Key Insights

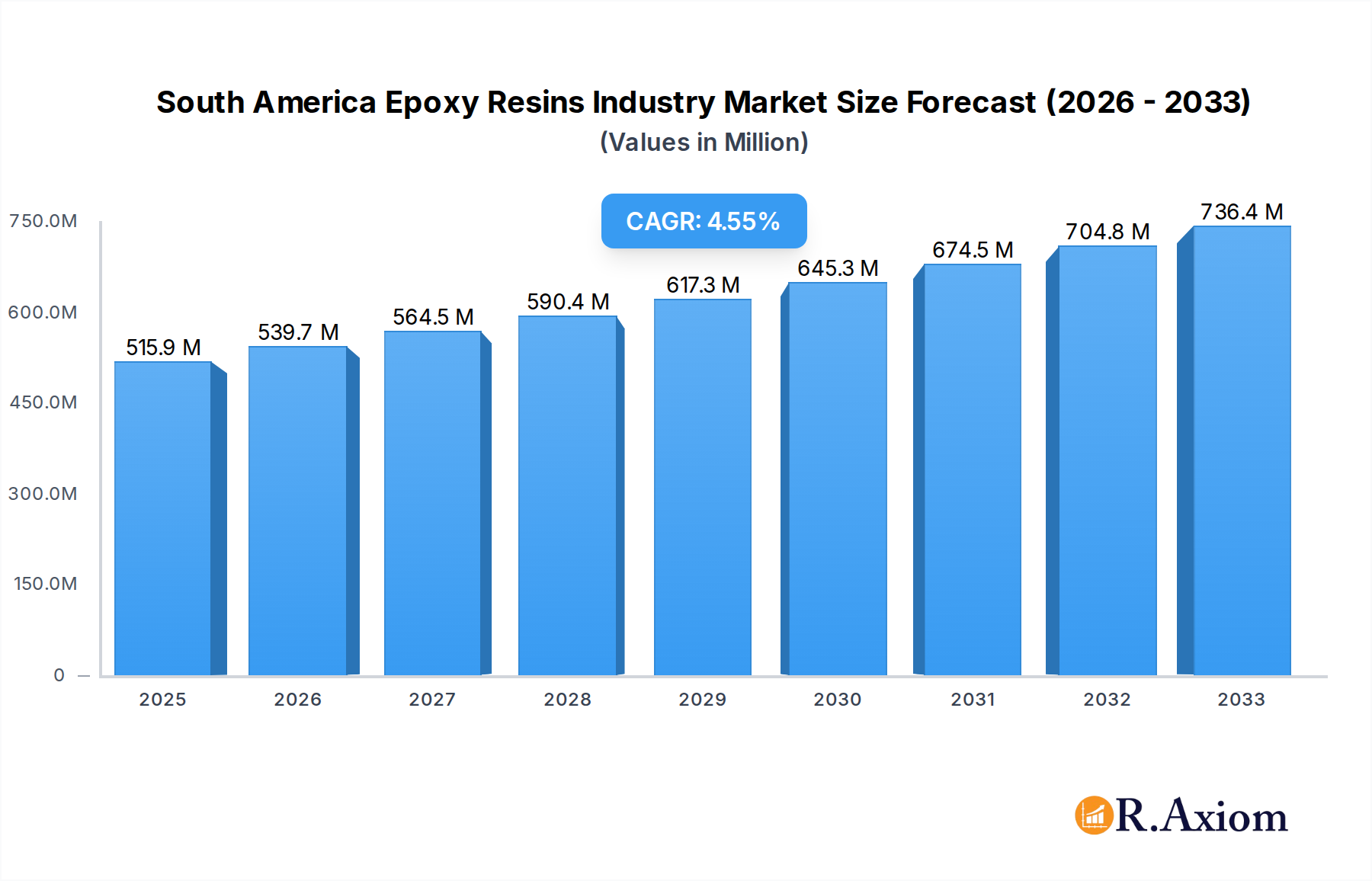

The South America Epoxy Resins Market is poised for significant expansion, projected to reach USD 515.9 million in 2025 and grow at a robust CAGR of 4.6% through 2033. This upward trajectory is primarily driven by burgeoning demand across key application sectors, particularly in paints and coatings, adhesives and sealants, and the rapidly advancing composites industry. The increasing adoption of advanced materials in infrastructure development, automotive manufacturing, and renewable energy projects, such as wind turbines, fuels the demand for high-performance epoxy resins. Furthermore, the growing electronics sector, requiring specialized epoxy formulations for insulation and protection, contributes substantially to market growth. Emerging economies within South America are witnessing increased industrialization and urbanization, directly translating into higher consumption of epoxy resin-based products.

South America Epoxy Resins Industry Market Size (In Million)

The market's growth, however, is not without its challenges. Fluctuations in the prices of key raw materials like Bisphenol A (BPA), Epichlorohydrin (ECH), and formaldehyde can impact profit margins for manufacturers. Environmental regulations concerning the use of certain chemicals, coupled with the inherent complexity and cost associated with some epoxy resin formulations, present potential restraints. Nevertheless, the industry is actively pursuing innovation, with a growing focus on developing bio-based and sustainable epoxy resin alternatives, alongside advancements in high-solid and low-VOC (Volatile Organic Compound) formulations. The diverse raw material landscape, encompassing DGBEA, DGBEF, Novolac, and Aliphatic epoxies, allows manufacturers to cater to a wide spectrum of application-specific requirements, ensuring continued market relevance and resilience.

South America Epoxy Resins Industry Company Market Share

South America Epoxy Resins Industry: Comprehensive Market Analysis and Forecast (2019-2033)

This in-depth report provides a thorough analysis of the South America epoxy resins industry, offering critical insights into market dynamics, growth trajectories, and strategic opportunities. The study covers the historical period from 2019 to 2024, with 2025 serving as the base and estimated year, and forecasts market performance through 2033. Leveraging high-traffic keywords such as "South America epoxy resins," "epoxy coatings market," "epoxy adhesives South America," "composite materials epoxy," and "electrical epoxy resins," this report is optimized for search engines and designed to engage industry stakeholders, including manufacturers, suppliers, investors, and end-users. The report meticulously examines market concentration, innovation, key trends, dominant segments, product developments, and strategic outlooks, providing actionable intelligence for informed decision-making in this rapidly evolving market.

South America Epoxy Resins Industry Market Concentration & Innovation

The South America epoxy resins market exhibits a moderate to high level of concentration, with key global players and emerging regional manufacturers vying for market share. Innovation remains a critical differentiator, driven by the demand for high-performance resins with enhanced properties such as improved chemical resistance, thermal stability, and faster curing times. Regulatory frameworks, particularly concerning environmental impact and material safety, are increasingly shaping product development and market entry strategies. The threat of product substitutes, such as polyurethanes and acrylics, necessitates continuous innovation in epoxy resin formulations to maintain competitive advantages. End-user trends, particularly the growing preference for sustainable and bio-based epoxy resins, are influencing R&D investments. Mergers and acquisitions (M&A) activities, while less prevalent than in more mature markets, are strategically employed by leading companies to expand their geographical reach and product portfolios. For instance, strategic partnerships aimed at technology transfer or market access are becoming more common. The market share of leading players is estimated to be substantial, with the top five companies collectively holding over 50% of the market value in 2025. M&A deal values, where publicly disclosed, are expected to range from tens to hundreds of millions for significant acquisitions.

South America Epoxy Resins Industry Industry Trends & Insights

The South America epoxy resins industry is poised for robust growth, driven by a confluence of factors including escalating demand from key application sectors, ongoing infrastructure development, and advancements in manufacturing technologies. The Compound Annual Growth Rate (CAGR) for the overall market is projected to be approximately 5.8% during the forecast period of 2025-2033. Technological disruptions are transforming the industry, with a growing emphasis on advanced curing technologies, nanoparticle integration for enhanced mechanical properties, and the development of low-VOC (Volatile Organic Compound) epoxy formulations to meet stringent environmental regulations. Consumer preferences are shifting towards more durable, sustainable, and aesthetically appealing products, directly impacting the demand for specialized epoxy resins in sectors like construction, automotive, and consumer electronics. Competitive dynamics are characterized by intense price competition, a focus on product differentiation, and strategic collaborations between raw material suppliers and epoxy resin manufacturers. Market penetration is deepening across various end-use industries, fueled by the superior performance characteristics of epoxy resins compared to traditional materials. The increasing adoption of high-performance composites in aerospace and wind energy sectors, alongside the sustained demand for protective coatings and advanced adhesives, are significant market drivers. The rise of smart cities and the need for resilient infrastructure further contribute to the positive market outlook for epoxy resins in South America.

Dominant Markets & Segments in South America Epoxy Resins Industry

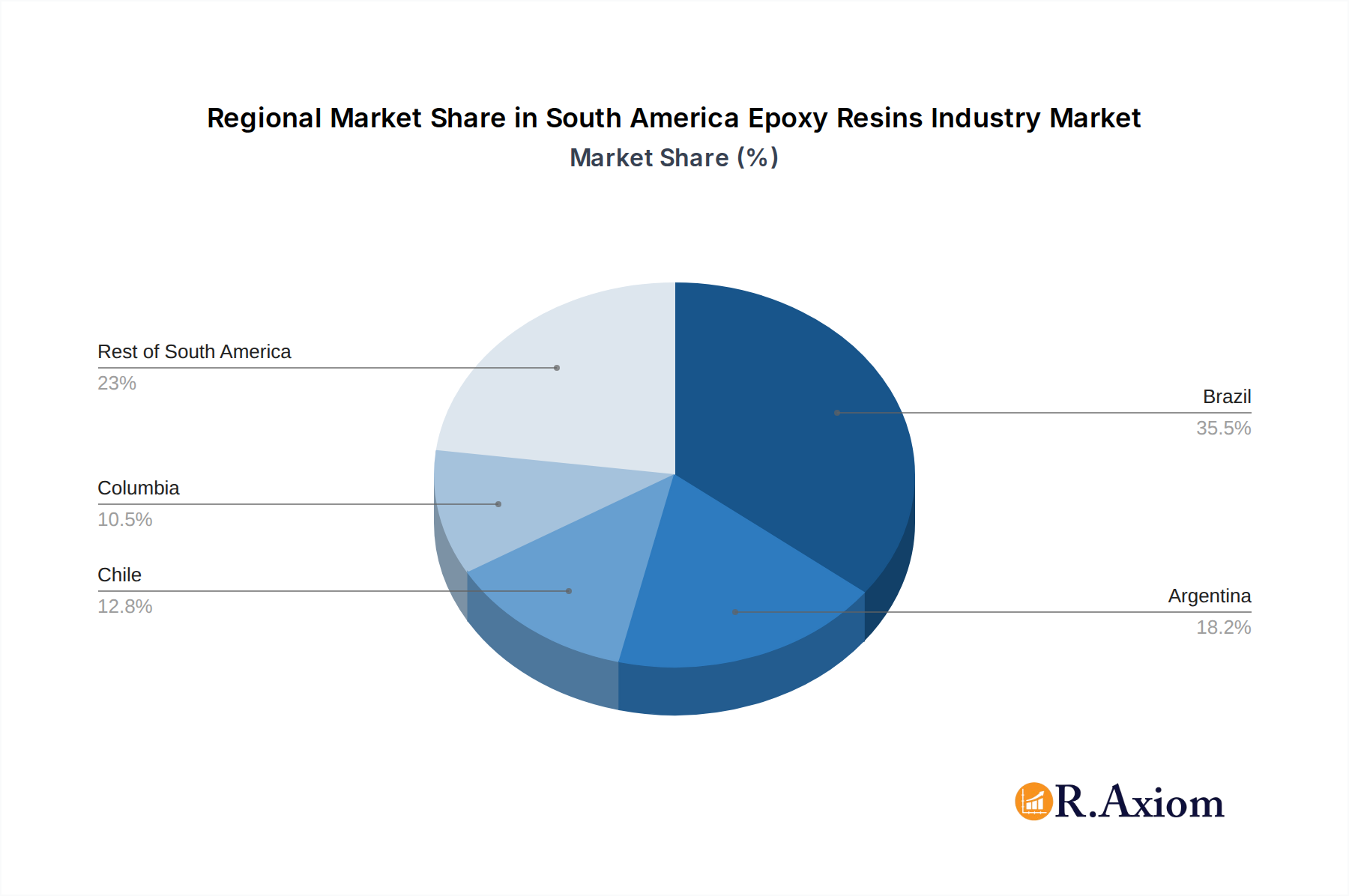

The South America epoxy resins industry's dominance is clearly defined by its leading geographical markets, key raw material segments, and high-growth application sectors. Brazil stands out as the most dominant market, driven by its large industrial base, extensive infrastructure projects, and significant manufacturing activities in sectors such as automotive, construction, and paints and coatings. Argentina and Colombia are also significant contributors, with their respective industrial and construction sectors showing steady growth. The Rest of South America, encompassing countries like Chile and Peru, is emerging as a region with substantial untapped potential, particularly in mining, infrastructure, and renewable energy initiatives.

Raw Material Dominance:

- DGBEA (Bisphenol A and ECH): This remains the most dominant raw material segment due to its widespread use in general-purpose epoxy resins, which are extensively employed in paints, coatings, and adhesives. Its cost-effectiveness and versatility contribute to its leading position.

- DGBEF (Bisphenol F and ECH): While not as dominant as DGBEA, DGBEF is gaining traction due to its superior chemical resistance and lower viscosity, making it ideal for high-performance applications such as industrial coatings and composites.

- Novolac (Formaldehyde and Phenols): This segment is crucial for high-temperature and chemically resistant applications, particularly in specialized coatings, electrical laminates, and molding compounds.

- Aliphatic (Aliphatic Alcohols): These are increasingly used in UV-curable coatings and flexible adhesives, catering to the growing demand for environmentally friendly and fast-curing solutions.

- Glycidylamine (Aromatic Amines and ECH): This segment is critical for applications requiring exceptional thermal stability and electrical insulation properties, such as in the electrical and electronics industry.

Application Dominance:

- Paints and Coatings: This is the largest and most dominant application segment, propelled by the construction industry's demand for protective and decorative coatings, as well as the automotive sector's need for durable finishes and anti-corrosion solutions. The market size for epoxy coatings is estimated to be over 1.5 billion dollars in 2025.

- Adhesives and Sealants: The growing demand for high-strength, durable bonding solutions in construction, automotive assembly, and consumer goods manufacturing makes this a significant and rapidly expanding segment.

- Composites: The increasing use of lightweight and high-strength composite materials in sectors like wind energy (wind turbines), aerospace, and sporting goods is a major growth driver for epoxy resins. The wind turbine segment alone is expected to contribute significantly to epoxy resin consumption.

- Electrical and Electronics: Epoxy resins are indispensable for encapsulation, insulation, and circuit board manufacturing due to their excellent dielectric properties and thermal resistance.

- Wind Turbines: This segment represents a high-growth area for epoxy resins, driven by the global push for renewable energy and the large-scale manufacturing of wind turbine blades.

South America Epoxy Resins Industry Product Developments

Product development in the South America epoxy resins industry is characterized by a strong focus on sustainability, enhanced performance, and specialized applications. Innovations are emerging in bio-based epoxy resins derived from renewable sources, offering a more environmentally friendly alternative. Advancements in nanoparticle-reinforced epoxy systems are yielding materials with significantly improved mechanical strength, abrasion resistance, and thermal conductivity. The development of faster-curing epoxy formulations is catering to the need for increased production efficiency in sectors like automotive and construction. Furthermore, tailor-made epoxy systems with specific functionalities, such as flame retardancy, UV resistance, and anti-microbial properties, are being introduced to meet niche market demands and provide competitive advantages to end-users.

Report Scope & Segmentation Analysis

This report meticulously analyzes the South America epoxy resins industry across several key segmentation dimensions, providing detailed market size estimations and growth projections. The Raw Material segmentation includes DGBEA (Bisphenol A and ECH), DGBEF (Bisphenol F and ECH), Novolac (Formaldehyde and Phenols), Aliphatic (Aliphatic Alcohols), Glycidylamine (Aromatic Amines and ECH), and Other Raw Materials, with DGBEA expected to maintain the largest market share, projected to reach over 800 million dollars by 2025. The Application segmentation encompasses Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, Wind Turbines, and Other Applications, with Paints and Coatings forecasted to dominate, followed closely by Composites and Adhesives. The Geography segmentation divides the market into Brazil, Argentina, Chile, Colombia, and Rest of South America. Brazil is projected to lead the market, with an estimated market size of over 1.2 billion dollars in 2025, driven by strong industrial and construction activity.

Key Drivers of South America Epoxy Resins Industry Growth

The growth of the South America epoxy resins industry is propelled by several interconnected factors. The burgeoning construction sector, fueled by urbanization and infrastructure development projects across the region, is a primary driver for epoxy-based paints, coatings, and adhesives. The expanding manufacturing base, particularly in the automotive and electronics industries, demands high-performance epoxy resins for assembly, encapsulation, and insulation. The global and regional push towards renewable energy sources, especially wind power, significantly boosts the demand for epoxy resins in the manufacturing of wind turbine blades. Furthermore, technological advancements leading to the development of more sustainable, high-performance, and cost-effective epoxy formulations are expanding their applicability across various sectors. Government initiatives promoting industrial growth and investment also play a crucial role.

Challenges in the South America Epoxy Resins Industry Sector

Despite its growth potential, the South America epoxy resins industry faces several challenges. Fluctuations in the prices of key raw materials, such as Bisphenol A and epichlorohydrin, can impact profit margins and necessitate adaptive pricing strategies. Stringent environmental regulations and increasing consumer demand for eco-friendly products require continuous investment in research and development for sustainable alternatives. Supply chain disruptions, particularly in the post-pandemic era, can affect the availability and timely delivery of raw materials and finished products. Intense competition, both from established global players and emerging regional manufacturers, can lead to price wars and pressure on profitability. Furthermore, the relatively underdeveloped logistics infrastructure in certain parts of the region can add to operational costs and delays.

Emerging Opportunities in South America Epoxy Resins Industry

The South America epoxy resins industry presents several emerging opportunities for growth and innovation. The increasing adoption of electric vehicles (EVs) in the region is creating new demand for lightweight composite materials and advanced adhesives in automotive manufacturing. The growing awareness and investment in renewable energy infrastructure, beyond wind turbines, such as solar panel manufacturing, also present opportunities for epoxy resin applications. The development and commercialization of bio-based and recycled epoxy resins are tapping into the growing market for sustainable materials. Furthermore, the expansion of the medical device industry and the demand for specialized coatings and adhesives in this sector offer significant potential. Digitalization and the implementation of Industry 4.0 principles in manufacturing processes can enhance efficiency and reduce costs, opening up new avenues for competitive advantage.

Leading Players in the South America Epoxy Resins Industry Market

- Olin Corporation

- DuPont de Nemours Inc

- 3M

- BASF SE

- Huntsman International LLC

- Aditya Birla Chemicals

- Daicel Corporation

- Hexion

- Covestro AG

- Spolchemie

Key Developments in South America Epoxy Resins Industry Industry

- 2023: Several companies focused on R&D for bio-based epoxy resins to meet growing sustainability demands.

- 2022: Increased strategic partnerships between raw material suppliers and epoxy resin manufacturers to secure supply chains.

- 2021: Introduction of advanced nanoparticle-infused epoxy resins offering enhanced mechanical properties for composite applications.

- 2020: Focus on developing low-VOC and faster-curing epoxy formulations to align with stricter environmental regulations.

- 2019: Expansion of production capacities by key players to meet the rising demand from the construction and automotive sectors.

Strategic Outlook for South America Epoxy Resins Industry Market

The strategic outlook for the South America epoxy resins industry is overwhelmingly positive, driven by sustained demand from core applications and the emergence of new growth frontiers. Companies that prioritize innovation, particularly in sustainable and high-performance epoxy formulations, will be well-positioned to capture market share. Strategic investments in expanding production capacities and optimizing supply chains will be crucial for maintaining competitiveness. Furthermore, exploring strategic alliances and partnerships to access new markets, technologies, and distribution channels will be key to long-term success. The industry's ability to adapt to evolving regulatory landscapes and capitalize on the increasing demand for advanced materials in sectors like renewable energy and electric mobility will define its trajectory in the coming years.

South America Epoxy Resins Industry Segmentation

-

1. Raw Material

- 1.1. DGBEA (Bisphenol A and ECH)

- 1.2. DGBEF (Bisphenol F and ECH)

- 1.3. Novolac (Formaldehyde and Phenols)

- 1.4. Aliphatic (Aliphatic Alcohols)

- 1.5. Glycidylamine (Aromatic Amines and ECH)

- 1.6. Other Raw Materials

-

2. Application

- 2.1. Paints and Coatings

- 2.2. Adhesives and Sealants

- 2.3. Composites

- 2.4. Electrical and Electronics

- 2.5. Wind Turbines

- 2.6. Other Applications

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Chile

- 3.4. Columbia

- 3.5. Rest of South America

South America Epoxy Resins Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Chile

- 4. Columbia

- 5. Rest of South America

South America Epoxy Resins Industry Regional Market Share

Geographic Coverage of South America Epoxy Resins Industry

South America Epoxy Resins Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 5.1.1. DGBEA (Bisphenol A and ECH)

- 5.1.2. DGBEF (Bisphenol F and ECH)

- 5.1.3. Novolac (Formaldehyde and Phenols)

- 5.1.4. Aliphatic (Aliphatic Alcohols)

- 5.1.5. Glycidylamine (Aromatic Amines and ECH)

- 5.1.6. Other Raw Materials

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Paints and Coatings

- 5.2.2. Adhesives and Sealants

- 5.2.3. Composites

- 5.2.4. Electrical and Electronics

- 5.2.5. Wind Turbines

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Chile

- 5.3.4. Columbia

- 5.3.5. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Chile

- 5.4.4. Columbia

- 5.4.5. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 6. South America Epoxy Resins Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 6.1.1. DGBEA (Bisphenol A and ECH)

- 6.1.2. DGBEF (Bisphenol F and ECH)

- 6.1.3. Novolac (Formaldehyde and Phenols)

- 6.1.4. Aliphatic (Aliphatic Alcohols)

- 6.1.5. Glycidylamine (Aromatic Amines and ECH)

- 6.1.6. Other Raw Materials

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Paints and Coatings

- 6.2.2. Adhesives and Sealants

- 6.2.3. Composites

- 6.2.4. Electrical and Electronics

- 6.2.5. Wind Turbines

- 6.2.6. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Chile

- 6.3.4. Columbia

- 6.3.5. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 7. Brazil South America Epoxy Resins Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 7.1.1. DGBEA (Bisphenol A and ECH)

- 7.1.2. DGBEF (Bisphenol F and ECH)

- 7.1.3. Novolac (Formaldehyde and Phenols)

- 7.1.4. Aliphatic (Aliphatic Alcohols)

- 7.1.5. Glycidylamine (Aromatic Amines and ECH)

- 7.1.6. Other Raw Materials

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Paints and Coatings

- 7.2.2. Adhesives and Sealants

- 7.2.3. Composites

- 7.2.4. Electrical and Electronics

- 7.2.5. Wind Turbines

- 7.2.6. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Chile

- 7.3.4. Columbia

- 7.3.5. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 8. Argentina South America Epoxy Resins Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 8.1.1. DGBEA (Bisphenol A and ECH)

- 8.1.2. DGBEF (Bisphenol F and ECH)

- 8.1.3. Novolac (Formaldehyde and Phenols)

- 8.1.4. Aliphatic (Aliphatic Alcohols)

- 8.1.5. Glycidylamine (Aromatic Amines and ECH)

- 8.1.6. Other Raw Materials

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Paints and Coatings

- 8.2.2. Adhesives and Sealants

- 8.2.3. Composites

- 8.2.4. Electrical and Electronics

- 8.2.5. Wind Turbines

- 8.2.6. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Chile

- 8.3.4. Columbia

- 8.3.5. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 9. Chile South America Epoxy Resins Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 9.1.1. DGBEA (Bisphenol A and ECH)

- 9.1.2. DGBEF (Bisphenol F and ECH)

- 9.1.3. Novolac (Formaldehyde and Phenols)

- 9.1.4. Aliphatic (Aliphatic Alcohols)

- 9.1.5. Glycidylamine (Aromatic Amines and ECH)

- 9.1.6. Other Raw Materials

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Paints and Coatings

- 9.2.2. Adhesives and Sealants

- 9.2.3. Composites

- 9.2.4. Electrical and Electronics

- 9.2.5. Wind Turbines

- 9.2.6. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Chile

- 9.3.4. Columbia

- 9.3.5. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 10. Columbia South America Epoxy Resins Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 10.1.1. DGBEA (Bisphenol A and ECH)

- 10.1.2. DGBEF (Bisphenol F and ECH)

- 10.1.3. Novolac (Formaldehyde and Phenols)

- 10.1.4. Aliphatic (Aliphatic Alcohols)

- 10.1.5. Glycidylamine (Aromatic Amines and ECH)

- 10.1.6. Other Raw Materials

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Paints and Coatings

- 10.2.2. Adhesives and Sealants

- 10.2.3. Composites

- 10.2.4. Electrical and Electronics

- 10.2.5. Wind Turbines

- 10.2.6. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. Brazil

- 10.3.2. Argentina

- 10.3.3. Chile

- 10.3.4. Columbia

- 10.3.5. Rest of South America

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 11. Rest of South America South America Epoxy Resins Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Raw Material

- 11.1.1. DGBEA (Bisphenol A and ECH)

- 11.1.2. DGBEF (Bisphenol F and ECH)

- 11.1.3. Novolac (Formaldehyde and Phenols)

- 11.1.4. Aliphatic (Aliphatic Alcohols)

- 11.1.5. Glycidylamine (Aromatic Amines and ECH)

- 11.1.6. Other Raw Materials

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Paints and Coatings

- 11.2.2. Adhesives and Sealants

- 11.2.3. Composites

- 11.2.4. Electrical and Electronics

- 11.2.5. Wind Turbines

- 11.2.6. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. Brazil

- 11.3.2. Argentina

- 11.3.3. Chile

- 11.3.4. Columbia

- 11.3.5. Rest of South America

- 11.1. Market Analysis, Insights and Forecast - by Raw Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Olin Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 DuPont de Nemours Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 3M

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BASF SE

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Huntsman International LLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Aditya Birla Chemicals

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Daicel Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hexion

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Covestro AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Spolchemie*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Olin Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: South America Epoxy Resins Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America Epoxy Resins Industry Share (%) by Company 2025

List of Tables

- Table 1: South America Epoxy Resins Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 2: South America Epoxy Resins Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: South America Epoxy Resins Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: South America Epoxy Resins Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: South America Epoxy Resins Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 6: South America Epoxy Resins Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: South America Epoxy Resins Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: South America Epoxy Resins Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: South America Epoxy Resins Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 10: South America Epoxy Resins Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: South America Epoxy Resins Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: South America Epoxy Resins Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: South America Epoxy Resins Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 14: South America Epoxy Resins Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: South America Epoxy Resins Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: South America Epoxy Resins Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: South America Epoxy Resins Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 18: South America Epoxy Resins Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: South America Epoxy Resins Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: South America Epoxy Resins Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: South America Epoxy Resins Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 22: South America Epoxy Resins Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: South America Epoxy Resins Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: South America Epoxy Resins Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Epoxy Resins Industry?

The projected CAGR is approximately 6.62%.

2. Which companies are prominent players in the South America Epoxy Resins Industry?

Key companies in the market include Olin Corporation, DuPont de Nemours Inc, 3M, BASF SE, Huntsman International LLC, Aditya Birla Chemicals, Daicel Corporation, Hexion, Covestro AG, Spolchemie*List Not Exhaustive.

3. What are the main segments of the South America Epoxy Resins Industry?

The market segments include Raw Material, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.84 billion as of 2022.

5. What are some drivers contributing to market growth?

; Strong Growth of the Construction Industry; Other Drivers.

6. What are the notable trends driving market growth?

Paints and Coatings Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

; Impact of COVID-19 Pandemic; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Epoxy Resins Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Epoxy Resins Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Epoxy Resins Industry?

To stay informed about further developments, trends, and reports in the South America Epoxy Resins Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence