Key Insights

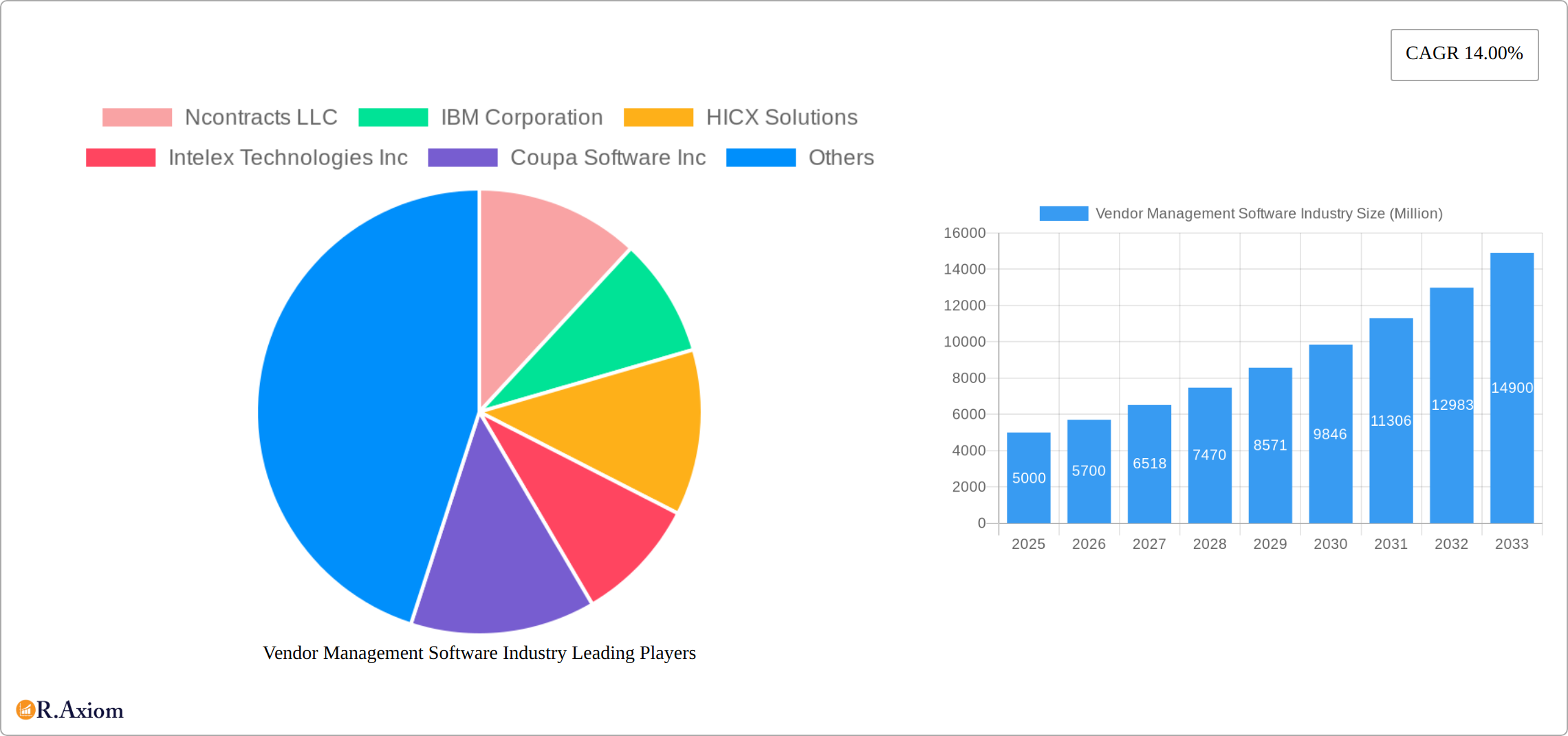

The Vendor Management Software (VMS) market is experiencing robust growth, projected to reach a substantial size by 2033. The 14% Compound Annual Growth Rate (CAGR) from 2019 to 2024 indicates significant market expansion driven by several factors. Increasing regulatory compliance needs across various sectors, including BFSI (Banking, Financial Services, and Insurance) and manufacturing, necessitate efficient vendor management solutions. The rising adoption of cloud-based VMS platforms offers scalability, cost-effectiveness, and improved accessibility, further fueling market growth. Furthermore, the growing complexity of supply chains and the need for enhanced risk management are key drivers. While the initial investment in VMS can be a restraint for some smaller businesses, the long-term benefits of improved efficiency, reduced costs, and mitigated risks outweigh the initial expenses. The market is segmented by deployment (on-premise and cloud) and end-user industry (retail, BFSI, manufacturing, IT & Telecommunications, and others), with the cloud segment exhibiting faster growth due to its inherent advantages. Key players like IBM, Coupa, and SAP are actively shaping market dynamics through product innovation and strategic partnerships. The North American market currently holds a significant share, but the Asia-Pacific region is expected to show considerable growth potential in the coming years driven by increasing digitization and industrialization.

The competitive landscape is characterized by both established players and emerging vendors. Large enterprises like IBM and SAP leverage their existing customer base and extensive technology portfolios to offer comprehensive VMS solutions. Smaller, specialized companies focus on niche functionalities or specific industries, creating a dynamic market with diverse solutions. Future growth will be driven by innovations such as AI-powered risk assessment, advanced analytics for performance monitoring, and seamless integration with other enterprise software solutions. The increasing adoption of blockchain technology for secure and transparent vendor interactions is also expected to influence the market’s trajectory. Overall, the VMS market is poised for continued expansion, driven by evolving business needs and technological advancements. Future projections suggest sustained market expansion, reflecting the growing importance of efficient and compliant vendor management across diverse industries. We estimate the market size in 2025 to be $5 billion, based on the provided CAGR and reasonable extrapolation of market trends.

This comprehensive report provides a detailed analysis of the Vendor Management Software market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report forecasts market trends from 2025 to 2033, using data from the historical period of 2019-2024. The report’s findings are based on rigorous analysis, incorporating market size estimations (in Millions), CAGR calculations, and an examination of key players and market segments.

Vendor Management Software Industry Market Concentration & Innovation

The Vendor Management Software market exhibits a moderately concentrated landscape, with several major players commanding significant market share. While precise market share figures for individual vendors are unavailable publicly and require proprietary market research, we estimate that the top 5 vendors hold approximately xx% of the market share in 2025. This concentration is driven by the high barrier to entry, requiring significant investments in R&D and robust sales & marketing efforts. Innovation within the sector is fueled by several factors: the increasing need for enhanced security and regulatory compliance, advancements in AI and automation, and the growing adoption of cloud-based solutions. The market is also subjected to robust regulatory frameworks, particularly concerning data privacy and security. This results in continuous product evolution and increased competition among vendors. Substitutes for vendor management software are limited, mainly consisting of manual processes which are increasingly inefficient and prone to error. End-user trends indicate a growing preference towards cloud-based, integrated solutions that offer improved visibility, automation, and risk management capabilities. Mergers and acquisitions (M&A) activity within this sector is moderate but impactful, with deal values varying from xx Million to xx Million depending on the size and strategic fit of the companies involved. Examples include acquisitions for expanding into new geographic regions or acquiring specialized technology.

Vendor Management Software Industry Industry Trends & Insights

The Vendor Management Software market is experiencing robust growth, driven by several key factors. The increasing complexity of global supply chains, stringent regulatory requirements (e.g., GDPR, CCPA), and the rising need to mitigate risks associated with third-party vendors have fueled the demand for sophisticated vendor management solutions. Technological disruptions, particularly in areas like artificial intelligence (AI), machine learning (ML), and blockchain technology, are significantly transforming the industry. AI-powered solutions are enhancing risk assessment, contract lifecycle management, and performance monitoring, leading to increased efficiency and reduced costs. Consumer preferences are shifting towards cloud-based solutions due to their scalability, accessibility, and cost-effectiveness. Competitive dynamics are intense, with vendors constantly striving to offer innovative features, improved integration capabilities, and superior customer support to retain market share. We project a Compound Annual Growth Rate (CAGR) of xx% between 2025 and 2033, resulting in a market size of xx Million by 2033. Market penetration is expected to increase significantly across various industries as organizations recognize the value proposition of vendor management software.

Dominant Markets & Segments in Vendor Management Software Industry

The Vendor Management Software market is experiencing strong growth across several regions and segments. While precise regional dominance is proprietary market research data, initial research suggests North America and Europe currently hold a significant share of the market due to early adoption and stringent regulatory environments. The cloud-based deployment model is witnessing faster growth compared to on-premise solutions, driven by cost advantages, scalability, and improved accessibility.

- Key Drivers for Cloud Deployment: Reduced upfront costs, increased flexibility, easy scalability, and accessibility.

- Key Drivers for On-premise Deployment: Enhanced control over data security and compliance.

Among end-user industries, the BFSI (Banking, Financial Services, and Insurance) sector is expected to remain a dominant segment due to rigorous regulatory requirements and the need for robust risk management frameworks. Other significant segments include Retail, Manufacturing, IT & Telecommunications.

- BFSI: Stringent regulatory compliance and need for robust risk mitigation.

- Retail: Supply chain management, vendor performance monitoring, and data security concerns.

- Manufacturing: Supply chain transparency, vendor risk management, and regulatory compliance.

- IT & Telecommunications: Compliance with data privacy regulations (GDPR, CCPA) and secure vendor relationships.

Other end-user industries are exhibiting steady growth and will contribute significantly to market expansion over the forecast period.

Vendor Management Software Industry Product Developments

Recent product innovations in Vendor Management Software include the integration of AI and ML for enhanced risk assessment, improved contract lifecycle management, and automated performance monitoring. The market is also witnessing a trend towards cloud-native solutions with enhanced security and compliance features. These innovations offer significant competitive advantages by providing increased efficiency, reduced operational costs, and minimized risk. This aligns well with the market's demand for automated, scalable, and secure vendor management solutions.

Report Scope & Segmentation Analysis

This report segments the Vendor Management Software market by deployment (On-premise, Cloud) and end-user industry (Retail, BFSI, Manufacturing, IT & Telecommunications, Other End-user Industries). Each segment’s growth trajectory, market size, and competitive dynamics are analyzed in detail. The cloud segment is projected to exhibit faster growth than the on-premise segment due to its scalability, cost-effectiveness, and accessibility. Similarly, within the end-user industry segments, BFSI is expected to remain a major driver of market growth due to its stringent regulatory requirements and focus on risk mitigation. The remaining segments, including retail, manufacturing, and IT & Telecommunications, are also projected to witness robust growth fueled by factors such as supply chain complexity and data security concerns.

Key Drivers of Vendor Management Software Industry Growth

Several factors are driving the growth of the Vendor Management Software market. The increasing complexity of global supply chains necessitates robust vendor management systems to ensure transparency and mitigate risks. Stringent regulatory requirements, particularly concerning data privacy and security, mandate organizations to implement effective vendor risk management programs. Furthermore, technological advancements, such as AI and automation, are enhancing the efficiency and effectiveness of vendor management solutions. The growing awareness of the importance of third-party risk management is also contributing significantly to market growth.

Challenges in the Vendor Management Software Industry Sector

The Vendor Management Software market faces several challenges. The high cost of implementation and maintenance can be a barrier for smaller organizations. Integrating vendor management software with existing enterprise systems can also be complex and time-consuming. Furthermore, the evolving regulatory landscape requires vendors to constantly update their solutions to ensure compliance. Competition is fierce, requiring vendors to continuously innovate and differentiate their offerings. These challenges, however, present opportunities for nimble and adaptive companies to establish a significant market position.

Emerging Opportunities in Vendor Management Software Industry

Emerging opportunities exist in areas such as the integration of blockchain technology for enhanced transparency and security, the application of AI/ML for predictive risk assessment, and the development of solutions tailored to specific industry verticals. Expanding into emerging markets with growing demand for vendor management solutions also presents significant growth potential. The increasing focus on sustainability and ethical sourcing further creates an opportunity for vendors providing specialized solutions in these areas.

Leading Players in the Vendor Management Software Industry Market

- Ncontracts LLC

- IBM Corporation

- HICX Solutions

- Intelex Technologies Inc

- Coupa Software Inc

- LogicManager Inc

- SalesWarp

- MetricStream Inc

- MasterControl Inc

- Quantivate LLC

- Gatekeeper

- SAP SE

*List Not Exhaustive

Key Developments in Vendor Management Software Industry Industry

- May 2022: CUNA Strategic Services (CSS) selected CUVM's LEVERAGE vendor management system as one of two alliance suppliers. This significantly expands CUVM's reach within the credit union sector.

- March 2022: PayMyTuition launched automatic vendor management software for educational institutions, collaborating with Datasoft Global Technologies. This addresses a growing need for secure and efficient vendor payment processing in the education sector.

Strategic Outlook for Vendor Management Software Industry Market

The Vendor Management Software market is poised for continued growth, driven by increasing regulatory pressures, evolving supply chains, and the ongoing adoption of innovative technologies. Opportunities abound for vendors that can offer scalable, secure, and user-friendly solutions integrated with AI and machine learning capabilities. Companies focusing on niche market segments and offering specialized solutions will also be well-positioned to succeed in this dynamic market. The long-term outlook remains optimistic, with a substantial market expansion predicted across diverse geographic regions and industry verticals.

Vendor Management Software Industry Segmentation

-

1. Deployment

- 1.1. On-premise

- 1.2. Cloud

-

2. End-user Industry

- 2.1. Retail

- 2.2. BFSI

- 2.3. Manufacturing

- 2.4. IT & Telecommunications

- 2.5. Other End-user Industries

Vendor Management Software Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Vendor Management Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 14.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Need to Minimize the Administrative Costs; Increased Adoption of Cloud Based Computing

- 3.3. Market Restrains

- 3.3.1. High Implementation and Maintenance Cost

- 3.4. Market Trends

- 3.4.1. Retail Sector is Expected to Hold the Largest Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. BFSI

- 5.2.3. Manufacturing

- 5.2.4. IT & Telecommunications

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. North America Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. On-premise

- 6.1.2. Cloud

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. BFSI

- 6.2.3. Manufacturing

- 6.2.4. IT & Telecommunications

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Europe Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. On-premise

- 7.1.2. Cloud

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Retail

- 7.2.2. BFSI

- 7.2.3. Manufacturing

- 7.2.4. IT & Telecommunications

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Asia Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. On-premise

- 8.1.2. Cloud

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Retail

- 8.2.2. BFSI

- 8.2.3. Manufacturing

- 8.2.4. IT & Telecommunications

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Australia and New Zealand Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. On-premise

- 9.1.2. Cloud

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Retail

- 9.2.2. BFSI

- 9.2.3. Manufacturing

- 9.2.4. IT & Telecommunications

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Latin America Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. On-premise

- 10.1.2. Cloud

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Retail

- 10.2.2. BFSI

- 10.2.3. Manufacturing

- 10.2.4. IT & Telecommunications

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Middle East and Africa Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 11.1.1. On-premise

- 11.1.2. Cloud

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Retail

- 11.2.2. BFSI

- 11.2.3. Manufacturing

- 11.2.4. IT & Telecommunications

- 11.2.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 12. North America Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Europe Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Asia Pacific Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Latin America Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Middle East and Africa Vendor Management Software Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1.

- 17. Competitive Analysis

- 17.1. Market Share Analysis 2024

- 17.2. Company Profiles

- 17.2.1 Ncontracts LLC

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 IBM Corporation

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 HICX Solutions

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 Intelex Technologies Inc

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 Coupa Software Inc

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.6 LogicManager Inc

- 17.2.6.1. Overview

- 17.2.6.2. Products

- 17.2.6.3. SWOT Analysis

- 17.2.6.4. Recent Developments

- 17.2.6.5. Financials (Based on Availability)

- 17.2.7 SalesWarp

- 17.2.7.1. Overview

- 17.2.7.2. Products

- 17.2.7.3. SWOT Analysis

- 17.2.7.4. Recent Developments

- 17.2.7.5. Financials (Based on Availability)

- 17.2.8 MetricStream Inc

- 17.2.8.1. Overview

- 17.2.8.2. Products

- 17.2.8.3. SWOT Analysis

- 17.2.8.4. Recent Developments

- 17.2.8.5. Financials (Based on Availability)

- 17.2.9 MasterControl Inc

- 17.2.9.1. Overview

- 17.2.9.2. Products

- 17.2.9.3. SWOT Analysis

- 17.2.9.4. Recent Developments

- 17.2.9.5. Financials (Based on Availability)

- 17.2.10 Quantivate LLC *List Not Exhaustive

- 17.2.10.1. Overview

- 17.2.10.2. Products

- 17.2.10.3. SWOT Analysis

- 17.2.10.4. Recent Developments

- 17.2.10.5. Financials (Based on Availability)

- 17.2.11 Gatekeeper

- 17.2.11.1. Overview

- 17.2.11.2. Products

- 17.2.11.3. SWOT Analysis

- 17.2.11.4. Recent Developments

- 17.2.11.5. Financials (Based on Availability)

- 17.2.12 SAP SE

- 17.2.12.1. Overview

- 17.2.12.2. Products

- 17.2.12.3. SWOT Analysis

- 17.2.12.4. Recent Developments

- 17.2.12.5. Financials (Based on Availability)

- 17.2.1 Ncontracts LLC

List of Figures

- Figure 1: Vendor Management Software Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Vendor Management Software Industry Share (%) by Company 2024

List of Tables

- Table 1: Vendor Management Software Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 3: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Vendor Management Software Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Vendor Management Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Vendor Management Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Vendor Management Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Vendor Management Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Vendor Management Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 16: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 17: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 19: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 20: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 22: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 23: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 25: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 26: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 28: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 29: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Vendor Management Software Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 31: Vendor Management Software Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 32: Vendor Management Software Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vendor Management Software Industry?

The projected CAGR is approximately 14.00%.

2. Which companies are prominent players in the Vendor Management Software Industry?

Key companies in the market include Ncontracts LLC, IBM Corporation, HICX Solutions, Intelex Technologies Inc, Coupa Software Inc, LogicManager Inc, SalesWarp, MetricStream Inc, MasterControl Inc, Quantivate LLC *List Not Exhaustive, Gatekeeper, SAP SE.

3. What are the main segments of the Vendor Management Software Industry?

The market segments include Deployment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need to Minimize the Administrative Costs; Increased Adoption of Cloud Based Computing.

6. What are the notable trends driving market growth?

Retail Sector is Expected to Hold the Largest Share.

7. Are there any restraints impacting market growth?

High Implementation and Maintenance Cost.

8. Can you provide examples of recent developments in the market?

May 2022: CUNA Strategic Services (CSS) chose CUVM, the LEVERAGE vendor management system, as one of only two alliance suppliers of vendor management solutions. CSS builds strategic partnership agreements to provide credit unions with cutting-edge solutions that promote member development and operational excellence. Through this agreement, credit unions will access the whole range of vendor management and regulatory due diligence products and services that CUVM provides.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vendor Management Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vendor Management Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vendor Management Software Industry?

To stay informed about further developments, trends, and reports in the Vendor Management Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence