Key Insights

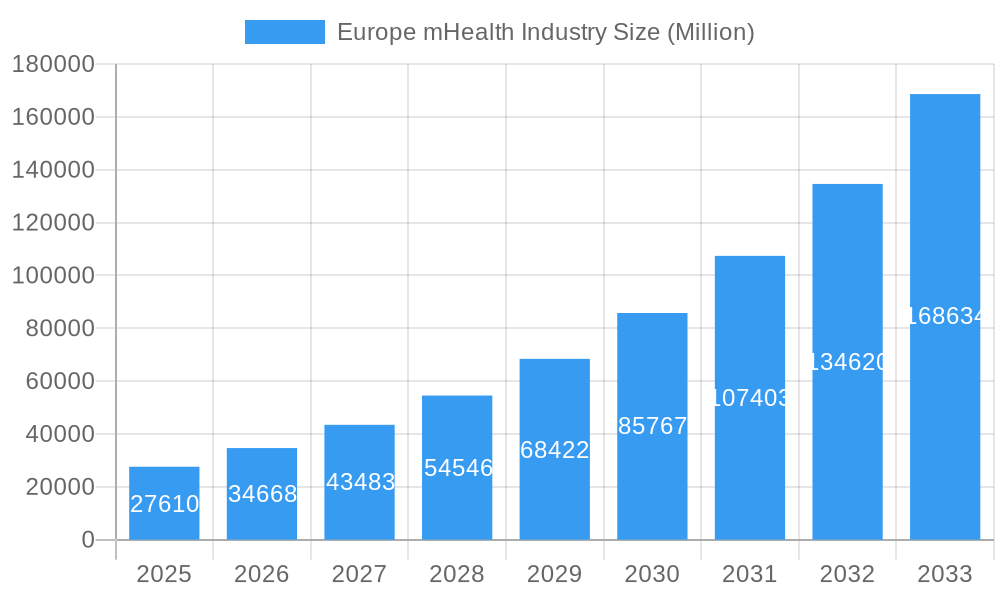

The European mHealth market is experiencing robust growth, projected to reach a substantial size driven by increasing smartphone penetration, aging populations demanding remote healthcare solutions, and supportive government initiatives. The 25.43% CAGR from 2019-2024 suggests a rapidly expanding market, indicating a strong demand for remote patient monitoring (RPM) devices and services. This growth is fueled by several key factors: the rising prevalence of chronic diseases necessitating continuous health monitoring; the increasing adoption of telehealth platforms and applications by healthcare providers aiming to improve efficiency and patient access; and the development of sophisticated, user-friendly mobile health applications and wearable technologies that facilitate data collection and analysis. Specific segments like blood glucose monitors, cardiac monitors, and remote patient monitoring devices are expected to witness significant traction. While the market faces challenges such as data security and privacy concerns, regulatory hurdles, and the need for improved interoperability between devices and platforms, the overall outlook remains positive.

Europe mHealth Industry Market Size (In Billion)

The European mHealth market's segmentation reveals a diverse landscape. Mobile operators play a pivotal role in delivering connectivity and services, partnering with healthcare providers and application developers. The service type segment is equally dynamic, encompassing monitoring services, post-acute care, diagnostic and treatment services via medical call centers, teleconsultation, and wellness solutions. Leading companies like Medtronic, Omron, Samsung, and Philips are actively shaping the market with their innovative devices and solutions. The geographic spread within Europe indicates strong market performance across major economies like Germany, France, UK, and Italy, reflecting these countries’ robust healthcare infrastructure and technological adoption rates. Future growth will hinge on addressing data security and interoperability issues while fostering wider adoption among both healthcare professionals and patients across the region. Expansion into underserved areas and the integration of artificial intelligence (AI) and machine learning (ML) are expected to further accelerate market growth over the forecast period.

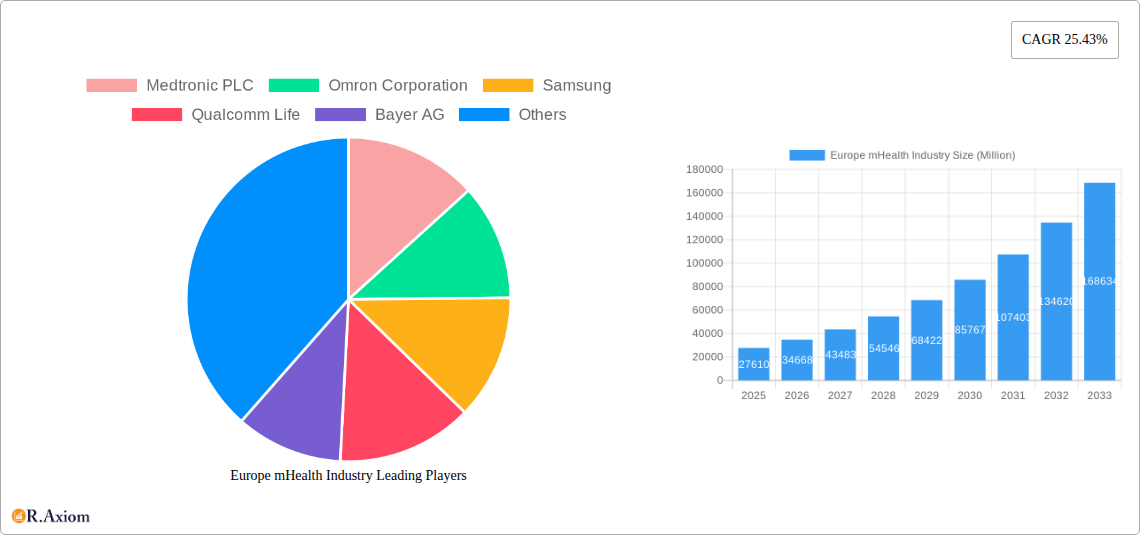

Europe mHealth Industry Company Market Share

Europe mHealth Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Europe mHealth industry, covering market size, segmentation, growth drivers, challenges, and key players. The report utilizes data from the historical period (2019-2024), base year (2025), and estimated year (2025) to forecast market trends from 2025-2033. The study reveals significant opportunities for growth within the European mHealth sector, driven by technological advancements, increasing adoption of remote healthcare solutions, and supportive government regulations.

Europe mHealth Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the European mHealth market, including market concentration, innovation drivers, regulatory frameworks, and M&A activities. The market is characterized by a mix of large multinational corporations and smaller specialized companies. Top players such as Medtronic PLC, Omron Corporation, and Koninklijke Philips N.V. hold significant market share, but the market also features numerous smaller players focusing on niche segments.

- Market Concentration: The top 5 players account for approximately xx% of the total market revenue in 2025. This concentration is expected to slightly decrease by 2033 due to increased competition and the emergence of innovative startups.

- Innovation Drivers: The industry is fueled by advancements in mobile technology, AI, big data analytics, and sensor technology. These advancements are enabling the development of more sophisticated and user-friendly mHealth devices and applications.

- Regulatory Frameworks: EU regulations, such as GDPR and the Medical Device Regulation (MDR), significantly impact the industry. Compliance requirements drive innovation in data security and device certification.

- Product Substitutes: Traditional healthcare services act as a substitute, however, the convenience and cost-effectiveness of mHealth are gradually shifting patient preference.

- End-User Trends: Growing adoption of smartphones and wearables, coupled with an aging population and increasing chronic disease prevalence, significantly boosts market growth.

- M&A Activities: Significant M&A activity has been observed in the recent years, with deal values exceeding €xx Million in 2024. These activities aim to expand market share, access new technologies, and strengthen product portfolios.

Europe mHealth Industry Industry Trends & Insights

The European mHealth market exhibits robust growth, driven by several key factors. The market is experiencing a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by technological advancements, changing consumer preferences towards convenient and accessible healthcare, and supportive government initiatives promoting digital health. Market penetration of mHealth solutions is expected to reach xx% by 2033, up from xx% in 2025. The competitive landscape is dynamic, with both established players and emerging startups vying for market share. Technological disruptions, such as the integration of AI and machine learning, are transforming service offerings and enhancing diagnostic capabilities. Consumer preference for personalized and proactive healthcare is driving demand for tailored mHealth solutions.

Dominant Markets & Segments in Europe mHealth Industry

This section identifies the leading regions, countries, and segments within the European mHealth market. Germany, France, and the UK are the dominant markets, owing to their advanced healthcare infrastructure, high technological adoption rates, and sizable populations. Within the device type segment, Remote Patient Monitoring (RPM) devices are experiencing the fastest growth, driven by their potential to reduce hospital readmissions and improve patient outcomes. The Healthcare Providers segment holds a significant market share among stakeholders due to the increasing adoption of mHealth solutions for remote patient monitoring and disease management. Regarding services, Monitoring Services holds the largest market share, and Teleconsultation is experiencing considerable growth.

- Key Drivers (Regional Dominance):

- Germany: Strong healthcare infrastructure, favorable regulatory environment, and high technological adoption.

- France: Significant government investment in digital health initiatives and a growing aging population.

- UK: Well-established National Health Service (NHS) and ongoing digital health transformation efforts.

- Segment Dominance Analysis: Detailed analysis of each segment (By Device Type, Stakeholder, and Service Type) including market size, growth rate, and competitive landscape will be provided in the full report.

Europe mHealth Industry Product Developments

The European mHealth industry witnesses continuous product innovation, focusing on improved user experience, enhanced data analytics capabilities, and seamless integration with existing healthcare systems. Technological trends such as AI-powered diagnostic tools, wearable sensors with advanced data collection capabilities, and secure cloud-based platforms are shaping product development. These innovations are improving the accuracy and effectiveness of mHealth solutions, enhancing patient engagement and adherence, and ultimately driving market growth.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the European mHealth market across various segments:

By Device Type: Blood Glucose Monitors, Cardiac Monitors, Hemodynamic Monitors, Neurological Monitors, Respiratory Monitors, Body and Temperature Monitors, Remote Patient Monitoring Devices, Other Device Types. Growth projections and market sizes are provided for each segment, along with a competitive analysis.

By Stakeholder: Mobile Operators, Healthcare Providers, Application/Content Players, Other Stakeholders. The report details the role of each stakeholder and their influence on market growth.

By Service Type: Monitoring Services, Post-Acute Care Services, Diagnostic Services, Medical Call Centers, Treatment Services, Teleconsultation, Wellness and Fitness Solutions, Other Services. Growth projections and market sizes are provided for each service type, along with analysis of competitive dynamics.

Key Drivers of Europe mHealth Industry Growth

Several key factors drive the growth of the European mHealth industry. These include technological advancements enabling the creation of sophisticated and user-friendly devices and applications; increasing prevalence of chronic diseases requiring continuous monitoring and management; supportive government initiatives and regulatory frameworks promoting the adoption of digital health technologies; and rising consumer demand for convenient and accessible healthcare.

Challenges in the Europe mHealth Industry Sector

The European mHealth industry faces challenges such as data security and privacy concerns stemming from the sensitive nature of patient data, stringent regulatory requirements impacting product development and market entry, ensuring interoperability across different mHealth platforms and systems, and addressing the digital literacy gap amongst some segments of the population. These factors can impact market growth and adoption rates.

Emerging Opportunities in Europe mHealth Industry

Emerging opportunities exist in the development of AI-powered diagnostic tools, personalized medicine solutions tailored to individual patient needs, integration of mHealth with wearable technology for continuous health monitoring, and expansion of mHealth services into underserved rural areas. The expansion of 5G network coverage further boosts opportunities.

Leading Players in the Europe mHealth Industry Market

Key Developments in Europe mHealth Industry Industry

- 2023-Oct: Launch of a new remote patient monitoring platform by Medtronic PLC.

- 2024-Feb: Acquisition of a smaller mHealth company by Johnson & Johnson.

- 2024-May: Approval of a new AI-powered diagnostic tool by the European Medicines Agency. (Further key developments with specific years/months will be included in the full report)

Strategic Outlook for Europe mHealth Industry Market

The European mHealth market presents substantial growth potential driven by technological innovation, favorable regulatory support, and rising consumer demand for convenient healthcare. Continued investment in R&D, strategic partnerships, and expansion into new markets will be crucial for success. The focus on personalized medicine, AI-driven diagnostics, and improved data security will shape the future of the industry.

Europe mHealth Industry Segmentation

-

1. Service Type

- 1.1. Monitoring Services

- 1.2. Diagnostic Services

- 1.3. Treatment Services

- 1.4. Wellness and Fitness Solutions

- 1.5. Other Services

-

2. Device Type

- 2.1. Blood Glucose Monitors

- 2.2. Cardiac Monitors

- 2.3. Hemodynamic Monitors

- 2.4. Neurological Monitors

- 2.5. Respiratory Monitors

- 2.6. Body and Temperature Monitors

- 2.7. Remote Patient Monitoring Devices

- 2.8. Other Device Types

-

3. Stake Holder

- 3.1. Mobile Operators

- 3.2. Healthcare Providers

- 3.3. Application/Content Players

- 3.4. Other Stake Holders

Europe mHealth Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. United Kingdom

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Rest of Europe

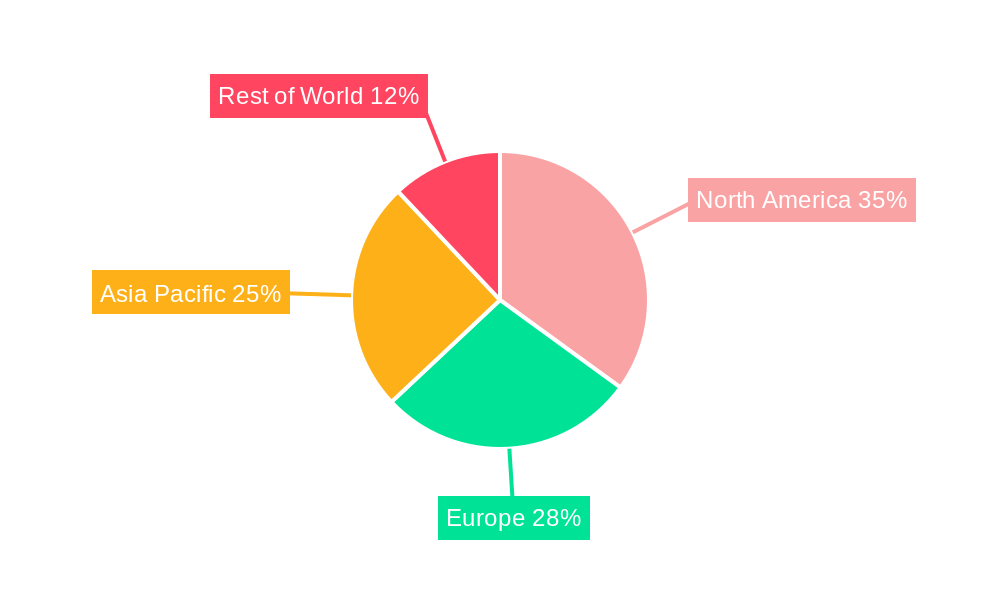

Europe mHealth Industry Regional Market Share

Geographic Coverage of Europe mHealth Industry

Europe mHealth Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 25.43% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Monitoring Services

- 5.1.2. Diagnostic Services

- 5.1.3. Treatment Services

- 5.1.4. Wellness and Fitness Solutions

- 5.1.5. Other Services

- 5.2. Market Analysis, Insights and Forecast - by Device Type

- 5.2.1. Blood Glucose Monitors

- 5.2.2. Cardiac Monitors

- 5.2.3. Hemodynamic Monitors

- 5.2.4. Neurological Monitors

- 5.2.5. Respiratory Monitors

- 5.2.6. Body and Temperature Monitors

- 5.2.7. Remote Patient Monitoring Devices

- 5.2.8. Other Device Types

- 5.3. Market Analysis, Insights and Forecast - by Stake Holder

- 5.3.1. Mobile Operators

- 5.3.2. Healthcare Providers

- 5.3.3. Application/Content Players

- 5.3.4. Other Stake Holders

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Europe mHealth Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Monitoring Services

- 6.1.2. Diagnostic Services

- 6.1.3. Treatment Services

- 6.1.4. Wellness and Fitness Solutions

- 6.1.5. Other Services

- 6.2. Market Analysis, Insights and Forecast - by Device Type

- 6.2.1. Blood Glucose Monitors

- 6.2.2. Cardiac Monitors

- 6.2.3. Hemodynamic Monitors

- 6.2.4. Neurological Monitors

- 6.2.5. Respiratory Monitors

- 6.2.6. Body and Temperature Monitors

- 6.2.7. Remote Patient Monitoring Devices

- 6.2.8. Other Device Types

- 6.3. Market Analysis, Insights and Forecast - by Stake Holder

- 6.3.1. Mobile Operators

- 6.3.2. Healthcare Providers

- 6.3.3. Application/Content Players

- 6.3.4. Other Stake Holders

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Medtronic PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Omron Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Samsung

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Qualcomm Life

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bayer AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Johnson & Johnson

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 AT&T Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Koninklijke Philips N V

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Cisco Systems Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Medtronic PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe mHealth Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe mHealth Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe mHealth Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 2: Europe mHealth Industry Volume K Unit Forecast, by Service Type 2020 & 2033

- Table 3: Europe mHealth Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 4: Europe mHealth Industry Volume K Unit Forecast, by Device Type 2020 & 2033

- Table 5: Europe mHealth Industry Revenue Million Forecast, by Stake Holder 2020 & 2033

- Table 6: Europe mHealth Industry Volume K Unit Forecast, by Stake Holder 2020 & 2033

- Table 7: Europe mHealth Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Europe mHealth Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Europe mHealth Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 10: Europe mHealth Industry Volume K Unit Forecast, by Service Type 2020 & 2033

- Table 11: Europe mHealth Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 12: Europe mHealth Industry Volume K Unit Forecast, by Device Type 2020 & 2033

- Table 13: Europe mHealth Industry Revenue Million Forecast, by Stake Holder 2020 & 2033

- Table 14: Europe mHealth Industry Volume K Unit Forecast, by Stake Holder 2020 & 2033

- Table 15: Europe mHealth Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Europe mHealth Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: Germany Europe mHealth Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Germany Europe mHealth Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: United Kingdom Europe mHealth Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: United Kingdom Europe mHealth Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: France Europe mHealth Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: France Europe mHealth Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Italy Europe mHealth Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Italy Europe mHealth Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Spain Europe mHealth Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Spain Europe mHealth Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Europe mHealth Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Rest of Europe Europe mHealth Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe mHealth Industry?

The projected CAGR is approximately 25.43%.

2. Which companies are prominent players in the Europe mHealth Industry?

Key companies in the market include Medtronic PLC, Omron Corporation, Samsung, Qualcomm Life, Bayer AG, Johnson & Johnson, AT&T Inc, Koninklijke Philips N V, Cisco Systems Inc.

3. What are the main segments of the Europe mHealth Industry?

The market segments include Service Type, Device Type, Stake Holder.

4. Can you provide details about the market size?

The market size is estimated to be USD 27.61 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Use of Smartphones. Tablets; Increasing Focus on Personalized Medicine and Patient-Centered Approach; Increased Need of Point of Care Diagnosis and Treatment.

6. What are the notable trends driving market growth?

Blood Glucose Monitors are Expected to Have the Largest Share in Device Type Segment.

7. Are there any restraints impacting market growth?

Data Security Issues; Stringent Regulatory Policies for mHealth Applications.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe mHealth Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe mHealth Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe mHealth Industry?

To stay informed about further developments, trends, and reports in the Europe mHealth Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence