Key Insights

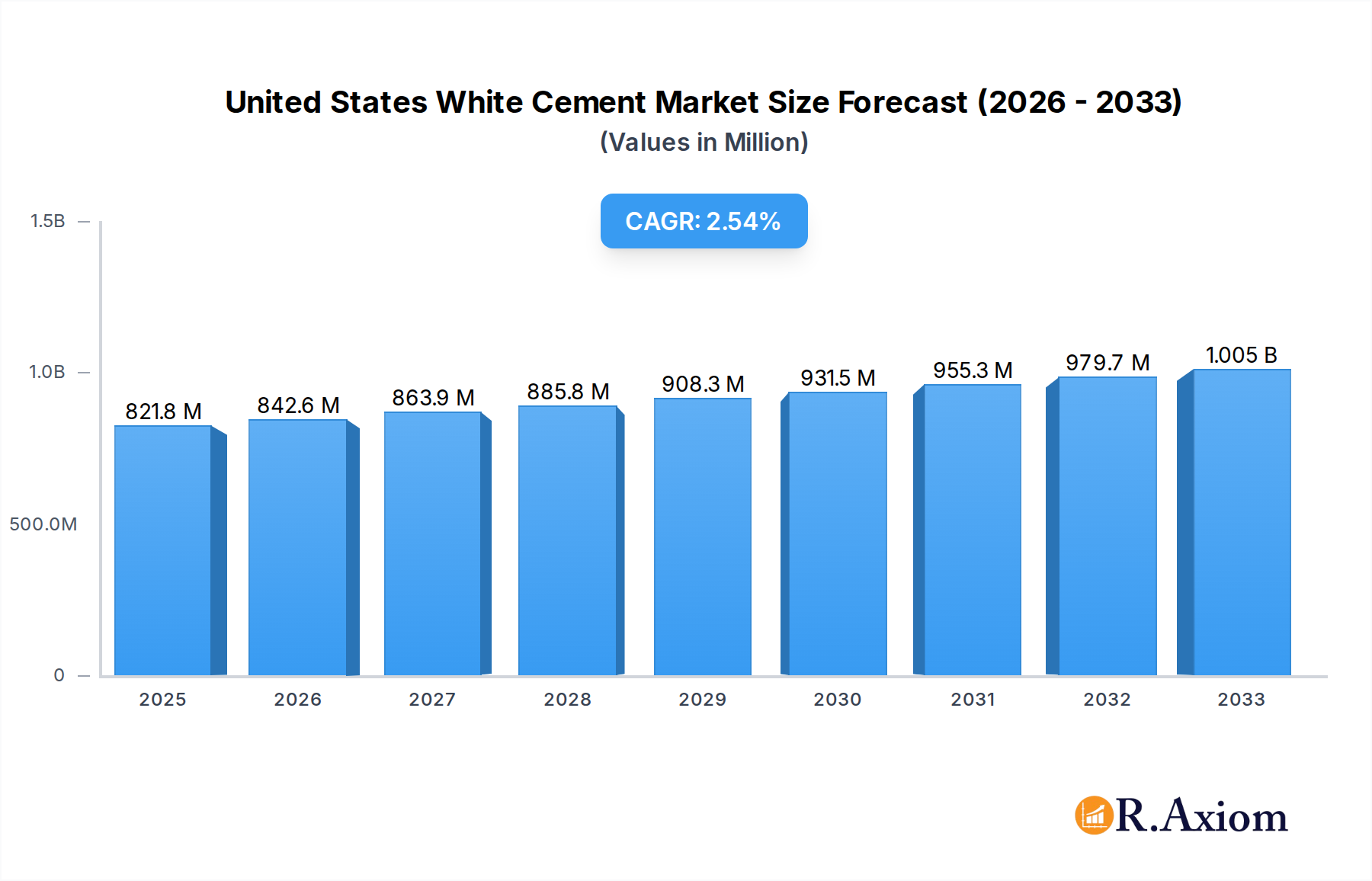

The United States White Cement Market is poised for steady expansion, projected to reach $821.79 million by 2025 with a Compound Annual Growth Rate (CAGR) of 2.58% through 2033. This growth is propelled by a significant increase in demand from various applications, notably infrastructure development and the burgeoning residential construction sector. White cement's aesthetic appeal and durability make it a preferred choice for decorative concrete, precast elements, and architectural finishes, driving its adoption in both new builds and renovation projects. Emerging trends such as the increasing use of white cement in high-performance concrete formulations for specialized applications and its growing integration into sustainable building practices are further bolstering market prospects. The inherent versatility of white cement, allowing for a wide array of colorations and finishes, continues to attract designers and builders seeking to enhance visual appeal and create unique architectural statements.

United States White Cement Market Market Size (In Million)

Despite its positive trajectory, the market encounters certain restraints, including the volatile raw material prices, particularly for the key components of white cement. Furthermore, the higher production cost compared to ordinary Portland cement can sometimes limit its widespread adoption in price-sensitive projects. However, the ongoing technological advancements in production processes, aimed at improving efficiency and reducing costs, are expected to mitigate these challenges. The market is segmented into Type I Cement and Type III Cement, with Type I dominating due to its broader applicability. Key application segments include residential, infrastructure, commercial, and industrial sectors, each contributing to the overall market demand. Major players like HOLCIM, CEMEX SAB De CV, and Heidelberg Materials are actively investing in research and development to innovate and expand their product portfolios, catering to evolving market needs and reinforcing their competitive positions.

United States White Cement Market Company Market Share

This in-depth report offers a definitive analysis of the United States White Cement Market, providing critical insights for industry stakeholders. Covering the historical period from 2019 to 2024, a base year of 2025, and a comprehensive forecast period from 2025 to 2033, this study delves into market dynamics, segmentation, competitive landscape, and future growth trajectories. With a focus on high-traffic keywords such as "white cement market," "US construction materials," "architectural cement," and "specialty cement applications," this report is meticulously designed for optimal search visibility and to inform strategic decision-making. The market size is projected to reach approximately $5,800 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 4.2% from the base year 2025, estimated at $4,200 Million.

United States White Cement Market Market Concentration & Innovation

The United States white cement market exhibits a moderately concentrated landscape, with a few key players dominating production and distribution. Major companies like Suwannee American Cement (CRH PLC), HOLCIM, Argos USA LLC, Federal White Cement, Cementer Holding NV (Lehigh White Cement Co LLC), CEMEX SAB De CV, Almaty's Gmbh (OYAK), Royal El Minya Cement (SESCO Cement Corp), Royal White Cement Inc., Titan America LLC, Heidelberg Materials, and CIMSA hold significant market share. Innovation in the white cement sector is primarily driven by the demand for enhanced aesthetic appeal in construction, leading to developments in particle fineness, color consistency, and workability. Regulatory frameworks, particularly those concerning environmental impact and building codes, also play a crucial role in shaping product development and manufacturing processes. The market's susceptibility to price fluctuations in raw materials and energy costs presents a continuous challenge. Product substitutes, such as alternative decorative concrete finishes and façade materials, exist but often fall short of the unique aesthetic and functional benefits offered by high-quality white cement. End-user trends are increasingly leaning towards sustainable and visually appealing construction materials, fueling demand for premium white cement grades. Mergers and acquisitions (M&A) activities, while not at a frenetic pace, are strategic moves to consolidate market presence and expand geographical reach. For instance, the acquisition of smaller, regional players by larger corporations is a recurring theme, aiming to leverage economies of scale and distribution networks. Deal values are typically undisclosed but are significant enough to impact market structure.

United States White Cement Market Industry Trends & Insights

The United States white cement market is experiencing robust growth, underpinned by several interconnected industry trends and insights. A significant growth driver is the escalating demand for aesthetically superior construction materials in both residential and commercial sectors. Architects and designers increasingly specify white cement for its clean, bright appearance, versatility in achieving specific textures, and compatibility with various pigments for colored concrete applications. This preference is particularly evident in high-end residential projects, luxury commercial developments, and prominent public infrastructure, where visual impact is paramount. Technological disruptions are contributing to improved product performance and sustainability. Innovations in cement production, such as enhanced grinding technologies and optimized clinker compositions, are leading to finer particle sizes, higher early strength, and reduced environmental footprints. The drive towards sustainable construction practices is also influencing the market, with manufacturers investing in energy-efficient production methods and exploring supplementary cementitious materials to lower CO2 emissions. Consumer preferences are shifting towards modern, minimalist designs that often benefit from the clean, bright aesthetic of white cement. The growing awareness of its durability and longevity as a construction material further bolsters its appeal. Competitive dynamics within the market are characterized by a focus on product quality, consistency, and reliable supply chains. Companies are investing in advanced quality control measures and expanding their distribution networks to serve a broader customer base. The market penetration of white cement is expected to deepen as awareness of its benefits grows and as construction projects continue to prioritize visual appeal and long-term value. The overall CAGR for the United States white cement market is projected at approximately 4.2% from 2025 to 2033, indicating a steady and sustained expansion. Market size is estimated to reach $4,200 Million in 2025 and grow to approximately $5,800 Million by 2033.

Dominant Markets & Segments in United States White Cement Market

The United States white cement market is characterized by regional strengths and distinct segment dominance, driven by specific economic policies, infrastructure development, and end-user demands.

- Dominant Product Type: Type I Cement currently holds the largest market share within the United States white cement sector. Its versatility and general-purpose applicability make it the preferred choice for a wide array of construction projects, from structural elements to decorative finishes. The consistent demand for a reliable, all-around white cement product ensures its continued dominance.

- Key Drivers for Type I Cement Dominance:

- Broad applicability across various construction needs.

- Established production processes and supply chains.

- Cost-effectiveness compared to specialized types for general applications.

- Favorable integration with diverse construction techniques.

- Key Drivers for Type I Cement Dominance:

- Emerging Product Type: Type III Cement is experiencing significant growth, attributed to its high early strength characteristics. This attribute is particularly valuable in construction projects requiring rapid formwork removal, accelerated project timelines, or cold-weather concreting. The increasing pace of construction and the need for efficiency are propelling its market penetration.

- Key Drivers for Type III Cement Growth:

- Faster construction schedules and reduced project lead times.

- Suitability for precast concrete applications.

- Enhanced performance in challenging environmental conditions.

- Growing adoption in infrastructure projects demanding quick turnaround.

- Key Drivers for Type III Cement Growth:

- Dominant Application: The Residential sector represents the largest application segment for white cement in the United States. Homeowners and developers increasingly seek premium aesthetics for new builds and renovations, including decorative driveways, patios, countertops, and interior finishes. The demand for custom and visually appealing homes directly fuels white cement consumption.

- Key Drivers for Residential Application Dominance:

- Growing disposable income and demand for premium home features.

- Trend towards personalized and aesthetically pleasing home designs.

- Use in interior design elements like polished concrete floors and feature walls.

- Renovation and remodeling projects seeking to upgrade property appeal.

- Key Drivers for Residential Application Dominance:

- Growing Application: Infrastructure development is emerging as a key growth driver for white cement. Its use in bridges, public plazas, decorative pavements, and architectural features within public spaces is on the rise. Government initiatives focused on urban beautification and the construction of landmark projects are contributing to this segment's expansion.

- Key Drivers for Infrastructure Application Growth:

- Government investments in public works and urban renewal projects.

- Demand for durable and visually appealing public spaces.

- Use in precast concrete elements for bridges and tunnels.

- Architectural design trends in civic buildings and transportation hubs.

- Key Drivers for Infrastructure Application Growth:

- Key Commercial Application Drivers: The Commercial segment, including retail spaces, offices, and hospitality venues, is also a significant consumer of white cement, driven by the need for sophisticated and inviting architectural designs. Industrial and Institutional applications, while smaller, are growing due to specialized uses requiring durability and specific aesthetic properties.

United States White Cement Market Product Developments

Product developments in the United States white cement market are focused on enhancing performance and expanding application versatility. Innovations include the development of white cements with improved whiteness and brightness, achieving a superior aesthetic for architectural finishes. Manufacturers are also focusing on cements with finer particle sizes and enhanced plasticity, leading to improved workability, reduced water demand, and higher ultimate strength. These advancements translate into competitive advantages by enabling architects and builders to achieve more intricate designs and durable structures. The integration of sustainable manufacturing practices and the exploration of supplementary cementitious materials are also key product development trends, aligning with market demand for environmentally friendly construction solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the United States white cement market, segmented by product type and application. The Product Type segmentation includes Type I Cement, Type III Cement, and Other Product Types, each offering distinct properties for varied construction needs. Type I Cement is the established market leader due to its general-purpose utility, with market size estimated at $2,500 Million in 2025, projected to grow at a CAGR of 3.8% to $3,600 Million by 2033. Type III Cement is a rapidly growing segment, driven by its high early strength, with an estimated market size of $1,200 Million in 2025, forecast to expand at a CAGR of 5.5% to $2,000 Million by 2033. Other Product Types, encompassing specialized white cements, represent a niche market with steady growth. The Application segmentation analyzes the market across Residential, Infrastructure, Commercial, and Industrial and Institutional sectors. The Residential segment, valued at $1,800 Million in 2025 with a projected CAGR of 4.5% to $2,700 Million by 2033, is the largest due to aesthetic demands. The Infrastructure segment, estimated at $1,000 Million in 2025 and growing at a CAGR of 4.8% to $1,500 Million by 2033, shows significant growth potential driven by public projects. Commercial applications, valued at $900 Million in 2025 with a CAGR of 4.0% to $1,300 Million by 2033, and Industrial and Institutional applications, with a market size of $500 Million in 2025 and a CAGR of 3.5% to $700 Million by 2033, contribute to the overall market demand.

Key Drivers of United States White Cement Market Growth

The United States white cement market's growth is propelled by several key drivers. Firstly, the sustained expansion of the construction industry, particularly in residential and commercial development, fuels demand for versatile and aesthetically pleasing materials like white cement. Secondly, increasing consumer preference for high-quality, visually appealing architectural designs in both residential and commercial spaces directly boosts the adoption of white cement for its superior finish and brightness. Thirdly, government investments in infrastructure projects, including urban beautification and public works, create significant opportunities for white cement in decorative and durable applications. Finally, technological advancements in cement production are leading to improved product performance, enhanced sustainability, and cost efficiencies, further stimulating market growth and adoption.

Challenges in the United States White Cement Market Sector

Despite its growth, the United States white cement market faces several challenges. Fluctuations in the prices of raw materials, such as limestone and gypsum, and volatile energy costs can significantly impact production expenses and profit margins for manufacturers. Stringent environmental regulations, while driving innovation towards sustainable practices, can also increase compliance costs and necessitate significant investment in new technologies. Supply chain disruptions, as witnessed in recent years, can affect the timely availability of raw materials and the distribution of finished products, leading to project delays and increased logistical expenses. Furthermore, the competitive pressure from alternative building materials and the potential for price wars among market players can constrain revenue growth and profitability.

Emerging Opportunities in United States White Cement Market

Emerging opportunities in the United States white cement market lie in several key areas. The increasing demand for sustainable and eco-friendly construction materials presents a significant avenue for growth, with opportunities for manufacturers to develop and market white cements with lower embodied carbon and recycled content. The growing trend of precast concrete construction, especially in infrastructure and large-scale commercial projects, offers a niche for high-performance white cements that can meet stringent strength and aesthetic requirements. Furthermore, the expanding use of white cement in decorative applications beyond traditional construction, such as in artistic installations, bespoke furniture, and interior design elements, opens up new market segments. The development of advanced white cement formulations with enhanced properties like self-cleaning capabilities or improved durability in harsh environments also presents significant innovation and market expansion potential.

Leading Players in the United States White Cement Market Market

- Suwannee American Cement (CRH PLC)

- HOLCIM

- Argos USA LLC

- Federal White Cement

- Cementer Holding NV (Lehigh White Cement Co LLC)

- CEMEX SAB De CV

- Almaty's Gmbh (OYAK)

- Royal El Minya Cement (SESCO Cement Corp)

- Royal White Cement Inc.

- Titan America LLC

- Heidelberg Materials

- CIMSA

Key Developments in United States White Cement Market Industry

- August 2023: Royal White Cement Inc. announced its plans to build a new cement terminal in Houston, Texas, to produce slag, grey cement, and white cement. The company has strengthened its market presence by expanding its footprint in Houston.

- March 2023: Argos USA LLC has been awarded the Energy Star certification from the US Environmental Protection Agency (EPA). The company has strengthened its market presence by reducing the electricity use and CO2 emissions from its manufacturing process.

Strategic Outlook for United States White Cement Market Market

The strategic outlook for the United States white cement market is highly positive, characterized by sustained growth and evolving market dynamics. Key growth catalysts include the ongoing urbanization trends, which necessitate continuous infrastructure development and expansion of residential and commercial spaces, all of which benefit from the aesthetic and functional properties of white cement. The increasing focus on sustainable construction practices presents an opportunity for manufacturers to innovate and offer eco-friendly white cement solutions, appealing to a growing segment of environmentally conscious consumers and developers. Furthermore, the continuous drive for architectural differentiation and premium finishes in the construction sector will ensure a consistent demand for high-quality white cement. Strategic investments in research and development for advanced formulations, coupled with efficient supply chain management and targeted marketing efforts to highlight the unique benefits of white cement, will be crucial for market leaders to capitalize on future opportunities and maintain a competitive edge.

United States White Cement Market Segmentation

-

1. Product Type

- 1.1. Type I Cement

- 1.2. Type III Cement

- 1.3. Other Product Types

-

2. Application

- 2.1. Residential

- 2.2. Infrastructure

- 2.3. Commercial

- 2.4. Industrial and Institutional

United States White Cement Market Segmentation By Geography

- 1. United States

United States White Cement Market Regional Market Share

Geographic Coverage of United States White Cement Market

United States White Cement Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Type I Cement

- 5.1.2. Type III Cement

- 5.1.3. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential

- 5.2.2. Infrastructure

- 5.2.3. Commercial

- 5.2.4. Industrial and Institutional

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United States White Cement Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Type I Cement

- 6.1.2. Type III Cement

- 6.1.3. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential

- 6.2.2. Infrastructure

- 6.2.3. Commercial

- 6.2.4. Industrial and Institutional

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Suwannee American Cement (CRH PLC)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 HOLCIM

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Argos USA LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Federal White Cement

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cementer Holding NV (Lehigh White Cement Co LLC)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CEMEX SAB De CV

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Almaty's Gmbh (OYAK)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Royal El Minya Cement (SESCO Cement Corp )

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Royal White Cement Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Titan America LLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Heidelberg Materials

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 CIMSA

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Suwannee American Cement (CRH PLC)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States White Cement Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United States White Cement Market Share (%) by Company 2025

List of Tables

- Table 1: United States White Cement Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: United States White Cement Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: United States White Cement Market Revenue Million Forecast, by Application 2020 & 2033

- Table 4: United States White Cement Market Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: United States White Cement Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: United States White Cement Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: United States White Cement Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: United States White Cement Market Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 9: United States White Cement Market Revenue Million Forecast, by Application 2020 & 2033

- Table 10: United States White Cement Market Volume K Tons Forecast, by Application 2020 & 2033

- Table 11: United States White Cement Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United States White Cement Market Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States White Cement Market?

The projected CAGR is approximately 2.58%.

2. Which companies are prominent players in the United States White Cement Market?

Key companies in the market include Suwannee American Cement (CRH PLC), HOLCIM, Argos USA LLC, Federal White Cement, Cementer Holding NV (Lehigh White Cement Co LLC), CEMEX SAB De CV, Almaty's Gmbh (OYAK), Royal El Minya Cement (SESCO Cement Corp ), Royal White Cement Inc, Titan America LLC, Heidelberg Materials, CIMSA.

3. What are the main segments of the United States White Cement Market?

The market segments include Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 821.79 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Residential Construction in the Country; Increasing Investments in the Infrastructure Sector.

6. What are the notable trends driving market growth?

Type I Cement to Dominate the Market.

7. Are there any restraints impacting market growth?

High Production Costs.

8. Can you provide examples of recent developments in the market?

August 2023: Royal White Cement Inc. announced its plans to build a new cement terminal in Houston, Texas, to produce slag, grey cement, and white cement. The company has strengthened its market presence by expanding its footprint in Houston.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States White Cement Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States White Cement Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States White Cement Market?

To stay informed about further developments, trends, and reports in the United States White Cement Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence