Key Insights

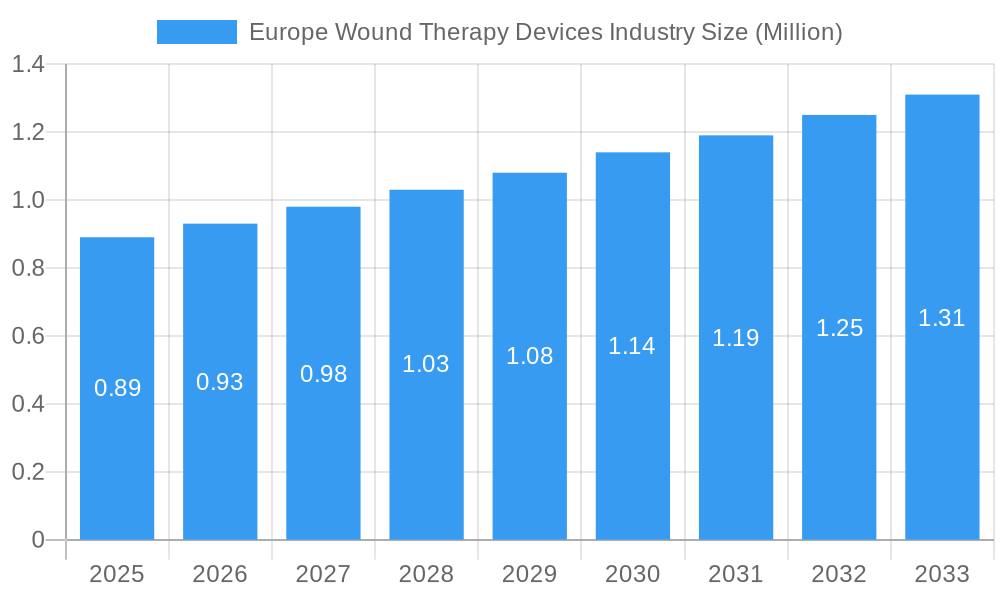

The European Wound Therapy Devices market is poised for robust growth, projected to reach $0.89 Million by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 5.06% through 2033. This expansion is fueled by an increasing prevalence of chronic wounds, particularly diabetic foot ulcers, pressure ulcers, and venous leg ulcers, driven by aging populations and a rise in lifestyle-related diseases like diabetes and obesity. Advanced wound care technologies, including negative pressure wound therapy (NPWT) and advanced wound dressings, are gaining traction due to their superior efficacy in promoting faster healing and reducing complications. The growing demand for homecare solutions and the increasing adoption of these devices in ambulatory settings further bolster market expansion, offering greater convenience and cost-effectiveness for patients and healthcare providers alike.

Europe Wound Therapy Devices Industry Market Size (In Million)

The market segmentation reveals a significant focus on both reusable and single-use devices, catering to diverse clinical needs and infection control protocols. While hospitals remain a primary end-user segment, the burgeoning homecare sector signifies a shift towards decentralized wound management. Key industry players are actively engaged in research and development to introduce innovative products and expand their market reach across key European nations such as Germany, the United Kingdom, France, Italy, and Spain. Emerging economies within "Rest of Europe" also present significant untapped potential. However, factors such as the high cost of advanced wound therapy devices and reimbursement challenges in certain regions may pose moderate restraints to the market's full potential.

Europe Wound Therapy Devices Industry Company Market Share

Europe Wound Therapy Devices Industry Market Concentration & Innovation

The Europe Wound Therapy Devices Industry is characterized by a moderate to high level of market concentration, with a few key players like Smith & Nephew plc, 3M (Acelity L.P. Inc), and Molnlycke Health Care AB holding significant market share. Innovation remains a critical driver, fueled by the increasing prevalence of chronic wounds, an aging population, and advancements in medical technology. Regulatory frameworks, such as those established by the European Medicines Agency (EMA), play a crucial role in product approval and market access, fostering a competitive yet controlled environment. While direct product substitutes are limited, advancements in alternative treatment modalities, like advanced biologics, present a potential area of competitive pressure. End-user preferences are shifting towards cost-effective, efficient, and patient-centric solutions, driving demand for advanced wound care devices. Mergers and acquisitions (M&A) are moderately active, with companies strategically acquiring smaller innovators or complementary product portfolios to expand their market reach and technological capabilities. Recent M&A activities have focused on consolidating expertise in specialized wound types and integrating novel therapeutic approaches. The estimated M&A deal value is in the range of hundreds of millions to billions of Euros, reflecting strategic consolidation.

Europe Wound Therapy Devices Industry Industry Trends & Insights

The Europe Wound Therapy Devices Industry is poised for robust growth, driven by a confluence of powerful trends and insights. A significant growth driver is the escalating prevalence of chronic wounds, particularly diabetic foot ulcers and pressure ulcers, which are directly linked to the rising incidence of diabetes and an aging demographic across Europe. This demographic shift necessitates more advanced and effective wound management solutions, thereby boosting demand for innovative therapy devices. Technological advancements are revolutionizing the sector, with a notable trend towards intelligent and connected wound care devices. This includes the development of biosensors for real-time wound monitoring, smart dressings that adapt to wound conditions, and negative pressure wound therapy (NPW) systems with enhanced efficacy and ease of use. The integration of artificial intelligence (AI) for predictive wound healing and personalized treatment plans is also gaining traction.

Consumer preferences are increasingly leaning towards minimally invasive and patient-friendly treatments that can be administered in homecare settings, reducing hospitalizations and associated costs. This shift is fueling the demand for portable, user-friendly, and effective wound therapy devices suitable for domiciliary care. Furthermore, there is a growing emphasis on evidence-based medicine and cost-effectiveness, pushing manufacturers to demonstrate the clinical and economic benefits of their products. The competitive landscape is intensifying, with both established global players and emerging regional companies vying for market share. This competition spurs continuous innovation and drives down costs, making advanced wound care more accessible. The market penetration of advanced wound care devices is steadily increasing as healthcare providers and payers recognize their value in improving patient outcomes and reducing the overall burden of wound care. The Compound Annual Growth Rate (CAGR) for the Europe Wound Therapy Devices Industry is projected to be between 6.5% and 8.0% over the forecast period of 2025–2033, indicating a healthy expansionary phase. Key market penetration metrics for advanced wound dressings and NPW systems are expected to rise significantly, particularly in countries with high chronic disease burdens.

Dominant Markets & Segments in Europe Wound Therapy Devices Industry

The Europe Wound Therapy Devices Industry exhibits distinct regional and segmental dominance, underscoring key market dynamics. Europe as a whole represents a leading market due to its advanced healthcare infrastructure, high disposable income, and a significant aging population prone to chronic wounds. Within Europe, countries like Germany, the United Kingdom, and France are dominant markets, driven by strong healthcare spending, well-established reimbursement policies, and a high concentration of specialized wound care centers. Economic policies in these nations often favor investment in advanced medical technologies, further bolstering the market for innovative wound therapy devices. Infrastructure development, including robust hospital networks and expanding homecare services, also plays a critical role in ensuring market penetration and accessibility.

Product Segmentation Dominance:

- Single-Use Device: This segment is experiencing significant growth and dominance, driven by the increasing emphasis on infection control, patient safety, and the convenience offered by disposable solutions. The demand for single-use NPW devices and advanced dressings is particularly high.

- Key Drivers: Enhanced hygiene, reduced cross-contamination risks, ease of use, and a preference for sterile, ready-to-use products in hospital and homecare settings.

- Re-Usable Device: While still holding a market share, this segment is relatively less dominant compared to single-use devices, especially in advanced wound care applications.

- Key Drivers: Cost-effectiveness in certain settings, established protocols in some healthcare facilities, and specialized applications where re-usability is managed under strict sterilization protocols.

Wound Type Dominance:

- Diabetic Foot Ulcer (DFU): This is a leading wound type driving market demand, attributed to the global epidemic of diabetes and the severe complications associated with foot ulcers, requiring specialized therapeutic interventions.

- Key Drivers: High prevalence of diabetes, long healing times, risk of amputation, and the need for advanced wound dressings and NPW therapy for effective management.

- Pressure Ulcer: Another highly prevalent wound type, particularly in elderly and immobile patient populations, contributing significantly to market growth.

- Key Drivers: Aging population, long-term care facilities, immobility, and the necessity for effective preventative and treatment strategies.

- Venous Leg Ulcer (VLU): This segment also represents a substantial market share due to the prevalence of chronic venous insufficiency, especially among older adults.

- Key Drivers: Chronic nature of VLUs, long treatment durations, and the need for advanced compression therapies and wound dressings.

End-User Dominance:

- Hospital: Hospitals remain a dominant end-user segment, as they are central to the diagnosis, treatment, and management of complex wounds, particularly those requiring advanced therapies and surgical interventions.

- Key Drivers: Availability of specialized medical personnel, advanced medical equipment, established protocols for wound care, and reimbursement structures for advanced treatments.

- Homecare: This segment is rapidly growing and gaining prominence, driven by the trend towards deinstitutionalization, cost containment in healthcare, and the demand for convenient, at-home wound management solutions.

- Key Drivers: Patient preference for home-based care, reduction in healthcare costs, availability of portable and user-friendly devices, and support from home nursing services.

Europe Wound Therapy Devices Industry Product Developments

Product developments in the Europe Wound Therapy Devices Industry are rapidly advancing, focusing on enhancing efficacy, patient comfort, and ease of use. Key innovations include the introduction of smart dressings embedded with sensors for real-time monitoring of wound exudate, pH, and temperature, enabling proactive treatment adjustments. Negative Pressure Wound Therapy (NPW) systems are becoming more sophisticated, with smaller, portable, and user-friendly designs suitable for homecare settings. Furthermore, there's a growing integration of advanced materials like silver-infused dressings for antimicrobial properties and hyaluronic acid-based products to promote cellular regeneration. These developments aim to reduce healing times, minimize pain, and improve patient outcomes, giving manufacturers a competitive edge in a dynamic market.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Europe Wound Therapy Devices Industry, encompassing detailed segmentation across key areas. The market is segmented by Product into Re-Usable Devices and Single-Use Devices. The Single-Use Device segment is expected to exhibit higher growth due to its advantages in infection control and convenience, with projected market sizes in the billions of Euros and a strong CAGR. The Re-Usable Device segment, while mature, will continue to hold a significant share, particularly in cost-sensitive markets or for specialized applications.

Further segmentation is based on Wound Type, including Diabetic Foot Ulcer, Pressure Ulcer, Venous Leg Ulcer, Burn Wounds, and Others. The Diabetic Foot Ulcer and Pressure Ulcer segments are anticipated to drive substantial market value and growth, reflecting the increasing prevalence of these conditions. Burn Wounds and Others also represent significant markets with specific therapeutic needs.

The End-User segmentation includes Hospitals, Homecare, and Others. The Hospital segment remains a dominant force, with substantial market size and consistent growth driven by complex wound management. The Homecare segment is poised for rapid expansion, fueled by patient preference and cost-saving initiatives, with projected market sizes reaching hundreds of millions to billions of Euros and a high CAGR.

Key Drivers of Europe Wound Therapy Devices Industry Growth

The growth of the Europe Wound Therapy Devices Industry is propelled by several key factors. Firstly, the escalating prevalence of chronic diseases like diabetes and the aging global population are directly increasing the incidence of chronic wounds such as diabetic foot ulcers and pressure ulcers, thereby creating a sustained demand for advanced wound care solutions. Secondly, continuous technological innovation, including the development of smart dressings, advanced NPW systems, and novel biomaterials, is enhancing treatment efficacy and patient outcomes, leading to greater adoption of these devices. Thirdly, favorable reimbursement policies and government initiatives in many European countries that promote wound management and reduce healthcare costs encourage investment and the use of advanced wound therapy devices. Finally, the growing awareness among healthcare professionals and patients about the benefits of advanced wound care over traditional methods contributes significantly to market expansion.

Challenges in the Europe Wound Therapy Devices Industry Sector

Despite its strong growth trajectory, the Europe Wound Therapy Devices Industry faces several challenges. Regulatory hurdles and stringent approval processes for novel medical devices can significantly prolong time-to-market and increase development costs, particularly for innovative technologies. High cost of advanced wound therapy devices compared to traditional treatments can be a barrier to adoption, especially in resource-constrained healthcare systems or for a large number of patients. Lack of standardized reimbursement policies across different European countries can lead to disparities in access and adoption rates. Furthermore, supply chain disruptions, as witnessed in recent global events, can impact the availability of raw materials and finished products, affecting market stability. Intense competition from both established players and emerging companies necessitates continuous innovation and cost management to maintain market share.

Emerging Opportunities in Europe Wound Therapy Devices Industry

The Europe Wound Therapy Devices Industry presents several promising emerging opportunities. The increasing focus on personalized medicine and digital health is driving the development of smart wound devices with integrated sensors and AI capabilities for real-time monitoring and predictive analytics, offering tailored treatment strategies. The growing demand for homecare solutions due to an aging population and the desire for patient convenience presents a significant opportunity for portable, user-friendly, and effective wound therapy devices that can be managed outside traditional healthcare settings. Expansion into emerging European markets with improving healthcare infrastructure and increasing disposable incomes offers untapped potential for market growth. Moreover, the development of novel biologics and regenerative medicine approaches in conjunction with advanced devices can create synergistic treatment modalities, opening new avenues for innovation and market penetration.

Leading Players in the Europe Wound Therapy Devices Industry Market

- DeRoyal Industries Inc

- Carilex Medical

- Talley Group Limited

- Smith & Nephew plc

- Medela AG

- 3M (Acelity L P Inc )

- Cardinal Health Inc

- ConvaTec Inc

- Molnlycke Health Care AB

Key Developments in Europe Wound Therapy Devices Industry Industry

- May 2023: Smith+Nephew announced in London that its PICO Single Use Negative Pressure Wound Therapy Systems have received an Innovative Technology contract from Vizient, Inc. The contract was awarded based on the PICO Single Use Negative Pressure Wound Therapy Systems recommendation by hospital experts who serve on one of Vizient's member-led councils.

- June 2022: Healiva, a Switzerland-based company that provides patients with chronic and acute wounds with life-improving precision medicine, acquired two innovative cell therapy assets from Smith&Nephew. The acquisition allowed Healiva to establish one of the world's broadest portfolios of affordable, personalized, end-to-end wound care consisting of enzyme technology, autologous & allogenic cell therapies, and medical devices, including negative pressure wound therapy devices.

Strategic Outlook for Europe Wound Therapy Devices Industry Market

The strategic outlook for the Europe Wound Therapy Devices Industry is highly positive, driven by a sustained increase in demand for advanced and innovative solutions. Key growth catalysts include the ongoing technological advancements leading to more intelligent and patient-centric devices, coupled with the expanding adoption of homecare wound management models. Companies focusing on product differentiation through enhanced efficacy, reduced invasiveness, and improved user experience will likely gain a competitive advantage. Strategic partnerships and collaborations, especially those that integrate digital health technologies with traditional wound care, are expected to play a crucial role in market expansion. Furthermore, addressing the cost-effectiveness of advanced therapies and navigating evolving regulatory landscapes will be critical for long-term success, ensuring broader access and continued market growth.

Europe Wound Therapy Devices Industry Segmentation

-

1. Product

- 1.1. Re-Usable Device

- 1.2. Single-Use Device

-

2. Wound Type

- 2.1. Diabetic Foot Ulcer

- 2.2. Pressure Ulcer

- 2.3. Venous Leg Ulcer

- 2.4. Burn Wounds

- 2.5. Others

-

3. End-User

- 3.1. Hospital

- 3.2. Homecare

- 3.3. Others

Europe Wound Therapy Devices Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Wound Therapy Devices Industry Regional Market Share

Geographic Coverage of Europe Wound Therapy Devices Industry

Europe Wound Therapy Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Number of Accidents and Traumatic Events; Rising Chronic Wounds Such as Diabetic Foot Ulcers; Technological Advancements in the NPWT Devices

- 3.3. Market Restrains

- 3.3.1. High Cost of Device and Treatment; Complications Associated With NPWT Device

- 3.4. Market Trends

- 3.4.1. Diabetic Foot Ulcers Segment is Expected to Witness Significant Growth Over The Forecast Period.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Re-Usable Device

- 5.1.2. Single-Use Device

- 5.2. Market Analysis, Insights and Forecast - by Wound Type

- 5.2.1. Diabetic Foot Ulcer

- 5.2.2. Pressure Ulcer

- 5.2.3. Venous Leg Ulcer

- 5.2.4. Burn Wounds

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Hospital

- 5.3.2. Homecare

- 5.3.3. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Germany Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Re-Usable Device

- 6.1.2. Single-Use Device

- 6.2. Market Analysis, Insights and Forecast - by Wound Type

- 6.2.1. Diabetic Foot Ulcer

- 6.2.2. Pressure Ulcer

- 6.2.3. Venous Leg Ulcer

- 6.2.4. Burn Wounds

- 6.2.5. Others

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. Hospital

- 6.3.2. Homecare

- 6.3.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. United Kingdom Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Re-Usable Device

- 7.1.2. Single-Use Device

- 7.2. Market Analysis, Insights and Forecast - by Wound Type

- 7.2.1. Diabetic Foot Ulcer

- 7.2.2. Pressure Ulcer

- 7.2.3. Venous Leg Ulcer

- 7.2.4. Burn Wounds

- 7.2.5. Others

- 7.3. Market Analysis, Insights and Forecast - by End-User

- 7.3.1. Hospital

- 7.3.2. Homecare

- 7.3.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. France Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Re-Usable Device

- 8.1.2. Single-Use Device

- 8.2. Market Analysis, Insights and Forecast - by Wound Type

- 8.2.1. Diabetic Foot Ulcer

- 8.2.2. Pressure Ulcer

- 8.2.3. Venous Leg Ulcer

- 8.2.4. Burn Wounds

- 8.2.5. Others

- 8.3. Market Analysis, Insights and Forecast - by End-User

- 8.3.1. Hospital

- 8.3.2. Homecare

- 8.3.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Italy Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Re-Usable Device

- 9.1.2. Single-Use Device

- 9.2. Market Analysis, Insights and Forecast - by Wound Type

- 9.2.1. Diabetic Foot Ulcer

- 9.2.2. Pressure Ulcer

- 9.2.3. Venous Leg Ulcer

- 9.2.4. Burn Wounds

- 9.2.5. Others

- 9.3. Market Analysis, Insights and Forecast - by End-User

- 9.3.1. Hospital

- 9.3.2. Homecare

- 9.3.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Spain Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Re-Usable Device

- 10.1.2. Single-Use Device

- 10.2. Market Analysis, Insights and Forecast - by Wound Type

- 10.2.1. Diabetic Foot Ulcer

- 10.2.2. Pressure Ulcer

- 10.2.3. Venous Leg Ulcer

- 10.2.4. Burn Wounds

- 10.2.5. Others

- 10.3. Market Analysis, Insights and Forecast - by End-User

- 10.3.1. Hospital

- 10.3.2. Homecare

- 10.3.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Rest of Europe Europe Wound Therapy Devices Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Re-Usable Device

- 11.1.2. Single-Use Device

- 11.2. Market Analysis, Insights and Forecast - by Wound Type

- 11.2.1. Diabetic Foot Ulcer

- 11.2.2. Pressure Ulcer

- 11.2.3. Venous Leg Ulcer

- 11.2.4. Burn Wounds

- 11.2.5. Others

- 11.3. Market Analysis, Insights and Forecast - by End-User

- 11.3.1. Hospital

- 11.3.2. Homecare

- 11.3.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2025

- 12.2. Company Profiles

- 12.2.1 DeRoyal Industries Inc

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Carilex Medical

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Talley Group Limited

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Smith & Nephew plc

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Medela AG

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 3M (Acelity L P Inc )

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Cardinal Health Inc

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 ConvaTec Inc

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Molnlycke Health Care AB

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.1 DeRoyal Industries Inc

List of Figures

- Figure 1: Europe Wound Therapy Devices Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Wound Therapy Devices Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 4: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 5: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 7: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 10: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 11: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 12: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 13: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 14: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 15: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 18: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 19: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 20: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 21: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 22: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 23: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 26: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 27: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 28: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 29: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 30: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 31: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 33: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 34: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 35: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 36: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 37: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 38: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 39: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 42: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 43: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 44: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 45: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 46: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 47: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 49: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 50: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 51: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Wound Type 2020 & 2033

- Table 52: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Wound Type 2020 & 2033

- Table 53: Europe Wound Therapy Devices Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 54: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by End-User 2020 & 2033

- Table 55: Europe Wound Therapy Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Europe Wound Therapy Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Wound Therapy Devices Industry?

The projected CAGR is approximately 5.06%.

2. Which companies are prominent players in the Europe Wound Therapy Devices Industry?

Key companies in the market include DeRoyal Industries Inc , Carilex Medical, Talley Group Limited, Smith & Nephew plc, Medela AG, 3M (Acelity L P Inc ), Cardinal Health Inc, ConvaTec Inc, Molnlycke Health Care AB.

3. What are the main segments of the Europe Wound Therapy Devices Industry?

The market segments include Product, Wound Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.89 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Number of Accidents and Traumatic Events; Rising Chronic Wounds Such as Diabetic Foot Ulcers; Technological Advancements in the NPWT Devices.

6. What are the notable trends driving market growth?

Diabetic Foot Ulcers Segment is Expected to Witness Significant Growth Over The Forecast Period..

7. Are there any restraints impacting market growth?

High Cost of Device and Treatment; Complications Associated With NPWT Device.

8. Can you provide examples of recent developments in the market?

May 2023: Smith+Nephew announced in London that its PICO Single Use Negative Pressure Wound Therapy Systems have received an Innovative Technology contract from Vizient, Inc. The contract was awarded based on the PICO Single Use Negative Pressure Wound Therapy Systems recommendation by hospital experts who serve on one of Vizient's member-led councils.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Wound Therapy Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Wound Therapy Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Wound Therapy Devices Industry?

To stay informed about further developments, trends, and reports in the Europe Wound Therapy Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence