Key Insights

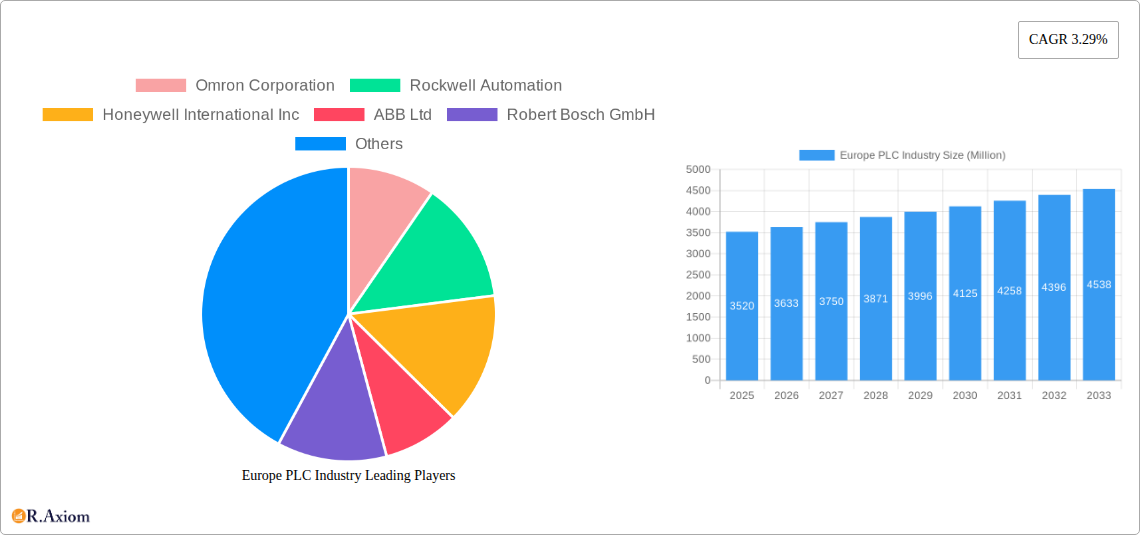

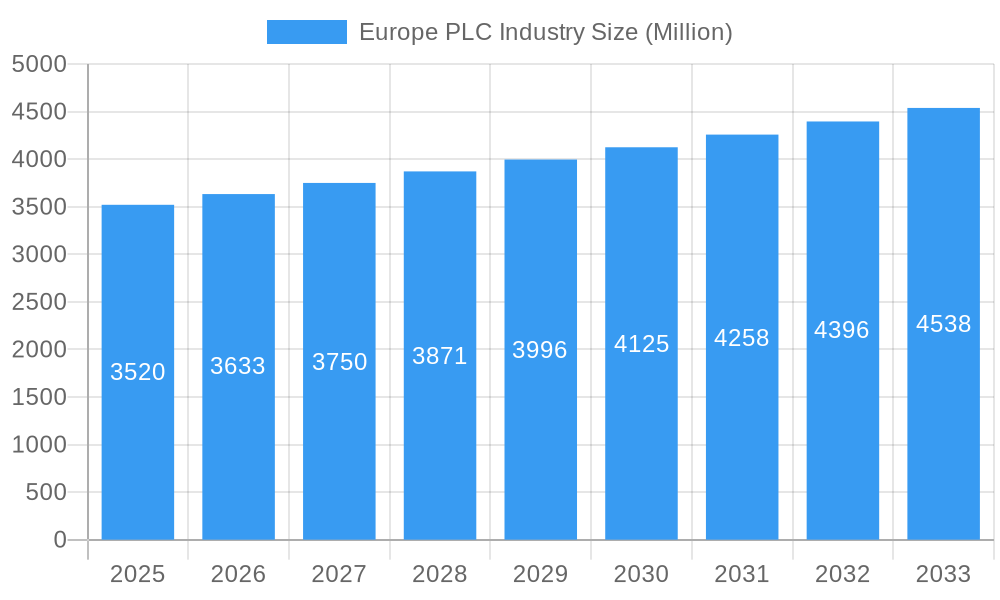

The European Programmable Logic Controller (PLC) market, valued at €3.52 billion in 2025, is projected to experience steady growth, driven by increasing automation across various sectors. The Compound Annual Growth Rate (CAGR) of 3.29% from 2025 to 2033 indicates a continuous, albeit moderate, expansion. Key drivers include the rising adoption of Industry 4.0 technologies, the need for enhanced operational efficiency and productivity in manufacturing, and the growing demand for sophisticated process automation solutions across industries such as automotive, food and beverage, and pharmaceuticals. The market's segmentation reveals a strong presence of hardware and software solutions, with hardware dominating the market share. Germany, France, and the UK are expected to remain the largest contributors to the European market due to their established manufacturing bases and advanced automation infrastructure. However, growth opportunities are emerging in other European countries as well, driven by investments in modernizing industrial processes and infrastructure. While the overall market growth is expected to be positive, factors like the economic climate and the fluctuating prices of raw materials could potentially restrain growth. The market is highly competitive, with major players such as Omron, Rockwell Automation, and Siemens vying for market share through technological innovation and strategic partnerships.

Europe PLC Industry Market Size (In Billion)

The projected growth in the European PLC market is supported by several factors. The ongoing trend of digital transformation within European industries is fueling demand for advanced automation solutions. Moreover, the increasing focus on optimizing supply chains and reducing operational costs makes PLCs an attractive investment for businesses across all sizes. The market is witnessing a significant shift towards cloud-based PLCs and the integration of advanced technologies such as artificial intelligence and machine learning. This trend enhances the capabilities of PLCs beyond basic automation, enabling predictive maintenance, real-time data analysis, and improved decision-making. However, challenges remain in terms of cybersecurity concerns related to connected PLC systems and the need for skilled professionals to manage and maintain these complex systems. Nevertheless, the long-term outlook for the European PLC market remains positive, driven by continuous technological advancements and increasing automation demands within the region.

Europe PLC Industry Company Market Share

This comprehensive report provides a detailed analysis of the Europe PLC industry, covering market size, growth drivers, challenges, and future opportunities. The study period spans 2019-2033, with 2025 as the base and estimated year. This report is essential for industry stakeholders, investors, and businesses seeking to understand the current landscape and future trajectory of the European PLC market.

Europe PLC Industry Market Concentration & Innovation

The European PLC market is characterized by a dynamic yet moderately concentrated landscape, where a core group of multinational corporations commands significant market share. Leading entities such as Siemens AG, Rockwell Automation, and Schneider Electric SE collectively hold an estimated xx% of the market. This dominant position is complemented by a vibrant ecosystem of smaller, specialized players vying for the remaining segment. Factors underpinning this market concentration include the strategic advantage of economies of scale, continuous technological breakthroughs, and the established brand equity of these major corporations. The industry is a hotbed of innovation, propelled by the escalating demand for advanced automation solutions across a diverse range of industrial sectors. This imperative has spurred substantial investment in research and development, with a particular focus on cutting-edge areas like Industrial Internet of Things (IIoT) integration, sophisticated cloud-based management platforms, and the seamless incorporation of Artificial Intelligence (AI) into PLC functionalities. Furthermore, regulatory frameworks, encompassing industrial safety standards and stringent data privacy mandates, critically shape the competitive environment and operational strategies within the industry. The presence of product substitutes, including advanced control systems and Programmable Automation Controllers (PACs), introduces additional competitive pressures, while prevailing end-user trends towards comprehensive digitalization and the adoption of Industry 4.0 principles act as powerful catalysts for ongoing innovation.

Mergers and acquisitions (M&A) have played a moderate but strategic role in industry evolution. In the past five years, M&A deal values have reached an approximate total of xx Million, reflecting a strategic approach to consolidation and the acquisition of specialized technological expertise to enhance competitive offerings.

- Estimated Market Share (2024): Siemens AG (xx%), Rockwell Automation (xx%), Schneider Electric SE (xx%), Other Players (xx%).

- M&A Deal Value (2019-2024): Approximately xx Million.

- Pioneering Innovation Drivers: Industrial Internet of Things (IIoT), Advanced Cloud Computing Solutions, AI Integration for Enhanced Control, Robust Cybersecurity Measures.

Europe PLC Industry Industry Trends & Insights

The European PLC market is experiencing robust growth, fueled by several key factors. The increasing adoption of automation technologies across various end-user industries, including automotive, food and beverage, and pharmaceuticals, is a primary driver. The rising demand for improved operational efficiency, enhanced productivity, and reduced labor costs is driving PLC adoption. Technological disruptions, such as the emergence of IIoT and cloud-based PLC solutions, are transforming industry practices, leading to increased connectivity, remote monitoring, and predictive maintenance capabilities. Consumer preferences are shifting towards more sophisticated and integrated automation systems, which offer greater flexibility and scalability. Competitive dynamics are characterized by intense competition among established players and emerging innovative companies, resulting in continuous product improvements and price pressures. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), with market penetration expected to increase significantly in emerging sectors. This growth is further amplified by government initiatives promoting industrial automation and digital transformation across Europe.

Dominant Markets & Segments in Europe PLC Industry

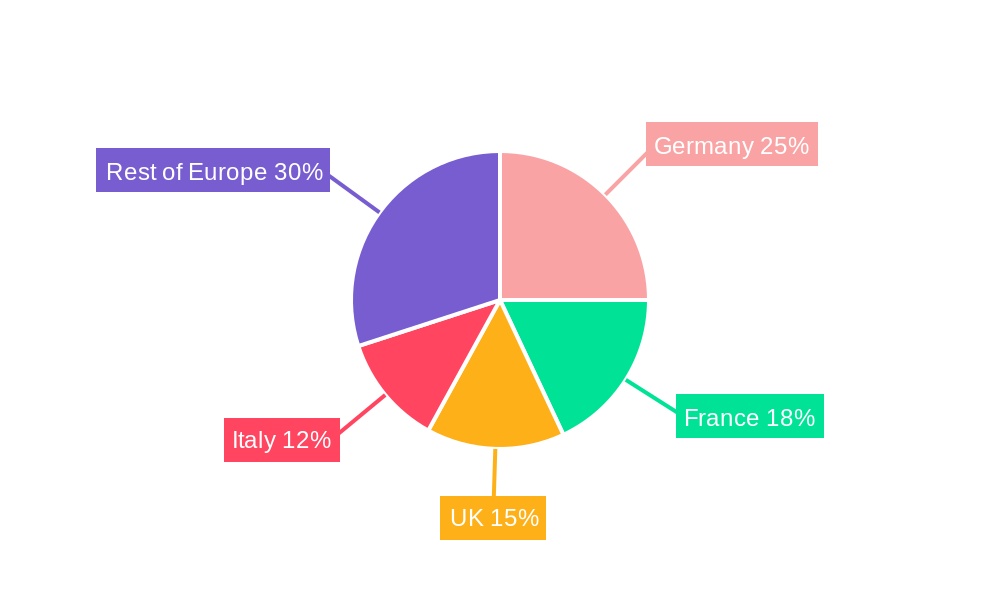

Geographically, the European PLC market is spearheaded by Germany, with the United Kingdom and France following closely. These leading nations benefit from highly developed industrial infrastructures, mature automation ecosystems, and a substantial concentration of manufacturing operations. Across end-user industries, the automotive sector, chemical and petrochemical industries, and the food and beverage segment represent the most significant adopters and consumers of PLC technology. In terms of product segmentation, the hardware component currently accounts for a larger market share, underscoring the foundational importance of physical PLC devices in industrial automation. However, the software segment is experiencing robust growth, fueled by the increasing need for sophisticated control algorithms, advanced data analytics capabilities, and seamless integration solutions. Complementing these, service revenue is also on an upward trajectory, driven by the escalating demand for comprehensive maintenance, support, and lifecycle management services for complex PLC installations.

- Key Factors Driving Regional Dominance (Germany): A formidable automotive and general manufacturing sector, highly advanced industrial automation infrastructure, and strong governmental initiatives supporting industrial modernization.

- Key Factors Driving Segment Dominance (Automotive): Intense automation requirements in production lines, adherence to rigorous quality control standards, and a persistent demand for highly precise and reliable control systems.

Germany's Prominence: Characterized by a powerful manufacturing base, widespread adoption of cutting-edge automation technologies, and a significant cluster of major PLC manufacturers and solution providers.

Automotive Sector's Demand: The automotive industry's high reliance on automation for its assembly lines and intricate manufacturing processes is a primary driver for extensive PLC implementation and continuous technological upgrades.

Europe PLC Industry Product Developments

Recent product innovations in the European PLC market are strongly aligned with enhanced connectivity, superior data analytics capabilities, and the seamless integration of PLCs into broader industrial automation architectures. Contemporary PLCs are increasingly equipped with advanced communication protocols, such as Ethernet/IP and PROFINET, which are instrumental in facilitating efficient data exchange and enabling real-time monitoring of industrial processes. Manufacturers are actively developing more compact, energy-efficient devices that deliver superior processing power. These advancements allow for the execution of complex control algorithms and the integration of AI, paving the way for more sophisticated and autonomous automation solutions. Such product enhancements are pivotal in boosting operational efficiency, minimizing downtime, and enabling the proactive implementation of predictive maintenance strategies. This continuous evolution in functionality and performance not only fortifies the competitive edge of PLC manufacturers but also ensures a stronger market fit across a wide spectrum of industrial applications.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation analysis of the European PLC market, examining the market by end-user industry, country, and type. The end-user segments include Food, Tobacco, and Beverage; Automotive; Chemical and Petrochemical; Energy and Utilities; Pharmaceutical; Oil and Gas; and Other End-user Industries. The country-level analysis focuses on major European markets. The type segment is categorized into Hardware and Software, with further sub-segmentation into various hardware types and service offerings. Growth projections, market sizes, and competitive dynamics are detailed for each segment, providing a granular view of the market landscape. The Automotive segment shows rapid growth, driven by increasing automation. The Chemical and Petrochemical segment exhibits steady growth due to process optimization needs. Growth projections vary depending on the specific sector and regional market. The Software segment is characterized by higher growth rates driven by software-centric solutions.

Key Drivers of Europe PLC Industry Growth

The growth of the Europe PLC industry is primarily driven by technological advancements, economic factors, and supportive regulatory frameworks. Technological advancements, such as IIoT, cloud computing, and AI, are enabling more sophisticated and efficient automation solutions. Economic growth in several European countries drives investments in manufacturing and automation upgrades. Government initiatives supporting industrial digitalization and automation provide a favorable environment for PLC adoption.

Challenges in the Europe PLC Industry Sector

Challenges facing the Europe PLC industry include increasing regulatory compliance costs, supply chain disruptions affecting component availability, and fierce competition from established and emerging players. These factors can impact manufacturing costs, product delivery times, and overall profitability. The industry faces pressure to keep up with changing regulatory environments and rapidly evolving technologies.

Emerging Opportunities in Europe PLC Industry

Emerging opportunities lie in the expansion of IIoT applications, the integration of AI and machine learning, and the growth of the service sector for PLC solutions. The development of new solutions for smart factories and Industry 4.0 initiatives presents significant growth prospects. New market segments, such as renewable energy and smart grids, are further creating opportunities.

Leading Players in the Europe PLC Industry Market

Key Developments in Europe PLC Industry Industry

- October 2023: Mouser Electronics, Inc. has strategically expanded its distribution network through a new agreement with Siemens, enhancing the accessibility of Siemens' comprehensive range of PLC products across Europe.

- February 2024: WEG has launched its innovative PLC410 programmable logic controller, specifically engineered to cater to the demanding requirements of Original Equipment Manufacturers (OEMs) in the packaging, labeling, and filling machine industries.

Strategic Outlook for Europe PLC Industry Market

The future of the European PLC market looks promising, with sustained growth driven by ongoing industrial automation, digital transformation, and the emergence of new technologies. Opportunities exist in developing specialized PLC solutions for niche industries and integrating advanced technologies, such as AI and machine learning, to enhance functionality and create innovative automation solutions. Further consolidation within the industry is anticipated as companies seek to expand their market reach and enhance their technological capabilities. The market is poised for continued growth and innovation.

Europe PLC Industry Segmentation

-

1. Type

-

1.1. Hardware and Software

- 1.1.1. Large PLC

- 1.1.2. Nano PLC

- 1.1.3. Small PLC

- 1.1.4. Medium PLC

- 1.1.5. Other Hardware Types

- 1.2. Service

-

1.1. Hardware and Software

-

2. End-user Industry

- 2.1. Food, Tobacco, and Beverage

- 2.2. Automotive

- 2.3. Chemical and Petrochemical

- 2.4. Energy and Utilities

- 2.5. Pharmaceutical

- 2.6. Oil and Gas

- 2.7. Other End-user Industries

Europe PLC Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe PLC Industry Regional Market Share

Geographic Coverage of Europe PLC Industry

Europe PLC Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Hardware and Software

- 5.1.1.1. Large PLC

- 5.1.1.2. Nano PLC

- 5.1.1.3. Small PLC

- 5.1.1.4. Medium PLC

- 5.1.1.5. Other Hardware Types

- 5.1.2. Service

- 5.1.1. Hardware and Software

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food, Tobacco, and Beverage

- 5.2.2. Automotive

- 5.2.3. Chemical and Petrochemical

- 5.2.4. Energy and Utilities

- 5.2.5. Pharmaceutical

- 5.2.6. Oil and Gas

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe PLC Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Hardware and Software

- 6.1.1.1. Large PLC

- 6.1.1.2. Nano PLC

- 6.1.1.3. Small PLC

- 6.1.1.4. Medium PLC

- 6.1.1.5. Other Hardware Types

- 6.1.2. Service

- 6.1.1. Hardware and Software

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Food, Tobacco, and Beverage

- 6.2.2. Automotive

- 6.2.3. Chemical and Petrochemical

- 6.2.4. Energy and Utilities

- 6.2.5. Pharmaceutical

- 6.2.6. Oil and Gas

- 6.2.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Omron Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Rockwell Automation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Honeywell International Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ABB Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Robert Bosch GmbH

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hitachi Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Emerson Electric Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Panasonic Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mitsubishi Electric Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Siemens AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Beckhoff Automatio

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 General Electric Co

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Schneider Electric SE

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Omron Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe PLC Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe PLC Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe PLC Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Europe PLC Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Europe PLC Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe PLC Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Europe PLC Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Europe PLC Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe PLC Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe PLC Industry?

The projected CAGR is approximately 3.29%.

2. Which companies are prominent players in the Europe PLC Industry?

Key companies in the market include Omron Corporation, Rockwell Automation, Honeywell International Inc, ABB Ltd, Robert Bosch GmbH, Hitachi Ltd, Emerson Electric Co, Panasonic Corporation, Mitsubishi Electric Corporation, Siemens AG, Beckhoff Automatio, General Electric Co, Schneider Electric SE.

3. What are the main segments of the Europe PLC Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.52 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Adoption of Automation Systems; Ease of Use and Familiarity with PLC Programming to Sustain Growth.

6. What are the notable trends driving market growth?

Oil and Gas Industry to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Increasing Adoption of AC Technology.

8. Can you provide examples of recent developments in the market?

February 2024 - WEG recently introduced the PLC410 programmable logic controller, a versatile solution for industrial automation. While it finds applications across diverse sectors like pulp and paper, metallurgy, pharmaceuticals, and sugar and alcohol, its primary focus targets equipment manufacturers (OEMs) in industries like packaging, labeling, and filling machines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe PLC Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe PLC Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe PLC Industry?

To stay informed about further developments, trends, and reports in the Europe PLC Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence