Key Insights

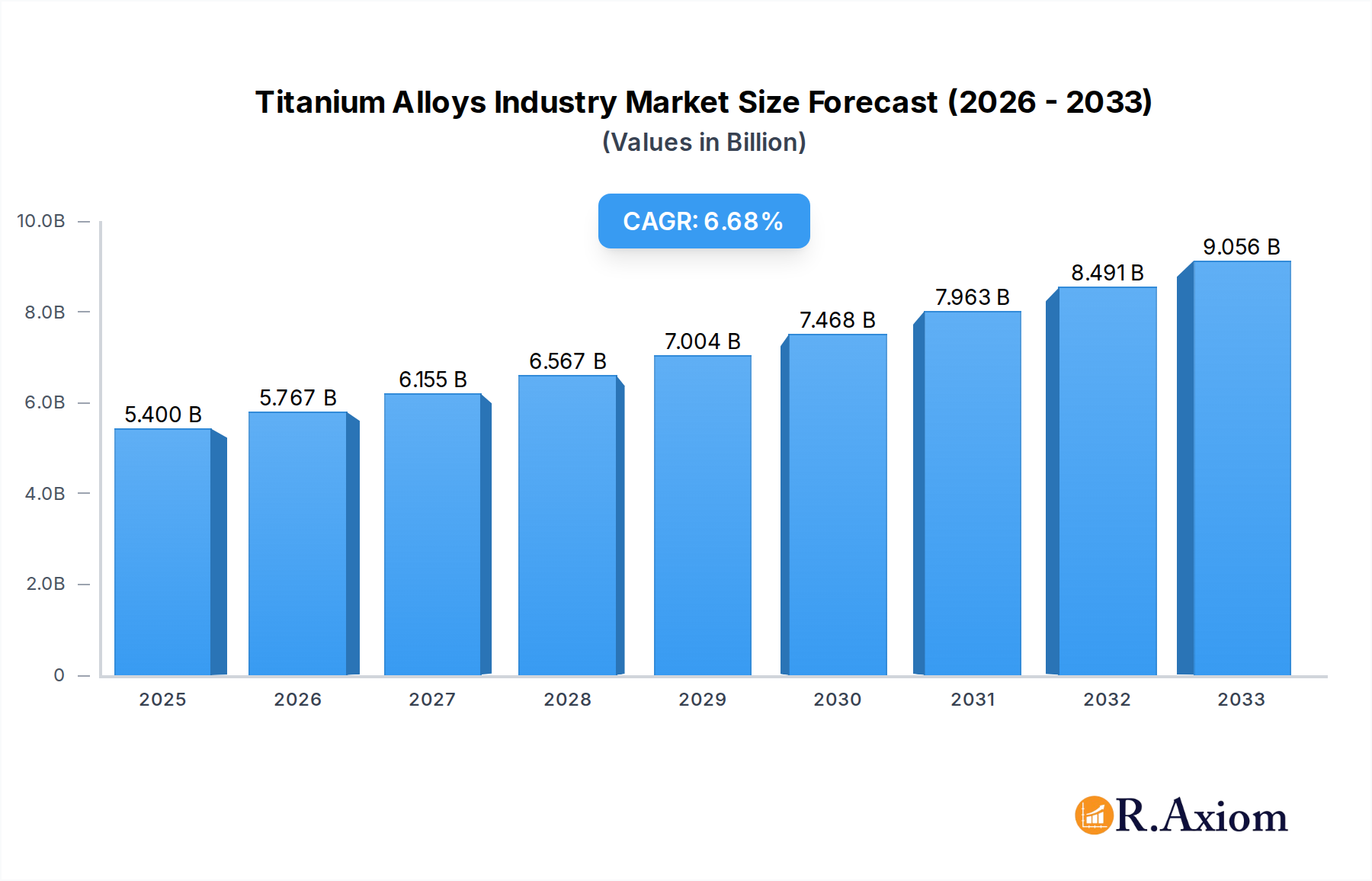

The global Titanium Alloys market is poised for significant expansion, projected to reach USD 5.4 billion in 2025 and accelerate at a robust CAGR of 6.8% through 2033. This growth is primarily fueled by escalating demand from the aerospace sector, driven by advancements in aircraft manufacturing and the increasing production of commercial and defense aircraft. The automotive industry is also emerging as a key consumer, seeking lightweight and high-strength materials to enhance fuel efficiency and performance, while shipbuilding and chemical processing industries also contribute to sustained demand due to titanium's exceptional corrosion resistance and durability in harsh environments. Emerging applications in medical implants and consumer electronics further bolster market prospects.

Titanium Alloys Industry Market Size (In Billion)

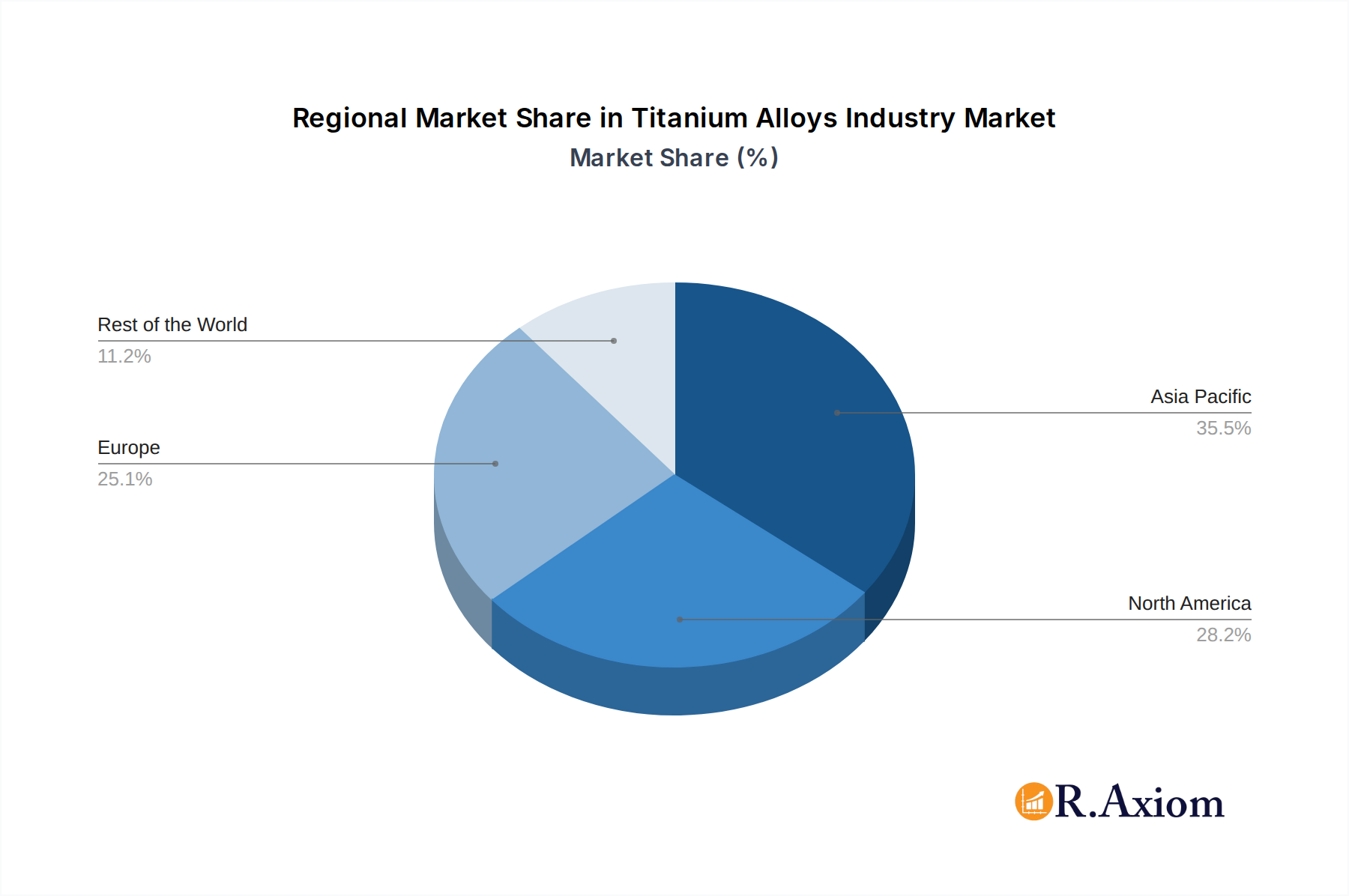

The market is characterized by distinct microstructure segments: Alpha and Near-alpha Alloys, Alpha-beta Alloys, and Beta Alloys, each catering to specific performance requirements. Geographically, Asia Pacific is expected to dominate the market, propelled by rapid industrialization and significant investments in aerospace and automotive manufacturing in countries like China and India. North America, with its established aerospace and defense industries, will remain a crucial market. Key players such as ATI, KOBE STEEL LTD, and VSMPO-AVISMA Corporation are actively engaged in research and development, expanding production capacities, and strategic collaborations to capitalize on these growth opportunities. Despite the positive outlook, the high cost of raw materials and complex manufacturing processes present potential restraints, necessitating innovation in production techniques and material sourcing to maintain competitive pricing.

Titanium Alloys Industry Company Market Share

This in-depth market research report provides a definitive analysis of the global titanium alloys market, projecting its trajectory from 2019 to 2033. With a base year of 2025, the report leverages comprehensive historical data (2019–2024) and detailed forecast insights (2025–2033) to offer actionable intelligence for industry stakeholders. We delve into market dynamics, technological advancements, competitive landscapes, and emerging opportunities within this high-value sector, vital for sectors like aerospace manufacturing, automotive innovation, and power generation.

Titanium Alloys Industry Market Concentration & Innovation

The global titanium alloys market exhibits a moderate to high concentration, with a few key players dominating a significant portion of the market share. Innovation remains a critical driver, fueled by the relentless demand for advanced materials with superior strength-to-weight ratios, corrosion resistance, and biocompatibility. Research and development efforts are primarily focused on enhancing alloy properties, improving manufacturing processes, and expanding applications into novel domains. Regulatory frameworks, particularly within the aerospace and medical sectors, play a crucial role in shaping product development and market access, ensuring stringent quality and safety standards. While product substitutes exist in certain applications, the unique performance characteristics of titanium alloys often make them indispensable. End-user trends are increasingly leaning towards lighter, more durable, and more efficient materials, directly benefiting the titanium industry. Mergers and acquisitions (M&A) activity, though not consistently high, are strategic moves by leading companies to consolidate market position, acquire new technologies, and expand geographical reach. M&A deal values are expected to see a steady rise as companies seek to secure critical supply chains and enhance their competitive edge. For instance, potential M&A activities could revolve around consolidating raw material sourcing or acquiring specialized manufacturing capabilities. The market share of leading players is anticipated to remain robust, with innovation acting as a key differentiator in capturing incremental growth.

Titanium Alloys Industry Industry Trends & Insights

The global titanium alloys market is poised for robust growth, driven by several compelling trends and insights. A significant growth driver is the escalating demand from the aerospace industry, where titanium alloys are indispensable for manufacturing aircraft components due to their exceptional strength-to-weight ratio, fuel efficiency benefits, and resistance to extreme temperatures and corrosive environments. The increasing production of commercial aircraft and the ongoing advancements in defense aviation are directly fueling this demand. The automotive sector is also emerging as a significant consumer, with manufacturers exploring titanium alloys for performance-enhancing applications, lightweighting initiatives to improve fuel economy and reduce emissions, and in high-performance vehicles. The medical industry continues to rely heavily on biocompatible titanium alloys for implants, prosthetics, and surgical instruments, creating a stable and growing segment. Furthermore, the expanding applications in power and desalination plants, owing to titanium's superior corrosion resistance in harsh environments, are contributing to market expansion. Technological disruptions, such as advancements in additive manufacturing (3D printing) of titanium alloys, are revolutionizing prototyping and complex part fabrication, leading to reduced waste and faster production cycles. The market penetration of titanium alloys is expected to deepen across existing and new applications as cost-optimization measures and manufacturing efficiencies improve. The compound annual growth rate (CAGR) for the titanium alloys industry is projected to remain strong throughout the forecast period, reflecting sustained demand and ongoing innovation. The competitive dynamics are characterized by a focus on product quality, technological superiority, supply chain reliability, and strategic partnerships, especially between raw material suppliers and component manufacturers. The increasing emphasis on sustainability and circular economy principles is also influencing manufacturing processes and material sourcing strategies within the titanium market.

Dominant Markets & Segments in Titanium Alloys Industry

The global titanium alloys market is characterized by dominant players across specific regions and end-user industries, driven by unique economic policies, infrastructure development, and technological adoption rates.

Dominant Regions:

- North America and Europe currently lead the titanium alloys market owing to their well-established aerospace and defense industries, coupled with significant investments in advanced manufacturing and research & development. Stringent quality standards and the presence of major aircraft manufacturers and tier-1 suppliers in these regions contribute to their dominance.

- Asia-Pacific is emerging as a high-growth region, driven by the expanding aerospace sector in countries like China and India, coupled with a growing automotive manufacturing base and increasing infrastructure projects that require corrosion-resistant materials. Government initiatives promoting domestic manufacturing and technological self-sufficiency are also key drivers.

Dominant End-user Industries:

- Aerospace: This segment consistently holds the largest market share. The unparalleled strength-to-weight ratio, fatigue resistance, and high-temperature performance of titanium alloys make them indispensable for critical aircraft components such as engine parts, airframes, landing gear, and fasteners. The continuous development of new aircraft models and the need for lighter, more fuel-efficient designs will sustain its dominance.

- Automotive and Shipbuilding: While smaller than aerospace, these sectors are showing significant growth potential. In automotive, lightweighting for improved fuel efficiency and performance in high-end vehicles is driving adoption. In shipbuilding, the need for corrosion-resistant materials in marine environments for structural components and offshore platforms is a key factor.

- Chemical: Titanium alloys' exceptional corrosion resistance makes them ideal for use in highly corrosive chemical processing equipment, such as heat exchangers, reactors, and pipelines, where they outperform many other metals.

- Power and Desalination: The increasing global demand for clean energy and freshwater is boosting the use of titanium alloys in power generation (especially nuclear and thermal) and desalination plants due to their ability to withstand aggressive environments and high temperatures.

Dominant Microstructure Segments:

- Alpha and Near-alpha Alloys: These alloys offer excellent weldability, strength at elevated temperatures, and good creep resistance, making them vital for jet engine components, airframes, and chemical processing equipment. Their reliability in demanding applications contributes to their significant market share.

- Alpha-beta Alloys: These alloys provide a balance of high strength, ductility, and formability, making them versatile for a wide range of applications, including aircraft structures, automotive components, and medical implants. Their adaptability to various manufacturing processes enhances their market presence.

- Beta Alloys: Known for their high strength, toughness, and hardenability, beta alloys are increasingly used in critical structural applications where maximum performance is required, such as in highly stressed aerospace components and specialized medical devices.

Titanium Alloys Industry Product Developments

Product developments in the titanium alloys industry are centered on enhancing material properties and expanding their application spectrum. Innovations focus on creating alloys with improved high-temperature strength, enhanced fatigue life, and superior corrosion resistance for demanding aerospace and industrial applications. Advancements in additive manufacturing are enabling the production of complex, lightweight titanium alloy components with reduced material waste and faster lead times, revolutionizing prototyping and bespoke part creation for the aerospace, automotive, and medical sectors. Furthermore, the development of cost-effective titanium alloy production methods and recycling technologies aims to increase market accessibility and sustainability, making these advanced materials viable for a broader range of industries.

Report Scope & Segmentation Analysis

This report comprehensively segments the global titanium alloys market across key dimensions. The microstructure segmentation includes Alpha and Near-alpha Alloys, Alpha-beta Alloys, and Beta Alloys, each with specific mechanical properties and optimal applications. The end-user industry segmentation encompasses Aerospace, Automotive and Shipbuilding, Chemical, Power and Desalination, and Other End-user Industries. Each segment is analyzed for its market size, growth projections, and competitive dynamics. For instance, the Aerospace segment is projected to witness substantial market size and steady growth due to continued demand for lightweight and high-strength materials in aircraft manufacturing. The Automotive and Shipbuilding segment, while smaller, is expected to show a higher CAGR as titanium alloys find new applications in vehicle lightweighting and marine infrastructure. The Chemical and Power and Desalination segments represent stable markets with consistent demand driven by the need for corrosion resistance.

Key Drivers of Titanium Alloys Industry Growth

The titanium alloys industry is propelled by several key growth drivers. The ever-increasing demand from the aerospace sector for lighter, stronger materials to improve fuel efficiency and performance in commercial and defense aircraft is paramount. Technological advancements, particularly in additive manufacturing (3D printing), are enabling novel applications and faster production of complex titanium alloy parts. The growing trend of lightweighting in the automotive industry to meet stringent fuel economy and emission standards also significantly boosts demand. Furthermore, the superior corrosion resistance of titanium alloys makes them indispensable in harsh environments found in chemical processing, power generation, and desalination plants. Government support for advanced manufacturing and defense industries in various regions further underpins market expansion.

Challenges in the Titanium Alloys Industry Sector

Despite its growth prospects, the titanium alloys industry sector faces notable challenges. The high cost of raw material extraction and processing remains a significant barrier to widespread adoption, especially in cost-sensitive applications. The complex and energy-intensive manufacturing processes further contribute to the overall expense. Supply chain volatility, including the availability of critical raw materials and geopolitical factors, can impact production and pricing. Stringent quality control and certification requirements, particularly in the aerospace and medical industries, necessitate substantial investment and can lead to longer lead times. Competition from other advanced materials, though often not direct substitutes, also presents a challenge in specific applications.

Emerging Opportunities in Titanium Alloys Industry

Emerging opportunities within the titanium alloys industry are abundant, driven by innovation and evolving market needs. The increasing adoption of additive manufacturing (3D printing) for complex titanium alloy components is opening new avenues in aerospace, medical implants, and custom automotive parts, promising faster development cycles and reduced material waste. The expanding use of titanium alloys in the renewable energy sector, such as in offshore wind turbines and geothermal energy systems, presents a significant growth area due to their corrosion resistance and durability. The continued development of new alloy compositions with enhanced properties tailored for specific applications, coupled with advancements in recycling technologies, will improve cost-effectiveness and sustainability. The growing demand for high-performance materials in medical devices and prosthetics, driven by an aging global population, offers a stable and expanding market.

Leading Players in the Titanium Alloys Industry Market

- Hermith GmbH

- BRISMET

- Weber Metals (OTTO FUCHS COMPANY)

- Perryman Company

- KOBE STEEL LTD

- ATI

- Daido Steel Co Ltd

- Toho Titanium Co Ltd

- VSMPO-AVISMA Corporation

- Howmet Aerospace

- CRS Holdings LLC

- Eramet

- M/s Bansal Brothers

- AMG Advanced Metallurgical Group N V

- Mishra Dhatu Nigam Limited

- TIMET (Precision Castparts Corp)

Key Developments in Titanium Alloys Industry Industry

- November 2022: PTC Industries and Defence PSU Mishra Dhatu Nigam (MIDHANI) signed a memorandum of understanding (MOU) for a technological partnership. This collaboration aims to leverage each other's resources for manufacturing titanium alloy pipes and tubes from locally processed raw materials, producing titanium alloy plates and sheets, and fabricating critical parts and LRUs for the defense and aerospace industries using PTC's machining facilities and Midhani's forged and rolled products. This development is crucial for enhancing domestic manufacturing capabilities and reducing reliance on imports for critical defense components.

- July 2022: Perryman Company, Houston, Pa., announced plans to significantly expand its titanium melting capacity by installing additional electron beam and vacuum arc remelt furnaces in Washington County, Pennsylvania. This expansion is set to increase Perryman's overall titanium melting capacity to 42 million pounds, adding an additional 16 million pounds. This strategic move solidifies Perryman's position as a global leader in titanium melting, particularly for the aerospace and medical sectors, ensuring greater supply capacity for high-demand markets.

Strategic Outlook for Titanium Alloys Industry Market

The titanium alloys industry market is set for a strategically positive outlook, fueled by sustained demand from core sectors and emerging opportunities. The ongoing advancements in additive manufacturing represent a significant growth catalyst, enabling the creation of highly complex and customized components with unparalleled efficiency. Continued investment in research and development to create novel alloy compositions with enhanced properties, such as superior high-temperature performance and improved fatigue resistance, will unlock new applications and market penetration. The growing global emphasis on lightweighting across automotive and aerospace industries will continue to drive demand for titanium alloys. Furthermore, the expanding applications in sectors like renewable energy and advanced medical devices provide robust avenues for future growth. Strategic collaborations between raw material producers, manufacturers, and end-users will be crucial for navigating supply chain dynamics and ensuring competitive pricing. The industry's focus on sustainability and efficient resource utilization through advanced recycling technologies will also play a pivotal role in its long-term strategic success.

Titanium Alloys Industry Segmentation

-

1. Microstructure

- 1.1. Alpha and Near-alpha Alloy

- 1.2. Alpha-beta Alloy

- 1.3. Beta Alloy

-

2. End-user Industry

- 2.1. Aerospace

- 2.2. Automotive and Shipbuilding

- 2.3. Chemical

- 2.4. Power and Desalination

- 2.5. Other End-user Industries

Titanium Alloys Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Titanium Alloys Industry Regional Market Share

Geographic Coverage of Titanium Alloys Industry

Titanium Alloys Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Microstructure

- 5.1.1. Alpha and Near-alpha Alloy

- 5.1.2. Alpha-beta Alloy

- 5.1.3. Beta Alloy

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Aerospace

- 5.2.2. Automotive and Shipbuilding

- 5.2.3. Chemical

- 5.2.4. Power and Desalination

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Microstructure

- 6. Global Titanium Alloys Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Microstructure

- 6.1.1. Alpha and Near-alpha Alloy

- 6.1.2. Alpha-beta Alloy

- 6.1.3. Beta Alloy

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Aerospace

- 6.2.2. Automotive and Shipbuilding

- 6.2.3. Chemical

- 6.2.4. Power and Desalination

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Microstructure

- 7. Asia Pacific Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Microstructure

- 7.1.1. Alpha and Near-alpha Alloy

- 7.1.2. Alpha-beta Alloy

- 7.1.3. Beta Alloy

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Aerospace

- 7.2.2. Automotive and Shipbuilding

- 7.2.3. Chemical

- 7.2.4. Power and Desalination

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Microstructure

- 8. North America Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Microstructure

- 8.1.1. Alpha and Near-alpha Alloy

- 8.1.2. Alpha-beta Alloy

- 8.1.3. Beta Alloy

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Aerospace

- 8.2.2. Automotive and Shipbuilding

- 8.2.3. Chemical

- 8.2.4. Power and Desalination

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Microstructure

- 9. Europe Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Microstructure

- 9.1.1. Alpha and Near-alpha Alloy

- 9.1.2. Alpha-beta Alloy

- 9.1.3. Beta Alloy

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Aerospace

- 9.2.2. Automotive and Shipbuilding

- 9.2.3. Chemical

- 9.2.4. Power and Desalination

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Microstructure

- 10. Rest of the World Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Microstructure

- 10.1.1. Alpha and Near-alpha Alloy

- 10.1.2. Alpha-beta Alloy

- 10.1.3. Beta Alloy

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Aerospace

- 10.2.2. Automotive and Shipbuilding

- 10.2.3. Chemical

- 10.2.4. Power and Desalination

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Microstructure

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Hermith GmbH

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 BRISMET

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Weber Metals (OTTO FUCHS COMPANY)*List Not Exhaustive

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Perryman Company

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 KOBE STEEL LTD

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 ATI

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Daido Steel Co Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Toho Titanium Co Ltd

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 VSMPO-AVISMA Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Howmet Aerospace

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 CRS Holdings LLC

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Eramet

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 M/s Bansal Brothers

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 AMG Advanced Metallurgical Group N V

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 Mishra Dhatu Nigam Limited

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.16 TIMET (Precision Castparts Corp )

- 11.1.16.1. Company Overview

- 11.1.16.2. Products

- 11.1.16.3. Company Financials

- 11.1.16.4. SWOT Analysis

- 11.1.1 Hermith GmbH

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Titanium Alloys Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 3: Asia Pacific Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 4: Asia Pacific Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 9: North America Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 10: North America Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 15: Europe Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 16: Europe Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 21: Rest of the World Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 22: Rest of the World Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Rest of the World Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Rest of the World Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 2: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Titanium Alloys Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 5: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 13: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 19: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 27: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: South America Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Middle East and Africa Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Titanium Alloys Industry?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Titanium Alloys Industry?

Key companies in the market include Hermith GmbH, BRISMET, Weber Metals (OTTO FUCHS COMPANY)*List Not Exhaustive, Perryman Company, KOBE STEEL LTD, ATI, Daido Steel Co Ltd, Toho Titanium Co Ltd, VSMPO-AVISMA Corporation, Howmet Aerospace, CRS Holdings LLC, Eramet, M/s Bansal Brothers, AMG Advanced Metallurgical Group N V, Mishra Dhatu Nigam Limited, TIMET (Precision Castparts Corp ).

3. What are the main segments of the Titanium Alloys Industry?

The market segments include Microstructure, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.34 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Usage of Titanium Alloys in the Aerospace Sector; Increasing Demand for Titanium Alloys for Combat Vehicles to Replace Steel and Aluminum.

6. What are the notable trends driving market growth?

Increasing Demand of Titanium Alloys in the Aerospace Industry.

7. Are there any restraints impacting market growth?

High Reactivity of Alloy Demands Specialized Care During Production; Other Restraints.

8. Can you provide examples of recent developments in the market?

In November 2022, PTC Industries and Defence PSU Mishra Dhatu Nigam (MIDHANI) signed a memorandum of understanding (MOU) for a technological partnership. In accordance with their MOU, PTC Industries and Midhani will make use of each other's technological resources to manufacture titanium alloy pipes and tubes using locally processed raw materials; manufacture titanium alloy plates and sheets; and fabricate critical parts and LRUs for the defense and aerospace industries using PTC's advanced machining facility and Midhani's forged and rolled products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Titanium Alloys Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Titanium Alloys Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Titanium Alloys Industry?

To stay informed about further developments, trends, and reports in the Titanium Alloys Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence