Key Insights

The global Banking System Software market is projected to reach an estimated USD 17.94 billion by 2025. This substantial growth is propelled by widespread digital transformation within the financial sector, increased demand for cloud-based solutions, and the imperative for robust security against evolving cyber threats. Financial institutions are prioritizing the modernization of core banking systems to boost operational efficiency, enhance customer experiences, and ensure regulatory compliance. The expansion of open banking, facilitated by APIs, is fostering innovation and enabling new service development, leading to a more interconnected and customer-centric financial ecosystem. This necessitates agile and scalable software solutions. Additionally, the growing focus on personalized banking and data analytics for risk management and fraud detection are key market drivers.

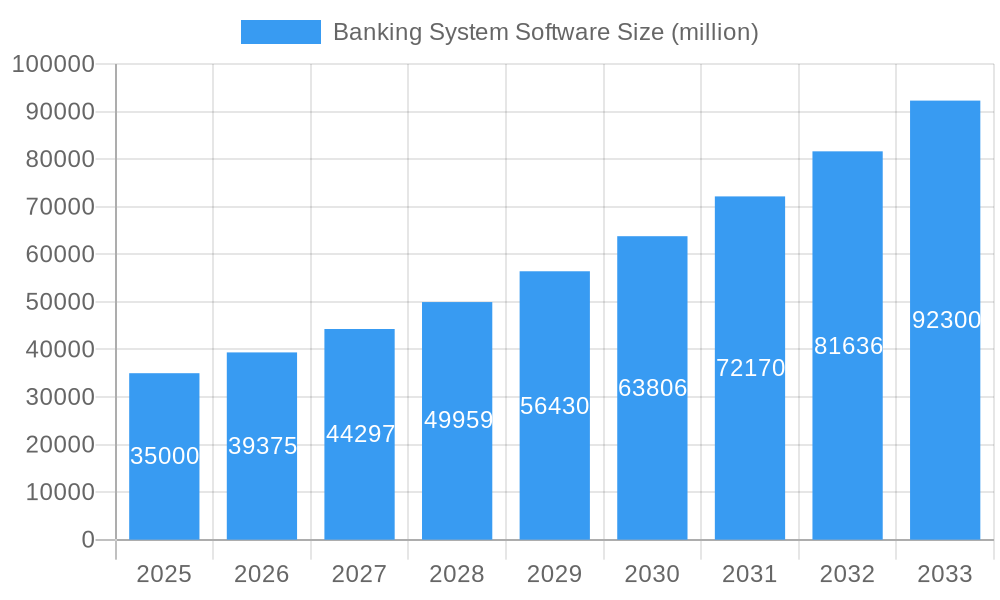

Banking System Software Market Size (In Billion)

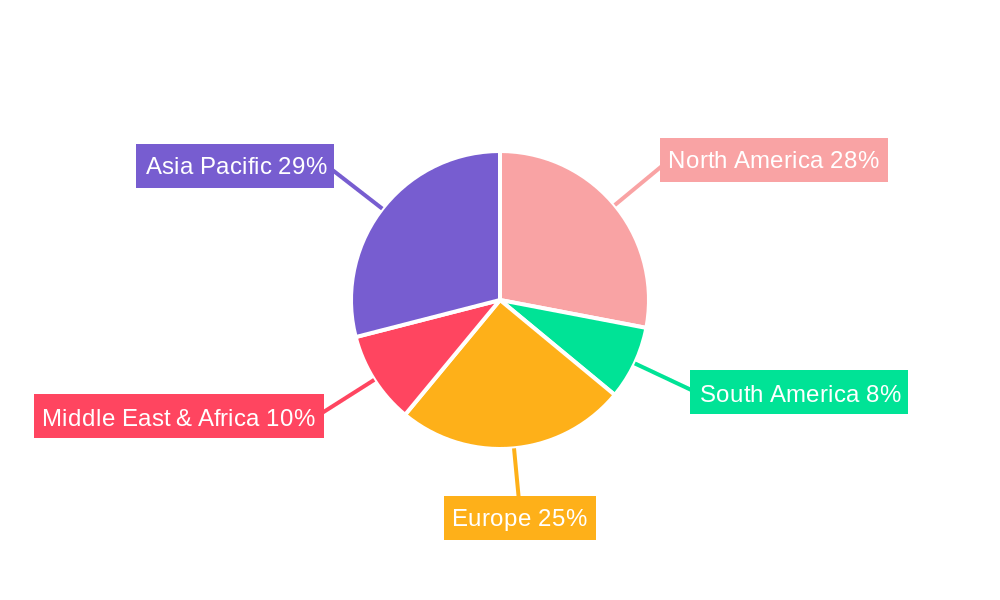

The market is anticipated to experience a compound annual growth rate (CAGR) of 15.3% from 2025 to 2033. Key segments, including PC and Mobile Terminal applications, are showing significant expansion, aligning with the trend towards omnichannel banking. Windows and Android platforms are expected to dominate in terms of operating systems due to their broad adoption. The Asia Pacific region is identified as a high-growth area, driven by rapid digitalization, a large population adopting digital financial services, and substantial FinTech investments. North America and Europe remain significant markets for advanced solutions, including AI-powered analytics and blockchain integration. While initial implementation costs and legacy system integration present challenges, the adoption of modular and cloud-native solutions is mitigating these restraints, ensuring sustained market growth.

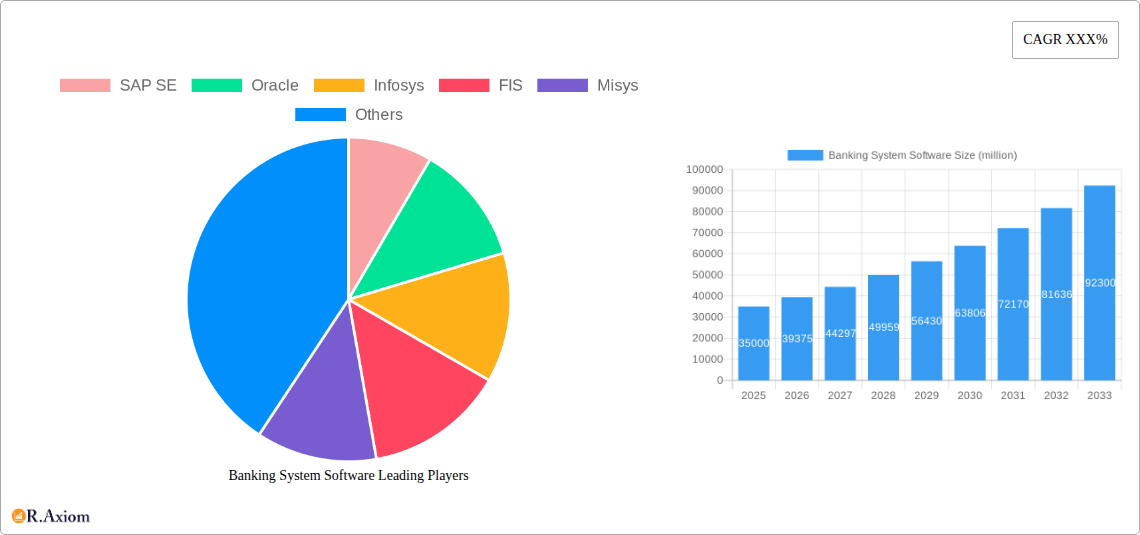

Banking System Software Company Market Share

Banking System Software Market Concentration & Innovation

The banking system software market is characterized by moderate to high concentration, with a few dominant players like SAP SE, Oracle, Infosys, FIS, and Temenos Group holding significant market shares, collectively estimated to be over 70% of the global market value. These established vendors leverage their extensive product portfolios, global reach, and robust R&D investments to maintain their competitive edge. Innovation is a key differentiator, driven by the increasing demand for digital transformation, cloud-based solutions, and advanced analytics in the financial sector. Regulatory frameworks, such as GDPR and various financial compliance mandates, are also shaping innovation by pushing for enhanced security, data privacy, and transparent operations. Product substitutes are emerging, including specialized fintech solutions and open banking platforms, which, while not direct replacements for core banking systems, are influencing customer expectations and pushing incumbents to adapt. End-user trends are heavily skewed towards enhanced customer experience, personalized services, and seamless digital interactions, compelling software providers to develop more agile and user-centric applications. Mergers and acquisitions (M&A) activity is a significant factor in market concentration, with strategic acquisitions by larger players to broaden their offerings, acquire new technologies, or gain market access. Past M&A deal values are in the hundreds of millions of dollars, consolidating the market further. For instance, the acquisition of smaller fintech firms by giants like SAP SE and Oracle highlights this trend.

- Market Concentration: Estimated to be over 70% held by the top 5 vendors.

- Innovation Drivers: Digital transformation, cloud adoption, AI/ML integration, cybersecurity.

- Regulatory Impact: Focus on compliance, data security, and financial inclusion.

- Product Substitutes: Fintech solutions, open banking APIs, specialized niche software.

- End-User Trends: Demand for personalized digital banking, omnichannel experiences, and real-time services.

- M&A Activity: Significant consolidation driven by strategic acquisitions and technology integration. M&A deal values often reach hundreds of millions of dollars.

Banking System Software Industry Trends & Insights

The global banking system software market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 8.5% from 2025 to 2033. This robust growth is primarily fueled by the relentless digital transformation initiatives undertaken by financial institutions worldwide. Banks are increasingly migrating from legacy systems to modern, integrated core banking platforms that offer greater flexibility, scalability, and efficiency. The widespread adoption of cloud computing is a pivotal trend, enabling banks to reduce infrastructure costs, enhance data security, and deploy new services faster. This shift to cloud-native architectures is transforming how banking software is developed, deployed, and managed. Technological disruptions, including the integration of Artificial Intelligence (AI) and Machine Learning (ML), are revolutionizing banking operations. These technologies are being leveraged for fraud detection, risk management, personalized customer service through chatbots, and algorithmic trading. The burgeoning adoption of mobile banking applications and the increasing preference for digital channels by consumers are compelling banks to invest in mobile-first banking solutions and enhance their mobile terminal applications. This shift in consumer preferences is driving market penetration of mobile-centric banking software. Furthermore, the rise of open banking and the increasing demand for API-driven ecosystems are fostering innovation and collaboration within the industry. Banks are seeking software solutions that facilitate seamless integration with third-party service providers, enabling them to offer a broader range of financial products and services. The competitive landscape is dynamic, with established players like SAP SE, Oracle, and Temenos Group constantly innovating to meet evolving market demands. Simultaneously, agile fintech startups are introducing disruptive solutions, forcing traditional banks and their software providers to adapt rapidly. The increasing digitalization of economies, particularly in emerging markets, also presents a significant growth opportunity for banking system software providers. The need for robust, scalable, and secure banking infrastructure to support financial inclusion and economic development is paramount. The integration of advanced analytics and big data capabilities is another key trend, empowering banks to gain deeper insights into customer behavior, market trends, and operational efficiency, thereby driving more informed decision-making. This continuous evolution of the banking landscape, driven by technology and consumer behavior, underpins the strong growth trajectory of the banking system software market. The market penetration of advanced banking solutions is expected to surpass 65% by 2033.

Dominant Markets & Segments in Banking System Software

The banking system software market exhibits strong regional dominance, with North America currently leading in terms of market share, closely followed by Europe. Asia-Pacific is emerging as the fastest-growing region, driven by rapid economic development, increasing financial inclusion initiatives, and the widespread adoption of digital technologies. Within North America, the United States accounts for a significant portion of the market, fueled by its highly developed financial infrastructure, large banking institutions, and early adoption of technological advancements. Key drivers for dominance in these regions include favorable economic policies that encourage financial innovation, robust regulatory frameworks that support digital banking, and substantial investments in IT infrastructure by financial institutions. The emphasis on enhancing customer experience and digitalizing banking services has led to a high demand for sophisticated banking system software.

Application Segment Dominance:

The Mobile Terminal application segment is experiencing explosive growth and is projected to become the dominant application in the coming years, projected to capture over 50% of the market share by 2033. This dominance is propelled by the undeniable shift in consumer behavior towards mobile-first banking. Customers increasingly prefer managing their finances, conducting transactions, and accessing banking services through their smartphones and tablets. The proliferation of smartphones, improved mobile internet connectivity, and the development of user-friendly mobile banking applications are key drivers. Banks are investing heavily in developing feature-rich mobile platforms to cater to this demand, offering services like mobile check deposits, peer-to-peer payments, and personalized financial insights directly on mobile devices. This trend necessitates banking system software that is seamlessly integrated with mobile front-end applications and can support the unique demands of a mobile environment, including real-time updates, push notifications, and robust security protocols to protect sensitive financial data.

Type Segment Dominance:

Among the different operating system types, Android is emerging as the dominant platform for mobile banking applications, reflecting its global market share in smartphones. The widespread adoption of Android devices across various demographics and economic strata makes it a crucial platform for financial institutions aiming for broad market reach. Consequently, banking system software providers are prioritizing the development and optimization of their solutions for the Android ecosystem. While iOS also holds significant importance, particularly in developed markets, Android's broader penetration globally positions it as the leading type segment. The flexibility and open nature of the Android platform allow for greater customization and integration capabilities, which are attractive to both developers and end-users. The continuous evolution of the Android operating system and its associated hardware capabilities further solidify its position.

- Regional Dominance: North America and Europe lead, with Asia-Pacific showing the fastest growth.

- Application Dominance: Mobile Terminal is the fastest-growing and projected to become the dominant application segment due to increasing mobile banking adoption.

- Type Segment Dominance: Android is expected to be the dominant type segment for mobile banking applications due to its global market share.

Banking System Software Product Developments

Recent product developments in banking system software focus on enhancing digital customer experience, improving operational efficiency, and bolstering cybersecurity. Innovations include AI-powered chatbots for instant customer support, advanced analytics for personalized financial advisory services, and cloud-native core banking platforms that offer unparalleled scalability and agility. Many vendors are also integrating blockchain technology for secure and transparent transaction processing. The competitive advantage lies in offering modular, API-driven solutions that facilitate seamless integration with third-party fintech applications, enabling banks to expand their service offerings and adapt quickly to market changes.

Banking System Software Report Scope & Segmentation Analysis

This report meticulously analyzes the global Banking System Software market, encompassing critical segments to provide a comprehensive industry overview. The study covers the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033.

Application Segmentation: The market is segmented by application into PC and Mobile Terminal. The PC segment, though mature, continues to be crucial for complex back-office operations and enterprise-level banking management. It is estimated to be valued at over $150 million in 2025. The Mobile Terminal segment is experiencing exponential growth, driven by the increasing adoption of mobile banking services. This segment is projected to reach over $500 million by 2033, highlighting its increasing dominance.

Type Segmentation: The market is further segmented by type: Windows, Android, iOS, and Others. Windows remains a significant platform for desktop banking solutions. Android is anticipated to lead the mobile banking software market due to its widespread global adoption, projected to capture over 60% of the mobile segment by 2033. iOS is also a key platform, particularly in developed markets. The Others segment encompasses emerging mobile operating systems and specialized platforms.

Key Drivers of Banking System Software Growth

The banking system software market is propelled by several powerful growth drivers. Digital transformation remains paramount, with financial institutions investing heavily in modernizing their IT infrastructure to enhance customer experience and operational efficiency. The widespread adoption of cloud computing offers scalability, cost savings, and faster deployment of new services. AI and machine learning are revolutionizing banking by enabling personalized services, advanced fraud detection, and intelligent risk management. The increasing demand for mobile banking services, driven by evolving consumer preferences, necessitates robust mobile-first solutions. Favorable regulatory environments that encourage innovation and competition, such as open banking initiatives, also play a crucial role by fostering new business models and partnerships.

Challenges in the Banking System Software Sector

Despite the robust growth, the banking system software sector faces significant challenges. The high cost of implementing and integrating new core banking systems with legacy infrastructure remains a major hurdle for many institutions. Stringent regulatory compliance requirements across different jurisdictions add complexity and cost to software development and deployment. Cybersecurity threats are constantly evolving, necessitating continuous investment in robust security measures, which can be resource-intensive. Furthermore, the intense competition from established players and agile fintech startups puts pressure on pricing and innovation cycles. The shortage of skilled professionals with expertise in modern banking technologies and cloud migration can also impede progress.

Emerging Opportunities in Banking System Software

Emerging opportunities in the banking system software market are abundant, driven by technological advancements and evolving consumer needs. The growth of embedded finance, where banking services are integrated into non-financial platforms, presents a significant avenue for expansion. The increasing demand for sustainable finance solutions and ESG (Environmental, Social, and Governance) reporting tools is creating a new market niche. The ongoing digital divide in emerging economies offers opportunities for scalable and affordable banking solutions that promote financial inclusion. Furthermore, the continued advancements in AI and blockchain technology will unlock new possibilities for personalized banking experiences, decentralized finance (DeFi) applications, and enhanced security protocols.

Leading Players in the Banking System Software Market

- SAP SE

- Oracle

- Infosys

- FIS

- Misys

- Infrasoft Technologies

- Capgemini

- CoBIS Microfinance Software

- Tata Consultancy Services

- Temenos Group

Key Developments in Banking System Software Industry

- January 2024: Temenos Group launched a new AI-powered digital banking platform, enhancing customer personalization and operational efficiency.

- December 2023: Oracle announced significant upgrades to its cloud-based banking solutions, focusing on data analytics and security.

- October 2023: FIS completed the acquisition of a specialized fintech firm, expanding its payment processing capabilities, with a deal value of approximately $500 million.

- August 2023: Infosys Finacle introduced a new suite of open banking APIs to facilitate seamless integration with third-party applications.

- May 2023: SAP SE announced strategic partnerships with several cloud providers to accelerate the adoption of its banking solutions on public cloud platforms.

- February 2023: Capgemini launched a new consultancy service focused on helping banks navigate the complexities of core banking transformation.

- November 2022: Infrasoft Technologies secured a major contract with a leading European bank for its core banking system upgrade, valued at over $100 million.

- July 2022: Misys (now Finastra) unveiled its new digital lending platform, designed for faster loan origination and servicing.

- April 2022: Tata Consultancy Services (TCS) announced its collaboration with a major Asian bank to implement its BaNCS solution, enhancing digital banking services.

- January 2022: CoBIS Microfinance Software launched a new mobile-first lending solution tailored for microfinance institutions in developing economies.

Strategic Outlook for Banking System Software Market

The strategic outlook for the banking system software market is exceptionally positive, driven by an unwavering demand for digital innovation and customer-centric solutions. The continuous evolution of technology, coupled with increasing regulatory pressures and the growing emphasis on financial inclusion, will shape the market's trajectory. Banks will continue to prioritize investments in cloud-native architectures, AI-driven capabilities, and robust cybersecurity measures to remain competitive. The expansion of open banking ecosystems and the rise of embedded finance will create new avenues for collaboration and service delivery. Financial institutions that strategically adopt agile, modular, and future-proof banking system software will be best positioned to capitalize on emerging opportunities and navigate the dynamic landscape of the global financial industry.

Banking System Software Segmentation

-

1. Application

- 1.1. PC

- 1.2. Mobile Terminal

-

2. Type

- 2.1. Windows

- 2.2. Android

- 2.3. iOS

- 2.4. Others

Banking System Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Banking System Software Regional Market Share

Geographic Coverage of Banking System Software

Banking System Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. PC

- 5.1.2. Mobile Terminal

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Windows

- 5.2.2. Android

- 5.2.3. iOS

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Banking System Software Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. PC

- 6.1.2. Mobile Terminal

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Windows

- 6.2.2. Android

- 6.2.3. iOS

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Banking System Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. PC

- 7.1.2. Mobile Terminal

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Windows

- 7.2.2. Android

- 7.2.3. iOS

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Banking System Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. PC

- 8.1.2. Mobile Terminal

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Windows

- 8.2.2. Android

- 8.2.3. iOS

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Banking System Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. PC

- 9.1.2. Mobile Terminal

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Windows

- 9.2.2. Android

- 9.2.3. iOS

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Banking System Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. PC

- 10.1.2. Mobile Terminal

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Windows

- 10.2.2. Android

- 10.2.3. iOS

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Banking System Software Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. PC

- 11.1.2. Mobile Terminal

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Windows

- 11.2.2. Android

- 11.2.3. iOS

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SAP SE

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Oracle

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Infosys

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 FIS

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Misys

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Infrasoft Technologies

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Capgemini

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CoBIS Microfinance Software

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Tata Consultancy Services

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Temenos Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 SAP SE

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Banking System Software Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Banking System Software Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Banking System Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Banking System Software Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Banking System Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Banking System Software Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Banking System Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Banking System Software Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Banking System Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Banking System Software Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Banking System Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Banking System Software Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Banking System Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Banking System Software Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Banking System Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Banking System Software Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Banking System Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Banking System Software Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Banking System Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Banking System Software Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Banking System Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Banking System Software Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Banking System Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Banking System Software Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Banking System Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Banking System Software Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Banking System Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Banking System Software Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Banking System Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Banking System Software Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Banking System Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Banking System Software Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Banking System Software Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Banking System Software Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Banking System Software Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Banking System Software Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Banking System Software Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Banking System Software Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Banking System Software Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Banking System Software Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Banking System Software Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Banking System Software Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Banking System Software Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Banking System Software Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Banking System Software Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Banking System Software Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Banking System Software Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Banking System Software Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Banking System Software Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Banking System Software Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Banking System Software?

The projected CAGR is approximately 15.3%.

2. Which companies are prominent players in the Banking System Software?

Key companies in the market include SAP SE, Oracle, Infosys, FIS, Misys, Infrasoft Technologies, Capgemini, CoBIS Microfinance Software, Tata Consultancy Services, Temenos Group.

3. What are the main segments of the Banking System Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.94 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Banking System Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Banking System Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Banking System Software?

To stay informed about further developments, trends, and reports in the Banking System Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence