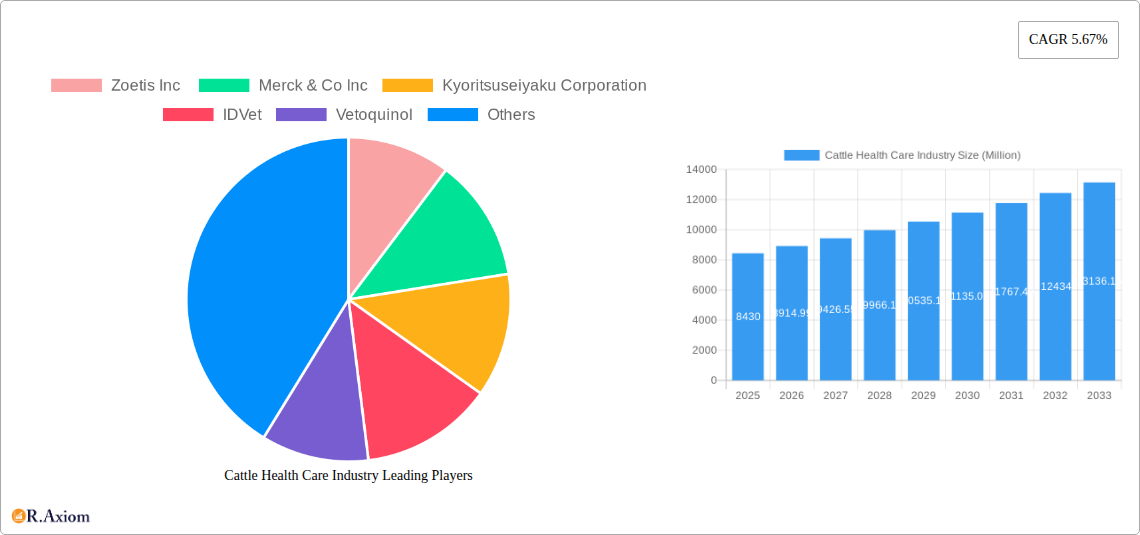

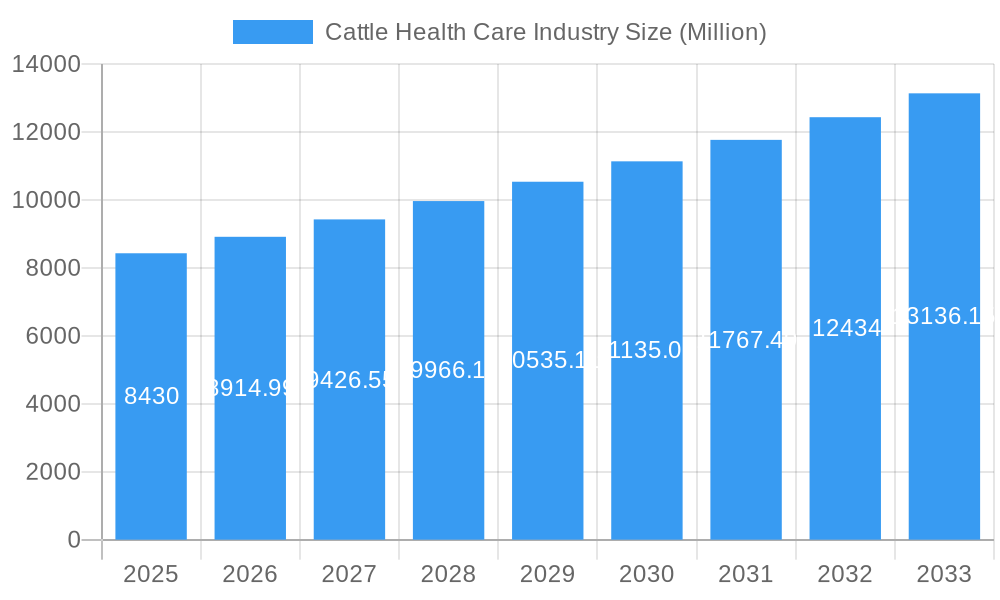

Key Insights

The global Cattle Health Care market is poised for robust expansion, projected to reach approximately USD 8.43 billion by 2025. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 5.67% during the forecast period of 2025-2033. The increasing global demand for animal protein, coupled with a growing awareness among livestock producers regarding the economic benefits of disease prevention and herd management, are primary growth catalysts. Advancements in veterinary diagnostics, such as sophisticated immunodiagnostic tests and molecular diagnostics, are enabling earlier and more accurate disease detection, leading to improved treatment outcomes and reduced losses. Furthermore, the development of novel vaccines and effective anti-infective therapies are crucial in combating prevalent cattle diseases, thereby bolstering market growth. The widespread adoption of medical feed additives for disease prevention and growth promotion also contributes significantly to the market's upward trajectory.

Cattle Health Care Industry Market Size (In Billion)

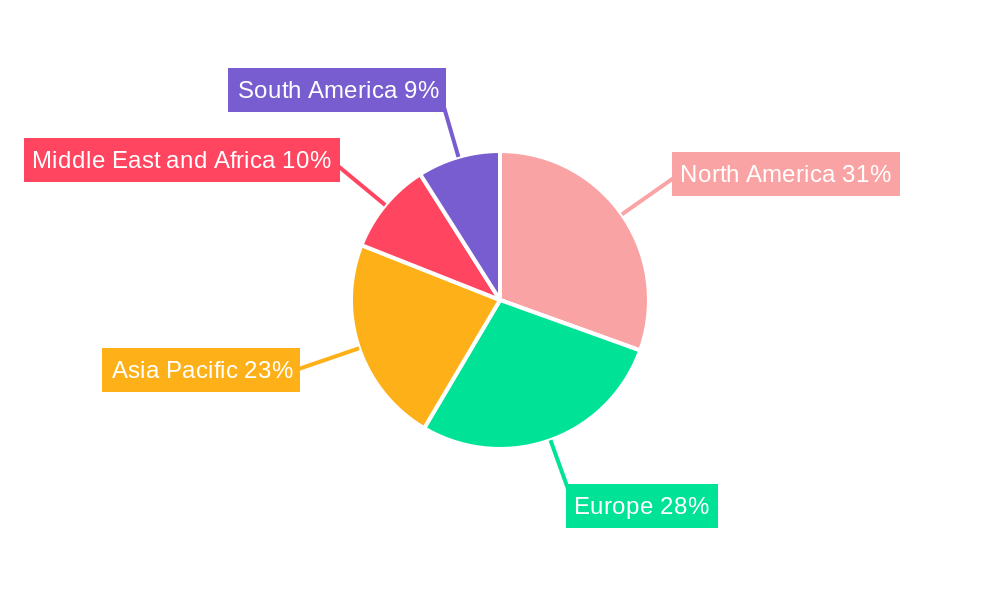

The market is segmented into two key areas: Product Type and Diagnostics. Within Product Type, Therapeutics, encompassing vaccines, parasiticides, anti-infectives, and medical feed additives, represent a substantial segment. The Diagnostics segment is experiencing rapid innovation, with immunodiagnostic tests and molecular diagnostics gaining prominence due to their speed and accuracy. Geographically, North America and Europe currently hold significant market shares, driven by advanced veterinary infrastructure and high adoption rates of modern cattle management practices. However, the Asia Pacific region, particularly China and India, is expected to exhibit the fastest growth, fueled by a burgeoning livestock industry and increasing investments in animal health. Key players like Zoetis Inc., Merck & Co. Inc., and Elanco Animal Health are actively investing in research and development to introduce innovative solutions, further shaping the competitive landscape and driving market evolution.

Cattle Health Care Industry Company Market Share

Cattle Health Care Industry Market Concentration & Innovation

The global cattle health care industry is characterized by a moderate to high level of market concentration, with a few dominant players holding substantial market share. Key companies such as Zoetis Inc., Merck & Co. Inc., Boehringer Ingelheim, and Elanco Animal Health are at the forefront, driving innovation and market dynamics. The market concentration is also influenced by a robust regulatory framework, particularly in developed economies, which dictates product approvals and manufacturing standards. Innovation in this sector is primarily fueled by the increasing demand for sustainable and efficient livestock farming, coupled with advancements in veterinary pharmaceuticals and diagnostics. Product substitutes, such as improved farm management practices and alternative feed sources, exist but are generally supplemented by dedicated health solutions. End-user trends highlight a growing preference for preventive health measures and precision livestock farming techniques, leading to increased adoption of advanced diagnostics and therapeutic solutions. Merger and acquisition (M&A) activities play a significant role in consolidating market share and acquiring innovative technologies. Notable M&A deals in recent years have focused on acquiring companies with expertise in novel drug delivery systems, vaccine technologies, and digital health platforms for cattle. For instance, strategic acquisitions of smaller biotech firms by larger corporations have been common, with deal values often reaching into the hundreds of millions of dollars, reflecting the perceived value and growth potential of specialized cattle health solutions. The overall market value is projected to reach approximately $XX Million by 2033, with M&A contributing to an estimated XX% of this growth through market consolidation and strategic expansion.

Cattle Health Care Industry Industry Trends & Insights

The global cattle health care industry is experiencing robust growth, driven by a confluence of factors that underscore the increasing importance of animal well-being and agricultural productivity. The Compound Annual Growth Rate (CAGR) for the industry is projected to be approximately XX% over the forecast period (2025–2033), reflecting sustained expansion. Market penetration is steadily increasing as adoption of advanced health management practices becomes more widespread across diverse geographical regions and farm sizes. Key growth drivers include the escalating global demand for protein, particularly beef and dairy, which necessitates improved herd health for efficient production. This demand is further amplified by a growing consumer awareness regarding food safety and the ethical treatment of animals, pushing producers to invest more in comprehensive cattle health solutions.

Technological disruptions are profoundly reshaping the industry. The integration of artificial intelligence (AI) and machine learning (ML) in diagnostics and data analytics allows for early disease detection and personalized treatment plans, significantly reducing economic losses from outbreaks. Wearable sensors and IoT devices are enabling real-time monitoring of individual animal health, facilitating proactive interventions. Advancements in biotechnology have led to the development of more effective vaccines and targeted antiparasitic treatments, offering improved efficacy and reduced resistance.

Consumer preferences are increasingly leaning towards products from animals raised under stringent health and welfare standards. This trend directly translates to increased demand for preventive care, sophisticated diagnostic tools, and high-quality therapeutic products. The emphasis on antibiotic stewardship also drives innovation towards non-antibiotic alternatives and precision medicine approaches.

The competitive dynamics within the cattle health care industry are characterized by intense innovation and strategic partnerships. Established players are continuously investing in research and development (R&D) to introduce novel products and expand their portfolios. Simultaneously, the rise of smaller, agile biotech firms specializing in niche areas like genomics and microbiome research presents a dynamic competitive landscape, often leading to strategic collaborations and acquisitions. The global market is projected to grow from an estimated $XX Million in the base year 2025 to over $XX Million by 2033, demonstrating significant market expansion potential.

Dominant Markets & Segments in Cattle Health Care Industry

The global cattle health care industry exhibits distinct dominance across various geographical regions and product segments, driven by a complex interplay of economic policies, infrastructure development, and regional health needs. North America and Europe currently represent the most dominant markets, characterized by highly developed agricultural sectors, strong regulatory oversight, and a significant emphasis on animal welfare and productivity. The economic policies in these regions often support research and development in animal health, coupled with substantial investments in advanced veterinary infrastructure, contributing to higher market penetration of sophisticated health solutions.

Within the Product Type segmentation, Therapeutics and Diagnostics are the two major pillars, each with its own set of influential sub-segments.

By Therapeutics:

- Vaccines: This segment holds a dominant position due to the continuous threat of infectious diseases in cattle populations. Economic policies promoting herd health management and disease prevention programs, especially in regions with large cattle populations like the United States and Brazil, significantly drive vaccine demand. Infrastructure development supporting widespread vaccination campaigns also plays a crucial role. The need to combat prevalent diseases such as Bovine Viral Diarrhea (BVD), Infectious Bovine Rhinotracheitis (IBR), and Foot-and-Mouth Disease (FMD) ensures a consistent market for effective vaccine solutions.

- Parasiticides: Parasitic infections represent a major economic drain on cattle farming, impacting growth rates, milk production, and overall herd health. Therefore, parasiticides are crucial. Government initiatives aimed at controlling parasitic outbreaks and improving animal productivity, alongside advancements in novel and more effective antiparasitic formulations, contribute to the segment's dominance. The development of resistance in parasites also spurs demand for new and improved products.

- Anti-infectives: While there is a global push towards reducing antibiotic use, anti-infectives remain critical for treating bacterial infections that can have severe economic consequences. Economic incentives for disease treatment and the ongoing need to manage prevalent bacterial diseases like mastitis and pneumonia ensure their continued importance. Regulatory frameworks focusing on judicious use and the development of newer, more targeted anti-infectives also shape this segment.

- Medical Feed Additives: These are vital for improving feed efficiency, gut health, and overall growth promotion. Economic policies focused on increasing agricultural output and reducing production costs, especially in intensive farming systems, drive the adoption of feed additives. The growing understanding of the gut microbiome's role in cattle health further bolsters this segment.

- Other Therapeutics: This category encompasses a range of products like anti-inflammatories, hormones, and nutritional supplements, which cater to specific health and production needs, contributing to the overall therapeutic market share.

By Diagnostics:

- Immunodiagnostic Tests: These are widely used for the rapid and cost-effective detection of various diseases. Economic policies promoting early disease detection and prevention, coupled with the availability of affordable and user-friendly diagnostic kits, make this a dominant segment. The demand for on-farm testing and rapid results fuels their widespread adoption across all cattle farming scales.

- Molecular Diagnostics: With advancements in genetic and genomic technologies, molecular diagnostics are gaining prominence for their high sensitivity and specificity in disease detection, strain identification, and herd profiling. Government funding for research in animal genomics and the increasing focus on biosecurity measures drive the growth of this segment.

- Diagnostic Imaging: While more prevalent in specialized veterinary clinics and research settings, diagnostic imaging (e.g., ultrasound, X-ray) plays a critical role in diagnosing complex conditions and injuries, contributing to the overall diagnostic market.

- Clinical Chemistry: Analysis of blood and other bodily fluids for various biochemical markers is essential for assessing organ function, metabolic status, and overall health, supporting therapeutic decisions.

- Other Diagnostics: This includes a variety of testing methods and equipment that complement the primary diagnostic categories.

The projected market value for the Cattle Health Care Industry is estimated to reach approximately $XX Million in 2025 and is expected to grow to over $XX Million by 2033, with significant contributions from both therapeutic and diagnostic segments.

Cattle Health Care Industry Product Developments

Product developments in the cattle health care industry are increasingly focused on precision, efficacy, and sustainability. Innovations are driven by advancements in biotechnology, leading to the creation of novel vaccines with enhanced immunogenicity and extended shelf life, such as those utilizing mRNA technology. The development of targeted antiparasitic treatments aims to combat resistance and minimize environmental impact. In diagnostics, the trend is towards point-of-care testing, miniaturized devices, and AI-powered analytical tools for faster, more accurate disease identification. For instance, the development of rapid diagnostic kits for common bovine diseases and advanced genomic testing services are providing veterinarians and farmers with actionable insights for proactive herd management. These developments offer competitive advantages by improving animal welfare, reducing economic losses, and contributing to more sustainable livestock production.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global cattle health care industry, segmented by Product Type.

By Therapeutics: The therapeutic segment encompasses vital solutions for preventing and treating cattle diseases.

- Vaccines: Projected to hold a significant market share due to their role in preventing widespread infectious diseases, with a market size of approximately $XX Million in 2025, growing to $XX Million by 2033.

- Parasiticides: Essential for controlling parasitic infections that impact productivity, with an estimated market of $XX Million in 2025, projected to reach $XX Million by 2033.

- Anti-infectives: Crucial for treating bacterial infections, with a market size of $XX Million in 2025, expected to grow to $XX Million by 2033.

- Medical Feed Additives: Key for improving gut health and growth promotion, with a market of $XX Million in 2025, projected to reach $XX Million by 2033.

- Other Therapeutics: A diverse category catering to specific needs, contributing a market of $XX Million in 2025, expected to reach $XX Million by 2033.

By Diagnostics: The diagnostic segment focuses on early disease detection and health monitoring.

- Immunodiagnostic Tests: Dominant due to their cost-effectiveness and speed, with a market size of $XX Million in 2025, growing to $XX Million by 2033.

- Molecular Diagnostics: Experiencing rapid growth due to advancements in genetic analysis, projected at $XX Million in 2025 and reaching $XX Million by 2033.

- Diagnostic Imaging: A specialized segment for complex diagnoses, with a market of $XX Million in 2025, expected to reach $XX Million by 2033.

- Clinical Chemistry: Important for metabolic and organ function assessment, with a market of $XX Million in 2025, growing to $XX Million by 2033.

- Other Diagnostics: Complementary testing methods, with a market of $XX Million in 2025, projected to reach $XX Million by 2033.

The overall market is anticipated to reach approximately $XX Million in 2025 and exceed $XX Million by 2033.

Key Drivers of Cattle Health Care Industry Growth

The growth of the cattle health care industry is propelled by several interconnected drivers. The escalating global demand for protein, particularly beef and dairy products, necessitates enhanced herd productivity and health management. Increasing awareness among consumers and regulators regarding animal welfare and food safety standards compels producers to invest more in preventive healthcare and advanced treatment solutions. Technological advancements, including AI-driven diagnostics, precision livestock farming tools, and innovative vaccine and therapeutic formulations, are significantly improving disease detection, treatment efficacy, and overall herd management. Government initiatives promoting sustainable agriculture and stricter biosecurity measures also contribute to market expansion by encouraging the adoption of advanced health solutions. Furthermore, the economic imperative to minimize losses from disease outbreaks and improve feed conversion ratios incentivizes investment in comprehensive cattle health management.

Challenges in the Cattle Health Care Industry Sector

Despite robust growth, the cattle health care industry faces several challenges. Stringent and evolving regulatory frameworks across different regions can create hurdles for product development and market entry, demanding significant investment in compliance and testing. The threat of antimicrobial resistance necessitates a shift towards alternative treatments and judicious antibiotic use, requiring substantial R&D investment in novel solutions. Supply chain disruptions, particularly those affecting the availability of raw materials and finished products, can impact market access and product availability. Furthermore, the high cost of advanced veterinary diagnostics and treatments can be a barrier for small-scale farmers, limiting market penetration in certain segments. Intense competition among established players and emerging biotech firms also puts pressure on pricing and necessitates continuous innovation to maintain market share.

Emerging Opportunities in Cattle Health Care Industry

The cattle health care industry is ripe with emerging opportunities driven by innovation and evolving market demands. The burgeoning field of microbiome research offers potential for developing novel gut health solutions and disease prevention strategies. The increasing adoption of digital health technologies, including AI-powered analytics and remote monitoring systems, presents significant opportunities for precision livestock farming and proactive herd management. Growing demand for organic and ethically sourced beef and dairy products is creating a niche for specialized health solutions that align with these production philosophies. Furthermore, the expansion of cattle farming in emerging economies, coupled with improving infrastructure and growing awareness of animal health best practices, presents substantial untapped market potential for both established and new entrants. The development of climate-resilient cattle breeds and associated health management strategies is also an emerging area of focus.

Leading Players in the Cattle Health Care Industry Market

- Zoetis Inc.

- Merck & Co Inc.

- Kyoritsuseiyaku Corporation

- IDVet

- Vetoquinol

- Qiagen

- Norbrook

- Boehringer Ingelheim

- Virbac

- Thermo Fisher Scientific

- Elanco Animal Health

- Idexx Laboratories

Key Developments in Cattle Health Care Industry Industry

- June 2022: Petco Health and Wellness Company Inc. launched a community-driven test concept designed to serve the health and wellness needs of pets and farm animals in small towns and rural communities. This initiative aims to increase accessibility to diagnostic tools and health information for a broader range of animal owners.

- April 2022: The United States-based synthetic biology companies Ginkgo Bioworks and Elanco launched a microbiome innovation company, BiomEdit, which will develop animal health products and services. This collaboration signifies a growing investment in harnessing the power of the microbiome for advanced animal health solutions, potentially leading to novel treatments and disease prevention strategies for cattle.

Strategic Outlook for Cattle Health Care Industry Market

The strategic outlook for the cattle health care industry remains highly positive, driven by the imperative to meet global protein demands sustainably and ethically. Key growth catalysts include the continued integration of digital technologies for precision farming, leading to enhanced efficiency and reduced waste. The development and adoption of innovative vaccines and non-antibiotic therapeutic alternatives will be critical in addressing antimicrobial resistance concerns and meeting evolving regulatory requirements. Strategic partnerships and acquisitions will continue to consolidate market share and accelerate the introduction of novel technologies. Furthermore, the increasing emphasis on animal welfare and food safety will fuel demand for advanced diagnostic tools and comprehensive health management programs. Emerging markets offer significant expansion opportunities as livestock industries mature and adopt modern health practices. The industry is poised for sustained growth through innovation and strategic alignment with global agricultural and health trends.

Cattle Health Care Industry Segmentation

-

1. Product Type

-

1.1. By Therapeutics

- 1.1.1. Vaccine

- 1.1.2. Parasiticide

- 1.1.3. Anti-infective

- 1.1.4. Medical Feed Additive

- 1.1.5. Other Therapeutics

-

1.2. By Diagnostics

- 1.2.1. Immunodiagnostic Test

- 1.2.2. Molecular Diagnostics

- 1.2.3. Diagnostic Imaging

- 1.2.4. Clinical Chemistry

- 1.2.5. Other Diagnostics

-

1.1. By Therapeutics

Cattle Health Care Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Cattle Health Care Industry Regional Market Share

Geographic Coverage of Cattle Health Care Industry

Cattle Health Care Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.67% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. By Therapeutics

- 5.1.1.1. Vaccine

- 5.1.1.2. Parasiticide

- 5.1.1.3. Anti-infective

- 5.1.1.4. Medical Feed Additive

- 5.1.1.5. Other Therapeutics

- 5.1.2. By Diagnostics

- 5.1.2.1. Immunodiagnostic Test

- 5.1.2.2. Molecular Diagnostics

- 5.1.2.3. Diagnostic Imaging

- 5.1.2.4. Clinical Chemistry

- 5.1.2.5. Other Diagnostics

- 5.1.1. By Therapeutics

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East and Africa

- 5.2.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Cattle Health Care Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. By Therapeutics

- 6.1.1.1. Vaccine

- 6.1.1.2. Parasiticide

- 6.1.1.3. Anti-infective

- 6.1.1.4. Medical Feed Additive

- 6.1.1.5. Other Therapeutics

- 6.1.2. By Diagnostics

- 6.1.2.1. Immunodiagnostic Test

- 6.1.2.2. Molecular Diagnostics

- 6.1.2.3. Diagnostic Imaging

- 6.1.2.4. Clinical Chemistry

- 6.1.2.5. Other Diagnostics

- 6.1.1. By Therapeutics

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Cattle Health Care Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. By Therapeutics

- 7.1.1.1. Vaccine

- 7.1.1.2. Parasiticide

- 7.1.1.3. Anti-infective

- 7.1.1.4. Medical Feed Additive

- 7.1.1.5. Other Therapeutics

- 7.1.2. By Diagnostics

- 7.1.2.1. Immunodiagnostic Test

- 7.1.2.2. Molecular Diagnostics

- 7.1.2.3. Diagnostic Imaging

- 7.1.2.4. Clinical Chemistry

- 7.1.2.5. Other Diagnostics

- 7.1.1. By Therapeutics

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Cattle Health Care Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. By Therapeutics

- 8.1.1.1. Vaccine

- 8.1.1.2. Parasiticide

- 8.1.1.3. Anti-infective

- 8.1.1.4. Medical Feed Additive

- 8.1.1.5. Other Therapeutics

- 8.1.2. By Diagnostics

- 8.1.2.1. Immunodiagnostic Test

- 8.1.2.2. Molecular Diagnostics

- 8.1.2.3. Diagnostic Imaging

- 8.1.2.4. Clinical Chemistry

- 8.1.2.5. Other Diagnostics

- 8.1.1. By Therapeutics

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Cattle Health Care Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. By Therapeutics

- 9.1.1.1. Vaccine

- 9.1.1.2. Parasiticide

- 9.1.1.3. Anti-infective

- 9.1.1.4. Medical Feed Additive

- 9.1.1.5. Other Therapeutics

- 9.1.2. By Diagnostics

- 9.1.2.1. Immunodiagnostic Test

- 9.1.2.2. Molecular Diagnostics

- 9.1.2.3. Diagnostic Imaging

- 9.1.2.4. Clinical Chemistry

- 9.1.2.5. Other Diagnostics

- 9.1.1. By Therapeutics

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Cattle Health Care Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. By Therapeutics

- 10.1.1.1. Vaccine

- 10.1.1.2. Parasiticide

- 10.1.1.3. Anti-infective

- 10.1.1.4. Medical Feed Additive

- 10.1.1.5. Other Therapeutics

- 10.1.2. By Diagnostics

- 10.1.2.1. Immunodiagnostic Test

- 10.1.2.2. Molecular Diagnostics

- 10.1.2.3. Diagnostic Imaging

- 10.1.2.4. Clinical Chemistry

- 10.1.2.5. Other Diagnostics

- 10.1.1. By Therapeutics

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Cattle Health Care Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. By Therapeutics

- 11.1.1.1. Vaccine

- 11.1.1.2. Parasiticide

- 11.1.1.3. Anti-infective

- 11.1.1.4. Medical Feed Additive

- 11.1.1.5. Other Therapeutics

- 11.1.2. By Diagnostics

- 11.1.2.1. Immunodiagnostic Test

- 11.1.2.2. Molecular Diagnostics

- 11.1.2.3. Diagnostic Imaging

- 11.1.2.4. Clinical Chemistry

- 11.1.2.5. Other Diagnostics

- 11.1.1. By Therapeutics

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Zoetis Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck & Co Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kyoritsuseiyaku Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 IDVet

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vetoquinol

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Qiagen

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Norbrook

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Boehringer Ingelheim

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Virbac

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Thermo Fisher Scientific

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Elanco Animal Health

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Idexx Laboratories

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Zoetis Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cattle Health Care Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Cattle Health Care Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Cattle Health Care Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America Cattle Health Care Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 5: North America Cattle Health Care Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Cattle Health Care Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Cattle Health Care Industry Revenue (Million), by Country 2025 & 2033

- Figure 8: North America Cattle Health Care Industry Volume (K Unit), by Country 2025 & 2033

- Figure 9: North America Cattle Health Care Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Cattle Health Care Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Europe Cattle Health Care Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 12: Europe Cattle Health Care Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 13: Europe Cattle Health Care Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: Europe Cattle Health Care Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 15: Europe Cattle Health Care Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: Europe Cattle Health Care Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: Europe Cattle Health Care Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Cattle Health Care Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Asia Pacific Cattle Health Care Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 20: Asia Pacific Cattle Health Care Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 21: Asia Pacific Cattle Health Care Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Asia Pacific Cattle Health Care Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 23: Asia Pacific Cattle Health Care Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Asia Pacific Cattle Health Care Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Asia Pacific Cattle Health Care Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cattle Health Care Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Middle East and Africa Cattle Health Care Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 28: Middle East and Africa Cattle Health Care Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 29: Middle East and Africa Cattle Health Care Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Middle East and Africa Cattle Health Care Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 31: Middle East and Africa Cattle Health Care Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Middle East and Africa Cattle Health Care Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Middle East and Africa Cattle Health Care Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Cattle Health Care Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: South America Cattle Health Care Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 36: South America Cattle Health Care Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 37: South America Cattle Health Care Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: South America Cattle Health Care Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 39: South America Cattle Health Care Industry Revenue (Million), by Country 2025 & 2033

- Figure 40: South America Cattle Health Care Industry Volume (K Unit), by Country 2025 & 2033

- Figure 41: South America Cattle Health Care Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Cattle Health Care Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cattle Health Care Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Cattle Health Care Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 3: Global Cattle Health Care Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Cattle Health Care Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 5: Global Cattle Health Care Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 6: Global Cattle Health Care Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 7: Global Cattle Health Care Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Global Cattle Health Care Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 9: United States Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: United States Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 11: Canada Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 13: Mexico Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Mexico Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Global Cattle Health Care Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 16: Global Cattle Health Care Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 17: Global Cattle Health Care Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Cattle Health Care Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Germany Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: France Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: France Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Italy Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Italy Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Spain Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Spain Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Global Cattle Health Care Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 32: Global Cattle Health Care Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 33: Global Cattle Health Care Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: Global Cattle Health Care Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 35: China Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: China Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Japan Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Japan Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: India Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: India Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Australia Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Australia Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: South Korea Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Rest of Asia Pacific Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Global Cattle Health Care Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 48: Global Cattle Health Care Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 49: Global Cattle Health Care Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Cattle Health Care Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: GCC Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: GCC Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: South Africa Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: South Africa Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Rest of Middle East and Africa Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: Rest of Middle East and Africa Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Global Cattle Health Care Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 58: Global Cattle Health Care Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 59: Global Cattle Health Care Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Cattle Health Care Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Brazil Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Brazil Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Argentina Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Argentina Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of South America Cattle Health Care Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Rest of South America Cattle Health Care Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cattle Health Care Industry?

The projected CAGR is approximately 5.67%.

2. Which companies are prominent players in the Cattle Health Care Industry?

Key companies in the market include Zoetis Inc , Merck & Co Inc, Kyoritsuseiyaku Corporation, IDVet, Vetoquinol, Qiagen, Norbrook, Boehringer Ingelheim, Virbac, Thermo Fisher Scientific, Elanco Animal Health, Idexx Laboratories.

3. What are the main segments of the Cattle Health Care Industry?

The market segments include Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.43 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing R&D Expenditure in the Cattle Health Sector; Rising Burden of Cattle Diseases; Increasing Initiatives by Government and Animal Welfare Associations.

6. What are the notable trends driving market growth?

Diagnostic Imaging are Expected to Hold Significant Share in the Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Infrastructure and Funding; Increasing Costs of Animal Testing and Veterinary Services.

8. Can you provide examples of recent developments in the market?

June 2022: Petco Health and Wellness Company Inc. launched a community-driven test concept designed to serve the health and wellness needs of pets and farm animals in small towns and rural communities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cattle Health Care Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cattle Health Care Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cattle Health Care Industry?

To stay informed about further developments, trends, and reports in the Cattle Health Care Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence