demonstrates considerable untapped potential.

The forecast period of 2025-2033 presents significant opportunities for players across the value chain. Successful strategies will incorporate a deep understanding of evolving consumer preferences in each specific South American market, efficient distribution strategies, and a focus on marketing initiatives that resonate with culturally diverse demographics. Companies are likely to see continued success by innovating product offerings, focusing on sustainability initiatives, and leveraging digital marketing channels to engage consumers effectively. Furthermore, maintaining compliance with the evolving regulatory environment in each country will be crucial for sustained growth. The continued development of the region's economy and its increasingly sophisticated consumer base will ultimately determine the pace and trajectory of the alcoholic beverage market’s evolution.

South America Alcoholic Beverage Industry: 2019-2033 Market Analysis & Forecast Report

This comprehensive report provides a detailed analysis of the South American alcoholic beverage industry, covering the period 2019-2033. It offers invaluable insights into market trends, competitive dynamics, and future growth opportunities for stakeholders including manufacturers, distributors, investors, and regulatory bodies. The report leverages extensive market data and expert analysis to provide a clear and actionable understanding of this dynamic sector. With a base year of 2025 and a forecast period extending to 2033, this report is an essential resource for navigating the complexities of the South American alcoholic beverage market.

South America Alcoholic Beverage Industry Market Concentration & Innovation

The South American alcoholic beverage market exhibits a moderately concentrated structure, with a few dominant players controlling significant market share. Key players such as Anheuser-Busch InBev, Diageo, and Heineken N.V. hold substantial positions, particularly in the beer segment. However, regional breweries and local producers also maintain significant presence, especially in the wine and spirits categories. The market is characterized by ongoing innovation driven by evolving consumer preferences, technological advancements, and regulatory changes.

- Market Concentration: The top 5 players account for approximately xx% of the total market value (2024 est.).

- Innovation Drivers: Rising demand for premium and craft beverages, health-conscious options (e.g., low-calorie beers, hard seltzers), and sustainable practices are major drivers.

- Regulatory Framework: Varying regulations across South American countries impact production, distribution, and marketing. Recent changes in alcohol taxation and advertising restrictions are analyzed.

- Product Substitutes: Non-alcoholic beverages, ready-to-drink (RTD) cocktails, and functional drinks pose competitive pressure.

- End-User Trends: Growing demand for premiumization, personalized experiences, and convenient consumption formats (e.g., canned cocktails, single-serve bottles) shape market dynamics.

- M&A Activities: Significant mergers and acquisitions (M&A) activity, including Diageo's acquisition of Balcones Distilling (November 2022), reshapes the competitive landscape. Total M&A deal value in the last 5 years is estimated at $xx Million.

South America Alcoholic Beverage Industry Industry Trends & Insights

The South American alcoholic beverage market is characterized by robust growth, driven by a combination of factors. Rising disposable incomes, expanding middle class, and increasing urbanization contribute to higher alcohol consumption. A shift towards premiumization, particularly in the beer and spirits segments, fuels market expansion. Technological disruptions, such as improved brewing techniques and innovative packaging solutions, enhance product quality and convenience, further stimulating demand.

The market witnessed a CAGR of xx% during the historical period (2019-2024) and is projected to grow at a CAGR of xx% during the forecast period (2025-2033). Market penetration of premium alcoholic beverages is increasing steadily, indicating a move away from mass-market brands. Competitive dynamics are intense, with established multinational corporations and local players vying for market share through product innovation, marketing campaigns, and strategic partnerships. Consumer preferences are evolving towards healthier, more convenient, and experience-driven options.

Dominant Markets & Segments in South America Alcoholic Beverage Industry

Brazil dominates the South American alcoholic beverage market due to its large population, high alcohol consumption per capita, and established beverage industry. Other key markets include Mexico, Argentina, and Colombia, each with distinct characteristics and growth drivers.

- Product Type: Beer remains the largest segment, driven by high consumption and widespread availability. Wine consumption shows steady growth, particularly in countries like Argentina and Chile. The spirits segment is also expanding, with increased demand for premium tequilas, rums, and whiskeys.

- Distribution Channel: The off-trade channel (retail stores, supermarkets) holds the larger share, while the on-trade channel (restaurants, bars) is gradually expanding, reflecting changing consumption patterns.

Key Drivers of Market Dominance:

- Brazil: Large population, high per capita consumption, strong domestic industry.

- Argentina: Established wine industry, strong export markets, favorable climatic conditions.

- Mexico: Strong tequila production, high tourism, growing demand for premium spirits.

- Economic Policies: Taxation policies, trade agreements, and regulatory frameworks influence market dynamics.

- Infrastructure: Distribution networks, logistics, and cold chain infrastructure impact market access and product availability.

South America Alcoholic Beverage Industry Product Developments

Recent product innovations reflect a focus on premiumization, health consciousness, and convenience. The introduction of hard seltzers (as exemplified by Grupo Peñaflor's Mingo Hard Seltzer) and low-calorie beers caters to health-conscious consumers. New packaging formats and improved brewing/distilling techniques enhance product quality and consumer appeal. These developments highlight the industry's responsiveness to evolving consumer preferences and technological advancements.

Report Scope & Segmentation Analysis

This report segments the South American alcoholic beverage market by product type (Beer, Wine, Spirits) and distribution channel (On-trade, Off-trade). Each segment is analyzed based on historical performance, current market size (2025), and future growth projections (2025-2033). Competitive dynamics, including market share, pricing strategies, and innovation activities are examined for each segment.

Beer: The beer segment dominates the market and is expected to maintain its leading position. xx Million in 2025 and projected to reach xx Million by 2033.

Wine: The wine segment displays steady growth driven by premiumization and export opportunities. xx Million in 2025 and projected to reach xx Million by 2033.

Spirits: The spirits market shows a significant rise, propelled by the growing demand for premium products and innovative offerings. xx Million in 2025 and projected to reach xx Million by 2033.

On-trade: The on-trade channel is experiencing growth, albeit at a slower pace than the off-trade channel. xx Million in 2025 and projected to reach xx Million by 2033.

Off-trade: The off-trade channel continues to be the dominant distribution channel for alcoholic beverages. xx Million in 2025 and projected to reach xx Million by 2033.

Key Drivers of South America Alcoholic Beverage Industry Growth

Several key factors contribute to the growth of the South American alcoholic beverage market. These include:

- Rising Disposable Incomes: Increased purchasing power enables higher alcohol consumption.

- Expanding Middle Class: A growing middle class fuels demand for premium and diverse beverage choices.

- Urbanization: Increased urbanization leads to higher concentration of consumers and greater access to alcoholic beverages.

- Tourism: Tourism contributes to increased demand, particularly in key tourist destinations.

- Product Innovation: New product launches and improved product quality stimulate market expansion.

Challenges in the South America Alcoholic Beverage Industry Sector

The South American alcoholic beverage industry faces various challenges, including:

- Regulatory Hurdles: Varying regulations across countries pose complexities for manufacturers and distributors. Taxation policies and advertising restrictions significantly impact market dynamics.

- Supply Chain Issues: Infrastructure limitations and logistical challenges can disrupt supply chains and increase production costs. The impact is estimated at xx% in increased production cost (2024).

- Economic Volatility: Fluctuations in exchange rates and macroeconomic conditions affect consumer spending and industry profitability.

- Competition: Intense competition among multinational corporations and local players pressures profit margins.

Emerging Opportunities in South America Alcoholic Beverage Industry

Several emerging trends present significant opportunities for growth:

- Premiumization: Increased demand for premium and craft beverages creates opportunities for high-value products.

- Health and Wellness: Growing interest in health-conscious options opens doors for low-calorie, functional, and non-alcoholic beverages.

- E-commerce: Expanding online retail platforms offer new channels for distribution and consumer reach.

- Sustainability: Consumer preference for environmentally friendly products and sustainable practices create new market segments.

Leading Players in the South America Alcoholic Beverage Industry Market

- Anheuser-Busch InBev

- CCU S.A.

- Heineken N.V.

- Cervejaria Petropolis S/A

- Diageo

- Brown-Forman

- Molson Coors Beverage Company

- Companhia Muller de Bebidas

- Pernod Ricard

- Grupo Penaflor

Key Developments in South America Alcoholic Beverage Industry Industry

- November 2022: Diageo Plc acquired Balcones Distilling, expanding its presence in the American Single Malt Whisky market. This significantly impacts the premium spirits segment.

- February 2022: Grupo Peñaflor launched Mingo Hard Seltzer, tapping into the growing demand for ready-to-drink (RTD) beverages and potentially increasing competition within the category.

- November 2021: Grupo Petrópolis Ltda. launched a 100% malt edition of its Itaipava beer, enhancing its premium offerings and strengthening its position in the Brazilian market.

Strategic Outlook for South America Alcoholic Beverage Industry Market

The South American alcoholic beverage market presents a promising outlook. Continued economic growth, rising disposable incomes, and evolving consumer preferences will drive future expansion. Opportunities lie in premiumization, health-conscious options, e-commerce, and sustainable practices. Companies that adapt to changing market dynamics and embrace innovation will be well-positioned for success. The market is poised for further growth, with significant potential for both established players and new entrants.

South America Alcoholic Beverage Industry Segmentation

-

1. Product Type

- 1.1. Beer

- 1.2. Wine

- 1.3. Spirits

-

2. Distribution Channel

- 2.1. On-trade

- 2.2. Off-trade

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Rest of South America

South America Alcoholic Beverage Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Rest of South America

South America Alcoholic Beverage Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.23% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend

- 3.3. Market Restrains

- 3.3.1. Stringent Government Regulations and Product Guidelines

- 3.4. Market Trends

- 3.4.1. Brazil Dominates the Region

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Beer

- 5.1.2. Wine

- 5.1.3. Spirits

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-trade

- 5.2.2. Off-trade

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Brazil South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Beer

- 6.1.2. Wine

- 6.1.3. Spirits

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On-trade

- 6.2.2. Off-trade

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Argentina South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Beer

- 7.1.2. Wine

- 7.1.3. Spirits

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. On-trade

- 7.2.2. Off-trade

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Rest of South America South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Beer

- 8.1.2. Wine

- 8.1.3. Spirits

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. On-trade

- 8.2.2. Off-trade

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Brazil South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 10. Argentina South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 11. Rest of South America South America Alcoholic Beverage Industry Analysis, Insights and Forecast, 2019-2031

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Grupo Penaflor

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Anheuser-Busch InBev

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 CCU S A

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Heineken N V

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Cervejaria Petropolis S/A

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Diageo

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Brown-Forman

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Molson Coors Beverage Company*List Not Exhaustive

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Companhia Muller de Bebidas

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Pernod Ricard

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.1 Grupo Penaflor

List of Figures

- Figure 1: South America Alcoholic Beverage Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: South America Alcoholic Beverage Industry Share (%) by Company 2024

List of Tables

- Table 1: South America Alcoholic Beverage Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: South America Alcoholic Beverage Industry Volume liter Forecast, by Region 2019 & 2032

- Table 3: South America Alcoholic Beverage Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: South America Alcoholic Beverage Industry Volume liter Forecast, by Product Type 2019 & 2032

- Table 5: South America Alcoholic Beverage Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: South America Alcoholic Beverage Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 7: South America Alcoholic Beverage Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: South America Alcoholic Beverage Industry Volume liter Forecast, by Geography 2019 & 2032

- Table 9: South America Alcoholic Beverage Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: South America Alcoholic Beverage Industry Volume liter Forecast, by Region 2019 & 2032

- Table 11: South America Alcoholic Beverage Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: South America Alcoholic Beverage Industry Volume liter Forecast, by Country 2019 & 2032

- Table 13: Brazil South America Alcoholic Beverage Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Brazil South America Alcoholic Beverage Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 15: Argentina South America Alcoholic Beverage Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Argentina South America Alcoholic Beverage Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 17: Rest of South America South America Alcoholic Beverage Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of South America South America Alcoholic Beverage Industry Volume (liter ) Forecast, by Application 2019 & 2032

- Table 19: South America Alcoholic Beverage Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 20: South America Alcoholic Beverage Industry Volume liter Forecast, by Product Type 2019 & 2032

- Table 21: South America Alcoholic Beverage Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 22: South America Alcoholic Beverage Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 23: South America Alcoholic Beverage Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 24: South America Alcoholic Beverage Industry Volume liter Forecast, by Geography 2019 & 2032

- Table 25: South America Alcoholic Beverage Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: South America Alcoholic Beverage Industry Volume liter Forecast, by Country 2019 & 2032

- Table 27: South America Alcoholic Beverage Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 28: South America Alcoholic Beverage Industry Volume liter Forecast, by Product Type 2019 & 2032

- Table 29: South America Alcoholic Beverage Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 30: South America Alcoholic Beverage Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 31: South America Alcoholic Beverage Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 32: South America Alcoholic Beverage Industry Volume liter Forecast, by Geography 2019 & 2032

- Table 33: South America Alcoholic Beverage Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: South America Alcoholic Beverage Industry Volume liter Forecast, by Country 2019 & 2032

- Table 35: South America Alcoholic Beverage Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 36: South America Alcoholic Beverage Industry Volume liter Forecast, by Product Type 2019 & 2032

- Table 37: South America Alcoholic Beverage Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 38: South America Alcoholic Beverage Industry Volume liter Forecast, by Distribution Channel 2019 & 2032

- Table 39: South America Alcoholic Beverage Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 40: South America Alcoholic Beverage Industry Volume liter Forecast, by Geography 2019 & 2032

- Table 41: South America Alcoholic Beverage Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: South America Alcoholic Beverage Industry Volume liter Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Alcoholic Beverage Industry?

The projected CAGR is approximately 3.23%.

2. Which companies are prominent players in the South America Alcoholic Beverage Industry?

Key companies in the market include Grupo Penaflor, Anheuser-Busch InBev, CCU S A, Heineken N V, Cervejaria Petropolis S/A, Diageo, Brown-Forman, Molson Coors Beverage Company*List Not Exhaustive, Companhia Muller de Bebidas, Pernod Ricard.

3. What are the main segments of the South America Alcoholic Beverage Industry?

The market segments include Product Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend.

6. What are the notable trends driving market growth?

Brazil Dominates the Region.

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Product Guidelines.

8. Can you provide examples of recent developments in the market?

November 2022: Diageo Plc announced the acquisition of Balcones Distilling ('Balcones'), a Texas Craft Distiller. Balcones is one of the leading producers of American Single Malt Whisky.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Alcoholic Beverage Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Alcoholic Beverage Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Alcoholic Beverage Industry?

To stay informed about further developments, trends, and reports in the South America Alcoholic Beverage Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence