Key Insights

The vacuum deposition services market is experiencing robust growth, driven by increasing demand across diverse sectors. The market's expansion is fueled by the unique capabilities of vacuum deposition techniques in creating high-performance coatings with exceptional properties like durability, wear resistance, and optical clarity. These coatings find applications in numerous industries, including electronics (for semiconductors and displays), automotive (for enhanced aesthetics and functionality), aerospace (for lightweight and corrosion-resistant components), and medical devices (for biocompatible surfaces). Technological advancements in vacuum deposition processes, such as atomic layer deposition (ALD) and pulsed laser deposition (PLD), are further contributing to market growth by enabling the creation of more precise and complex coatings with tailored properties. The market is segmented by coating type (e.g., metallic, dielectric, polymeric), substrate material, and application. While specific market size figures are unavailable, considering a reasonable CAGR of 7% and a 2025 market value estimated in the range of $2.5 Billion, the market is projected to significantly increase over the forecast period. Competition is intense among various established players and emerging companies, each vying to improve upon vacuum deposition methods and broaden their industry reach.

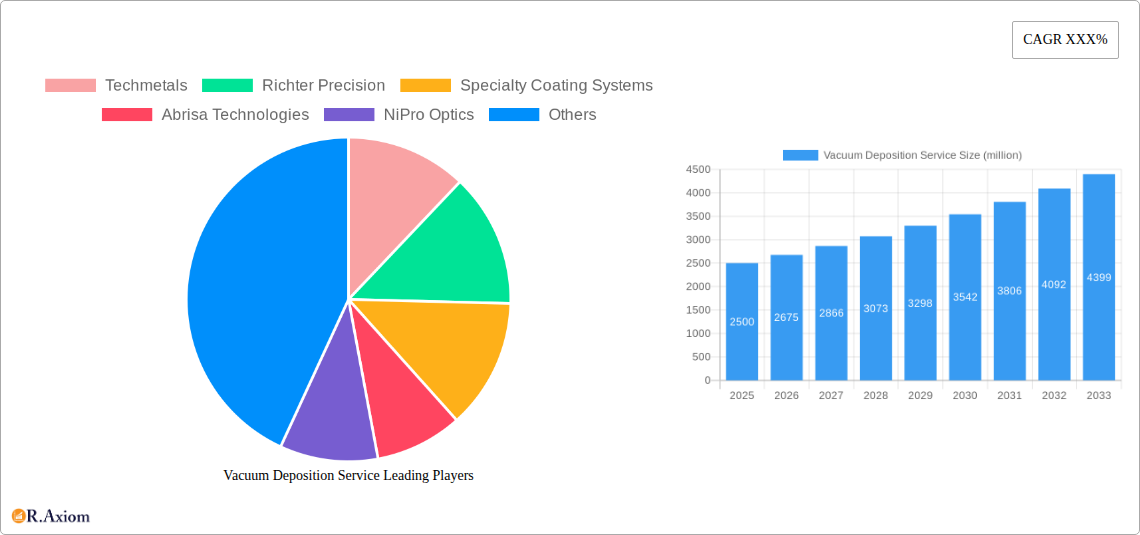

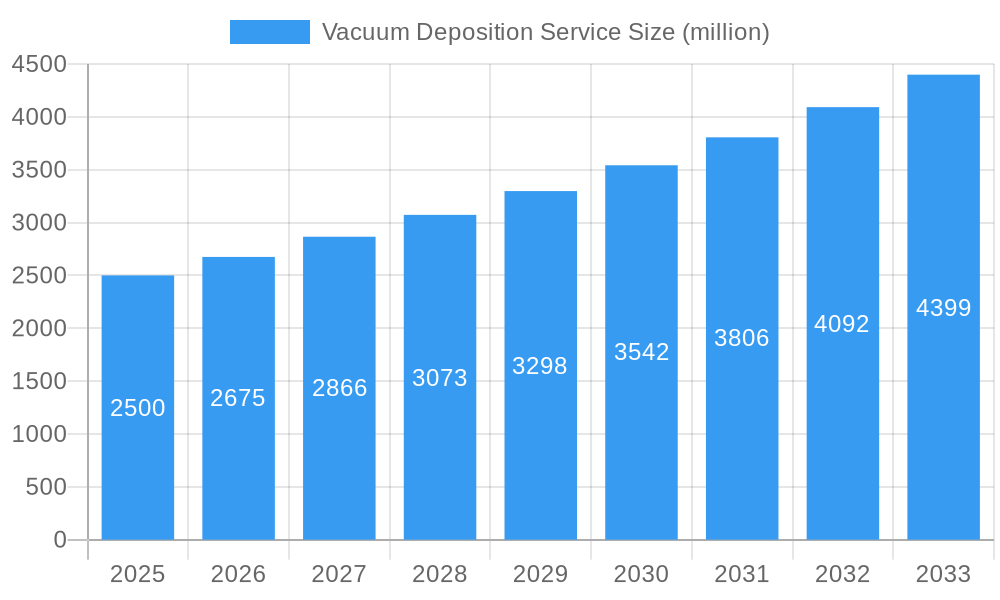

Vacuum Deposition Service Market Size (In Billion)

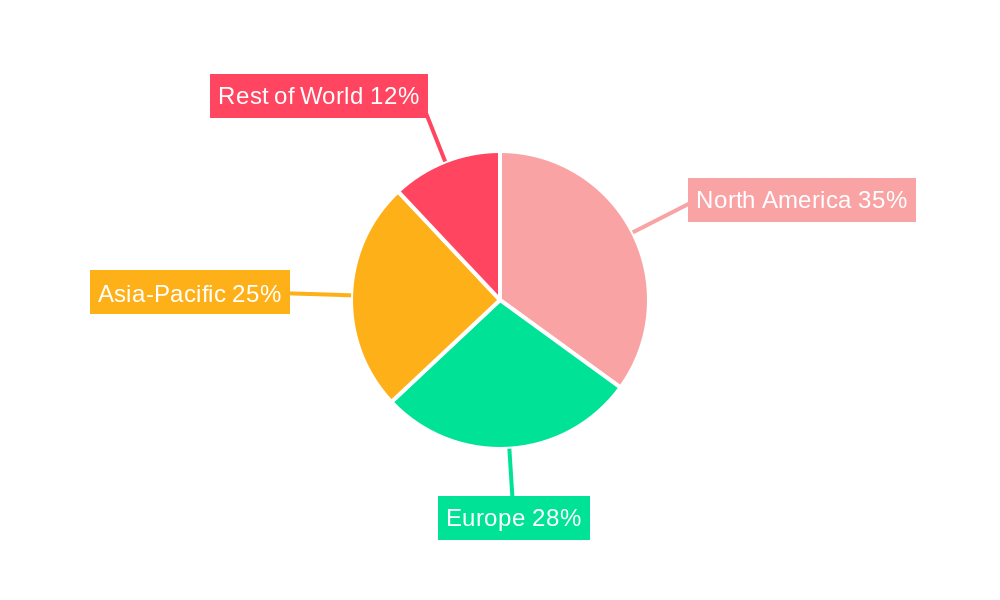

The major restraints to market growth include the high capital investment required for vacuum deposition equipment, the complexity of the processes involved, and potential environmental concerns associated with certain deposition materials. Despite these challenges, continuous innovation in the field is overcoming these obstacles. This includes the development of more energy-efficient and environmentally friendly deposition techniques, as well as the emergence of smaller, more cost-effective equipment suitable for smaller businesses and research laboratories. Furthermore, the growing emphasis on sustainability and the need for advanced materials in various industries are expected to drive further growth in this market. The geographical distribution shows strong growth across North America and Asia-Pacific owing to robust technological advancements and increased adoption in various end-use sectors. Europe also constitutes a significant market share, driven by the strong presence of established companies and government funding for research and development in advanced materials.

Vacuum Deposition Service Company Market Share

Vacuum Deposition Service Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the global Vacuum Deposition Service market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The study covers the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages extensive primary and secondary research to provide a robust understanding of market dynamics, growth drivers, challenges, and emerging opportunities. The market size is estimated in millions of dollars.

Vacuum Deposition Service Market Concentration & Innovation

The global vacuum deposition service market exhibits a moderately concentrated landscape, with several key players holding significant market share. Techmetals, Richter Precision, and Specialty Coating Systems are among the leading companies, collectively accounting for an estimated xx% of the market in 2025. However, the presence of numerous smaller players and emerging technologies fosters a dynamic competitive environment.

Market Concentration Metrics (2025 Estimates):

- Top 3 Players Market Share: xx%

- Top 5 Players Market Share: xx%

- Herfindahl-Hirschman Index (HHI): xx

Innovation Drivers:

- Advancements in thin-film deposition technologies (e.g., atomic layer deposition, pulsed laser deposition) are driving innovation.

- Growing demand for advanced materials with tailored properties in diverse applications fuels R&D investment.

- Stringent regulatory frameworks focused on environmental sustainability and material efficiency are pushing for greener deposition methods.

Product Substitutes and End-User Trends:

- Alternative coating technologies, such as electroplating and chemical vapor deposition, offer limited substitution. However, vacuum deposition techniques maintain advantages in precision and material control.

- Increasing demand for high-performance coatings in electronics, optics, and medical devices is a key end-user trend.

M&A Activities:

Over the historical period (2019-2024), the market witnessed xx M&A deals, with a total estimated value of $xx million. These activities primarily involved the acquisition of smaller specialized firms by larger companies to expand their service offerings and geographical reach.

Vacuum Deposition Service Industry Trends & Insights

The global vacuum deposition service market is experiencing robust growth, driven by several key factors. The market is estimated to grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by increasing demand from key sectors such as electronics, optics, automotive, and healthcare. Technological advancements, such as the development of high-throughput deposition systems and the integration of advanced process control techniques, are further accelerating market expansion. Consumer preferences for enhanced product performance, durability, and aesthetics also contribute to the growth of the vacuum deposition service market.

Furthermore, the market is undergoing significant technological disruption, with the emergence of novel materials and deposition techniques. The market penetration of advanced coating technologies, particularly those offering improved adhesion, scratch resistance, and corrosion protection, is steadily increasing. The competitive landscape is characterized by both intense rivalry among established players and the emergence of new entrants. This dynamic environment encourages continuous innovation and the development of differentiated service offerings. The increasing adoption of sustainable and environmentally friendly deposition techniques is also a significant trend, driven by growing environmental concerns and regulatory pressure.

Dominant Markets & Segments in Vacuum Deposition Service

The Asia-Pacific region dominates the global vacuum deposition service market, accounting for approximately xx% of the total market revenue in 2025. This dominance is attributed to several key factors:

- Rapid economic growth: The region's robust economic expansion fuels demand for advanced materials and coatings across various industries.

- Expanding electronics manufacturing: The concentration of electronics manufacturing hubs in countries like China, South Korea, and Taiwan drives significant demand.

- Government support for technological advancements: Several governments are actively promoting R&D initiatives, further boosting market growth.

Key Drivers for Asia-Pacific Dominance:

- Strong infrastructure development.

- Favorable government policies and incentives for the electronics industry.

- Large consumer base with increasing disposable income.

- Growing adoption of advanced technologies across sectors.

Other significant regions include North America and Europe, each contributing approximately xx% and xx% to the global market, respectively. These regions exhibit steady growth driven by robust industrial activity and technological advancements. However, the Asia-Pacific region's rapid growth trajectory suggests its dominance will likely persist in the coming years.

Vacuum Deposition Service Product Developments

Recent product innovations focus on enhancing deposition process efficiency, expanding material choices, and improving coating performance. This includes developments in high-throughput sputtering systems, advanced plasma-enhanced chemical vapor deposition (PECVD) techniques, and the incorporation of novel materials such as graphene and 2D materials. These advancements enhance coating properties, leading to superior performance in terms of hardness, wear resistance, optical transparency, and electrical conductivity, making them suitable for applications ranging from consumer electronics to aerospace components. The enhanced precision and customization capabilities are crucial competitive advantages in this market.

Report Scope & Segmentation Analysis

The report segments the vacuum deposition service market based on several criteria:

By Coating Material: This segment includes metallic coatings (e.g., Aluminum, Chromium, Gold), dielectric coatings (e.g., Silicon dioxide, Titanium dioxide), and others. The metallic coatings segment dominates, driven by diverse applications in electronics and automotive sectors. Growth projections for each sub-segment vary depending on factors such as price, availability and technological feasibility.

By Application: The market is further segmented by application, which include consumer electronics, optics, automotive, medical devices, aerospace, and others. The electronics sector holds the largest share due to the high demand for thin-film coatings in integrated circuits and display panels. The automotive segment is experiencing significant growth, driven by applications in automotive lighting and decorative coatings.

By Deposition Technique: Several techniques exist including Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), and Atomic Layer Deposition (ALD). PVD is currently dominant but the other two techniques hold significant growth potential given their improved properties.

By Region: The regional segmentation provides granular data by region, including analysis of each region’s key drivers and challenges. Asia-Pacific dominates and is projected to continue doing so in the forecast period.

Key Drivers of Vacuum Deposition Service Growth

The growth of the vacuum deposition service market is primarily driven by several factors:

- Technological Advancements: Continuous innovation in deposition techniques (ALD, PECVD) enables the creation of more precise and tailored coatings with enhanced properties.

- Expanding Electronics Sector: The electronics industry's relentless expansion necessitates high-performance coatings for improved device functionality and durability.

- Rising Demand for Advanced Materials: Across various sectors, there's a growing demand for materials with specific optical, electrical, and mechanical properties, which vacuum deposition excels in providing.

- Government Regulations: Regulations promoting energy efficiency and environmental sustainability are encouraging the development of green coating technologies.

Challenges in the Vacuum Deposition Service Sector

Several challenges hinder the growth of the vacuum deposition service market:

- High Capital Expenditure: The initial investment required for advanced deposition equipment is substantial, limiting entry for smaller players.

- Complex Process Control: Achieving precise and repeatable coating quality necessitates highly skilled operators and sophisticated process control systems.

- Material Costs: The cost of some specialized coating materials can be high, impacting the overall service price.

- Intense Competition: The market experiences considerable competition, necessitating continuous innovation to maintain a competitive edge.

Emerging Opportunities in Vacuum Deposition Service

Several emerging trends offer significant opportunities for growth in the vacuum deposition service market:

- Flexible Electronics: The rise of flexible displays and wearable electronics presents a rapidly expanding market for flexible coating solutions.

- Sustainable Coatings: Growing environmental concerns are driving demand for environmentally friendly deposition techniques and materials.

- Advanced Materials Integration: The integration of novel materials like graphene and 2D materials into coatings opens avenues for enhanced functionalities.

- New Applications: Emerging applications in fields like biomedical devices and energy storage offer significant growth potential.

Leading Players in the Vacuum Deposition Service Market

- Techmetals

- Richter Precision

- Specialty Coating Systems

- Abrisa Technologies

- NiPro Optics

- Madico

- IBC Coating Technologies

- VDI

- HZO

- Aalberts Surface Treatment

- IJ Research

- Phoenix Electroformed Products

- Advanced Coating

- Para Tech Coating

- Deep Coat

- Vast Films

- VTI Vacuum Technologies

- Vacuum Process Engineering

- Industrial Hard Carbon

Key Developments in Vacuum Deposition Service Industry

- 2022-Q4: Specialty Coating Systems launched a new high-throughput sputtering system, expanding its capacity and service offerings.

- 2023-Q1: Techmetals acquired a smaller competitor, strengthening its market position and expanding its geographical reach.

- 2023-Q2: A significant investment was made in R&D of sustainable coating solutions by IBC Coating Technologies. (Specific investment value unavailable - xx million predicted).

- 2024-Q3: Richter Precision partnered with a material supplier to introduce a new range of high-performance coatings.

Strategic Outlook for Vacuum Deposition Service Market

The vacuum deposition service market is poised for substantial growth in the coming years, driven by the sustained expansion of existing application areas and the emergence of new, high-growth segments. Continued advancements in deposition technologies and the development of eco-friendly processes will fuel this expansion. The strategic focus of major players should be on expanding their service capabilities, investing in R&D, and exploring new market opportunities. Companies that adapt to technological shifts and adopt sustainable practices are well-positioned to succeed in this dynamic market. The increasing emphasis on material customization and precision coating will further drive the growth trajectory of the market.

Vacuum Deposition Service Segmentation

-

1. Application

- 1.1. Electronics and Semiconductors

- 1.2. Automotive

- 1.3. Photoelectric

- 1.4. Chemical

- 1.5. Industrial

-

2. Type

- 2.1. PVD

- 2.2. CVD

Vacuum Deposition Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Vacuum Deposition Service Regional Market Share

Geographic Coverage of Vacuum Deposition Service

Vacuum Deposition Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electronics and Semiconductors

- 5.1.2. Automotive

- 5.1.3. Photoelectric

- 5.1.4. Chemical

- 5.1.5. Industrial

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. PVD

- 5.2.2. CVD

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Vacuum Deposition Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electronics and Semiconductors

- 6.1.2. Automotive

- 6.1.3. Photoelectric

- 6.1.4. Chemical

- 6.1.5. Industrial

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. PVD

- 6.2.2. CVD

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Vacuum Deposition Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electronics and Semiconductors

- 7.1.2. Automotive

- 7.1.3. Photoelectric

- 7.1.4. Chemical

- 7.1.5. Industrial

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. PVD

- 7.2.2. CVD

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Vacuum Deposition Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electronics and Semiconductors

- 8.1.2. Automotive

- 8.1.3. Photoelectric

- 8.1.4. Chemical

- 8.1.5. Industrial

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. PVD

- 8.2.2. CVD

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Vacuum Deposition Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electronics and Semiconductors

- 9.1.2. Automotive

- 9.1.3. Photoelectric

- 9.1.4. Chemical

- 9.1.5. Industrial

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. PVD

- 9.2.2. CVD

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Vacuum Deposition Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electronics and Semiconductors

- 10.1.2. Automotive

- 10.1.3. Photoelectric

- 10.1.4. Chemical

- 10.1.5. Industrial

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. PVD

- 10.2.2. CVD

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Vacuum Deposition Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Electronics and Semiconductors

- 11.1.2. Automotive

- 11.1.3. Photoelectric

- 11.1.4. Chemical

- 11.1.5. Industrial

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. PVD

- 11.2.2. CVD

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Techmetals

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Richter Precision

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Specialty Coating Systems

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Abrisa Technologies

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NiPro Optics

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Madico

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 IBC Coating Technologies

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 VDI

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 HZO

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Aalberts Surface Treatment

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 IJ Research

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Phoenix Electroformed Products

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Advanced Coating

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Para Tech Coating

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Deep Coat

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Vast Films

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 VTI Vacuum Technologies

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Vacuum Process Engineering

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Industrial Hard Carbon

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 Techmetals

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Vacuum Deposition Service Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Vacuum Deposition Service Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Vacuum Deposition Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Vacuum Deposition Service Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Vacuum Deposition Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Vacuum Deposition Service Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Vacuum Deposition Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Vacuum Deposition Service Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Vacuum Deposition Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Vacuum Deposition Service Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Vacuum Deposition Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Vacuum Deposition Service Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Vacuum Deposition Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Vacuum Deposition Service Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Vacuum Deposition Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Vacuum Deposition Service Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Vacuum Deposition Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Vacuum Deposition Service Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Vacuum Deposition Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Vacuum Deposition Service Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Vacuum Deposition Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Vacuum Deposition Service Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Vacuum Deposition Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Vacuum Deposition Service Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Vacuum Deposition Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Vacuum Deposition Service Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Vacuum Deposition Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Vacuum Deposition Service Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Vacuum Deposition Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Vacuum Deposition Service Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Vacuum Deposition Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vacuum Deposition Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Vacuum Deposition Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Vacuum Deposition Service Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Vacuum Deposition Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Vacuum Deposition Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Vacuum Deposition Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Vacuum Deposition Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Vacuum Deposition Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Vacuum Deposition Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Vacuum Deposition Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Vacuum Deposition Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Vacuum Deposition Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Vacuum Deposition Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Vacuum Deposition Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Vacuum Deposition Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Vacuum Deposition Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Vacuum Deposition Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Vacuum Deposition Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Vacuum Deposition Service Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vacuum Deposition Service?

The projected CAGR is approximately 11.1%.

2. Which companies are prominent players in the Vacuum Deposition Service?

Key companies in the market include Techmetals, Richter Precision, Specialty Coating Systems, Abrisa Technologies, NiPro Optics, Madico, IBC Coating Technologies, VDI, HZO, Aalberts Surface Treatment, IJ Research, Phoenix Electroformed Products, Advanced Coating, Para Tech Coating, Deep Coat, Vast Films, VTI Vacuum Technologies, Vacuum Process Engineering, Industrial Hard Carbon.

3. What are the main segments of the Vacuum Deposition Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vacuum Deposition Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vacuum Deposition Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vacuum Deposition Service?

To stay informed about further developments, trends, and reports in the Vacuum Deposition Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence