Key Insights

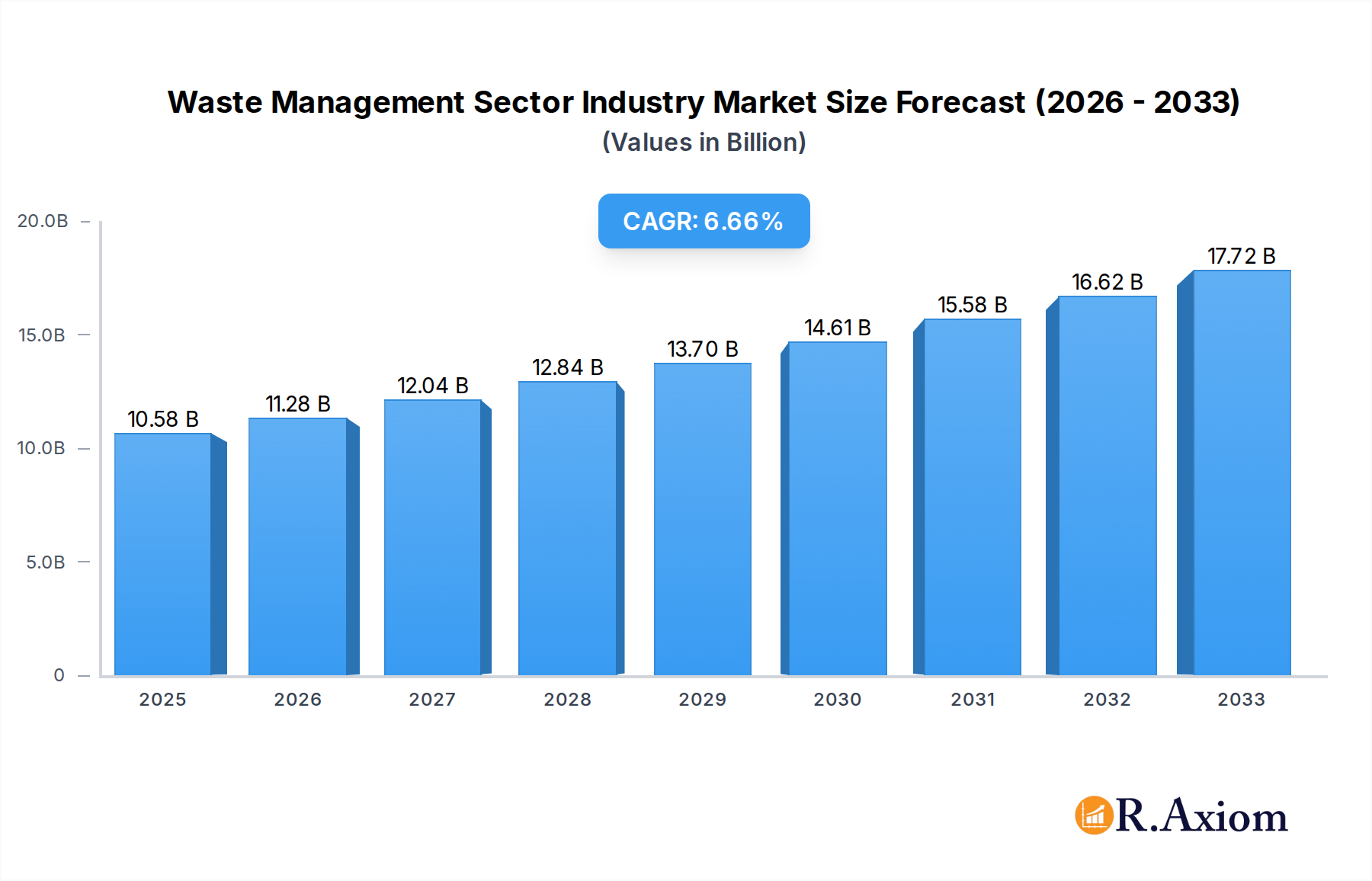

The global Waste Management Sector is poised for robust growth, projected to reach $10.58 billion by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 6.63% through 2033. This significant expansion is fueled by a confluence of critical drivers, including increasingly stringent environmental regulations worldwide, a growing awareness of the detrimental effects of improper waste disposal on public health and ecosystems, and the accelerating pace of industrialization and urbanization, particularly in emerging economies. These factors collectively necessitate more sophisticated and sustainable waste management solutions. The sector is witnessing a pronounced shift towards circular economy principles, with recycling and waste-to-energy initiatives gaining substantial traction as viable alternatives to traditional landfilling. This evolution is further propelled by technological advancements in waste sorting, processing, and energy recovery, making waste management a more efficient and economically attractive industry.

Waste Management Sector Industry Market Size (In Billion)

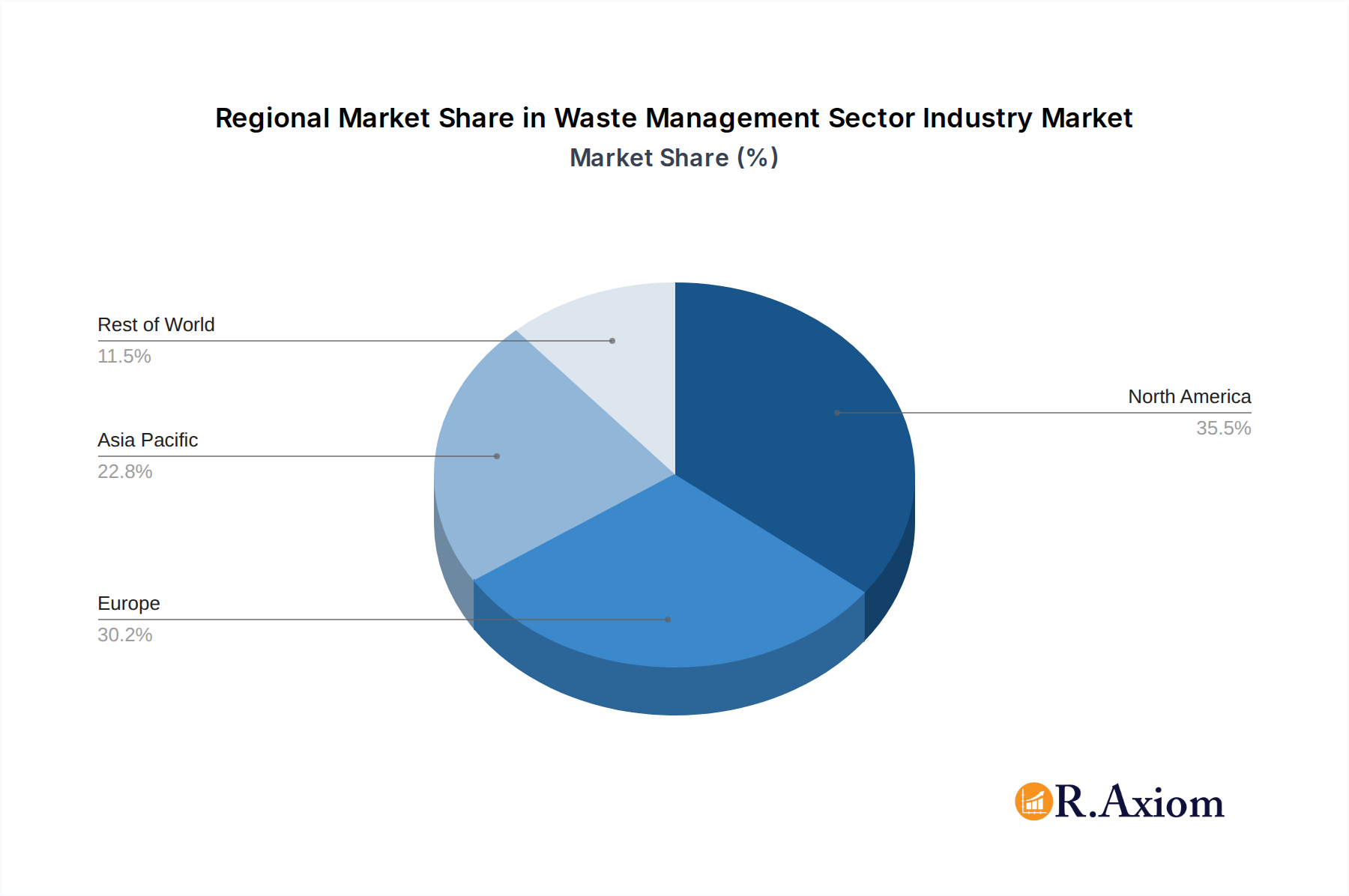

The market is segmented across various waste types, with Industrial waste and Municipal solid waste representing the largest contributors, followed by rapidly growing segments like E-waste and Plastic waste, driven by increased consumption and product obsolescence. Disposal methods are also diversifying, with a move away from sole reliance on landfills towards incineration with energy recovery and comprehensive recycling programs. Key players like Veolia Environment SA, Waste Management Inc., and Biffa Group are at the forefront, investing in innovative technologies and expanding their service portfolios to meet evolving demands. Geographically, North America and Europe currently dominate the market, but the Asia Pacific region, propelled by its dense population and rapid economic development, is expected to emerge as a major growth engine in the coming years. Addressing the escalating volumes of waste generated globally, particularly plastic and electronic waste, remains a significant challenge, yet it also presents substantial opportunities for market expansion and innovation in sustainable waste management practices.

Waste Management Sector Industry Company Market Share

Here is the SEO-optimized, detailed report description for the Waste Management Sector Industry, incorporating high-traffic keywords and adhering to all your specifications.

Waste Management Sector Industry Market Concentration & Innovation

The global waste management sector, a critical component of environmental sustainability, is characterized by moderate market concentration with a significant number of players ranging from large multinational corporations to specialized regional operators. Key entities driving this landscape include Waste Management Inc., Veolia Environnement SA, and Republic Services, alongside emerging regional leaders like Biffa Group and Averda. Innovation is a paramount driver, propelled by advancements in recycling technologies, waste-to-energy solutions, and digital platforms for optimized collection and processing. Regulatory frameworks, such as stringent environmental protection laws and extended producer responsibility schemes, are increasingly shaping industry practices and incentivizing sustainable waste management. Product substitutes, while limited for core waste disposal, are evolving with the rise of circular economy models and advanced material recovery processes. End-user trends are increasingly demanding environmentally conscious disposal and resource recovery services, pushing for greater transparency and efficiency. Mergers and acquisitions (M&A) remain a strategic imperative for market consolidation and expansion. For instance, the Waste Management Inc. acquisition of Advanced Disposal in October 2020, valued at USD 4.6 billion, exemplifies this trend, integrating substantial debt and enhancing operational scale. Similarly, Biffa Group's acquisition of Company Shop Group in February 2021 bolsters its capabilities in surplus product redistribution, reflecting a broader move towards value chain integration and circularity. These M&A activities underscore a strategic push to gain market share, acquire new technologies, and expand service portfolios within the burgeoning global waste management market.

Waste Management Sector Industry Industry Trends & Insights

The waste management sector industry is experiencing robust growth, fueled by an escalating global population, increasing industrialization, and heightened environmental awareness. The market is projected to witness a significant Compound Annual Growth Rate (CAGR) over the forecast period of 2025–2033, driven by a confluence of economic, technological, and regulatory factors. Growing urbanization leads to a surge in municipal solid waste generation, demanding efficient collection and disposal systems. Industrial expansion, particularly in developing economies, contributes to a rising volume of industrial waste, requiring specialized handling and treatment. The escalating concerns around plastic pollution have placed a spotlight on plastic waste management, spurring innovation in recycling technologies and the development of alternative materials. E-waste is another rapidly expanding segment, driven by the short lifecycles of electronic devices and the presence of valuable and hazardous materials, necessitating specialized recycling processes. The healthcare sector's growth further fuels the demand for safe and compliant biomedical waste management. Technological disruptions are at the forefront of industry transformation. Advanced sorting technologies, including AI-powered optical sorters and robotics, are enhancing recycling efficiency and purity. The adoption of digital solutions, such as route optimization software and real-time tracking, is improving operational logistics and reducing costs. Waste-to-energy technologies are gaining traction as a means to reduce landfill reliance and generate renewable energy. Consumer preferences are shifting towards sustainable consumption patterns, leading to increased demand for recycled products and a greater willingness to participate in recycling programs. This evolving consumer behavior is pressuring businesses to adopt more environmentally responsible waste management practices. Competitive dynamics are intensifying, with established players expanding their service offerings and geographic reach through strategic acquisitions and organic growth. The increasing focus on circular economy principles is fostering new business models centered on resource recovery and waste valorization. Market penetration for advanced recycling and waste-to-energy solutions is steadily increasing as regulatory mandates become more stringent and public awareness grows. The overall industry outlook points towards sustained growth and a paradigm shift towards a more circular and sustainable approach to waste management, with a market valuation expected to reach several hundred billion dollars by the end of the forecast period.

Dominant Markets & Segments in Waste Management Sector Industry

The waste management sector industry exhibits significant regional and segmental dominance, driven by varying economic development, regulatory landscapes, and population densities. Globally, North America and Europe currently represent the largest markets, owing to their established infrastructure, stringent environmental regulations, and high levels of consumer awareness concerning waste management. Countries like the United States, Germany, and the United Kingdom lead in market size and adoption of advanced waste management technologies. Asia Pacific, however, is emerging as the fastest-growing region, propelled by rapid industrialization, increasing urbanization, and a growing middle class, leading to higher waste generation.

Within the waste types, Municipal Solid Waste (MSW) consistently holds the largest market share due to its sheer volume generated by households and commercial establishments. The increasing population density in urban centers globally directly correlates with the rising generation of MSW, necessitating comprehensive collection, treatment, and disposal strategies. Economic policies promoting waste segregation at source and robust public awareness campaigns are key drivers for effective MSW management.

Industrial Waste is another substantial segment, driven by manufacturing, construction, and mining activities. The stringent regulations surrounding the disposal of hazardous industrial waste are a major catalyst for the growth of specialized industrial waste management services. Investments in advanced treatment facilities and compliance monitoring are crucial for this segment.

The Plastic Waste segment is experiencing unprecedented attention due to global environmental concerns. Market growth here is driven by innovations in recycling technologies, the development of biodegradable alternatives, and increasing legislative pressures to reduce single-use plastics. Extended Producer Responsibility (EPR) schemes are significantly impacting the plastic waste management landscape, pushing for higher collection and recycling rates.

E-waste is the fastest-growing waste stream globally, characterized by rapid technological obsolescence of electronic devices. The presence of valuable metals and hazardous substances in e-waste necessitates specialized collection and dismantling processes. Government initiatives for e-waste recycling and consumer awareness about proper disposal are key growth enablers.

Biomedical and Other Waste Types represent a critical niche segment, driven by the healthcare industry. The highly regulated nature of biomedical waste, requiring safe collection, sterilization, and disposal to prevent the spread of infectious diseases, ensures consistent demand for specialized services. Stringent healthcare waste management policies are paramount for this segment's growth.

In terms of disposal methods, Recycling is experiencing the most significant growth, driven by sustainability initiatives, circular economy mandates, and the economic value of recovered materials. Technological advancements in sorting and processing are improving the efficiency and viability of recycling operations.

Incineration, particularly waste-to-energy (WtE) technologies, is gaining traction as a method to reduce landfill volume and generate renewable energy. Supportive government policies and the need for energy security are key drivers for this segment, especially in regions with limited land availability for landfills.

Landfill remains a primary disposal method in many regions, especially for residual waste that cannot be recycled or incinerated. However, its dominance is gradually decreasing due to environmental concerns, land scarcity, and stricter regulations aimed at promoting waste diversion. Modern sanitary landfills with advanced leachate and gas management systems are becoming the norm.

Waste Management Sector Industry Product Developments

Product developments in the waste management sector are increasingly focused on enhancing efficiency, sustainability, and resource recovery. Innovations include advanced sorting machinery employing artificial intelligence and robotics for improved separation of recyclables. The development of novel biodegradable and compostable materials is gaining momentum to address the plastic waste crisis. Waste-to-energy technologies are evolving with more efficient combustion processes and improved emission controls. Smart bins equipped with sensors for real-time fill-level monitoring and optimized collection routes are transforming urban waste logistics. Furthermore, digital platforms for waste tracking, compliance reporting, and customer engagement are offering greater transparency and operational control, providing significant competitive advantages in a rapidly evolving market.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global Waste Management Sector Industry. The market is segmented by Waste Type, including Industrial Waste, Municipal Solid Waste (MSW), E-waste, Plastic Waste, and Biomedical and Other Waste Types. Each segment's unique generation drivers, regulatory considerations, and technological requirements are examined. The market is also analyzed by Disposal Methods, encompassing Landfill, Incineration, and Recycling. Growth projections, market sizes, and competitive dynamics within these segments are detailed, highlighting the evolving preferences towards sustainable disposal and resource recovery.

For Industrial Waste, the report details the challenges and opportunities in managing diverse hazardous and non-hazardous streams generated by manufacturing, construction, and other industrial activities. The Municipal Solid Waste segment focuses on the increasing volumes from urban centers and the demand for efficient collection, processing, and landfill management. The E-waste segment delves into the complexities of handling obsolete electronics, driven by rapid technological advancements and the presence of valuable or hazardous components. The Plastic Waste segment examines innovative recycling technologies and the impact of global anti-plastic campaigns on market dynamics. Finally, the Biomedical and Other Waste Types segment covers the critical need for safe and compliant disposal of healthcare and other specialized waste streams.

Key Drivers of Waste Management Sector Industry Growth

The Waste Management Sector Industry is propelled by several key drivers. Rising global populations and increasing urbanization lead to higher waste generation volumes. Stringent environmental regulations and government mandates for waste reduction, recycling, and diversion from landfills are a primary catalyst. Technological advancements in recycling, waste-to-energy, and digital waste management solutions are enhancing efficiency and opening new revenue streams. Growing corporate social responsibility (CSR) and consumer demand for sustainable practices are pushing businesses to adopt eco-friendly waste management strategies. The economic imperative to recover valuable resources from waste streams and the development of the circular economy further fuel industry growth.

Challenges in the Waste Management Sector Industry Sector

Despite robust growth, the Waste Management Sector Industry faces several challenges. Inadequate infrastructure, particularly in developing regions, can hinder efficient waste collection and processing. Fluctuations in commodity prices for recycled materials can impact the profitability of recycling operations. Stringent and evolving regulatory frameworks, while driving sustainability, can also increase compliance costs for businesses. Public perception and acceptance of certain disposal methods, like incineration, can pose hurdles. Moreover, the informal sector's involvement in waste collection and recycling in some regions can create complexities in formalizing the industry and ensuring safe practices.

Emerging Opportunities in Waste Management Sector Industry

Emerging opportunities in the Waste Management Sector Industry are abundant, driven by the global push towards sustainability. The expansion of the circular economy presents significant opportunities in resource recovery and upcycling of waste materials. Advancements in chemical recycling of plastics offer solutions for difficult-to-recycle plastics. The growing demand for waste-to-energy solutions, particularly in regions with limited landfill space, is a key growth area. The proliferation of smart city initiatives is creating demand for integrated and technology-driven waste management solutions. Furthermore, the increasing focus on producer responsibility and extended producer responsibility schemes opens avenues for innovative service models and partnerships.

Leading Players in the Waste Management Sector Industry Market

- Biffa Group

- Clean Harbors Inc

- Covanta Holding Corporation

- Veolia Environnement SA

- Waste Connections

- Remondis AG & Co Kg

- Suez Environment S A

- Daiseki Co Ltd

- Waste Management Inc

- Republic Services

- Averda

Key Developments in Waste Management Sector Industry Industry

- February 2021: Biffa Group announced the acquisition of Company Shop Group ('CSG'), the UK's leading and largest redistributor of surplus food and household products.

- October 2020: Waste Management completed its acquisition of all outstanding shares of Advanced Disposal, following the receipt of required regulatory approvals. The previously announced purchase price of USD 30.30 per share in cash represents a total enterprise value of USD 4.6 billion when including approximately USD 1.8 billion of Advanced Disposal's net debt.

Strategic Outlook for Waste Management Sector Industry Market

The strategic outlook for the Waste Management Sector Industry is overwhelmingly positive, driven by a global commitment to environmental stewardship and resource efficiency. Future growth will be catalyzed by continued innovation in recycling technologies, the expanding adoption of waste-to-energy solutions, and the widespread implementation of circular economy principles. Investments in digital transformation, including AI and IoT for optimized operations, will remain crucial. The increasing stringency of environmental regulations worldwide will further incentivize sustainable practices and create opportunities for market leaders who can offer comprehensive, compliant, and cost-effective waste management solutions. Strategic partnerships and consolidations through M&A will continue to shape the competitive landscape, enabling companies to expand their service portfolios and geographic reach, ultimately driving the sector towards a more sustainable and profitable future.

Waste Management Sector Industry Segmentation

-

1. Waste type

- 1.1. Industrial waste

- 1.2. Municipal solid waste

- 1.3. E-waste

- 1.4. Plastic waste

- 1.5. Biomedical and Other Waste Types

-

2. Disposal methods

- 2.1. Landfill

- 2.2. Incineration

- 2.3. Recycling

Waste Management Sector Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

- 4. Middle East

- 5. Latin America

Waste Management Sector Industry Regional Market Share

Geographic Coverage of Waste Management Sector Industry

Waste Management Sector Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Waste type

- 5.1.1. Industrial waste

- 5.1.2. Municipal solid waste

- 5.1.3. E-waste

- 5.1.4. Plastic waste

- 5.1.5. Biomedical and Other Waste Types

- 5.2. Market Analysis, Insights and Forecast - by Disposal methods

- 5.2.1. Landfill

- 5.2.2. Incineration

- 5.2.3. Recycling

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East

- 5.3.5. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Waste type

- 6. Global Waste Management Sector Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Waste type

- 6.1.1. Industrial waste

- 6.1.2. Municipal solid waste

- 6.1.3. E-waste

- 6.1.4. Plastic waste

- 6.1.5. Biomedical and Other Waste Types

- 6.2. Market Analysis, Insights and Forecast - by Disposal methods

- 6.2.1. Landfill

- 6.2.2. Incineration

- 6.2.3. Recycling

- 6.1. Market Analysis, Insights and Forecast - by Waste type

- 7. North America Waste Management Sector Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Waste type

- 7.1.1. Industrial waste

- 7.1.2. Municipal solid waste

- 7.1.3. E-waste

- 7.1.4. Plastic waste

- 7.1.5. Biomedical and Other Waste Types

- 7.2. Market Analysis, Insights and Forecast - by Disposal methods

- 7.2.1. Landfill

- 7.2.2. Incineration

- 7.2.3. Recycling

- 7.1. Market Analysis, Insights and Forecast - by Waste type

- 8. Europe Waste Management Sector Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Waste type

- 8.1.1. Industrial waste

- 8.1.2. Municipal solid waste

- 8.1.3. E-waste

- 8.1.4. Plastic waste

- 8.1.5. Biomedical and Other Waste Types

- 8.2. Market Analysis, Insights and Forecast - by Disposal methods

- 8.2.1. Landfill

- 8.2.2. Incineration

- 8.2.3. Recycling

- 8.1. Market Analysis, Insights and Forecast - by Waste type

- 9. Asia Pacific Waste Management Sector Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Waste type

- 9.1.1. Industrial waste

- 9.1.2. Municipal solid waste

- 9.1.3. E-waste

- 9.1.4. Plastic waste

- 9.1.5. Biomedical and Other Waste Types

- 9.2. Market Analysis, Insights and Forecast - by Disposal methods

- 9.2.1. Landfill

- 9.2.2. Incineration

- 9.2.3. Recycling

- 9.1. Market Analysis, Insights and Forecast - by Waste type

- 10. Middle East Waste Management Sector Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Waste type

- 10.1.1. Industrial waste

- 10.1.2. Municipal solid waste

- 10.1.3. E-waste

- 10.1.4. Plastic waste

- 10.1.5. Biomedical and Other Waste Types

- 10.2. Market Analysis, Insights and Forecast - by Disposal methods

- 10.2.1. Landfill

- 10.2.2. Incineration

- 10.2.3. Recycling

- 10.1. Market Analysis, Insights and Forecast - by Waste type

- 11. Latin America Waste Management Sector Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Waste type

- 11.1.1. Industrial waste

- 11.1.2. Municipal solid waste

- 11.1.3. E-waste

- 11.1.4. Plastic waste

- 11.1.5. Biomedical and Other Waste Types

- 11.2. Market Analysis, Insights and Forecast - by Disposal methods

- 11.2.1. Landfill

- 11.2.2. Incineration

- 11.2.3. Recycling

- 11.1. Market Analysis, Insights and Forecast - by Waste type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Biffa Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Clean Harbors Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Covanta Holding Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Veolia Environment SA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Waste Connections

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Remondis AG & Co Kg

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Suez Environment S A

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Daiseki Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Waste Management Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Republic Services

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Averda**List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Biffa Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Waste Management Sector Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Waste Management Sector Industry Revenue (billion), by Waste type 2025 & 2033

- Figure 3: North America Waste Management Sector Industry Revenue Share (%), by Waste type 2025 & 2033

- Figure 4: North America Waste Management Sector Industry Revenue (billion), by Disposal methods 2025 & 2033

- Figure 5: North America Waste Management Sector Industry Revenue Share (%), by Disposal methods 2025 & 2033

- Figure 6: North America Waste Management Sector Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Waste Management Sector Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Waste Management Sector Industry Revenue (billion), by Waste type 2025 & 2033

- Figure 9: Europe Waste Management Sector Industry Revenue Share (%), by Waste type 2025 & 2033

- Figure 10: Europe Waste Management Sector Industry Revenue (billion), by Disposal methods 2025 & 2033

- Figure 11: Europe Waste Management Sector Industry Revenue Share (%), by Disposal methods 2025 & 2033

- Figure 12: Europe Waste Management Sector Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Waste Management Sector Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Waste Management Sector Industry Revenue (billion), by Waste type 2025 & 2033

- Figure 15: Asia Pacific Waste Management Sector Industry Revenue Share (%), by Waste type 2025 & 2033

- Figure 16: Asia Pacific Waste Management Sector Industry Revenue (billion), by Disposal methods 2025 & 2033

- Figure 17: Asia Pacific Waste Management Sector Industry Revenue Share (%), by Disposal methods 2025 & 2033

- Figure 18: Asia Pacific Waste Management Sector Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Waste Management Sector Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East Waste Management Sector Industry Revenue (billion), by Waste type 2025 & 2033

- Figure 21: Middle East Waste Management Sector Industry Revenue Share (%), by Waste type 2025 & 2033

- Figure 22: Middle East Waste Management Sector Industry Revenue (billion), by Disposal methods 2025 & 2033

- Figure 23: Middle East Waste Management Sector Industry Revenue Share (%), by Disposal methods 2025 & 2033

- Figure 24: Middle East Waste Management Sector Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East Waste Management Sector Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Waste Management Sector Industry Revenue (billion), by Waste type 2025 & 2033

- Figure 27: Latin America Waste Management Sector Industry Revenue Share (%), by Waste type 2025 & 2033

- Figure 28: Latin America Waste Management Sector Industry Revenue (billion), by Disposal methods 2025 & 2033

- Figure 29: Latin America Waste Management Sector Industry Revenue Share (%), by Disposal methods 2025 & 2033

- Figure 30: Latin America Waste Management Sector Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Latin America Waste Management Sector Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Waste Management Sector Industry Revenue billion Forecast, by Waste type 2020 & 2033

- Table 2: Global Waste Management Sector Industry Revenue billion Forecast, by Disposal methods 2020 & 2033

- Table 3: Global Waste Management Sector Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Waste Management Sector Industry Revenue billion Forecast, by Waste type 2020 & 2033

- Table 5: Global Waste Management Sector Industry Revenue billion Forecast, by Disposal methods 2020 & 2033

- Table 6: Global Waste Management Sector Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Waste Management Sector Industry Revenue billion Forecast, by Waste type 2020 & 2033

- Table 10: Global Waste Management Sector Industry Revenue billion Forecast, by Disposal methods 2020 & 2033

- Table 11: Global Waste Management Sector Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Germany Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Russia Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Global Waste Management Sector Industry Revenue billion Forecast, by Waste type 2020 & 2033

- Table 18: Global Waste Management Sector Industry Revenue billion Forecast, by Disposal methods 2020 & 2033

- Table 19: Global Waste Management Sector Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: China Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Japan Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: India Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: South Korea Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of Asia Pacific Waste Management Sector Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Waste Management Sector Industry Revenue billion Forecast, by Waste type 2020 & 2033

- Table 26: Global Waste Management Sector Industry Revenue billion Forecast, by Disposal methods 2020 & 2033

- Table 27: Global Waste Management Sector Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Global Waste Management Sector Industry Revenue billion Forecast, by Waste type 2020 & 2033

- Table 29: Global Waste Management Sector Industry Revenue billion Forecast, by Disposal methods 2020 & 2033

- Table 30: Global Waste Management Sector Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Waste Management Sector Industry?

The projected CAGR is approximately 6.63%.

2. Which companies are prominent players in the Waste Management Sector Industry?

Key companies in the market include Biffa Group, Clean Harbors Inc, Covanta Holding Corporation, Veolia Environment SA, Waste Connections, Remondis AG & Co Kg, Suez Environment S A, Daiseki Co Ltd, Waste Management Inc, Republic Services, Averda**List Not Exhaustive.

3. What are the main segments of the Waste Management Sector Industry?

The market segments include Waste type, Disposal methods.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.58 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Spotlight on the Construction and Demolition waste management systems.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2021: Biffa group announced the acquisition of Company Shop Group ('CSG'), the UK's leading and largest redistributor of surplus food and household products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Waste Management Sector Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Waste Management Sector Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Waste Management Sector Industry?

To stay informed about further developments, trends, and reports in the Waste Management Sector Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence