Key Insights

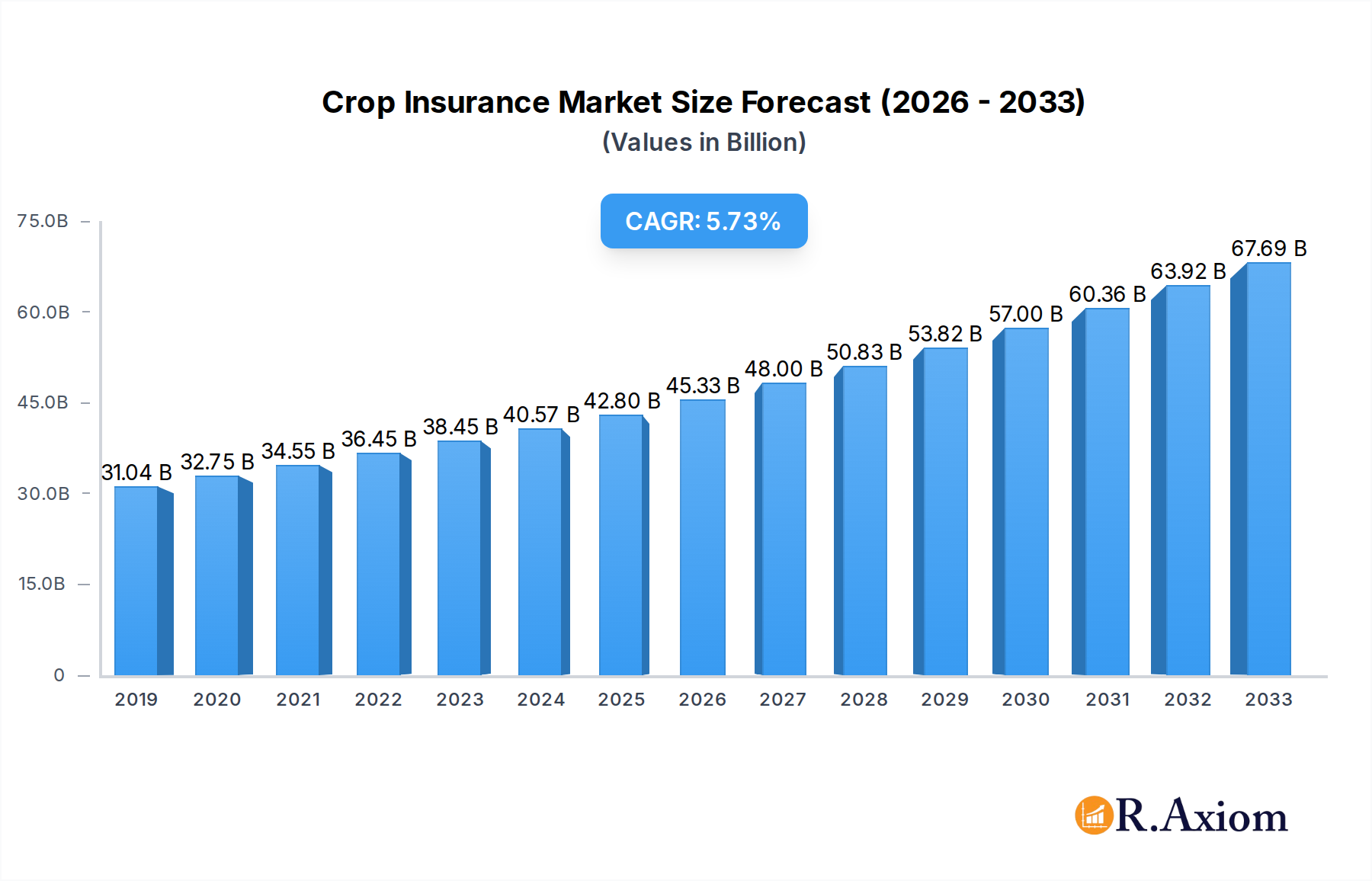

The global Crop Insurance market is experiencing significant growth, driven by an escalating need to safeguard agricultural investments against a backdrop of increasing climate volatility and geopolitical uncertainties impacting food supply chains. In 2025, the market is valued at USD 42.8 billion, underscoring its pivotal role in ensuring agricultural resilience and food security worldwide. This robust growth trajectory is projected to continue at a compelling Compound Annual Growth Rate (CAGR) of 5.9% from 2025 to 2033. A primary catalyst for this expansion is the intensifying impact of climate change, which manifests in more frequent and severe weather events such as prolonged droughts, devastating floods, and unpredictable frosts, posing existential threats to crop yields. Furthermore, strong governmental support, often in the form of premium subsidies and policy frameworks aimed at promoting farmer welfare and national food self-sufficiency, significantly incentivizes the adoption of crop insurance. The rising cost of agricultural inputs, including seeds, fertilizers, and energy, further compels farmers to mitigate financial risks through comprehensive insurance coverage, safeguarding their livelihoods.

Crop Insurance Market Size (In Billion)

Several transformative trends are shaping the crop insurance landscape. The accelerated adoption of advanced agricultural technologies, including satellite imagery, artificial intelligence (AI), and the Internet of Things (IoT), is revolutionizing risk assessment, enabling more precise underwriting and faster claims processing, particularly fostering the rise of parametric insurance solutions. There is also a noticeable industry shift towards customized insurance products designed to cater to specialty crops, diverse farming practices, and the unique climatic nuances of specific regions. Digitalization is streamlining policy management, enhancing accessibility, and improving the overall efficiency of insurance distribution. However, the market does contend with certain challenges, including the perceived high cost of premiums, particularly for smallholder farmers in developing regions, and a persistent need for greater farmer education regarding the long-term benefits and operational aspects of insurance. Despite these complexities, the market remains dynamic, segmented by application into crucial categories like Multi-Peril Crop Insurance (MPCI) and Crop Hail, and by type into offerings such as Crop Yield Insurance, Crop Price Insurance, and Crop Revenue Insurance, providing tailored protection solutions. Leading global and regional players, including PICC, Zurich, Chubb, American Financial Group, and Agriculture Insurance Company of India, are at the forefront of innovation, continually expanding and refining their offerings to meet the evolving demands of the global agricultural sector across key regions like North America, Asia Pacific, and Europe.

Crop Insurance Company Market Share

This comprehensive report offers an unparalleled deep dive into the Global Crop Insurance Market, providing crucial insights for industry stakeholders, investors, and policymakers navigating the evolving landscape of agricultural risk management. Spanning the Study Period 2019–2033, with a Base Year of 2025 and an Estimated Year of 2025, this analysis meticulously forecasts market trajectories through the Forecast Period 2025–2033 and examines historical trends from 2019–2024. Leveraging high-traffic keywords such as Crop Insurance Market, Agricultural Risk Management, MPCI, Crop Hail, Crop Yield Insurance, Crop Price Insurance, Crop Revenue Insurance, Agricultural Insurance Companies, Global Crop Insurance, Farm Income Protection, Sustainable Agriculture, Climate Change Impact, Digital Agriculture, and Agri-tech, this report is designed to enhance search visibility and deliver actionable intelligence on one of the most vital sectors protecting global food security. All monetary values are presented in billion.

Crop Insurance Market Concentration & Innovation

The global Crop Insurance Market is characterized by a significant degree of concentration, with a handful of major players holding substantial market shares, driving both competition and innovation. Companies like PICC, Zurich, Chubb, QBE, China United Property Insurance, and Agriculture Insurance Company of India command a substantial portion of the market, influencing pricing strategies and product development. For instance, PICC alone commands an estimated market share valued at xx billion, reflecting its dominance in key agricultural regions. This concentration, however, fuels intense innovation as firms strive to differentiate their offerings. Innovation drivers include the integration of advanced technologies such as satellite imagery, drones, AI-powered predictive analytics, and blockchain for claims processing and fraud detection, enhancing the efficiency and accuracy of crop insurance products.

Regulatory frameworks play a pivotal role in shaping market dynamics, often acting as both a catalyst for growth and a barrier to entry. Government subsidy programs, such as those in the United States and India, are critical in encouraging farmer participation, making insurance more accessible and affordable. However, evolving regulations concerning data privacy, climate risk disclosure, and actuarial standards require constant adaptation from insurers. Product substitutes, including self-insurance, forward contracts, and commodity hedging, exert competitive pressure, compelling insurers to offer more comprehensive and flexible solutions. End-user trends indicate a growing demand for customized policies, especially those covering specific climate risks or offering parametric triggers. Furthermore, M&A activities are a notable feature of the market, with larger entities acquiring smaller, specialized agri-tech firms or regional insurers to expand their geographical reach and technological capabilities. For example, xx billion worth of M&A deals were observed between 2019-2024, signaling consolidation and strategic partnerships aimed at strengthening market positions and fostering collaborative innovation.

Crop Insurance Industry Trends & Insights

The Crop Insurance Industry is experiencing profound transformations driven by a confluence of global trends, technological disruptions, and evolving stakeholder preferences. A primary market growth driver is the escalating frequency and intensity of extreme weather events attributed to climate change, necessitating robust agricultural risk management solutions. Farmers globally are increasingly vulnerable to droughts, floods, hailstorms, and pests, leading to greater adoption of crop insurance to safeguard farm income. Simultaneously, the burgeoning global population and rising demand for food exert pressure on agricultural productivity, making crop yield stability paramount. Governments worldwide are responding with supportive policies, including subsidies and mandatory insurance schemes, which have demonstrably boosted market penetration, reaching an estimated xx% in key agricultural economies. These governmental interventions, often driven by food security concerns, are projected to contribute to a market CAGR of xx% during the forecast period.

Technological disruptions are reshaping every facet of the crop insurance value chain. The advent of precision agriculture technologies, remote sensing via satellites and drones, and advanced data analytics platforms allows for more accurate risk assessment, personalized policy creation, and efficient claims processing. Digital agriculture tools are enabling real-time monitoring of crop health, weather patterns, and soil conditions, transforming traditional underwriting and loss adjustment processes. This digital transformation reduces operational costs for insurers and provides farmers with faster, more transparent services. Consumer preferences are shifting towards more flexible, data-driven, and transparent insurance products. There's a growing demand for parametric insurance, where payouts are triggered automatically based on predefined thresholds (e.g., rainfall deviation) rather than traditional damage assessment, offering quicker claims settlement. Farmers also increasingly seek comprehensive coverage that extends beyond just yield loss to include price volatility and revenue protection. The competitive dynamics are intensifying, with traditional insurance giants like PICC, Zurich, and Agriculture Insurance Company of India investing heavily in agri-tech startups and digital capabilities. Emerging players, often tech-centric, are entering the market, leveraging innovative platforms to offer niche or highly specialized products. This competitive environment fosters continuous product innovation, pushing the boundaries of what crop insurance can offer farmers in a rapidly changing agricultural landscape. The interplay of these factors suggests a vibrant and dynamic industry poised for significant expansion, with market penetration rates anticipated to increase by xx% over the forecast period as awareness and accessibility improve.

Dominant Markets & Segments in Crop Insurance

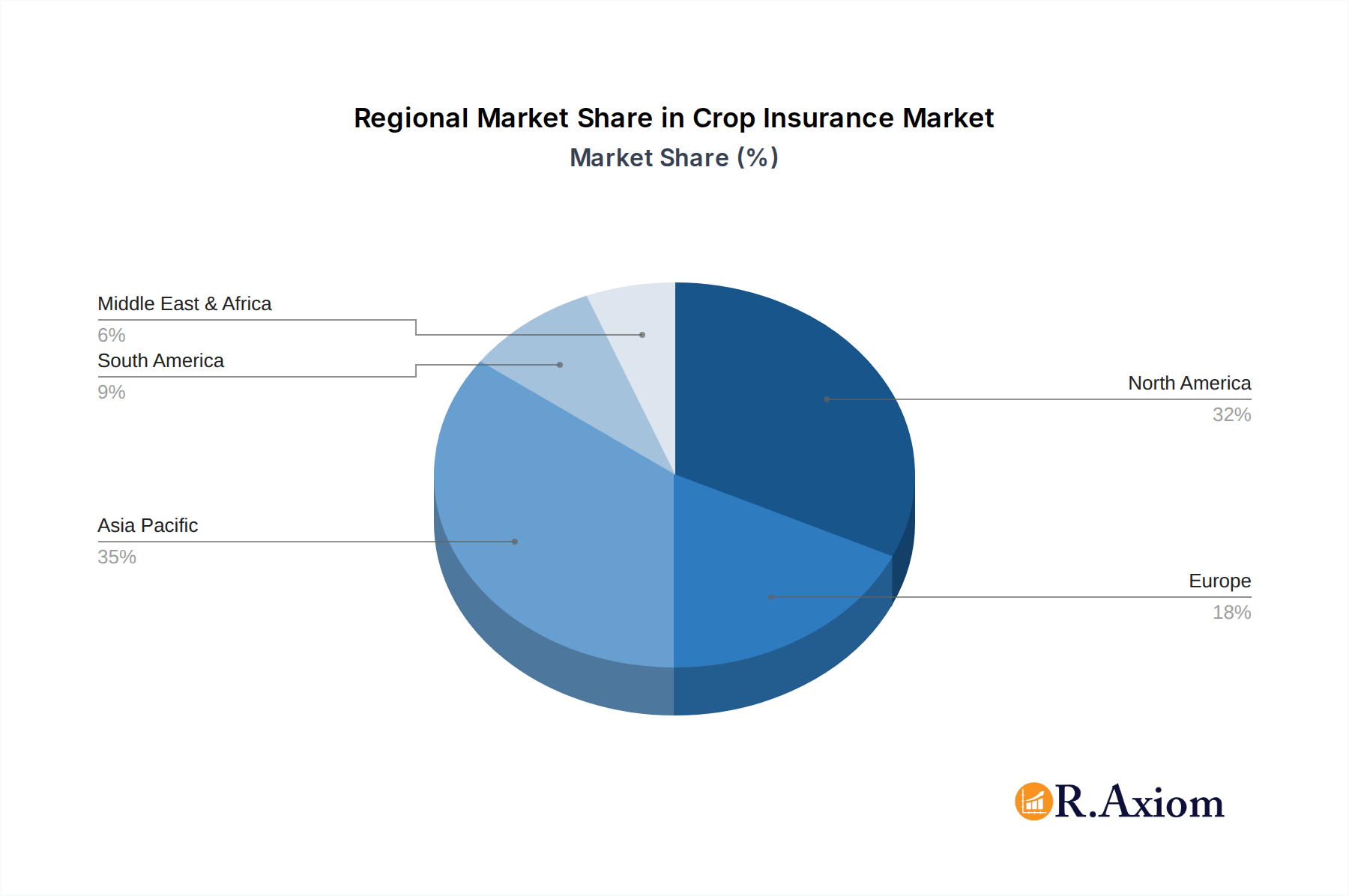

The Crop Insurance Market exhibits distinct regional and segmental dominance, driven by varied agricultural practices, economic policies, and risk exposures. Currently, North America and Asia-Pacific stand out as the leading regions. North America, particularly the United States, holds a dominant position, primarily due to well-established federal crop insurance programs and a high degree of agricultural modernization. Asia-Pacific, led by China and India, represents a burgeoning market, propelled by a vast agricultural base and increasing government support.

Within the application segments, Multi-Peril Crop Insurance (MPCI) is the undisputed leader, representing the largest share of the market.

- MPCI Dominance Drivers:

- Comprehensive Coverage: MPCI offers protection against a wide array of natural perils, including drought, excessive moisture, hail, frost, and pests, making it a holistic risk management tool for farmers.

- Government Subsidies: Significant government subsidies in key agricultural nations make MPCI policies more affordable and attractive to a broad base of farmers. For example, in the U.S., federal programs cover a substantial portion of premium costs.

- Risk Aversion: Growing awareness among large-scale commercial farmers regarding the financial impact of climate variability drives the adoption of comprehensive coverage.

- Policy Evolution: Continuous refinement and expansion of MPCI policies to include new perils and coverage options (e.g., prevented planting, replanting costs) enhance their appeal.

- Integration with Credit: MPCI often serves as a prerequisite for agricultural loans, embedding it within the financial ecosystem of farming.

The MPCI segment is projected to achieve a market size of xx billion by 2033, underscoring its pivotal role. Crop Hail insurance, while crucial for specific localized risks, remains a niche segment compared to the broader coverage of MPCI.

In terms of type segments, Crop Yield Insurance holds significant sway, often forming the core of comprehensive policies.

- Crop Yield Insurance Drivers:

- Direct Impact on Income: Farmers primarily depend on yield for their income, making protection against yield losses a fundamental concern.

- Simplicity and Clarity: The concept of insuring against a shortfall in harvested bushels or tons is straightforward and easily understood by farmers.

- Established Methodologies: Well-developed actuarial methods and historical yield data allow for accurate risk assessment and pricing.

- Alignment with Basic Farm Operations: It directly addresses the most immediate and tangible risk faced by crop producers—the actual quantity produced.

Crop Revenue Insurance, which combines yield protection with price protection, is rapidly gaining traction. This segment addresses both production risk and market price volatility, offering a more complete financial safety net for farmers. The increasing volatility in commodity markets makes Crop Revenue Insurance particularly appealing, as it provides a guarantee of a certain level of income per acre, even if yields are good but prices plummet. This segment is expected to reach a market value of xx billion by 2033, driven by a desire for more robust financial protection against market fluctuations. Crop Price Insurance, while less common as a standalone product, is typically integrated into Crop Revenue Insurance or other sophisticated risk management tools.

Crop Insurance Product Developments

The Crop Insurance market is witnessing a wave of innovations, transforming how agricultural risks are managed. Key product developments center around integrating cutting-edge technology to enhance accuracy and efficiency. Parametric insurance, for instance, is gaining traction, offering rapid payouts based on predefined weather indices (e.g., rainfall, temperature) rather than actual field damage, significantly reducing claims processing time. Digital platforms are becoming standard, enabling farmers to purchase, manage, and file claims remotely via mobile applications, improving accessibility and user experience. Furthermore, insurers are developing products that leverage precision agriculture data, incorporating insights from satellite imagery, drone surveillance, and IoT sensors to create hyper-localized, customized policies that better fit individual farm needs. This technological integration offers competitive advantages by reducing administrative costs, minimizing fraud, and providing tailored coverage that aligns perfectly with modern farming practices and evolving climate risks, ultimately enhancing market fit and farmer satisfaction.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the Crop Insurance Market, segmented comprehensively to offer granular insights into its dynamic landscape. The market is segmented by Application into Multi-Peril Crop Insurance (MPCI) and Crop Hail. MPCI, the most widely adopted segment, covers a broad spectrum of natural disasters and is projected to reach a market size of xx billion by 2033, showcasing robust growth driven by government support and increasing climate variability. The Crop Hail segment, while more specialized, addresses specific damage from hail and wind, maintaining a steady presence with unique competitive dynamics among regional players.

Further segmentation by Type includes Crop Yield Insurance, Crop Price Insurance, and Crop Revenue Insurance. Crop Yield Insurance, focusing on protecting against yield shortfalls, remains a foundational product, expected to grow to xx billion, largely due to its direct impact on farm output. Crop Price Insurance, while often integrated into broader offerings, addresses the volatility of commodity prices, securing farmers against market fluctuations. The Crop Revenue Insurance segment, which combines yield and price protection, is rapidly expanding, projected to be valued at xx billion by 2033, as farmers increasingly seek comprehensive income stability in an unpredictable market environment. Each segment presents distinct growth projections, market sizes, and competitive landscapes, detailed extensively within the report.

Key Drivers of Crop Insurance Growth

The growth of the Crop Insurance sector is underpinned by several powerful drivers. Firstly, technological advancements are revolutionizing risk assessment and claims processing. The integration of satellite imagery, drone technology, AI-driven analytics, and blockchain enhances accuracy, reduces fraud, and expedifies payouts, making insurance more attractive and efficient for farmers. Secondly, economic factors such as the increasing commercialization of agriculture and the rising value of agricultural output compel farmers to protect their investments. The global population growth further fuels demand for stable food production, thereby indirectly supporting the insurance sector. Thirdly, regulatory and policy support from governments worldwide is crucial. Subsidies, premium support, and mandatory insurance programs, particularly in large agricultural economies, significantly reduce the financial burden on farmers and boost adoption rates. For example, government-backed programs have led to a substantial increase in insured acreage, creating a market valued at xx billion. Lastly, heightened awareness of climate change impacts and increased frequency of extreme weather events (e.g., droughts, floods, temperature extremes) have dramatically elevated farmers' perception of risk, driving them towards comprehensive insurance solutions for income stability and resilience.

Challenges in the Crop Insurance Sector

Despite robust growth, the Crop Insurance sector faces significant barriers and restraints. Regulatory hurdles vary widely across regions, leading to complex compliance requirements and inconsistent policy structures, which can impede market expansion and product standardization. Supply chain issues, particularly data collection and validation in remote agricultural areas, present substantial operational challenges for insurers. Accurate historical yield data and real-time climate information are crucial for effective risk modeling, yet often lacking in developing markets. Competitive pressures from both traditional insurers and emerging agri-tech startups create pricing challenges and demand continuous innovation, impacting profit margins. Furthermore, the inherent risk of moral hazard and adverse selection can lead to higher claim rates and financial instability for insurers. For example, a severe, widespread catastrophic event could result in claims totaling xx billion, significantly straining insurer reserves. Limited farmer awareness, especially among smallholder farmers in developing economies, coupled with affordability concerns even with subsidies, also restricts market penetration. These factors collectively constrain the sector's potential and necessitate strategic responses from industry players and policymakers.

Emerging Opportunities in Crop Insurance

The Crop Insurance sector is ripe with emerging opportunities, driven by technological advancements and evolving market dynamics. A significant opportunity lies in the expansion into underserved markets, particularly in developing economies where smallholder farmers often lack access to formal insurance. Micro-insurance products, tailored for these segments, present a vast untapped potential. The proliferation of parametric insurance offers a growth pathway, as it provides rapid, objective payouts based on predefined triggers (e.g., rainfall, temperature) rather than traditional damage assessment, appealing to farmers seeking speed and transparency. Leveraging blockchain technology for claims processing and smart contracts can significantly enhance transparency, reduce administrative costs, and minimize fraud, fostering greater trust among stakeholders. Furthermore, integrating crop insurance with broader sustainable agriculture initiatives and climate resilience programs can create new product lines that incentivize environmentally friendly practices. As climate change impacts intensify, opportunities for specialized coverage against specific perils like prolonged heatwaves or new pest outbreaks will also emerge, catering to evolving farmer needs and preferences.

Leading Players in the Crop Insurance Market

- PICC

- Zurich

- Chubb

- QBE

- China United Property Insurance

- American Financial Group

- Prudential

- XL Catlin

- Everest Re Group

- Endurance Specialty

- CUNA Mutual

- Agriculture Insurance Company of India

- Tokio Marine

- CGB Diversified Services

- Farmers Mutual Hail

- Archer Daniels Midland

- New India Assurance

- ICICI Lombard

Key Developments in Crop Insurance Industry

- 2024 Q1: Zurich announced a strategic investment of xx billion in a leading agri-tech startup specializing in AI-driven crop health monitoring, aiming to enhance its predictive analytics capabilities for risk assessment.

- 2023 Q3: PICC launched a new suite of parametric drought insurance products across several key agricultural provinces, utilizing satellite-based rainfall data to offer quicker, more transparent claims processing. This significantly expanded its product portfolio to address climate volatility more effectively.

- 2023 Q2: A consortium including Chubb, QBE, and Everest Re Group initiated a pilot program to utilize blockchain technology for streamlining crop insurance claims in specific regions, targeting a reduction in processing times by xx% and enhancing transparency.

- 2022 Q4: Agriculture Insurance Company of India expanded its micro-insurance offerings to cover an additional xx million smallholder farmers, focusing on simplified enrollment and claims procedures to improve financial inclusion in rural areas.

- 2022 Q1: Farmers Mutual Hail partnered with a major weather data provider to integrate hyper-local weather forecasting into its crop hail insurance models, allowing for more precise risk mapping and personalized premium adjustments.

- 2021 Q3: ICICI Lombard introduced a new crop revenue insurance product that incorporates both yield protection and market price hedging, responding to increasing farmer demand for comprehensive income stability against market fluctuations.

Strategic Outlook for Crop Insurance Market

The Crop Insurance Market is poised for significant and sustained growth, driven by a powerful synergy of escalating climate risks, technological innovation, and proactive government support. The strategic outlook points towards a future where data-driven, highly customizable insurance products will become the norm, moving beyond traditional indemnity models to embrace parametric and revenue-based solutions. Continued investment in agri-tech, particularly in AI, remote sensing, and blockchain, will act as a primary catalyst, enhancing operational efficiency and expanding market reach into underserved agricultural regions. Governments will remain pivotal, with policies evolving to balance farmer protection, fiscal sustainability, and climate resilience objectives, ensuring the market's stability and fostering broader adoption. The overall market potential is immense, with the Global Crop Insurance Market projected to reach a valuation of xx billion by 2033, characterized by increased innovation, deeper market penetration, and a robust framework for managing the multifaceted risks facing global agriculture. This forward trajectory signifies a resilient and adaptive industry, crucial for securing food systems worldwide.

Crop Insurance Segmentation

-

1. Application

- 1.1. MPCI

- 1.2. Crop Hail

-

2. Type

- 2.1. Crop Yield Insurance

- 2.2. Crop Price Insurance

- 2.3. Crop Revenue Insurance

Crop Insurance Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Crop Insurance Regional Market Share

Geographic Coverage of Crop Insurance

Crop Insurance REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. MPCI

- 5.1.2. Crop Hail

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Crop Yield Insurance

- 5.2.2. Crop Price Insurance

- 5.2.3. Crop Revenue Insurance

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Crop Insurance Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. MPCI

- 6.1.2. Crop Hail

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Crop Yield Insurance

- 6.2.2. Crop Price Insurance

- 6.2.3. Crop Revenue Insurance

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Crop Insurance Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. MPCI

- 7.1.2. Crop Hail

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Crop Yield Insurance

- 7.2.2. Crop Price Insurance

- 7.2.3. Crop Revenue Insurance

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Crop Insurance Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. MPCI

- 8.1.2. Crop Hail

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Crop Yield Insurance

- 8.2.2. Crop Price Insurance

- 8.2.3. Crop Revenue Insurance

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Crop Insurance Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. MPCI

- 9.1.2. Crop Hail

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Crop Yield Insurance

- 9.2.2. Crop Price Insurance

- 9.2.3. Crop Revenue Insurance

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Crop Insurance Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. MPCI

- 10.1.2. Crop Hail

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Crop Yield Insurance

- 10.2.2. Crop Price Insurance

- 10.2.3. Crop Revenue Insurance

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Crop Insurance Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. MPCI

- 11.1.2. Crop Hail

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Crop Yield Insurance

- 11.2.2. Crop Price Insurance

- 11.2.3. Crop Revenue Insurance

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 PICC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Zurich

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Chubb

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 QBE

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 China United Property Insurance

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 American Financial Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Prudential

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 XL Catlin

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Everest Re Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Endurance Specialty

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 CUNA Mutual

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Agriculture Insurance Company of India

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Tokio Marine

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 CGB Diversified Services

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Farmers Mutual Hail

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Archer Daniels Midland

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 New India Assurance

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 ICICI Lombard

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 PICC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Crop Insurance Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Crop Insurance Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Crop Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Crop Insurance Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Crop Insurance Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Crop Insurance Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Crop Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Crop Insurance Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Crop Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Crop Insurance Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Crop Insurance Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Crop Insurance Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Crop Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Crop Insurance Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Crop Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Crop Insurance Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Crop Insurance Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Crop Insurance Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Crop Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Crop Insurance Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Crop Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Crop Insurance Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Crop Insurance Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Crop Insurance Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Crop Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Crop Insurance Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Crop Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Crop Insurance Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Crop Insurance Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Crop Insurance Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Crop Insurance Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Crop Insurance Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Crop Insurance Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Crop Insurance Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Crop Insurance Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Crop Insurance Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Crop Insurance Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Crop Insurance Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Crop Insurance Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Crop Insurance Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Crop Insurance Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Crop Insurance Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Crop Insurance Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Crop Insurance Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Crop Insurance Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Crop Insurance Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Crop Insurance Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Crop Insurance Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Crop Insurance Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Crop Insurance Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Crop Insurance?

The projected CAGR is approximately 6.1%.

2. Which companies are prominent players in the Crop Insurance?

Key companies in the market include PICC, Zurich, Chubb, QBE, China United Property Insurance, American Financial Group, Prudential, XL Catlin, Everest Re Group, Endurance Specialty, CUNA Mutual, Agriculture Insurance Company of India, Tokio Marine, CGB Diversified Services, Farmers Mutual Hail, Archer Daniels Midland, New India Assurance, ICICI Lombard.

3. What are the main segments of the Crop Insurance?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 45.61 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Crop Insurance," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Crop Insurance report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Crop Insurance?

To stay informed about further developments, trends, and reports in the Crop Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence