Key Insights

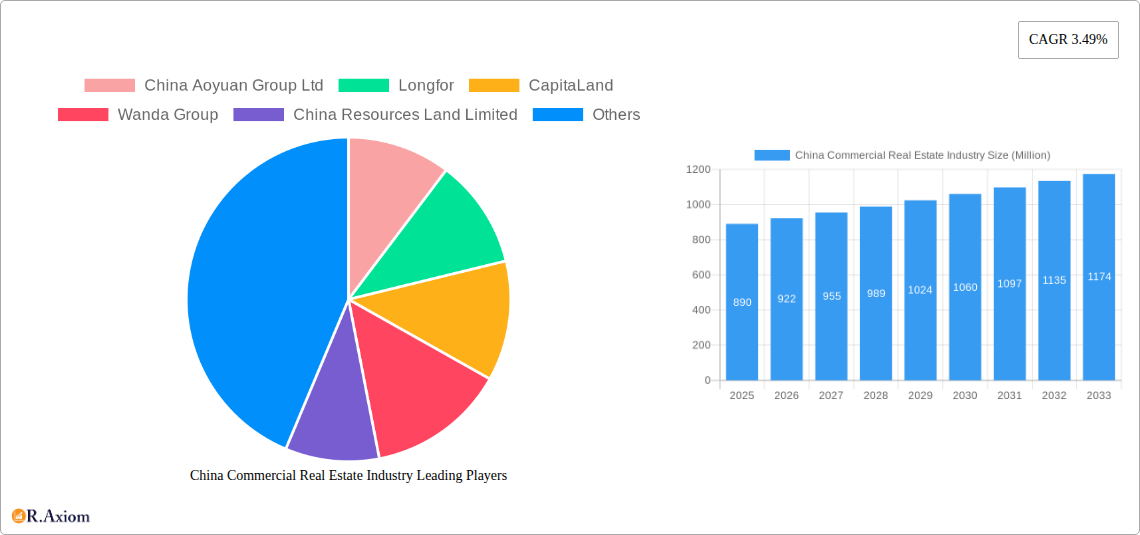

The China commercial real estate market, valued at $890 million in 2025, is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of 3.49% from 2025 to 2033. This growth is driven by several factors. Firstly, China's sustained economic expansion fuels demand for office spaces, particularly in major metropolitan areas like Beijing, Shanghai, and Guangzhou, accommodating the expanding technology and financial sectors. Secondly, the burgeoning e-commerce sector is driving significant demand for logistics and warehousing facilities, leading to considerable investment in industrial real estate. Furthermore, the increasing urbanization and a growing middle class are boosting the demand for retail spaces and multi-family residential properties. However, the market faces certain headwinds. Government regulations aimed at curbing excessive speculation and debt within the real estate sector could temper growth. Additionally, global economic uncertainties and potential shifts in consumer spending patterns pose potential risks. The market is segmented by property type, encompassing office, retail, industrial, logistics, multi-family, and hospitality sectors. Major players such as China Aoyuan Group Ltd, Longfor, CapitaLand, Wanda Group, and others, are actively shaping the market landscape through development and investment strategies.

The forecast for the next decade suggests a continued, albeit moderated, expansion of the China commercial real estate market. The projected CAGR indicates a consistent, albeit not explosive, increase in market value. The ongoing development of smart city initiatives and the government's focus on sustainable infrastructure will likely further influence investment patterns. Competition among developers remains intense, necessitating strategic partnerships and innovative approaches to development and management. The long-term outlook remains positive, contingent upon maintaining stable economic conditions and addressing potential regulatory challenges effectively. Further diversification within the commercial real estate portfolio, focusing on resilient sectors such as logistics and data centers, is likely to become a key strategy for developers seeking sustained growth.

China Commercial Real Estate Industry: 2019-2033 Market Analysis & Forecast Report

This comprehensive report provides an in-depth analysis of the China commercial real estate industry, covering the period from 2019 to 2033. It offers invaluable insights for investors, developers, policymakers, and industry stakeholders navigating the dynamic landscape of this crucial sector. With a focus on market concentration, emerging trends, key players, and future growth projections, this report is an essential resource for understanding and capitalizing on opportunities within the Chinese commercial real estate market. The report uses 2025 as the base year and provides forecasts until 2033. All monetary values are expressed in millions of US Dollars unless otherwise specified.

China Commercial Real Estate Industry Market Concentration & Innovation

This section analyzes the market concentration, innovation drivers, regulatory landscape, and competitive dynamics within the Chinese commercial real estate industry from 2019-2024. The study period (2019-2033) allows for a comprehensive view of historical trends and future projections.

The industry exhibits a moderate level of concentration, with a few large players commanding significant market share. For example, Wanda Group and China Resources Land Limited hold xx% and xx% market share respectively (estimated 2025), while smaller players compete intensely within specific segments. The industry is characterized by ongoing consolidation through mergers and acquisitions (M&A), with deal values reaching xx Million in 2024.

- Key Innovation Drivers: Technological advancements in smart building technologies, sustainable design, and property management software are driving innovation.

- Regulatory Framework: Government policies regarding land use, zoning regulations, and environmental standards significantly impact development and investment decisions.

- Product Substitutes: The rise of co-working spaces and flexible office solutions presents a competitive challenge to traditional office buildings.

- End-User Trends: Demand for sustainable and technologically advanced commercial spaces is increasing, driven by evolving business needs and environmental concerns.

- M&A Activities: Recent years have witnessed a surge in M&A activities, reflecting both strategic consolidation and opportunities arising from market shifts. For instance, CapitaLand’s acquisition of the Beijing Suning Life Plaza in 2023 highlights the ongoing investment activity within the sector.

China Commercial Real Estate Industry Industry Trends & Insights

The China commercial real estate market is characterized by several significant trends that shape its future trajectory. From 2019 to 2024, the market experienced a Compound Annual Growth Rate (CAGR) of xx%, driven primarily by robust economic growth and increasing urbanization. Market penetration rates for various segments show considerable variation, with office space consistently commanding a high share, followed by retail, industrial, and logistics. However, the market also faced challenges due to the tightening regulatory environment and fluctuating economic conditions impacting investment and development. Technological disruption, particularly in property management and building technology, is altering operational efficiency and customer experiences, leading to increased adoption of smart building solutions. Consumer preferences are shifting towards sustainable and technologically advanced spaces, prompting developers to incorporate these features in their projects. Competitive dynamics are characterized by increasing consolidation through mergers and acquisitions (M&A), driving market share concentration among major players. Future projections suggest continued growth, although at a moderated pace, as the market matures and adapts to evolving dynamics. The predicted CAGR for 2025-2033 is estimated to be xx%.

Dominant Markets & Segments in China Commercial Real Estate Industry

The Chinese commercial real estate market is geographically diverse, with certain regions exhibiting stronger performance than others. While data on precise regional dominance is not fully available, the coastal regions (Shanghai, Beijing, Guangdong) consistently attract significant investment and development due to their robust economies and well-developed infrastructure. Among the various property types, the office sector typically holds the largest market share, driven by continuous expansion of businesses and demand for high-quality workspaces. However, the relative dominance shifts slightly depending on current economic conditions and government policies.

- Key Drivers for Dominant Segments:

- Office: Strong demand from domestic and multinational companies, coupled with limited supply in prime locations.

- Retail: Growth of e-commerce and changing consumer behavior are impacting the retail segment. The shift towards experiential retail is reshaping the sector.

- Industrial & Logistics: Booming e-commerce and expanding manufacturing sectors fuel demand for industrial and logistics space.

- Multi-Family: Urbanization and rising disposable incomes are driving the growth of the multi-family segment.

- Hospitality: Tourism growth and increasing business travel contribute to the demand for hospitality properties.

China Commercial Real Estate Industry Product Developments

Recent product innovations in China's commercial real estate sector are heavily influenced by technological advancements and sustainability concerns. Smart building technologies, incorporating IoT and AI, are improving energy efficiency, security, and tenant experiences. Sustainable design principles are becoming increasingly integral, with developers focusing on energy-efficient materials, green building certifications, and reduced carbon footprints. These innovations are not only enhancing the value proposition for tenants but also contributing to a more sustainable real estate ecosystem. The market fit for these advancements is strong due to the growing awareness among both developers and tenants regarding environmental responsibility and operational efficiency.

Report Scope & Segmentation Analysis

This report segments the China commercial real estate market based on property type: Office, Retail, Industrial, Logistics, Multi-Family, and Hospitality. Each segment's growth projections, market sizes, and competitive dynamics are analyzed separately.

Office: The office segment is projected to maintain steady growth throughout the forecast period, driven by strong demand from both domestic and international businesses. Competition is fierce, with a focus on providing high-quality, technologically advanced workspaces. The market size in 2025 is estimated at xx Million.

Retail: The retail segment is undergoing transformation, with a focus on experiential retail and the integration of e-commerce. Market growth is expected to be moderate, with competition increasing among traditional retail spaces and new experiential retail formats. The market size in 2025 is estimated at xx Million.

Industrial & Logistics: The industrial and logistics segment is experiencing robust growth, driven by the expansion of e-commerce and manufacturing. Competition in this segment is focused on providing efficient and strategically located facilities. The market size in 2025 is estimated at xx Million.

Multi-Family: The multi-family segment is showing considerable growth due to urbanization and rising disposable incomes. Competition is increasingly focused on providing high-quality, amenity-rich residential spaces. The market size in 2025 is estimated at xx Million.

Hospitality: The hospitality segment is experiencing fluctuating growth depending on tourism trends and business travel. Competition is fierce, with a focus on providing unique and memorable guest experiences. The market size in 2025 is estimated at xx Million.

Key Drivers of China Commercial Real Estate Industry Growth

Several factors drive growth in China’s commercial real estate industry. Rapid urbanization and economic development create consistent demand for commercial spaces. Government initiatives promoting infrastructure development and investment in key sectors also fuel growth. Furthermore, technological advancements in smart building technologies and sustainable design attract investment and increase efficiency. The increasing adoption of e-commerce further boosts the demand for industrial and logistics spaces.

Challenges in the China Commercial Real Estate Industry Sector

The China commercial real estate industry faces several challenges. Stricter government regulations and environmental concerns impact development costs and timelines. Fluctuations in the national and global economy also affect investment decisions and market confidence. Supply chain disruptions occasionally delay projects. Intense competition among developers adds pressure on profitability. These factors contribute to the sector's inherent volatility.

Emerging Opportunities in China Commercial Real Estate Industry

Emerging opportunities exist in sustainable development, smart building technologies, and specialized commercial real estate niches. Government initiatives supporting green buildings and renewable energy present opportunities for developers to create environmentally friendly commercial spaces. The increasing adoption of technology in building management creates new opportunities for innovation. Finally, specialized niches, such as data centers and life science facilities, are attracting substantial investment.

Leading Players in the China Commercial Real Estate Industry Market

- China Aoyuan Group Ltd

- Longfor

- CapitaLand

- Wanda Group

- China Resources Land Limited

- Sun Hung Kai Properties Limited

- Henderson Land Development Company Limited

- Greenland Business Group

- Wharf Real Estate Investment Company Limited

- Prologis

- Seazen Holdings Co Ltd

- Powerlong Real Estate Holdings Limited

Key Developments in China Commercial Real Estate Industry Industry

April 2023: AIA invested US$1.3 billion in a Shanghai office-retail complex, while Ping An invested approximately US$7 billion in industrial and office assets in Shanghai and Beijing. This significant investment by insurers highlights the enduring attractiveness of the Chinese real estate market despite market downturn.

May 2023: CapitaLand Investment Private Fund acquired the Beijing Suning Life Plaza mixed-use complex from Suning for approximately USD 400 million, facilitated by Cushman & Wakefield's Greater China Capital Markets division. This transaction reflects the ongoing consolidation within the sector and the appetite for mixed-use developments.

Strategic Outlook for China Commercial Real Estate Industry Market

The future of China's commercial real estate market appears promising, driven by long-term urbanization trends, robust economic growth, and increasing demand for modern, sustainable commercial spaces. However, navigating the regulatory landscape and adapting to technological disruptions will be key to success. The market offers significant opportunities for investors and developers who can effectively integrate sustainability, technology, and innovative business models into their strategies. Continued growth is expected, albeit at a potentially moderated pace, as the sector matures and adjusts to evolving market dynamics.

China Commercial Real Estate Industry Segmentation

-

1. Type

- 1.1. Office

- 1.2. Retail

- 1.3. Industrial (Logistics)

- 1.4. Hospitality

China Commercial Real Estate Industry Segmentation By Geography

- 1. China

China Commercial Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.49% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Foreign Investments driving the market; Implementation of government policies driving the market

- 3.3. Market Restrains

- 3.3.1. Oversupply of commercial real estate; Increasing property prices affecting the growth of the market

- 3.4. Market Trends

- 3.4.1. Technology and Innovation Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Commercial Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Office

- 5.1.2. Retail

- 5.1.3. Industrial (Logistics)

- 5.1.4. Hospitality

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 China Aoyuan Group Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Longfor

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 CapitaLand

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Wanda Group

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 China Resources Land Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Sun Hung Kai Properties Limited

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Henderson Land Development Company Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Greenland Business Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Wharf Real Estate Investment Company Limited

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Prologis**List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Seazen Holdings Co Ltd

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Powerlong Real Estate Holdings Limited

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 China Aoyuan Group Ltd

List of Figures

- Figure 1: China Commercial Real Estate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Commercial Real Estate Industry Share (%) by Company 2024

List of Tables

- Table 1: China Commercial Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Commercial Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: China Commercial Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: China Commercial Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: China Commercial Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 6: China Commercial Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Commercial Real Estate Industry?

The projected CAGR is approximately 3.49%.

2. Which companies are prominent players in the China Commercial Real Estate Industry?

Key companies in the market include China Aoyuan Group Ltd, Longfor, CapitaLand, Wanda Group, China Resources Land Limited, Sun Hung Kai Properties Limited, Henderson Land Development Company Limited, Greenland Business Group, Wharf Real Estate Investment Company Limited, Prologis**List Not Exhaustive, Seazen Holdings Co Ltd, Powerlong Real Estate Holdings Limited.

3. What are the main segments of the China Commercial Real Estate Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.89 Million as of 2022.

5. What are some drivers contributing to market growth?

Foreign Investments driving the market; Implementation of government policies driving the market.

6. What are the notable trends driving market growth?

Technology and Innovation Driving the Market.

7. Are there any restraints impacting market growth?

Oversupply of commercial real estate; Increasing property prices affecting the growth of the market.

8. Can you provide examples of recent developments in the market?

May 2023: The Beijing Suning Life Plaza mixed-use complex was recently purchased from Suning for about USD 400 million by CapitaLand Investment Private Fund with the help of Cushman & Wakefield's Greater China Capital Markets division.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Commercial Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Commercial Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Commercial Real Estate Industry?

To stay informed about further developments, trends, and reports in the China Commercial Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence