Key Insights

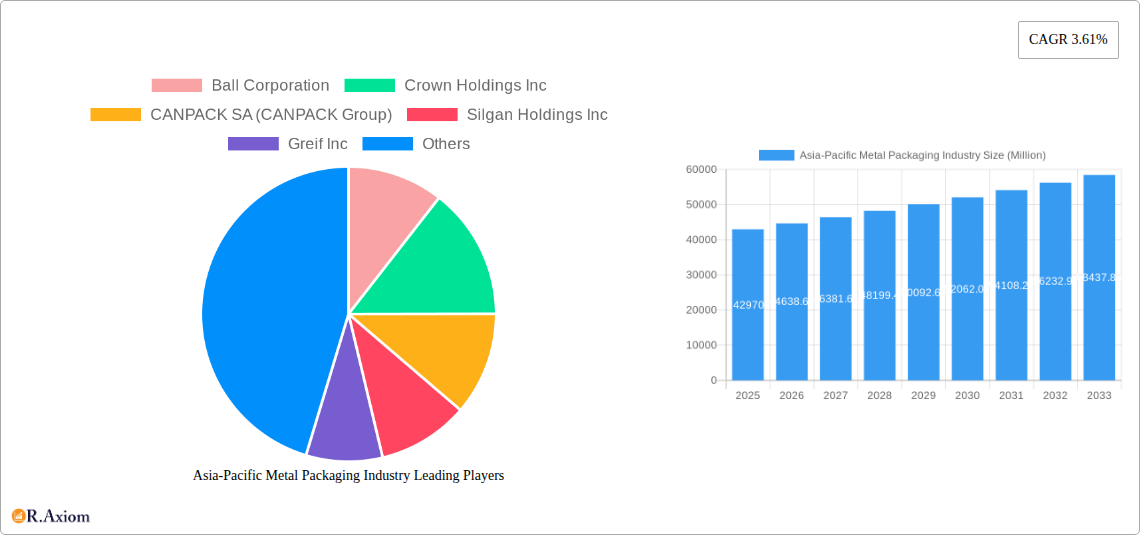

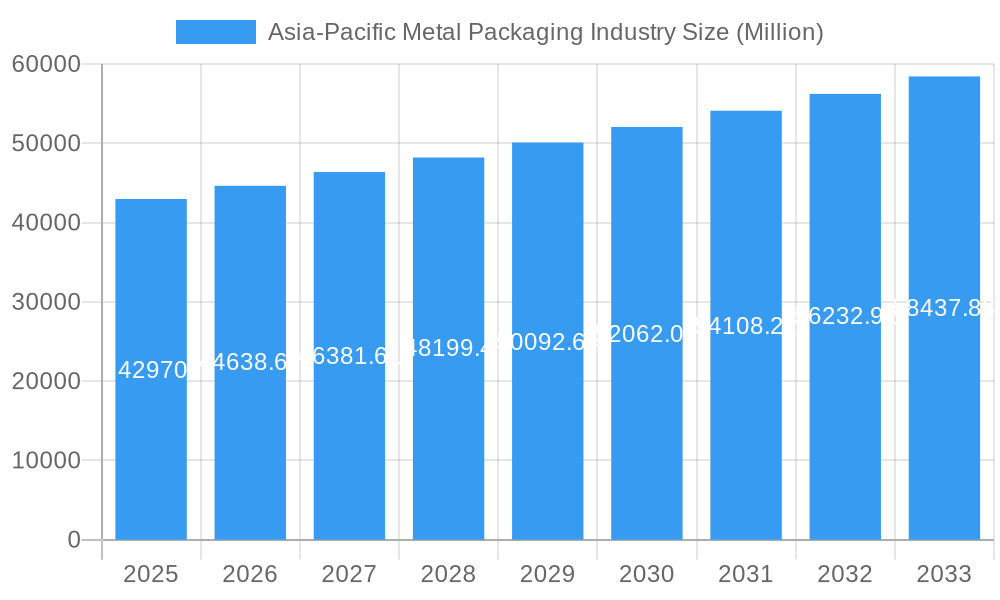

The Asia-Pacific metal packaging industry, currently valued at approximately $42.97 billion in 2025, is projected to experience robust growth, driven by several key factors. Rising disposable incomes, particularly in rapidly developing economies like India and China, are fueling increased consumer spending on packaged goods, thereby boosting demand for metal packaging. The region's burgeoning food and beverage sector, coupled with a growing preference for convenient, shelf-stable products, further strengthens this demand. Furthermore, the inherent properties of metal packaging—its durability, recyclability, and ability to protect product quality—contribute to its continued appeal over alternative packaging materials. Sustainable packaging solutions are gaining traction, with companies investing in lightweighting and improving recyclability initiatives to meet evolving consumer and regulatory demands. This trend is expected to further propel the market's growth trajectory.

Asia-Pacific Metal Packaging Industry Market Size (In Billion)

However, challenges remain. Fluctuations in raw material prices, particularly aluminum and steel, pose a significant risk to profitability. Increasing competition from flexible packaging alternatives, such as plastic and paper-based options, also presents a challenge. To mitigate these challenges, industry players are focusing on innovation, exploring new materials and technologies to enhance product offerings and reduce costs. This includes the development of more sustainable and eco-friendly metal packaging solutions, catering to the growing environmental consciousness of consumers. The ongoing focus on enhancing supply chain efficiency and adopting advanced manufacturing technologies will also play a crucial role in shaping the industry's future. Overall, the Asia-Pacific metal packaging market is anticipated to maintain a healthy growth trajectory over the forecast period (2025-2033), albeit with some inherent volatility due to external factors.

Asia-Pacific Metal Packaging Industry Company Market Share

Asia-Pacific Metal Packaging Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Asia-Pacific metal packaging industry, covering market size, growth drivers, challenges, key players, and future outlook. The report utilizes data from the historical period (2019-2024), base year (2025), and estimated year (2025) to forecast market trends until 2033. This crucial analysis is essential for stakeholders seeking to navigate the dynamic landscape of this thriving sector.

Asia-Pacific Metal Packaging Industry Market Concentration & Innovation

The Asia-Pacific metal packaging market is characterized by a moderately concentrated landscape, featuring a core group of major players who collectively hold a substantial portion of the market share. While precise figures necessitate in-depth proprietary data analysis, it is estimated that the top five key entities command approximately [XX]% of the total market revenue in 2025. This concentration is largely attributed to the strategic advantages of economies of scale, well-established brand equity, and extensive, robust distribution networks. Simultaneously, the market presents significant opportunities and a dynamic environment for innovation, particularly in the development of sustainable packaging solutions and the adoption of advanced manufacturing technologies.

- Key Innovation Drivers: A paramount driver of innovation is the escalating global emphasis on sustainability. This translates into a strong push towards lightweighting metal packaging, the utilization of highly recyclable materials, and a concerted effort to reduce overall carbon footprints throughout the production and lifecycle of packaging. Furthermore, advancements in cutting-edge printing, specialized coating techniques, and sophisticated shaping technologies are continuously enhancing both the functional performance and the aesthetic appeal of metal packaging products.

- Evolving Regulatory Frameworks: Government regulations, increasingly focused on environmental protection and ensuring food safety standards, play a crucial role in influencing packaging design choices and the selection of materials. The compliance requirements can vary significantly from one country to another, presenting a dual landscape of both challenges and strategic opportunities for businesses operating within the region.

- Competitive Landscape of Product Substitutes: The metal packaging industry actively navigates competition from alternative packaging materials, most notably plastics and paperboard. However, metal packaging often retains a distinct competitive advantage due to its inherent superior barrier properties, its high recyclability rate, and its strong brand-building capabilities, which resonate well with consumers.

- Shifting End-User Trends: Evolving consumer preferences are a significant force shaping the industry. The growing demand for convenience in product consumption, a trend towards premiumization in product offerings, and an increasing preference for sustainable and eco-friendly products are collectively influencing packaging choices and driving innovation initiatives across the sector.

- Strategic Mergers & Acquisitions (M&A) Activities: The Asia-Pacific metal packaging industry is a vibrant arena for mergers and acquisitions. Deal values are observed to range annually from [XX] Million to [XX] Million. These strategic transactions are frequently undertaken with the objectives of consolidating market share, broadening geographic operational reach, and integrating pioneering and innovative technologies. The average deal size for the period spanning 2019-2024 is estimated to be around [XX] Million.

Asia-Pacific Metal Packaging Industry Industry Trends & Insights

The metal packaging market in the Asia-Pacific region is currently experiencing a phase of robust and sustained growth. This expansion is propelled by a confluence of favorable factors, including a notable rise in disposable incomes, the ongoing process of urbanization across many nations, and a significant surge in the demand for a wide array of packaged food and beverage products. The market is strategically projected to achieve a Compound Annual Growth Rate (CAGR) of [XX]% during the comprehensive forecast period spanning from 2025 to 2033. This upward trajectory is further amplified by the increasing adoption of metal packaging across a diverse spectrum of end-use sectors. These include, but are not limited to, the food and beverage industry, personal care products, pharmaceuticals, and various industrial goods. Technological advancements, such as the widespread implementation of automation in production lines and the adoption of digital printing capabilities, are actively optimizing manufacturing processes and enabling enhanced product customization. Concurrently, shifting consumer preferences, leaning towards convenience, a desire for premiumization, and a strong emphasis on sustainability and aesthetically pleasing packaging, are collectively reshaping the market dynamics. Competition within the industry remains exceptionally intense, with both established, long-standing players and agile new entrants vigorously competing for market share. Market penetration is particularly pronounced in more mature economies such as Japan, Australia, and South Korea, while substantial growth opportunities are readily available in rapidly developing emerging markets like India and across the vibrant Southeast Asian region.

Dominant Markets & Segments in Asia-Pacific Metal Packaging Industry

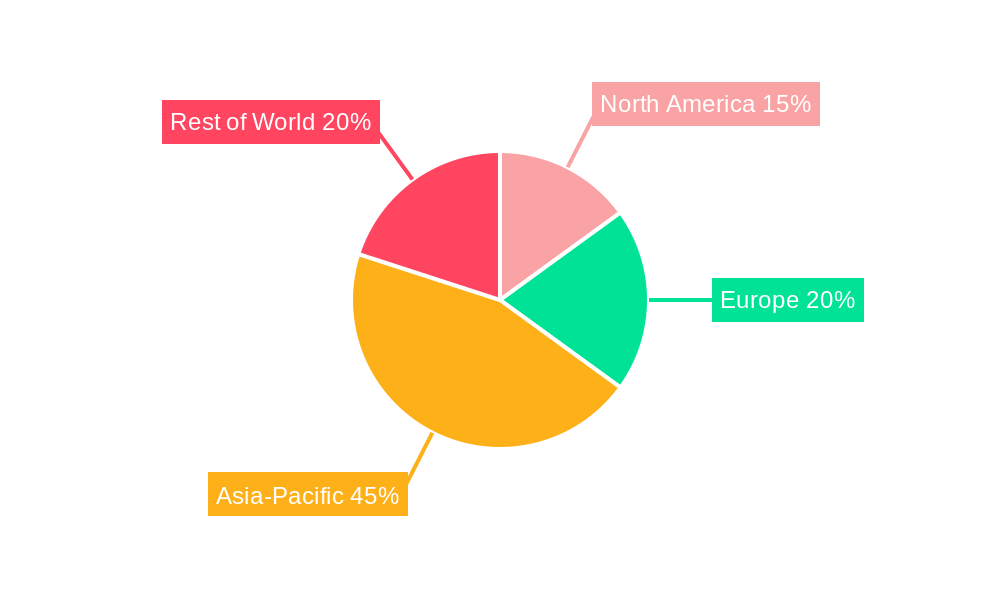

China unequivocally holds the dominant position within the Asia-Pacific metal packaging market, projected to account for an impressive [XX]% of the regional market share in 2025. This pronounced dominance is a direct consequence of a potent combination of advantageous factors:

- Pivotal Drivers in China:

- The nation's sustained rapid economic growth and the continuous expansion of its substantial middle class, leading to increased purchasing power.

- The presence of robust infrastructure that effectively supports both large-scale manufacturing operations and efficient distribution networks.

- Favorable government policies and initiatives that actively promote and support industrial development and manufacturing capabilities.

- The existence of a vast and ever-growing domestic food and beverage market, creating consistent and high demand.

Beyond China, other significant markets that contribute substantially to the regional landscape include India, Japan, South Korea, and Australia. Analyzing the market segments, the beverage cans segment stands out as the largest and most prominent, closely followed by the food cans segment and other diverse metal packaging applications. The ongoing robust growth of these key segments is anticipated to play a pivotal role in driving the overall expansion of the industry. A more detailed analysis substantiates that the clear dominance of specific countries within the market is fundamentally underpinned by a unique interplay of their respective economic policies, the developmental stages of their infrastructure, and the distinct preferences of their consumer bases.

Asia-Pacific Metal Packaging Industry Product Developments

Significant advancements in metal packaging technology are driving product innovation. Lightweighting through advanced manufacturing processes such as compression bottom reform (CBR) is enhancing sustainability and reducing material costs. The integration of smart packaging features such as QR codes and RFID tags is enhancing consumer engagement and product traceability. These innovations are enhancing the competitive advantages of metal packaging by offering improved performance, sustainability, and brand differentiation.

Report Scope & Segmentation Analysis

This report segments the Asia-Pacific metal packaging market based on several key factors:

- By Material: Aluminum, Steel, and Others. Aluminum is the leading material, driven by its lightweight properties and recyclability. Steel holds a significant share, particularly in food canning applications.

- By Product Type: Cans (Beverage cans, Food cans, Aerosol cans, Other cans), Closures, Drums, and other metal packaging forms. Each segment offers different growth potential and competitive dynamics.

- By End-Use Industry: Food & Beverage, Personal Care, Pharmaceuticals, Industrial goods, and others. Growth rates are varying depending on economic and market conditions.

- By Country: This report provides a detailed analysis for major countries in the region.

Each segment's growth projection, market size, and competitive landscape are thoroughly examined in the complete report.

Key Drivers of Asia-Pacific Metal Packaging Industry Growth

Several fundamental drivers are critically influencing and propelling the growth trajectory of the Asia-Pacific metal packaging industry:

- Technological Advancements: Continuous innovations across material science, manufacturing processes, and sophisticated printing technologies are instrumental in enhancing overall product quality, improving sustainability credentials, and making metal packaging more cost-effective and accessible.

- Economic Growth: The prevailing trend of rising disposable incomes across the region, coupled with the expanding size and influence of the middle class, is directly fueling a greater demand for a wider variety of packaged goods.

- Favorable Government Regulations: Strategic government policies that actively support industrial development initiatives and promote environmental sustainability are creating an increasingly conducive and supportive ecosystem for industry expansion and investment.

- Evolving Consumer Preferences: The discernible and growing consumer demand for convenience in their purchasing and consumption habits, a trend towards premiumization in product offerings, and an increasing prioritization of sustainable packaging solutions are collectively shaping and directing key industry trends.

Challenges in the Asia-Pacific Metal Packaging Industry Sector

The industry faces several challenges:

- Fluctuating raw material prices: Aluminum and steel prices can significantly impact profitability.

- Environmental concerns: Meeting increasing sustainability demands requires continuous innovation and investment in eco-friendly solutions.

- Intense competition: The market is fragmented, with numerous players competing on price, quality, and innovation. This competition is pressuring profit margins in some areas.

- Supply chain disruptions: Global events can cause supply chain issues, impacting production and delivery timelines. This has resulted in estimated xx Million in lost revenue for some companies between 2020 and 2022.

Emerging Opportunities in Asia-Pacific Metal Packaging Industry

Significant opportunities exist for growth:

- Sustainable packaging solutions: Demand for eco-friendly packaging is driving innovation in recyclable and biodegradable materials.

- Smart packaging technologies: Integration of sensors and tracking systems enhances product security and consumer engagement.

- Expansion into emerging markets: Untapped potential exists in rapidly growing economies across the region.

- Premiumization and customization: Rising consumer demand for premium and customized packaging offers lucrative avenues for growth.

Leading Players in the Asia-Pacific Metal Packaging Industry Market

- Ball Corporation

- Crown Holdings Inc

- CANPACK SA (CANPACK Group)

- Silgan Holdings Inc

- Greif Inc

- Mauser Packaging Solutions

- Balmer Lawrie & Co Ltd

- Closure Systems International Inc (CSI)

- Guala Closures SpA

- Schutz GmbH & Co KGaA

- Ceylon Beverage Can Pvt Ltd

- Casablanca Industries Pvt Ltd

- *This list is not exhaustive and represents a selection of prominent players in the market.

Key Developments in Asia-Pacific Metal Packaging Industry Industry

- September 2023: Casablanca Industries Pvt. Ltd announced plans to establish a manufacturing unit for aluminum monobloc aerosol cans at the Adali Industrial Area in the Sindhudurg district of Maharashtra. This expansion reflects the growing demand for aerosol packaging in the region.

- March 2024: Toyo Seikan Co. Ltd announced the development of the lightest aluminum can body in Japan using compression bottom reform (CBR) technology. This innovation highlights the industry's focus on sustainability and lightweighting.

Strategic Outlook for Asia-Pacific Metal Packaging Industry Market

The Asia-Pacific metal packaging market is poised for sustained growth, driven by continuous innovation, expanding consumer base, and increasing demand across various end-use sectors. The focus on sustainable packaging, smart packaging technologies, and expansion into emerging markets will shape the industry's future. Companies that adapt to changing consumer preferences, embrace sustainable practices, and invest in technological advancements are well-positioned to capitalize on the significant growth opportunities that lie ahead. The market is expected to reach xx Million by 2033, presenting lucrative prospects for investors and industry players.

Asia-Pacific Metal Packaging Industry Segmentation

-

1. Material Type

- 1.1. Aluminium

- 1.2. Steel

-

2. Product Type

-

2.1. Cans

- 2.1.1. Food Cans

- 2.1.2. Beverage Cans

- 2.1.3. Aerosol Cans

- 2.2. Bulk Containers

- 2.3. Shipping Barrels and Drums

- 2.4. Caps & Closures

- 2.5. Other Product Types

-

2.1. Cans

-

3. End-user Industry

- 3.1. Beverage

- 3.2. Food

- 3.3. Cosmetics & Personal Care

- 3.4. Household

- 3.5. Paints & Varnishes

- 3.6. Other End-user Industries

Asia-Pacific Metal Packaging Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Metal Packaging Industry Regional Market Share

Geographic Coverage of Asia-Pacific Metal Packaging Industry

Asia-Pacific Metal Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.61% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Aluminium

- 5.1.2. Steel

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Cans

- 5.2.1.1. Food Cans

- 5.2.1.2. Beverage Cans

- 5.2.1.3. Aerosol Cans

- 5.2.2. Bulk Containers

- 5.2.3. Shipping Barrels and Drums

- 5.2.4. Caps & Closures

- 5.2.5. Other Product Types

- 5.2.1. Cans

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Beverage

- 5.3.2. Food

- 5.3.3. Cosmetics & Personal Care

- 5.3.4. Household

- 5.3.5. Paints & Varnishes

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Asia-Pacific Metal Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Aluminium

- 6.1.2. Steel

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Cans

- 6.2.1.1. Food Cans

- 6.2.1.2. Beverage Cans

- 6.2.1.3. Aerosol Cans

- 6.2.2. Bulk Containers

- 6.2.3. Shipping Barrels and Drums

- 6.2.4. Caps & Closures

- 6.2.5. Other Product Types

- 6.2.1. Cans

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Beverage

- 6.3.2. Food

- 6.3.3. Cosmetics & Personal Care

- 6.3.4. Household

- 6.3.5. Paints & Varnishes

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ball Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Crown Holdings Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 CANPACK SA (CANPACK Group)

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Silgan Holdings Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Greif Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mauser Packaging Solutions

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Balmer Lawrie & Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Closure Systems International Inc (CSI)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Guala Closures SpA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Schutz GmbH & Co KGaA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Ceylon Beverage Can Pvt Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Casablanca Industries Pvt Ltd*List Not Exhaustive

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Ball Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Metal Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Metal Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by Material Type 2020 & 2033

- Table 3: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 5: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 10: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by Material Type 2020 & 2033

- Table 11: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 12: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 13: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Asia-Pacific Metal Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Metal Packaging Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 17: China Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Japan Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: South Korea Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: India Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: New Zealand Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: New Zealand Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Indonesia Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Malaysia Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Malaysia Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Singapore Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Singapore Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Thailand Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Thailand Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 37: Vietnam Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Vietnam Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 39: Philippines Asia-Pacific Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Philippines Asia-Pacific Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Metal Packaging Industry?

The projected CAGR is approximately 3.61%.

2. Which companies are prominent players in the Asia-Pacific Metal Packaging Industry?

Key companies in the market include Ball Corporation, Crown Holdings Inc, CANPACK SA (CANPACK Group), Silgan Holdings Inc, Greif Inc, Mauser Packaging Solutions, Balmer Lawrie & Co Ltd, Closure Systems International Inc (CSI), Guala Closures SpA, Schutz GmbH & Co KGaA, Ceylon Beverage Can Pvt Ltd, Casablanca Industries Pvt Ltd*List Not Exhaustive.

3. What are the main segments of the Asia-Pacific Metal Packaging Industry?

The market segments include Material Type, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.97 Million as of 2022.

5. What are some drivers contributing to market growth?

Metal Containers Preferred for Edible Oil Packaging along with Increasing Consumption of Edible Oil in India; Increasing Adoption of Aluminum Flexible Tubes in the Cosmetics and Personal Care Industry.

6. What are the notable trends driving market growth?

Metal Containers Preferred for Edible Oil Packaging. Along with Increasing Consumption of Edible Oil. in India.

7. Are there any restraints impacting market growth?

Metal Containers Preferred for Edible Oil Packaging along with Increasing Consumption of Edible Oil in India; Increasing Adoption of Aluminum Flexible Tubes in the Cosmetics and Personal Care Industry.

8. Can you provide examples of recent developments in the market?

March 2024: Toyo Seikan Co. Ltd announced the development of the lightest aluminum can body in Japan. The company used compression bottom reform (CBR) technology to reinforce the bottom of the beverage can, which will help the company reduce greenhouse gas (GHG) emissions by lowering the weight of the can.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Metal Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Metal Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Metal Packaging Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Metal Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence