Key Insights

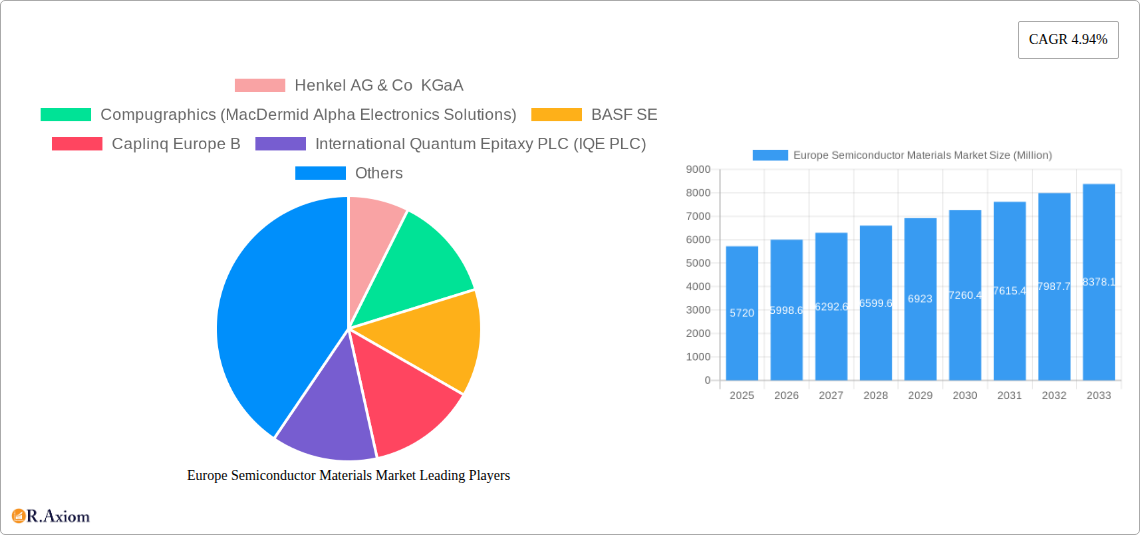

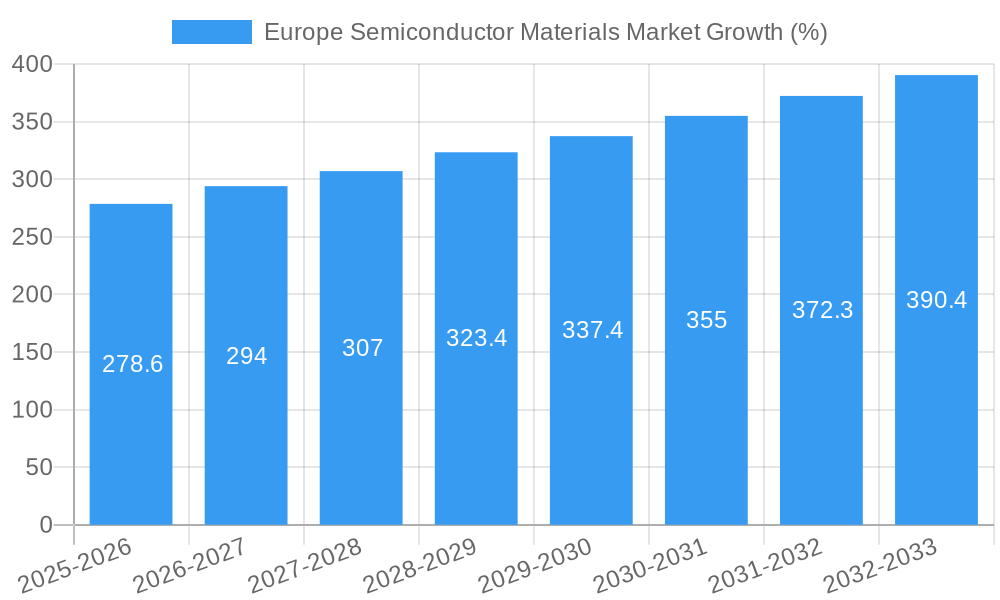

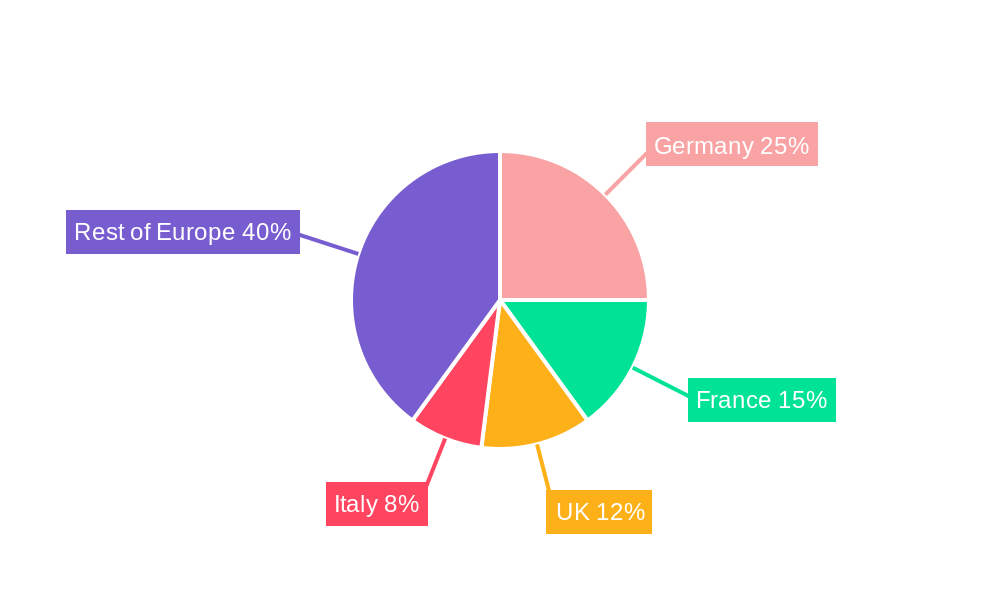

The European semiconductor materials market, valued at €5.72 billion in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 4.94% from 2025 to 2033. This expansion is fueled by several key factors. The burgeoning consumer electronics sector, particularly in the areas of smartphones, wearables, and advanced computing devices, demands increasingly sophisticated semiconductor materials. Simultaneously, the telecommunications industry's continuous drive towards 5G and beyond necessitates high-performance materials capable of supporting faster data transmission and network efficiency. The automotive industry's transition towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) also contributes significantly to market growth, requiring specialized semiconductor materials for power electronics and sensor applications. Furthermore, the growing energy and utility sector's reliance on smart grids and renewable energy technologies further enhances the demand for specialized materials. Germany, France, and the United Kingdom are expected to be the leading markets within Europe, reflecting their robust manufacturing sectors and technological advancements.

However, market growth is not without its challenges. Supply chain disruptions, geopolitical uncertainties, and the volatile pricing of raw materials present potential restraints. Competition among established players and emerging technological advancements may also influence market dynamics. Nevertheless, the long-term outlook remains positive, with continued innovation in semiconductor technology and expanding applications across diverse end-user industries ensuring a sustained period of growth for the European semiconductor materials market. The market segmentation reveals strong demand across various applications, notably fabrication and packaging within the consumer electronics, telecommunications, and automotive sectors. Leading players like Henkel, BASF, and Solvay are strategically positioned to capitalize on these trends through technological advancements, strategic partnerships, and investments in research and development.

This in-depth report provides a comprehensive analysis of the Europe Semiconductor Materials market, offering invaluable insights for stakeholders across the semiconductor value chain. Spanning the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market trends, competitive dynamics, and future growth prospects. The report leverages robust data and expert analysis to provide actionable intelligence for strategic decision-making.

Europe Semiconductor Materials Market Market Concentration & Innovation

The European semiconductor materials market exhibits a moderately concentrated landscape, with a few major players holding significant market share. Henkel AG & Co KGaA, BASF SE, and Solvay SA, for example, command substantial portions of the market, driven by their established technological capabilities and extensive distribution networks. However, the market also features several smaller, specialized players that are innovating rapidly, particularly in niche segments like advanced packaging materials.

Market Concentration Metrics (2024 Estimates):

- Top 3 players: xx% combined market share

- Top 5 players: xx% combined market share

- Average market share of top 10 players: xx%

Innovation Drivers:

- Miniaturization: The relentless pursuit of smaller, more powerful chips fuels demand for advanced materials with enhanced performance characteristics.

- 5G and IoT: The proliferation of 5G networks and the Internet of Things (IoT) is creating significant demand for semiconductor materials with high bandwidth and low power consumption.

- AI and Machine Learning: Advancements in artificial intelligence and machine learning are driving the need for specialized materials that support high-performance computing.

Regulatory Landscape: EU regulations regarding environmental sustainability and supply chain security are impacting the market, pushing companies to adopt more environmentally friendly manufacturing processes and diversify their sourcing strategies. The EU's Chips Act is further shaping the industry landscape, driving investments in domestic production and innovation.

M&A Activities: While precise deal values are unavailable, significant merger and acquisition (M&A) activities have been observed in the past five years, focusing on enhancing technology portfolios and expanding market reach. These activities demonstrate a dynamic competitive landscape.

Product Substitutes: Emerging alternative materials are posing a challenge. The introduction of new materials with superior performance or cost advantages necessitates ongoing innovation and adaptation within the industry. The market is also witnessing the exploration of eco-friendly alternatives.

End-User Trends: The increasing adoption of semiconductors across diverse end-user industries, such as automotive, consumer electronics, and telecommunications, fuels continuous market growth. Changing consumer preferences regarding device functionality and sustainability also influence the demand for specific materials.

Europe Semiconductor Materials Market Industry Trends & Insights

The European semiconductor materials market is experiencing robust growth, driven by strong demand from multiple end-user sectors. The market is characterized by a high degree of technological innovation, with continuous improvements in material properties and manufacturing processes. This innovation is influenced by the rise of advanced computing applications, including AI and machine learning, along with the demands of 5G networks.

The compound annual growth rate (CAGR) for the period 2025-2033 is projected to be xx%. The market penetration of advanced materials (e.g., SiC, GaN) is steadily increasing, driven by the need for higher power efficiency and performance in end-use applications. The market's evolution is influenced by several factors:

- Technological Disruptions: The ongoing miniaturization trend necessitates new material development; materials such as silicon carbide (SiC) and gallium nitride (GaN) are gaining traction, presenting significant growth opportunities.

- Consumer Preferences: Increasing demand for smaller, faster, and more energy-efficient devices fuels the demand for high-performance materials.

- Competitive Dynamics: Intense competition amongst established players and new entrants is driving innovation and price reductions.

The automotive sector remains a key driver, fueled by the global shift toward electric vehicles, which necessitate high-performance semiconductor components. Growth is also witnessed in telecommunications due to the ongoing expansion of 5G infrastructure. The manufacturing sector, with its increasing automation and digitalization, contributes significantly to market growth.

Dominant Markets & Segments in Europe Semiconductor Materials Market

The automotive sector is a dominant end-user industry, significantly impacting market growth. Germany, France, and Italy represent leading regional markets, benefiting from established automotive manufacturing hubs and robust R&D activities. Within applications, fabrication materials hold the largest market share due to their crucial role in chip manufacturing.

Key Drivers for Dominant Segments:

- Automotive: The rapid adoption of electric vehicles and advanced driver-assistance systems (ADAS) is significantly increasing the demand for high-performance semiconductors.

- Fabrication: Constant innovation in semiconductor technology necessitates advanced materials for chip fabrication, leading to substantial growth.

- Germany: A strong automotive industry and extensive semiconductor manufacturing capabilities contribute to Germany's dominance.

- France: A robust electronics industry and substantial government investment in R&D contribute to France's significant market share.

The dominance of these segments is reinforced by several factors: robust government support for the semiconductor industry, a skilled workforce, and strategic partnerships between material suppliers and semiconductor manufacturers. The ongoing investments in the automotive and manufacturing sectors are likely to enhance this dominance in the forecast period. These factors collectively shape the market's regional and segmental dynamics.

Europe Semiconductor Materials Market Product Developments

Recent product developments focus on enhancing material properties like thermal conductivity, dielectric strength, and purity. New materials like silicon carbide (SiC) and gallium nitride (GaN) are gaining prominence due to their superior performance characteristics compared to traditional silicon-based materials. These advancements cater to the increasing demands of high-performance computing, 5G networks, and electric vehicles. Companies are emphasizing eco-friendly solutions and sustainable manufacturing processes to meet growing environmental concerns.

Report Scope & Segmentation Analysis

This report segments the Europe semiconductor materials market by application (Fabrication, Packaging) and end-user industry (Consumer Electronics, Telecommunication, Manufacturing, Automotive, Energy and Utility, Other End-User Industries).

By Application:

- Fabrication: This segment comprises the largest market share, driven by the continuous advancements in semiconductor technology. Growth is projected at xx% CAGR during the forecast period. Competition is intense due to the high technological barriers to entry.

- Packaging: This segment exhibits steady growth due to increasing demand for advanced packaging solutions to enhance chip performance and reliability. The projected CAGR is xx%.

By End-user Industry:

Each end-user segment displays unique growth dynamics and competitive landscapes, influenced by factors such as technological advancements, regulatory environments, and economic conditions. Growth rates vary across segments, with automotive and telecommunications showing particularly strong potential.

Key Drivers of Europe Semiconductor Materials Market Growth

The European semiconductor materials market's growth is driven by several key factors:

- Technological Advancements: Continuous innovation in semiconductor technology necessitates advanced materials with improved performance characteristics, fueling market expansion.

- Government Initiatives: Government support for the semiconductor industry, including subsidies and tax incentives, stimulates domestic production and strengthens the market.

- Rising Demand: The increasing adoption of semiconductors in diverse end-user sectors, particularly automotive and telecommunications, drives strong market demand.

Challenges in the Europe Semiconductor Materials Market Sector

Several challenges hinder the Europe semiconductor materials market's growth:

- Supply Chain Disruptions: Geopolitical instability and pandemic-related disruptions have created significant supply chain challenges, impacting material availability and cost.

- Price Volatility: Fluctuations in raw material prices significantly impact the cost of production and profitability.

- Competition: Intense competition from both established and emerging players exerts downward pressure on pricing.

Emerging Opportunities in Europe Semiconductor Materials Market

Several emerging opportunities are shaping the market’s future:

- Sustainable Materials: Growing environmental concerns are driving the demand for eco-friendly and sustainable materials.

- New Applications: Emerging applications in areas such as renewable energy and IoT are creating new avenues for market growth.

- Technological Innovation: Continuous advancements in semiconductor technology and material science generate opportunities for new product development.

Leading Players in the Europe Semiconductor Materials Market Market

- Henkel AG & Co KGaA

- Compugraphics (MacDermid Alpha Electronics Solutions)

- BASF SE

- Caplinq Europe B

- International Quantum Epitaxy PLC (IQE PLC)

- Solvay SA

- Air Liquide SA

- Messer SE & Co KGaA

Key Developments in Europe Semiconductor Materials Market Industry

- October 2022: STMicroelectronics announced a EUR 730 million (USD 728 million) investment in a silicon carbide wafer plant in Italy, boosted by EU initiatives to bolster domestic chip production.

- June 2022: BASF announced the construction of a commercial-scale battery recycling plant in Germany, strengthening its position in the battery materials market and supporting the growing demand for electric vehicles.

Strategic Outlook for Europe Semiconductor Materials Market Market

The European semiconductor materials market presents significant growth potential driven by technological advancements, increasing demand from various end-user sectors, and supportive government policies. The market’s future is shaped by the ongoing development of advanced materials, the expansion of 5G and IoT, and the increasing adoption of electric vehicles. Companies focusing on innovation, sustainability, and supply chain resilience are poised to capitalize on these opportunities.

Europe Semiconductor Materials Market Segmentation

-

1. Application

-

1.1. Fabrication

- 1.1.1. Process Chemicals

- 1.1.2. Photomasks

- 1.1.3. Electronic Gases

- 1.1.4. Photoresists Ancillaries

- 1.1.5. Sputtering Targets

- 1.1.6. Silicon

- 1.1.7. Other Fabrication Applications

-

1.2. Packaging

- 1.2.1. Substrates

- 1.2.2. Lead Frames

- 1.2.3. Ceramic Packages

- 1.2.4. Bonding Wire

- 1.2.5. Encapsulation Resins (Liquid)

- 1.2.6. Die Attach Materials

- 1.2.7. Other Packaging Applications

-

1.1. Fabrication

-

2. End-user Industry

- 2.1. Consumer Electronics

- 2.2. Telecommunication

- 2.3. Manufacturing

- 2.4. Automotive

- 2.5. Energy and Utility

- 2.6. Other End-User Industries

Europe Semiconductor Materials Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Semiconductor Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.94% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Technical Advancement and Product Innovation of the Semiconductor Materials; Rising Demand for Consumer Electronics Goods; Increased Demand from OSAT/Packaging Companies

- 3.3. Market Restrains

- 3.3.1. Complexity in the Manufacturing Process

- 3.4. Market Trends

- 3.4.1. Technical Advancement and Product Innovation of the Semiconductor Materials

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fabrication

- 5.1.1.1. Process Chemicals

- 5.1.1.2. Photomasks

- 5.1.1.3. Electronic Gases

- 5.1.1.4. Photoresists Ancillaries

- 5.1.1.5. Sputtering Targets

- 5.1.1.6. Silicon

- 5.1.1.7. Other Fabrication Applications

- 5.1.2. Packaging

- 5.1.2.1. Substrates

- 5.1.2.2. Lead Frames

- 5.1.2.3. Ceramic Packages

- 5.1.2.4. Bonding Wire

- 5.1.2.5. Encapsulation Resins (Liquid)

- 5.1.2.6. Die Attach Materials

- 5.1.2.7. Other Packaging Applications

- 5.1.1. Fabrication

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Consumer Electronics

- 5.2.2. Telecommunication

- 5.2.3. Manufacturing

- 5.2.4. Automotive

- 5.2.5. Energy and Utility

- 5.2.6. Other End-User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Germany Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Semiconductor Materials Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Henkel AG & Co KGaA

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Compugraphics (MacDermid Alpha Electronics Solutions)

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 BASF SE

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Caplinq Europe B

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 International Quantum Epitaxy PLC (IQE PLC)

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Solvay SA

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Air Liquide SA

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Messer SE & Co KGaA

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.1 Henkel AG & Co KGaA

List of Figures

- Figure 1: Europe Semiconductor Materials Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Semiconductor Materials Market Share (%) by Company 2024

List of Tables

- Table 1: Europe Semiconductor Materials Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Semiconductor Materials Market Revenue Million Forecast, by Application 2019 & 2032

- Table 3: Europe Semiconductor Materials Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Europe Semiconductor Materials Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Semiconductor Materials Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Semiconductor Materials Market Revenue Million Forecast, by Application 2019 & 2032

- Table 14: Europe Semiconductor Materials Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 15: Europe Semiconductor Materials Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark Europe Semiconductor Materials Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Semiconductor Materials Market?

The projected CAGR is approximately 4.94%.

2. Which companies are prominent players in the Europe Semiconductor Materials Market?

Key companies in the market include Henkel AG & Co KGaA, Compugraphics (MacDermid Alpha Electronics Solutions), BASF SE, Caplinq Europe B, International Quantum Epitaxy PLC (IQE PLC), Solvay SA, Air Liquide SA, Messer SE & Co KGaA.

3. What are the main segments of the Europe Semiconductor Materials Market?

The market segments include Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Technical Advancement and Product Innovation of the Semiconductor Materials; Rising Demand for Consumer Electronics Goods; Increased Demand from OSAT/Packaging Companies.

6. What are the notable trends driving market growth?

Technical Advancement and Product Innovation of the Semiconductor Materials.

7. Are there any restraints impacting market growth?

Complexity in the Manufacturing Process.

8. Can you provide examples of recent developments in the market?

October 2022 - STMicroelectronics (ST) declared that it would construct a EUR 730 million (USD 728 million) silicon carbide wafer plant in Italy. This project is the first approved as part of an EU initiative to move chip production closer to consumers' homes. With the switch to electrification, the new integrated silicon carbide (SiC) substrate manufacturing plant would be able to handle the rising demand from automotive and industrial clients.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Semiconductor Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Semiconductor Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Semiconductor Materials Market?

To stay informed about further developments, trends, and reports in the Europe Semiconductor Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence